Can the stablecoin GHO help the Aave protocol surpass MakerDAO and DAI?

Gain a deeper understanding of the design concept behind the GHO stablecoin.

Gain a deeper understanding of the design concept behind the GHO stablecoin.Original Title: 《Can Aave's GHO stablecoin help the protocol further grow and overtake MakerDAO and DAI?》

Original Author: tokenbrice

Original Compilation: PANews

A few weeks ago, the concept of the GHO stablecoin was proposed on the Aave governance forum, attracting significant attention across the DeFi industry. Undoubtedly, launching such a decentralized, collateral-backed, and USD-pegged native stablecoin for the Aave DAO makes a lot of sense as the next step in the development of the Aave protocol. PANews has also published an article introducing this proposal.

Before the Aave DAO and team bring GHO to market and establish it as an important stablecoin like DAI, let’s first take a look at the design philosophy behind this stablecoin. However, due to the currently limited information, the second part of this article mainly consists of some inferences based on experience in the DeFi industry.

1 What is Aave's native stablecoin GHO?

Since Aave is the preferred DeFi lending protocol for most borrowers, one of its initial goals was to attract a sufficient amount of stablecoin deposits. Subsequently, creating a DAO native stablecoin became a natural progression, as it could lower borrowing costs for users. Additionally, by minting stablecoins, depositors would not need to pay extra fees for annual yields.

Next, let’s delve into the main features of GHO proposed on the governance forum.

1.1 Over-collateralized USD-pegged stablecoin

GHO is an over-collateralized stablecoin minted using aTokens as collateral. In some sense, GHO is similar to MakerDAO, but it is slightly more efficient because all collateral is productive capital that generates interest (aTokens) — depending on borrowing demand.

Interestingly, Aave did not include the term "USD" in the name of this stablecoin. Given that U.S. regulators are generally aggressive, GHO likely aims to avoid unnecessary legal troubles. Furthermore, Aave founder Stani hinted that GHO might undergo a peg change in the future, explaining:

Long-term pegging to a specific currency is limiting; you might want to switch the peg from one underlying asset to another (for various reasons), and being tied to the USD will be a significant limiting factor. Most importantly, everyone has already done this, which seems a bit redundant and brings some restrictions. In fact, DAI has followed the same path and has been providing liquidity assets through USD pegging for years.

1.2 Interest rate model and staking discounts

The interest rate model may be the least impressive part of GHO so far. Aave's initial idea was for the Aave DAO to directly determine interest rates, similar to how Maker operates, but this approach is inefficient and adds unnecessary complications to governance. A more reasonable approach would be to use an interest rate model that adjusts based on market conditions and is determined algorithmically, just like other tokens on Aave, where interest rates are dictated by supply and demand in the pool.

Typically, DAOs are absolutely unsuitable for participating in the management of system operational parameters, as this would create a hybrid model with a fixed base interest rate that can only be adjusted within a certain range based on market conditions. Therefore, the idea of involving the DAO in determining interest rates is quite absurd.

In fact, dynamic changes in interest rates can protect GHO's peg by preventing large-scale minting events, similar to how the baseRate on the Liquity protocol can prevent LUSD from being pegged downwards. On the Liquity protocol, the initial fee is 0.5%, and as demand surges, the fee increases, gradually returning to 0.5% once demand stabilizes.

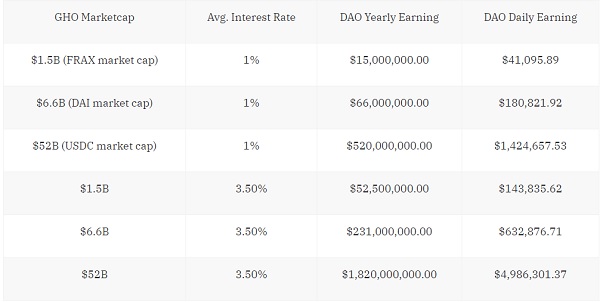

During this governance forum, Aave also mentioned the discount for GHO borrowers staking AAVE tokens, believing this would create further synergies. All interest paid by stakers will ultimately flow to the Aave DAO (most other tokens are in the range of 0-10%), which means that once GHO reaches a substantial market cap, it could become a cash cow for the DAO. With a market cap similar to DAI and a higher average interest rate of 3.5%, Aave DAO could earn nearly $150,000 daily from GHO.

