As the Ethereum merge approaches, how are DeFi leaders affected and what preparations are they making?

Involving Lido, Aave, Compound, Bancor, Synthetix, Frax, Maker, etc.

Involving Lido, Aave, Compound, Bancor, Synthetix, Frax, Maker, etc.Original authors: Akhil Vajjhala & Jack, Polygon

Original title: 《What's Up With DeFi Before Merge? A Compilation of all the Important Findings from Different DeFi Forums》

*Compiled by: Katie Gu, * Odaily Planet Daily

The merge will significantly change how Ethereum operates, its environmental impact, and its narrative. With this hard fork, Ethereum will run on the new consensus mechanism PoS instead of the original PoW. In this article, we will introduce the important events that occurred in various DeFi governance forums as the merge approaches.

Lido Staking

Lido provides liquid staking for ETH holders who wish to earn rewards by staking ETH2.0, without needing to hold the 32 ETH required to run a full node to stake their assets. Lido lowers the barrier for staking ETH and offers stETH (a liquid derivative of staked ETH), allowing users to utilize it in other DeFi protocols.

When discussing the Ethereum merge, Lido is one of the most important components. It involves the process of liquid staking and plays a crucial role when it comes to the impact of the merge on ETH stakers in PoS.

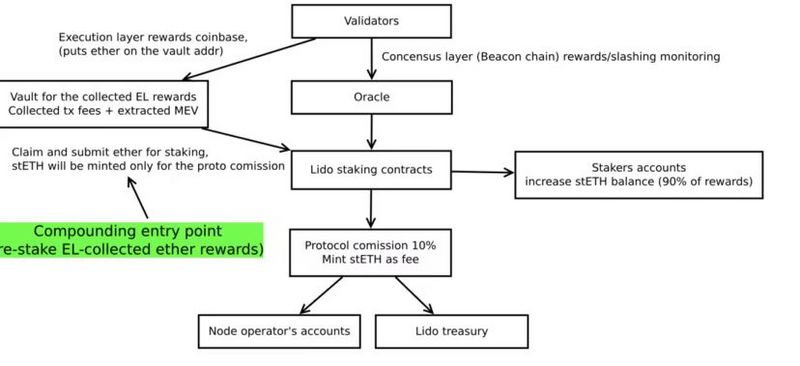

Lido protocol upgrade to reset newly emerged rewards post-Ethereum merge, achieving multiple rewards.

(On-chain portion of reward distribution post-merge)

The proposal suggests reallocating all collected execution layer rewards while generating protocol fees (0%) stETH as part of the beacon chain reward distribution operation. However, the non-profit Lido oracle reports do not charge/distribute any protocol fees.

The distribution mechanism is as follows:

Node operators collect ETH designated execution layer rewards on a dedicated treasury contract. Specifically, MEV rewards can be obtained in such treasury contracts.

Lido contracts withdraw all collected rewards from the treasury, re-stake them, and only distribute protocol fees (10%) as part of the beacon chain (or consensus layer) reward distribution operation, minting new stETH.

If it is a non-profit Lido oracle report, no new stETH will be minted (i.e., protocol fees).

This proposal will bring multiple returns, with minimal impact on the existing distribution scheme and fast transaction times. It is also quite automated and autonomous. Finally, in the event of a delay in the merge hard fork, it will revert to the already adopted solution.

Main goal: To measure whether clients continue to generate more block proposer rewards.

Airdrop fork tokens and maintain peg: If there are any airdropped ETH PoW to ETH stakers, it will return to potential holders of stETH.

AAVE Lending

AAVE is a decentralized lending market where lending yields are based on utilization (borrowed amount/deposited amount).

Considering that the merge is a perfect opportunity for a PoW airdrop or just hoping the merge is not yet priced in, leveraging your position and increasing your ETH holdings seems to be the choice of most crypto investors.

However, there are many issues in this regard:

If there are any merge-related issues > ETH price drops -> mass liquidations occur.

Aave lends users collateral > merge issues > both Aave and users are severely affected.

