The Predicament and Choices of MakerDAO: Losses, Regulation, MetaDAO

According to revenue data, MakerDAO incurs an annual loss of approximately 9.4 million dollars.

According to revenue data, MakerDAO incurs an annual loss of approximately 9.4 million dollars.Author: PANews

The reality of DeFi protocols may not be as glamorous as the surface data suggests. Our impression of MakerDAO might include: a long-term TVL at the top, DAI as an important DeFi infrastructure, and MakerDAO relying on stable fee income to buy back and burn MKR. But who would have thought that the most representative DeFi protocol, MakerDAO, has also fallen into a quagmire.

The Predicament of MakerDAO

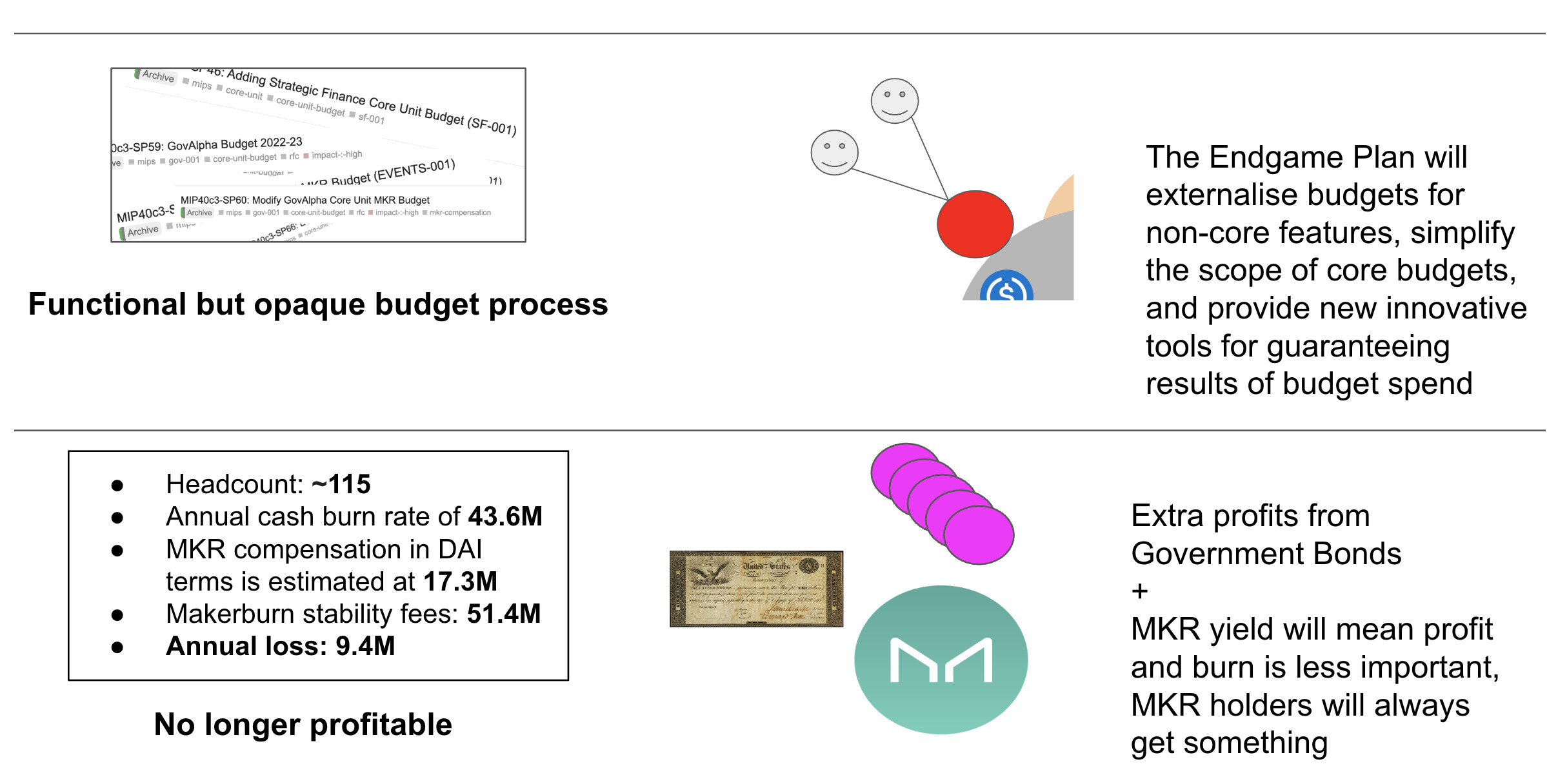

According to MakerDAO's revenue data, the annual stable fee income is about $51.4 million. However, beyond the apparent income, maintaining this large and complex governance machine requires 115 employees, consuming $43.6 million in cash annually, with MKR compensation in DAI amounting to about $17.3 million. These payment costs have already exceeded MakerDAO's stable fee income, resulting in an annual loss of about $9.4 million.

