Ethereum Merge Short, Medium, and Long-term Investment Guide

The merger has not been priced in yet, and ETH still has potential worth looking forward to.

The merger has not been priced in yet, and ETH still has potential worth looking forward to.Written by: Hal Press, Founder of North Rock Digital

Compiled by: AididiaoJP, Foresight News

The Largest Structural Shift in Crypto History

As the Ethereum merge approaches, we have been eager to provide an article on how to view the Ethereum ecosystem, particularly regarding investments related to the merge. This is a follow-up to an article we published in January of this year. Although many assumptions and outlooks have changed since the last article was published, the core argument remains unchanged: Ethereum will undergo the largest structural shift in crypto history. The final testnet, Goerli, has recently been successfully completed, and the mainnet target date is set for September 15, 2022.

After the merge, Ethereum will become the first large-scale structural demand asset in crypto history. This article aims to understand the key fundamentals by analyzing various aspects of the Ethereum model, such as supply reduction and the staking rate post-merge.

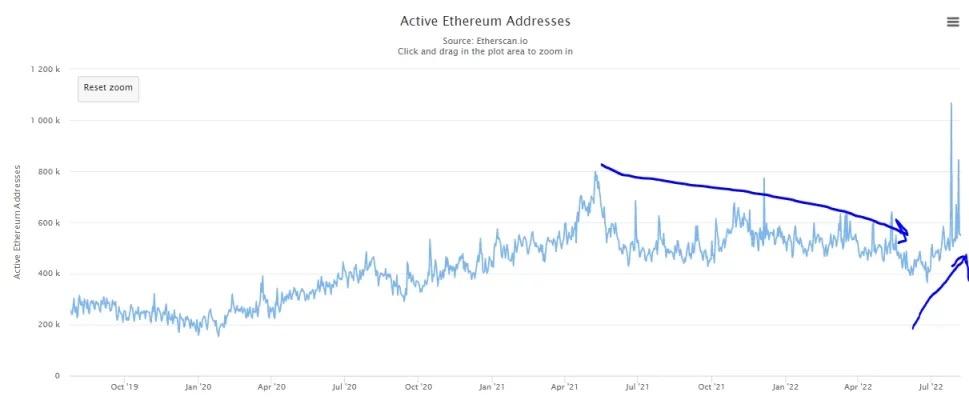

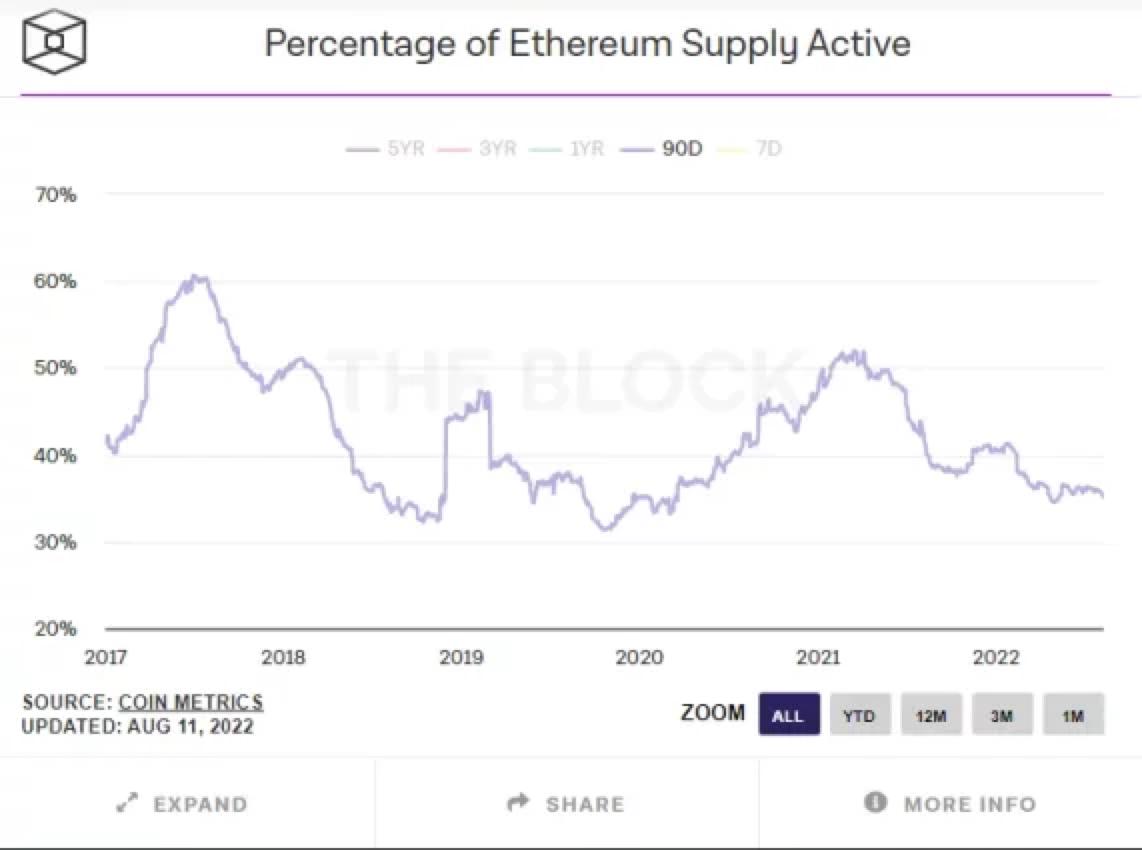

Since last December, the price of Ethereum has experienced a significant decline, but there has been a steady increase in active users since late June.