The following chart provides interest rates and yield reference values corresponding to different GHO market caps:

Table Explanation:

GHO Market Cap: $1.5 billion = Current market cap of FRAX, $6.6 billion = Current market cap of DAI, $52 billion = Current market cap of USDC.

GHO Average Interest Rate: 1% represents highly competitive rates, while 3.5% represents quite high rates.

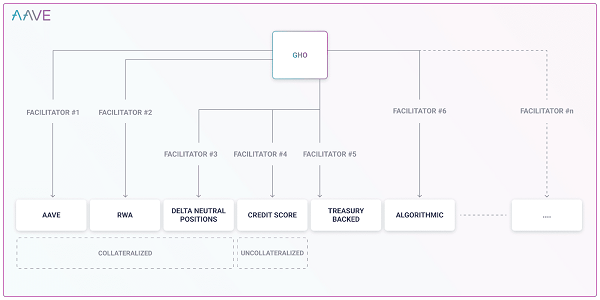

1.3 "Facilitators" and risk-weighted assets

In the design process of GHO, the team proposed the concept of "Facilitators." A "Facilitator" can mint GHO and is governed by Aave. The first "Facilitator" will be the Aave protocol itself, followed by other protocols or entities that will follow suit. This design significantly expands the GHO space, and it is expected that many other protocols will apply to become "Facilitators" on Aave and GHO after its launch, which is quite exciting to think about.

It is worth noting that the DAO will determine the maximum GHO minting capacity for each "Facilitator."

1.4 "Decentralization" and anti-censorship

The Aave team describes GHO as a decentralized stablecoin, even mentioning anti-censorship. However, this seems to have no direct connection to GHO:

As the integration of crypto assets with non-crypto native user groups continues, the adoption of stablecoins will keep growing. Decentralized stablecoins provide censorship-resistant fiat currency on the blockchain. GHO, a decentralized multi-collateral native stablecoin, is fully supported by the Aave protocol.

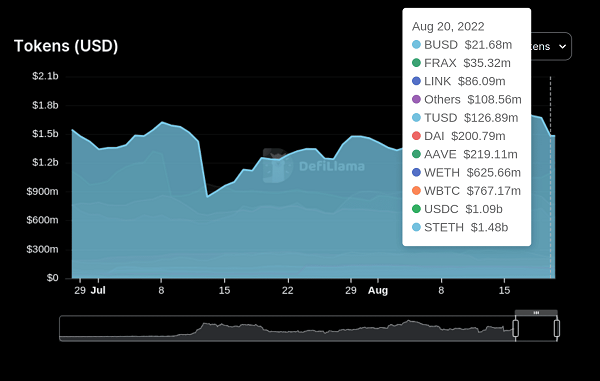

From the team's description, GHO will be "decentralized" like DAI, and due to the composition of its collateral, it will have relatively weak anti-censorship properties. In fact, assuming that all aTokens that can be used as collateral for borrowing on Aave can also be borrowed for GHO, the collateral for GHO will mainly consist of some censorable tokens like USDC:

Source: DeFiLlama

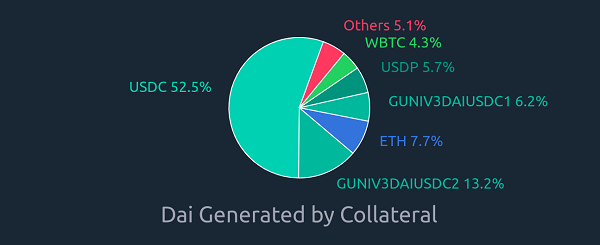

Source: DeFiLlama

In reality, excluding stETH (liquid staked ETH on Lido), USDC is the most commonly used collateral on Aave, followed closely by another trusted token, wBTC. Nevertheless, the composition of collateral on Aave is still much better than that of DAI, where over 50% of the collateral is pure USDC.

It is worth mentioning that over 75% of the tokens supporting DAI are censorable (as shown in the above image), while about 25% of the tokens come from other trusted collateral or self-referential liquidity provision positions (e.g., DAI/USDC LP, used as collateral for minting DAI).