MakerDAO co-founder Rune Christensen recognized this issue in May this year and formally proposed an Endgame Plan in June, hoping to simplify the complexity in governance. Rune's signature has also changed to "currently engaged in some new projects and contributing to Maker as a community member."

After Tornado Cash was sanctioned, USDC issuer Circle actively cooperated with the U.S. Treasury's sanctions, while the Peg Stability Module (PSM) in the Maker protocol holds over $3 billion in USDC, with USDC accounting for more than half of all collateral in Maker. This requires the Endgame Plan to address security issues from regulation simultaneously.

Governance Reform: MetaDAO

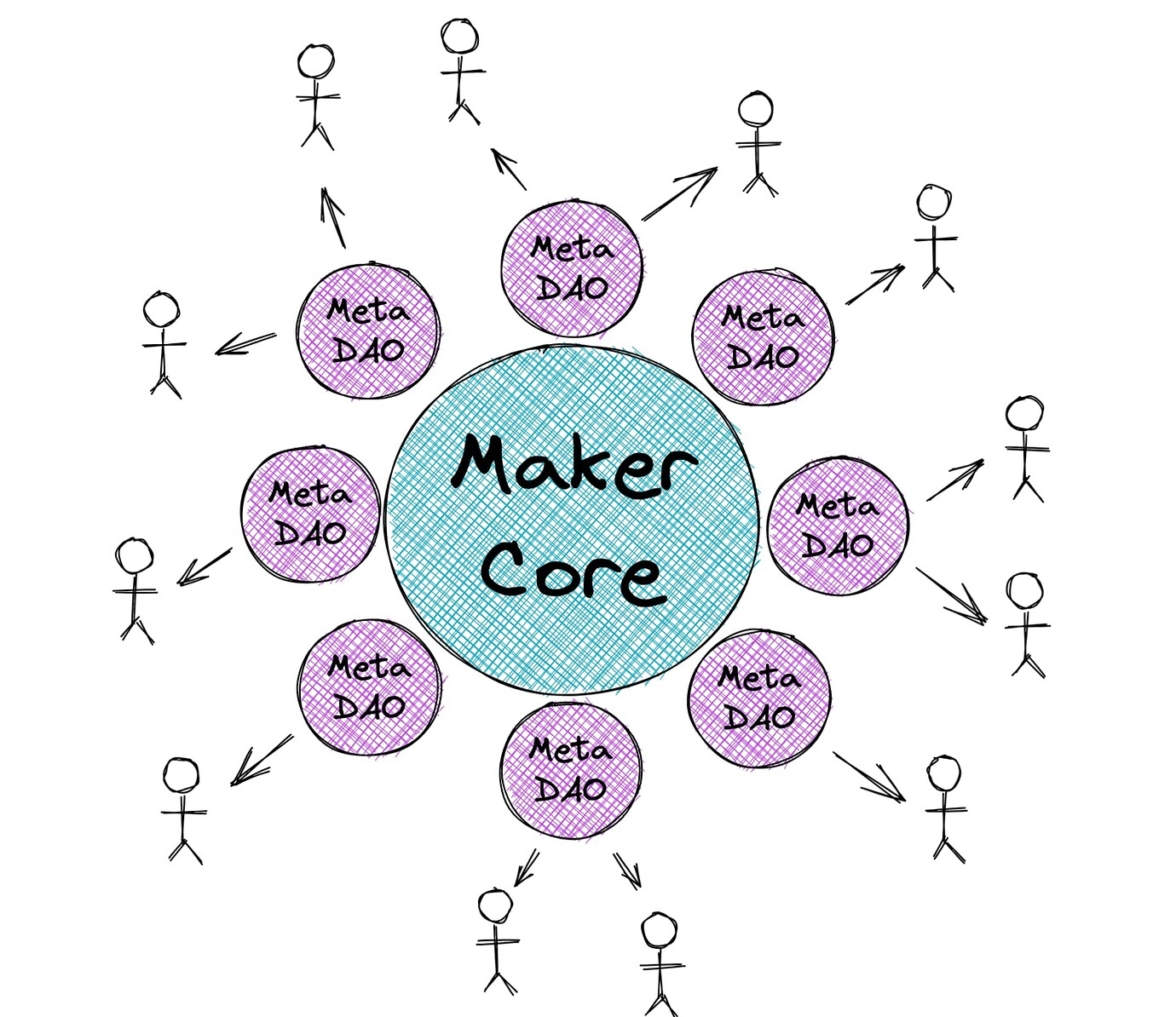

The existing governance process is overly complex, hindering MakerDAO's speed in developing new features; on the other hand, it relies on a large human workforce, which has become the main reason for MakerDAO's losses in the bear market. As an important component of the Endgame Plan, MetaDAO aims to accelerate the governance process, reduce MakerDAO's labor costs, isolate risks, and parallelize the highly complex governance processes.