Typically, more users lead to higher GAS fees; however, due to the recent optimization of various popular applications on Ethereum, GAS fees have not risen significantly. For example, after OpenSea migrated from Wyvern to Seaport, GAS fees decreased by 35%.

Multiple indicators show that despite lower GAS fees, recent activity on Ethereum has been increasing. This raises an interesting question: What is the optimal GAS fee operating rate for Ethereum? Higher fees mean more ETH is burned, but higher fees also limit the adoption of the Ethereum network.

When Ethereum fees are too high, users will choose to use other L1 ecosystems. After appropriate scaling, Ethereum should maintain high fees and a sustained adoption rate. If the optimal fee point for Ethereum aligns with the fees for burning newly issued nodes, the ETH supply will remain stable while keeping fees sufficiently low to avoid suppressing adoption. A recent interesting phenomenon is that lower fees have positively impacted the adoption rate, with active users beginning to increase after a long-term downward trend.

Although we are now close to the optimal fee operating rate, reduced fees can indeed negatively impact various model outputs. This impact is not severe, as the current burn rate remains sufficiently high, leading to slight deflation of ETH post-merge. Importantly, the current operating rate will continue to drive structural demand, as most issued ETH is unlikely to be sold, and the fees used must be purchased on the open market.

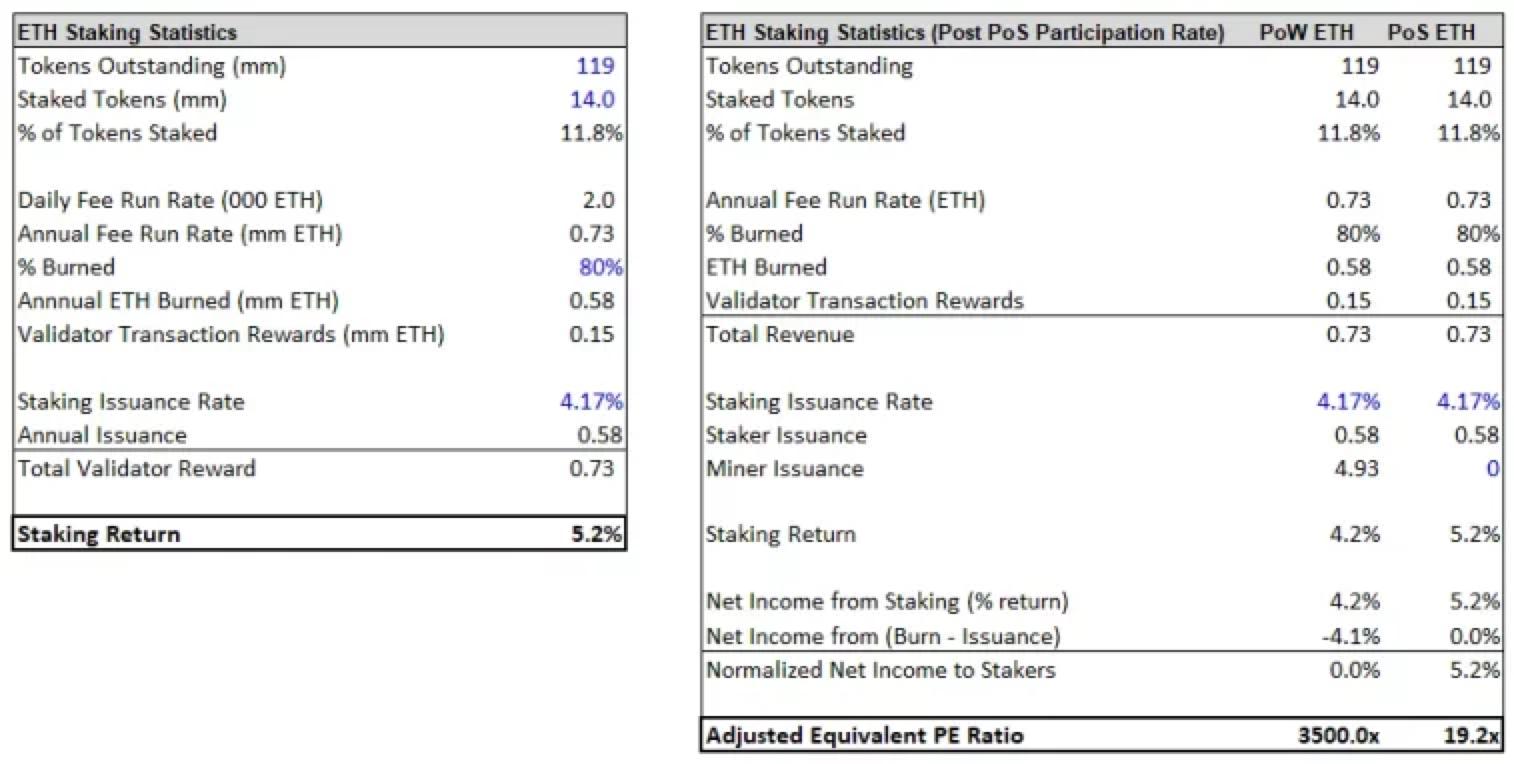

The staking rate post-merge will increase from 4.2% to approximately 5.2%, but this does not imply that the actual yield will effectively increase. To fully understand this shift, we must assess the real yield rather than the nominal yield. With an annual issuance of 4.4% of ETH, the current accrued yield of 4.2% means the real yield is close to 0%. However, when the staking rate increases to about 5% post-merge, this will largely create the highest real yield in cryptocurrency. The only comparable asset is BNB, which has a real yield of 1%.

Stakers will receive a net yield of about 5%, equivalent to approximately 20 times the return. Due to the very low staking participation rate, stakers can capture a large portion of the total rewards, which is one of the main investment advantages of ETH.

Since ETH has many other uses, most ETH in the entire crypto ecosystem ultimately gets locked in these applications rather than being staked, which in turn allows stakers to achieve higher real yields.

From the chart, it can be seen that post-merge, ETH will shift from a continuous structural outflow of about $18 million per day to a structural inflow of about $300,000 per day. While demand may decrease, the impact of a complete reduction on the supply side will become more significant. As the price of ETH falls from its peak, the corresponding hash rate has not followed suit, resulting in a sharp decline in miners' profitability, leading them to likely sell all mined ETH.

For the sake of calculation, assume that 80% of miners' output is sold, with daily sales exceeding 10,800 ETH (approximately $18 million). After deducting about $2 million in fees, this results in a net outflow of $16 million. Post-merge, market sell pressure will drop to zero, and there will be a structural inflow of $300,000 per day. In simple terms, before the merge, ETH needed $18 million in inflows to prevent price declines; after the merge, it will require $300,000 in outflows to prevent price increases.