2 What will Aave and GHO look like after launch?

Now, everything is basically ready, and we can enter a more "speculative" phase and consider how GHO will be applied in practice.

In fact, the interaction between the Aave protocol and GHO will undoubtedly be very exciting: although there have been discussions about Aave x GHO and enabling eMode trading mode on GHO — leveraging selected currency pairs (like USDC/DAI) — there are not many details available, so I will briefly outline some ideas here.

aGHO should become the most fascinating collateral on the Aave protocol, but allowing borrowing of GHO could also create significant reflexive risks. Therefore, it would be best to prevent GHO from being minted using aGHO; otherwise, we might see issues similar to those currently occurring with DAI.

Nonetheless, the interaction between the Aave protocol and GHO can still create a nice "stablecoin arbitrage loop," such as: aUSDC > Mint GHO > aGHO > Borrow another stablecoin. With eMode, the combination of Aave and GHO will help it become a very effective stablecoin arbitrage protocol. Additionally, GHO interest rates will also become a "base stablecoin interest rate," which will help control the interest rates of other stablecoins like USDC.

2.1 GHO's liquidity strategy

Another key part of stablecoin design is the liquidity strategy. On Aave, CRV, CVX, and BAL can all be used as collateral. Based on the Reserve Factor, these tokens locked in the native protocol will continuously accumulate in the "treasury," allowing Aave DAO to direct incentives to mining pools related to GHO.

Above: Current status of Aave's "treasury," with over 615,000 CRV, Source: Aave "Treasury" Report (July 2022)

Currently, Frax is trying to "break free" from USDT and DAI and is attempting to establish the Frax Basepool (FRAX/USDC) to become the base currency pair for trading other stablecoins on Curve. We can envision that Aave will likely take similar actions in the future. In fact, many projects currently interacting with USDC and DAI are seeking to diversify their liquidity, and GHO may also be waiting for a "perfect timing" to reduce DeFi's reliance on USDC.

Frankly speaking, Frax previously controlled a significant amount of governance and regulatory voting power during its "confrontation" with Curve, but Aave DAO may not be able to do the same. The CRV/CVX balance in its treasury is clearly insufficient to incentivize the growth of the liquidity pool to a billion-dollar scale, which means Aave DAO needs to seek more liquidity incentive-driven tokens. However, since Aave DAO can earn substantial income from GHO interest, they should have sufficient means to support a certain level of liquidity, regardless of GHO's eventual market cap.

Lastly, it’s worth noting that the relationship between Aave and Balancer is actually "good." First, since transitioning to the AAVE token, the distribution rules used in Aave's security module have been "80% AAVE / 20% wETH Balancer Pool." Second, Aave's treasury currently holds 200,000 BAL and plans to increase its holdings. Therefore, we can expect the stablecoin GHO to perform well on the Balancer protocol. However, compared to Balancer, the potential risk point for Aave's stablecoin GHO may lie on Curve, as Curve is both the "king" and the "kingmaker." Thus, increasing GHO liquidity on Curve may not be easy and could even force it to choose "confrontation" with Curve, similar to Frax.

It is important to note that for stablecoins, the liquidity strategy may be one of the most critical factors, aside from basic protocol incentives (such as dynamic borrowing rates or DAO-managed borrowing rates) and liquidation mechanisms, and is key to whether the stablecoin can maintain its peg.

3 Conclusion

I hope this article helps you better understand the stakes in the stablecoin war. As the release of GHO approaches, Curve stablecoins will also support over-collateralization and launch within the year, making this year's stablecoin market very interesting. For the DeFi market, the expansion of stablecoin scale may be the next development trend, and most DeFi protocols are exploring their own native stablecoin expansions, such as:

Frax initially was just a stablecoin, but it has now launched the DEX FraxSwap and will soon introduce the lending platform FraxLend;

Aave initially was just a money market, but it quickly developed its own native stablecoin;

Curve initially was just a DEX, but it soon added its own stablecoin and began providing effective lending services for liquidity providers.

As mentioned earlier, ultimately, the reason DeFi protocols begin to explore and issue stablecoins is that there is a huge market demand; stablecoins have a high product/market fit. Moreover, it is clear that stablecoins can help protocols gain more profits.