Aave's borrowing limits have been reduced, fees have increased, until ETH borrowing is completely paused until the merge is completed.

Technical analysis of Aave's impact from Ethereum PoS merge:

Claims that the merge should not affect AAVE's system.

Block structure: unaffected.

Block time: only Aave governance is slightly affected (voting duration).

Smart contracts: Aave is unaffected.

On-chain randomness sources: unaffected.

New concepts of safe head and final block (potential changes in Ethereum finality): Aave may be slightly affected but will not impact smart contracts.

Chainlink's stance will align with the PoS chain. Chainlink will not integrate into the Ethereum PoW fork; it will fully commit to the PoS chain, ensuring that oracles and data have no issues.

AAVE ETH PoW fork risk mitigation plan:

Aside from ETH, most tokens may be worthless on the ETH PoW chain. Therefore, the strategy that users may adopt to maximize their crypto asset holdings may be to borrow as much ETH as possible (mainly collateralized by stablecoins or other tokens).

Additionally, the flow from stETH holders to ETH should be monitored, as stETH may also be worthless on the ETH PoW chain.

Speculative strategies related to the PoS merge and potential ETH PoW fork may impact Aave, especially since Aave allows borrowing ETH from stETH. Using stETH to collateralize and borrow ETH on Aave has become a popular strategy, raising the utilization rate of the ETH market to 62%.

Speculators are leveraging ETH market-related risks:

High utilization of ETH may make liquidations more difficult or impossible.

In a heavily utilized ETH market, due to the merge event, the market may start to experience high volatility, making it difficult to liquidate regular ETH long/stablecoin short positions.

This is because liquidators will not be able to obtain ETH as collateral since most ETH will be borrowed.

This may lead to some positions becoming uncollateralized.

High ETH utilization raises the ETH rate to a level where the APY for ETH/th positions is negative.

High ETH utilization will raise the ETH rate to a level where ETH/ETH positions generate negative APY.

Once the ETH borrowing rate reaches 5%, this occurs shortly after 70% utilization (we are currently at 63%), stETH/ETH positions begin to become unprofitable.

Currently, due to depreciation risks, borrowers on Aave are not maximizing their leverage. Therefore, it is possible that some positions will show negative APY earlier. This will lead to users closing positions until the ETH borrowing rate stabilizes, making APY steady.

This means we will see a large amount of stETH redeemed for ETH, further driving down the price of stETH, as regular stETH holders turn to ETH to gain the benefits of ETH PoW work.

Already high ETH utilization has led regular ETH suppliers to start withdrawing their ETH.

Due to uncertainties and risks associated with the ETH PoW fork (typically the PoS merge, especially ETH usage on Aave), current liquidity providers may become increasingly concerned about their ETH on Aave, potentially leading to withdrawals from the supply side.

The increase in utilization is unrelated to ETH borrowers.

Furthermore, if the ETH price drops, ETH long/stablecoin short positions may need to deleverage by selling supplied ETH.

This is why ETH borrowing is frozen.

Alternative: Increase the variable borrowing annual interest rate from 103% to 1000% under 100% utilization.

AAVE DAO's stance on ETH PoW fork:

Aave's request for comments on Aave governance (ARC) requires Aave DAO to commit to choosing to operate the Ethereum mainnet under proof of stake consensus rather than running any Ethereum branch under alternative consensus (such as proof of work).

ARC will formally state that Aave DAO deployments will only occur on Ethereum PoS.

Authorize community guardians to take necessary actions to shut down Aave deployments on any forks generated by the Ethereum Paris hard fork (merge).

AAVE Snapshot Voting:

- Propose to limit ETH borrowing close to the merge.

Compound Lending

The Compound lending market is very similar to AAVE, but with fewer assets available for borrowing. It only exists on Ethereum, while AAVE has moved towards multi-chain.

Adjusting ETH interest rate model:

Update the cETH interest rate model to a new jump rate model with the following parameters:

Rate at 0% utilization: 2%

Optimal utilization (knee point): 80%

Optimal utilization: 20%

100% utilization: 1000%

Set a borrowing cap of 100,000 ETH for the cETH market.