During periods of economic slowdown, it is expected that the staking rate and structural demand will be below the levels of six months ago, but if economic activity continues to rebound, these ratios will increase. The merge is not just a shift in supply and demand; it is a large-scale foundational upgrade, making the network more efficient and secure in many ways, which is also part of what distinguishes it from Bitcoin's halving.

Time Value

Before discussing the future pricing of Ethereum, let’s consider why the SPX (or almost any U.S. or global stock index) has been a profitable investment tool in the long run. Most people believe that this long-term growth opportunity is driven entirely by earnings growth and multiple expansion. The primary reason for the price growth of these indices is the value of time compounding.

For example, a lemonade stand earns $1 per year, and the stand has 10 shares outstanding, with no cash or debt on its balance sheet. If the market values the $1 equity growth at a 10x multiple, how much is the lemonade stand worth today? What is the value of one share? If we assume the lemonade stand continues to earn $1 per year next year, and the market applies the same multiple, what will the value of the lemonade stand be in one year?

The first question easily leads to the conclusion that a 10x valuation of $1 is indeed $10. If the second answer is still $10, it ignores the value of time compounding. The first balance sheet value is $0. The second balance sheet value is $10, and if it earns another $1 next year, the lemonade stand's value will be $11, making each share worth $1.1. Once a company starts making money, cash flows into the company's balance sheet, and its value belongs to the shareholders. Despite having 0 growth and the same earnings, the lemonade stand's valuation increased by 10% in one year.

This is the value of time compounding; however, cryptocurrencies seem to have not benefited from this dynamic at all and have been adversely affected. Since almost all crypto projects have expenses exceeding revenues, they must generate funds through the issuance of currency to cover their negative net income. Therefore, unless earnings grow or their multiples expand, the price of each token will decline. The most notable example is BNB, which is currently the only L1 token with revenues exceeding expenses. As shown in the chart below, BNB/BTC has been in an upward trend for most of the time and recently broke through its previous high.

Post-merge, Ethereum will generate approximately a 5% real yield. Unlike other L1s, staking yields only need to offset the inflation of the yield, and all ETH holders will earn a 5% return annually. This will greatly incentivize investors to buy and hold long-term. Additionally, the real yield will attract many institutions, helping to accelerate institutional adoption.

Concerns About the Merge

In recent months, investors have expressed significant skepticism regarding technical risks, extreme scenarios, and timing risks.

One of the cases that has raised concern is the Ethereum PoW fork. Some PoW extremists (such as miners) prefer to use PoW ETH and believe that the current forked version of ETH is superior to the PoW alternative, ETC. We believe the fork has little value, but that is beside the point.

The key is that the Ethereum fork will not negatively impact the PoS ETH post-merge. All potential risks are easily manageable or do not exist at all. For example, replay attacks are virtually impossible to execute, and it is unlikely that the PoW chain will use the same chain ID. Even if they maliciously choose to use the same chain ID, this attack can be avoided by disconnecting from the PoW chain or sending assets to a splitter contract. Even if a user is affected by a replay attack, it will only impact that user's assets and not the health of the blockchain network.