Similar to the mainstream "modular" approach in blockchain today, the complex governance of MakerDAO is broken down into smaller pieces, namely individual MetaDAOs, each of which can focus on its own tasks without being distracted by other responsibilities. For example, a MetaDAO focused on creation will recruit developers to build front-end products and on-chain functions; a MetaDAO focused on RWA (Real World Assets) will be responsible for managing RWA Vaults. This also overcomes the current single-threaded issue in Maker governance, achieving a multi-centered governance structure that allows MetaDAOs to execute in parallel, speeding up the governance process.

Maker can create new MetaDAOs by deploying new ERC20 tokens. Ideally, the final Maker Core only needs to support collaborative MetaDAOs, while the specific work will be done by individual MetaDAOs, alleviating the burden on MakerDAO. Some members of the Meta Core will also be reorganized into Meta DAOs, reducing MakerDAO's labor cost expenditure by half.

Comparing MakerDAO and MetaDAO is like the relationship between Layer 1 and Layer 2; Maker governance can be seen as a slow, expensive but more secure "governance Layer 1," while MetaDAO is like a fast and flexible "governance Layer 2," but the ultimate security is elevated to Maker governance.

MetaDAOs are independent of each other, with their own governance tokens and governance processes, needing to earn their own revenue. According to Rune's description in the "Endgame Plan v3 Complete Overview," MetaDAO tokens (MDAO) will be distributed through mining, with 20% allocated to DAI farms, 40% to ETHD farms, and 40% to MKR farms, to promote decentralized collateral entry.

Path to Achieving Decentralization

MakerDAO primarily increases its degree of decentralization through the following paths, focusing on increasing the use of decentralized collateral and accumulating decentralized assets owned by the protocol through protocol income.

- Increase the use of ETH collateral

After Tornado Cash was sanctioned by the U.S. Treasury, Maker has taken a series of measures to reduce its dependence on USDC.

For instance, raising the debt ceiling of the WSTETH-B Vault and lowering the stable fee to zero, as well as reducing the stable fees for ETH-A, ETH-B, WSTETH-A, WBTC-A, WBTC-B, and RENBTC-A Vaults.

Lowering the funding rates of other Vaults may reduce the demand for minting DAI using USDC through the PSM.

- Introduce EtherDai

The introduction of EtherDai aims to have staked ETH under the control of Maker governance, including ETHD and EtherDai Vaults. ETHD is a wrapper around Lido's Staked ETH (stETH) (similar to wstETH). Users can wrap stETH into ETHD or redeem ETHD back to stETH. The emergence of ETHD and wstETH may be because Lido distributes staking rewards through rebase, where users holding stETH see their balance continuously increase, but it may be inconvenient to use in certain scenarios.

Maker governance will have backdoor access to ETHD collateral, potentially incentivizing liquidity by setting up short-term liquidity mining for ETHD/DAI on Uniswap. On the other hand, the stable fee for the EtherDai Vault may be set to zero to guide demand for the EtherDai Vault.

- Adjust the use of Real World Assets (RWA)