Bancor DEX

Bancor is a decentralized exchange that allows users to trade between tokens. Its unique value proposition is the ability to provide liquidity to the DEX through its native BNT token without facing impermanent loss; however, due to poor performance in the recent bear market, users have indeed faced impermanent loss, and this capability has recently come under fire.

Proposal: Determine the operation of the Bancor governance forum during the fork:

Propose to disable Bancor contracts on all PoW forks.

Disable contracts: This option will include disabling all Bancor platform functionalities on the Ethereum branch. This choice should pose no risk. The main argument against this is that most tokens on the proof of work fork will soon become worthless, leading to the Bancor platform being drained of any value that can be extracted on the fork chain.

No action taken: In the case of an Ethereum fork, no action will be taken. This will not pose any risk to Bancor on the Ethereum mainnet; however, any value that could be extracted from the Ethereum fork will be lost quickly.

Synthetix Derivatives

Synthetix will pause all Synthetix contracts on Ethereum and Optimism approximately 3 hours before the anticipated merge block and will resume activity once the Chainlink information flow and other parts of the protocol are stable.

SNX tokens will still be tradable, but all other parts of the protocol, such as synthetic exchanges, futures, loans, staking (claiming, minting, burning), and cross-chain bridges will be paused. Once the pause is complete, communication will be made through all channels, and all protocol partners will be notified.

Frax Stablecoin

FRAX stablecoin can only be redeemed on ETH PoS:

Sam Kazemian (founder of FRAX) submitted a proposal requiring that the project's stablecoin can only be redeemed on the Ethereum proof of stake (PoS) mainnet.

FRAX will reject any Ethereum PoW forks.

While this is a step towards the future of Ethereum PoS, it may create FUD among Ethereum PoW users.

MakerDAO Stablecoin & Lending

Overview of risks and market impacts ------ futures spot premium and negative financing:

Holding ETH in spot will receive any PoW fork tokens, while ETH quarterly futures or perpetual contracts will not. Assuming the market is efficient, this means that quarterly futures should start trading at an additional discount based on the expected value of PoW fork tokens after the anticipated merge date.

Recently, we have seen the quarterly forecast report for December 2022 shift from a premium to a spot premium, reflecting the possibility of PoW forks accumulating some "salable value." In practice, market participants can buy spot ETH and then sell an equivalent amount of ETH futures, staking the fork value while maintaining delta neutrality. As the anticipated date of the merge approaches, we may see some similar activity on perpetual contracts, with significant discounts and negative financing reflecting the expected value of PoW fork ETH.

Impact on Maker: The nominal leverage cost through futures contracts (excluding potential fork value) decreases, creating competitive pressure on the Maker vault. Users who believe the market implies too high a fork value will be incentivized to leverage on futures, while those who believe the implied value is lower may prefer to leverage using the Maker vault (where vault owners will still receive any potential fork tokens).

Reaction: Maintain competitive rates to avoid losing too much trading volume due to futures contracts.

stETH Value Decline:

stETH and other liquid staking assets are likely to become worthless on any PoW Ethereum fork.

Therefore, based on the expected value of ETH from the PoW fork, the market price of liquid staking assets may decline.

Reaction: Monitor stETH liquidity, adjust parameters as necessary (increase stability fees or liquidation ratios); use ETH collateral across DeFi lending protocols to monitor competitive rates.

External Asset Fork Options:

Ethereum hosts a variety of externally supported assets, including cross-chain bridges, centralized stablecoins, and real-world assets. Because these assets are supported by external collateral (either held off-chain or on another chain), they can only be fully staked on a single chain at a time, and issuers typically need to identify one chain as the normative chain during a fork.

The merge upgrade has received strong support from the Ethereum community, DeFi users, and protocols, which should help ensure that fork options consistently support the mainnet (PoS) Ethereum. However, due to financial exposure to miners or other reasons, one or more external asset issuers may acknowledge the PoW fork to some extent. This could render assets connected to the mainnet Ethereum worthless.