The PoW fork could provide dividends for ETH holders, further increasing the value of the merge. ETH holders will be able to send their forked tokens to exchanges and sell them for additional funds. Most of these additional funds will be used to purchase PoS ETH. After weighing the various risks, the conclusion is that the benefits outweigh the drawbacks.

Nevertheless, many long-term believers will still have concerns. As the merge progresses, many of these worries will gradually dissipate, and eventually, skeptics will also shift, with a large number of buyers likely to purchase ETH before the successful merge.

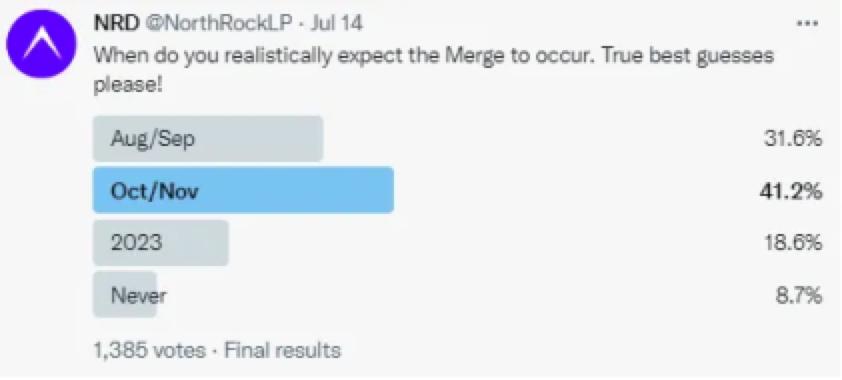

Last month, less than one-third of people believed the merge would occur before October. Even with the merge confirmed for mid-September, the market still believes the likelihood of a smooth execution is only two-thirds.

In this context, the core question is: What changes are expected in the price? Although macroeconomic factors will continue to have a significant impact on the crypto market, the merge will also have a substantial effect on the price of ETH.

Short-term

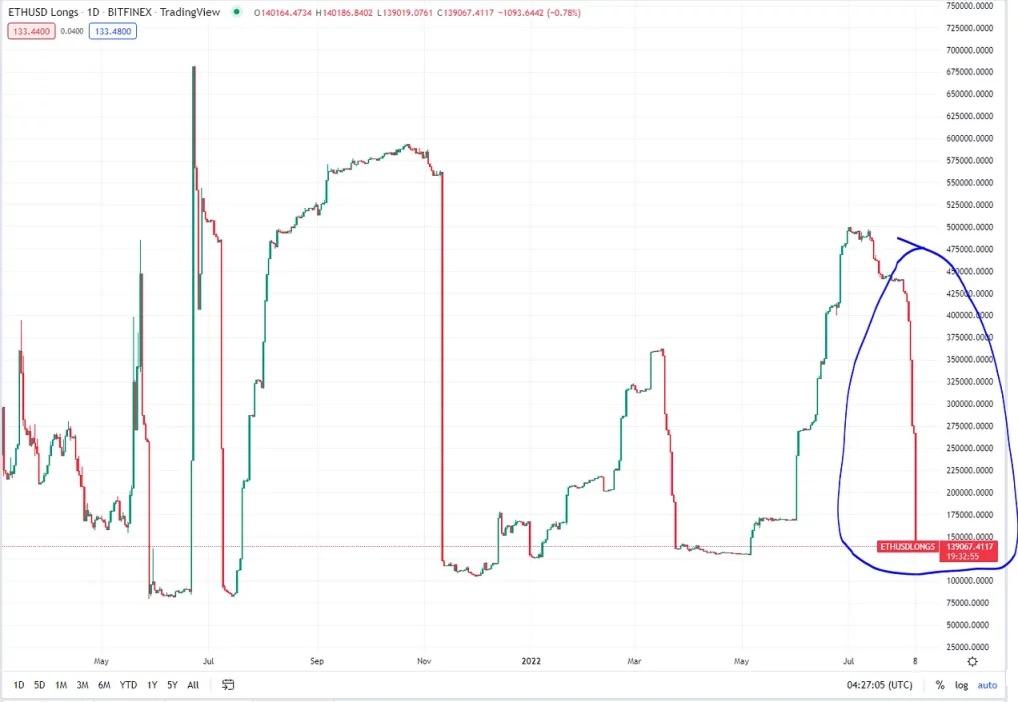

Although the merge has led to a wave of price increases, the crypto market's reaction has been relatively muted. Throughout most of the price rise since June, perpetual funding has remained negative, indicating that there are more shorts than longs in the perpetual contract market.

Another data point shows that Bitfinex longs have dropped to a low point.