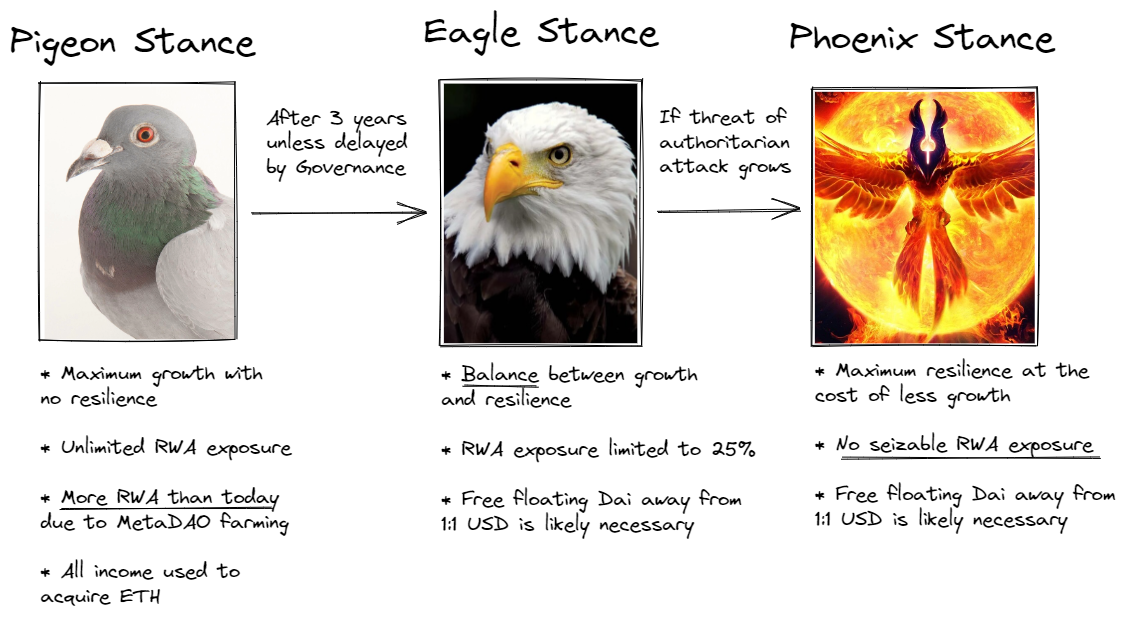

The Endgame Plan proposes three different collateral strategies: dovish, hawkish, and phoenix, progressively advancing over time based on regulatory threats.

First is the dovish strategy, where the main task during this period is to increase RWA as much as possible and maintain rapid growth. Since RWA collateral can bring relatively higher stable fees to Maker, Maker aims to maximize profits during this period to exchange for ETH.

After three years, if DAI begins to face authoritative attacks, and RWA collateral risks being confiscated, the strategy will switch to hawkish, limiting exposure to RWA risks to 25% to seek a balance between performance growth and resilience.

If there is evidence that authoritative attacks are imminent or all RWA collateral has been confiscated, the strategy will shift to the phoenix strategy, eliminating all RWA risk exposure, allowing only RWA that cannot be controlled by authoritative institutions to be used as collateral.

Starting from the hawkish strategy, if there is a risk of RWA being confiscated, it becomes necessary to allow DAI to decouple from the dollar and become a freely floating asset.

The rationale for adopting this development path is that regulation may become stricter, and the degree of threat to RWA collateral from authoritative institutions increases over time. Meanwhile, MakerDAO can utilize the current time window to expand the market and accumulate assets as much as possible.

- Protocol-owned Vault

When users stake assets in Maker to borrow DAI, a Vault is created. The Peg Stability Module does not differentiate between users, has no stable fee, cannot be liquidated, and can be seen as a special Vault.

Protocol-owned Vaults will help MakerDAO accumulate more ETH. The plan is to use the surplus of 40 million DAI to acquire Staked ETH with 2x leverage. This means that there will be $80 million worth of Staked ETH earning revenue, and the surplus will also be placed in the protocol-owned Vault. As Ethereum completes its transition to PoS, MakerDAO can gain an additional source of staking income.

In the Short Term, DAI Will Still Be Pegged to the Dollar

According to the current plan, DAI will remain pegged to the dollar for a considerable period. Rune also explained on his Twitter that he believes "converting all stablecoin collateral to ETH is a bad idea."

MakerDAO is still leveraging the assets in the PSM to increase its influence, as two aggregation DEXs, 1inch and Paraswap, have already integrated the PSM, allowing large transactions between USDC and DAI to go directly through Maker's PSM, with no trading slippage and no transaction fees.

Rune's timeline for the Endgame Plan published on the MakerDAO governance forum on August 30 also indicates that DAI will maintain its peg to the dollar for at least three years, and this timeframe will be extended if there is no direct threat. If the degree of decentralization of collateral can be increased to 75%, then the peg to the dollar will be maintained indefinitely.

Conclusion

In the short term, DAI will still be pegged to the dollar, and Maker's current primary task is to continue expanding its business and accumulating assets. The reform of governance through MetaDAO may primarily aim to reduce MakerDAO's large labor costs during the bear market and also improve the efficiency of subsequent work.

Regulatory pressure may not arrive quickly, providing a time window to seize opportunities for development. When regulatory pressure truly arrives, MakerDAO's plan is to achieve censorship resistance in the medium to long term while remaining pegged to the dollar.