Due to potential financial ties with miners, Tether is particularly seen as a potential risk.

Impact on Maker: If all external supported asset issuers support the merge upgrade, the impact is minimal; if one or more issuers support the PoW fork, this could significantly affect DEX liquidity pools and other protocols accepting the asset as collateral.

Reaction: Confirm merge support from key external asset providers interacting with the Maker protocol, including: Circle, Paxos, Binance, Bitgo, Gemini, Centrifuge issuers, other RWA (real-world asset) issuers, and services connecting DAI to other chains, such as Wormhole, Axelar, Gravity Bridge, and Multichain.

Liquidity Pool Protocols:

Maker does not provide users with borrowable collateral, while many other lending protocols (including Aave, Compound, and Euler protocols) do. After the PoW fork, a significant subset of important assets on the fork chain (including stablecoins and cross-chain bridge assets) will immediately become worthless. This may lead to concentrated lending markets becoming insolvent and incentivize users to borrow all available ETH (as the asset most likely to retain some value in the fork).

Withdrawing ETH from liquidity protocols (especially Aave and Euler) may cause ETH borrowing costs to soar, putting pressure on leveraged stETH positions and potentially affecting parity with ETH prices.

Impact on Maker: Some users may migrate from external lending protocols to the Maker vault; ETH may be withdrawn from lending protocols, putting pressure on stETH; decentralized exchange liquidity for ETH may decline before and after the merge.

Reaction: Monitor user behavior and maintain competitive rates to facilitate any potential migration or user acquisition; monitor stETH leveraged positions and ETH borrowing utilization on Aave and Euler; monitor forex liquidity and consider parameter changes as necessary.

Oracle Networks and Indices:

Oracle networks like Maker and Chainlink are planning to support the merge and consider the mainnet Ethereum as the normative chain. However, the possibility of a PoW fork complicates this issue, increasing the likelihood of erroneous data due to potential centralization trading issues or code conflicts.

Impact on Maker: Increased likelihood of bad data/anomalous data being sent to oracle information streams; potential market disruptions due to bad price data included from third-party oracles or prepared indices.

Reaction: Confirm centralized trading plans, including PoW fork listings, quotes, and API changes; encourage industry participants to adopt alternative quotes for any PoW forks to avoid conflicts and ensure continuity of mainnet Ethereum data.

Network Downtime:

This merge can be considered the largest upgrade in Ethereum's history. With this significant protocol change, the risk of technical failures increases, potentially leading to activity failures and unavailability. If Ethereum experiences a downturn for a period, DeFi protocols like Maker may experience price gaps (discontinuous price drops) in collateral assets, which could lead to vault liquidations or even bankruptcy.

Impact on Maker: Increased risk of downtime and activity failures before and after the PoS merge; negative price spreads may occur during any network downtime; reduced ability for users to deleverage or protect their vault positions.

Reaction: Consider changing parameters to increase the safety margin of vault positions (e.g., increasing liquidation ratios, raising stability fees for high-leverage vault types); encourage users to increase their position safety margins before the merge upgrade.

Replay Attacks:

Replay attacks allow transactions or messages signed on one chain to be "replayed" on another chain under certain circumstances. Ethereum users (even custodians or infrastructure providers) may become victims of so-called "replay attacks" after the PoW Ethereum fork.

While EIP-155 provides a simple protection against transaction replay by adding Chain ID as a transaction signature parameter, it cannot guarantee that the PoW fork will adopt a different Chain ID from the Ethereum mainnet (Chain-ID 1).

Impact on Maker: Increased likelihood of unintended transactions on the mainnet being replayed from the PoW fork chain (e.g., closing vault positions, selling fork DAI or fork MKR tokens, etc.); likelihood of mainnet transactions, including Maker oracle and keeper operations, being replayed to the PoW fork chain.

Reaction: Share information about replay attack risks within the Maker community; advocate for PoW forks to use alternative Chain IDs (instead of the Chain-ID 1 that the mainnet Ethereum will continue to use) to avoid replaying transactions.

Risk warning

Risk warning Risk warning

Risk warning