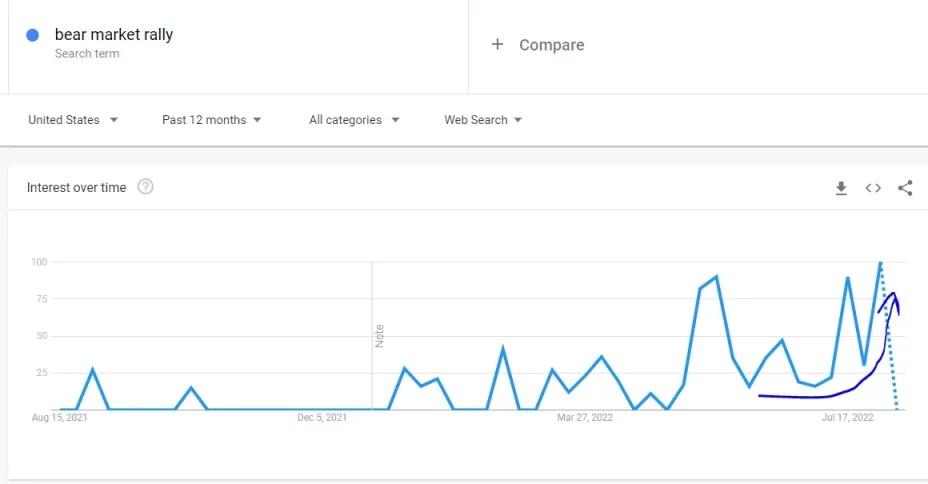

Most participants view this price increase as a bear market rebound and thus are only lightly involved.

Most investors still lean towards Bitcoin maximalism and consistently downplay the impact of the merge. For instance, they believe the merge has been in the works for six years, experiencing countless delays, and this time will be no different; secondly, they believe the technical issues and execution risks of the merge remain significant, with a low chance of success. After assessing the timing and execution risks, we are confident about the merge. After the successful merge of the final testnet, Goerli, earlier this week, core developers have confirmed the merge will occur on September 15 or 16, with the following time primarily focused on coordinating various aspects of the ecosystem.

Despite many concerns about execution risks, the merge has undergone extremely rigorous testing and has been cross-checked by many teams. Additionally, the Ethereum ecosystem has many different clients acting as a safety net, requiring multiple unrelated malicious events to occur simultaneously to impact the protocol, which is one of Ethereum's core advantages. The core advantages and the most accomplished development teams in the field, along with years of preparation, give us confidence that while technical issues exist, they are unlikely to occur.

When people overanalyze extremely unlikely scenarios, the market will exhibit clear fear; however, I expect the price drop at this time to be minimal. In the coming weeks, almost everyone selling ETH is doing so strategically, planning to buy it back at some point before or after the merge occurs. On the other hand, as the date approaches and mainstream media begins to report, the hype surrounding the merge will be amplified. As the merge progresses, capital inflows will accelerate, and ETH may continue to reach new highs as the merge date approaches.

Medium-term

Short-term traders will engage in swing trading during this period, and this selling pressure will be absorbed by structural demand and institutions. The price movements during this period are difficult to predict, primarily influenced by the macro environment. Macroeconomic conditions are hard to forecast, and this article provides some thoughts.

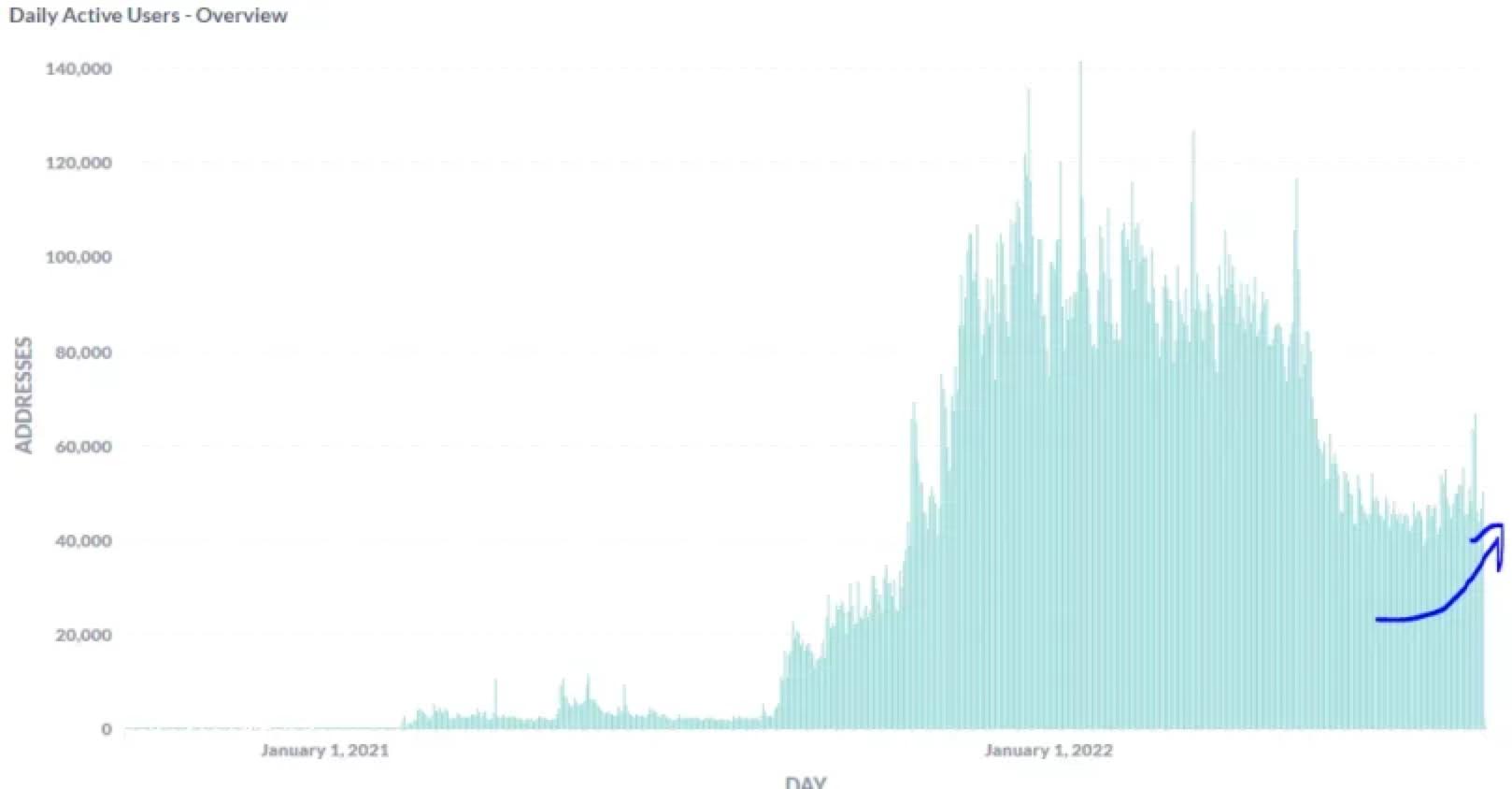

The macro environment for crypto is driven by one core indicator: changes in adoption rates. This indicator is somewhat influenced by the broader macro environment. The reason this indicator affects prices is that changes in adoption rates drive long-term capital inflows or outflows. In short, when users adopt cryptocurrencies, they typically also inject new funds into the crypto ecosystem. For most of the past 8-9 months, we have been in an environment of declining adoption rates, with user funds experiencing net outflows.

From May 2021 to the end of June, the number of daily active users showed a downward trend. However, in the past six weeks, the number of users has steadily increased, indicating that the macro environment may be improving. After several weeks of redemptions, Tether has begun to slowly mint new coins, and new funds are starting to enter the market.

This is not unique to the Ethereum ecosystem; the daily active users in the AVAX ecosystem are also increasing.

NFT users and transactions have stabilized recently.

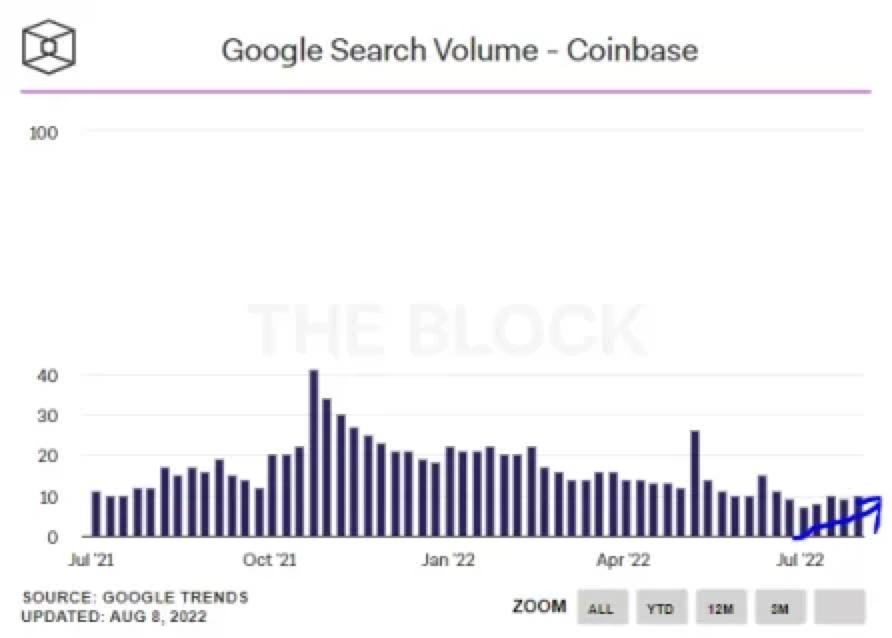

Network searches are also beginning to show positive changes.

This is completely different from the exponential growth we saw at the beginning of the 2021 bull market; these signs can only be considered a signal that may develop into a trend, but they may also disappear quickly.

The broader macro environment will play a crucial role. Inflation is by far the most important macroeconomic variable, and if inflation slows and allows the Federal Reserve to adjust and ease monetary policy, the signs are likely to become stronger. However, if inflation remains high, and the Federal Reserve is forced to continue tightening policy, these signs may disappear. Predicting inflation is not the primary focus of our research, but due to its importance in today's market, we have studied it carefully. After research, we believe that a slowdown in inflation is the most likely outcome, which should gradually turn these market improvement signs into reality.

The massive sell-offs of projects launched in the past 24 months have now been absorbed. Additionally, most projects have seen their market values decline by 70-95%, significantly reducing the scale of future sell-offs, meaning that the market will only need a smaller amount of capital to maintain price stability in the future.

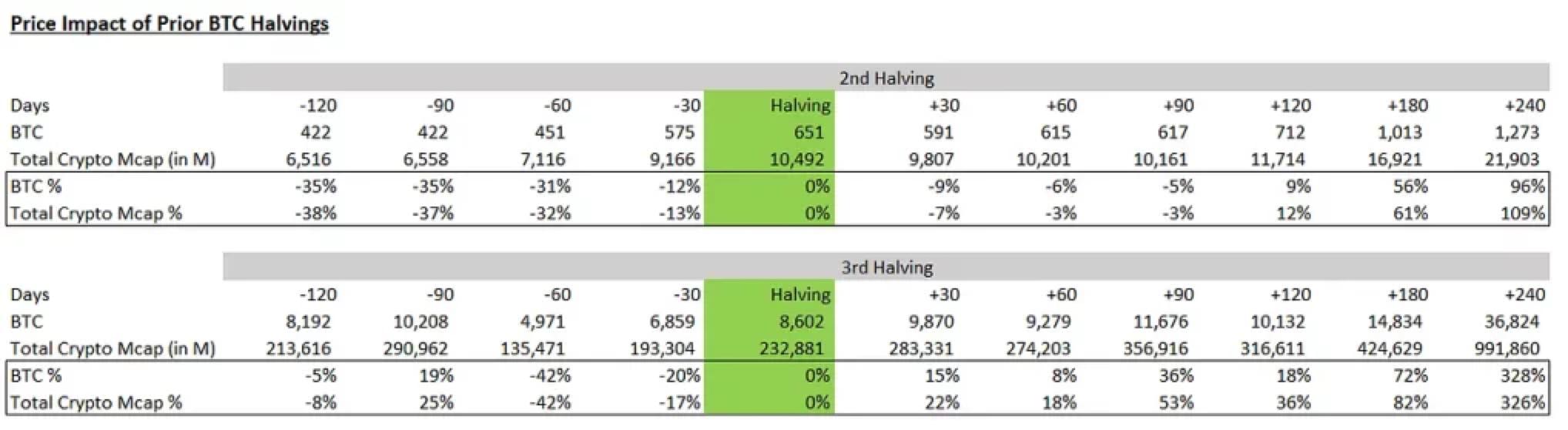

Investors have underestimated the impact of the merge on the overall macro environment. There is much discussion about how the previous BTC halving led to a reduction in supply that drove subsequent price movements, not just aligning with the natural cycles of market sentiment and monetary policy. Another common saying is that supply changes do not drive prices; rather, it is demand changes that matter. We believe that a reduction in supply is no different from an increase in demand. Assume miners sell 10,000 ETH daily; if there is simply an increase in daily purchases of 10,000 ETH, this would eliminate the selling pressure from miners, but this is a demand change rather than a supply change. Clearly, both options would have the same effect, so the impacts of reduced supply and increased demand are equivalent.

If the BTC halving affected the macro environment of the crypto market, then the merge can have a similar impact. Although Ethereum's dominance was significantly lower than BTC's during the last halving, the impact of the merge is almost as significant as the previous BTC halving, and may even be greater.

Post-merge, the cryptocurrency supply will decrease by about $16 million daily. Cumulatively, this is not a small number. A weekly reduction of 70,000 ETH in supply will impact the market, and this is essentially the effect the merge will have, and it will continue to persist. As the impact gradually permeates other parts of the market, it could positively affect the overall macro environment. In summary, if the macro environment slows down, then a rebound from the bottom is likely to turn into an opportunity for sustainable recovery, and the merge will accelerate the market's recovery pace.

Long-term

In the long run, the future becomes easier to predict because structural liquidity changes will play a key role, which is where the impact of the merge is most evident. As long as Ethereum's network adoption continues to increase, structural demand will remain unchanged and will promote further capital inflows. This should lead to sustained appreciation, with Ethereum expected to surpass Bitcoin as the largest cryptocurrency in the coming years, as traffic is the most important variable in cryptocurrency. Ethereum will sail smoothly post-merge, while Bitcoin will continue to face headwinds. The BNB/BTC chart is a good illustration.

Despite the narrative momentum being limited, BNB/BTC has steadily grown during this bear market and has reached new highs multiple times. This is primarily because BNB is the only L1 with structural demand. On both an absolute and market cap-weighted basis, post-merge Ethereum will have greater structural demand than BNB.

Facing Investment Strategies During the Merge

ETH/BTC

Before assessing ETH/BTC trading, it is necessary to provide some background information on the PoW vs. PoS debate. PoS is fundamentally a more secure system. To understand why PoS offers more effective security than PoW, one must first understand how consensus mechanisms generate security. Security is related to the cost of a 51% hash power attack. In other words, how much must the network pay in dollars to obtain $1 of protection against a 51% attack? For PoW, the cost of a 51% attack primarily involves the hardware required to obtain 51% of the hash power, meaning how much miners need to invest in mining hardware to secure $1 of security. In a PoW network, about $1 of supply needs to be issued annually to generate $1 of security.

In a PoS network, stakers do not need to purchase hardware; the question becomes what return stakers require to lock in their share in the PoS consensus mechanism.

Generally, the return rate demanded by stakers is significantly lower than the 100% return typically required by miners. The main reason is the absence of increased cost expenditures, and their assets do not depreciate (mining hardware typically depreciates to nearly 0 after a few years). The required return rate for stakers should generally be in the range of 3-10%, and the currently estimated 5% staking rate post-merge falls right in the middle of this range. This means that to obtain $1 of security, PoS needs to issue $0.03-$0.10, making it 10-33 times more efficient than PoW.

In summary, it effectively only requires issuing about 1/10 of the pre-merge issuance to ensure that the network's security will be double that during the PoW period. This efficiency is not the only advantage; both consensus mechanisms share a common issue: the security of the blockchain is related to the price of the token. A decline in token price can lead to reduced security, which in turn erodes confidence and drives the token price down further, potentially leading to a self-reinforcing negative cycle. PoS has a natural defense against this risk of token price decline, while PoW does not.

First, to attack a PoS system, one must control a majority of the stake. To do this, one must purchase at least as many tokens as those staked from the market. However, not all tokens are available for sale; most of the supply has never been traded, leading to a lack of liquidity in the market. Furthermore, and most importantly, as each token is acquired, the cost of acquiring the next token will increase.

In the past 90 days, only about one-third of Ethereum tokens have been liquid. This means that once a stable staking rate of nearly 30% is reached, it will be extremely difficult to attack the network, regardless of how much capital is available. Another important feature of this defense mechanism is that it is relatively unaffected by price, as the limiting factor for an attack is the liquidity supply rather than capital, making it difficult to attack the network at a lower price. If there is insufficient liquidity supply, it does not matter how cheap each token becomes. This price-insensitive defense mechanism is crucial for defending against potential negative feedback loops that may arise from price declines. PoS certainly has other advantages, such as better energy efficiency and improved healing mechanisms.

Another misconception about PoS is that it may become increasingly centralized, as larger stakers receive more rewards. While large stakers do receive more staking rewards than small stakers, this does not drive centralization. Centralization refers to the process by which large stakeholders increase their percentage of shares over time.

This will not happen in a PoS system. Since large stakers already have a larger share from the outset, greater rewards will not increase their percentage of shares. For example, if two counterparties stake 10 ETH, with counterparty X having 9 ETH and counterparty Z having 1 ETH, X controls 90% of the stake. A year later, X will receive 0.45 ETH, while Z will receive 0.05 ETH. X's rewards are 9 times that of Z. However, X still controls 90% of the stake, and Z still controls 10%. The proportion remains unchanged, so there is no potential for centralization.

Most people view ETH as a completely different asset from BTC, with BTC designed as a decentralized store of value (gold substitute). In many important aspects, Ethereum is better suited than Bitcoin to serve as a long-term store of value. Before comparing the two, it is first necessary to assess Bitcoin's current security model and how it has evolved over time.

From a security perspective, Bitcoin uses a PoW network. As mentioned earlier, the security of the system is related to the cost of a 51% hash power attack. This cost depends on the amount needed to purchase sufficient hardware and control 51% of the hash power, as well as the other equipment/power required. As previously stated, this security is both inefficient and lacks the reflexive defenses of a PoS system.

What happens when Bitcoin halves every four years? Assuming all other variables remain constant, the system fundamentally reduces its security by 50%. Historically, this has not been a major issue, as the value of the issuance (and security) is a function of two variables: the number of tokens issued and the value of each token. Since the price of tokens has more than doubled during each halving cycle, this compensates for the reduction in issuance on an absolute basis. Although the number of tokens issued is halved, the absolute security of the network has been increasing with each cycle. However, this is not a sustainable long-term dynamic; first, it is unrealistic to expect the value of each token to continue to double within each cycle, and mathematically, exponential price increases cannot be sustained long-term. If BTC prices doubled in each halving cycle, it would exceed global M2 after about seven halving cycles. It is clear that BTC prices will stop rising at this rate, and at that point, each halving cycle will significantly reduce its security.

If BTC prices drop around halving cycles, the decline in security will be even more pronounced and may trigger the aforementioned negative feedback loop. As long as prices are constrained, this security system is fundamentally unsustainable. The only way to resolve this issue is to generate meaningful fee income. This fee income can replace part of the issuance and continue to incentivize miners, ensuring security even after issuance decreases. The reality is that Bitcoin's network fee income has been low for a long time and is on a downward trend.

In the long run, the only viable way to ensure security is to generate substantial fee income. Therefore, to become a sustainable store of value, it must generate fees. The alternative is to issue more tokens, which leads to inflation and undermines the utility of the store of value.

Long-term security is the most important attribute of a store of value. For example, as long as almost all market participants believe that gold will retain its legitimacy for a long time to come, gold occupies a large portion of the store of value market.

To make a crypto asset an adopted store of value, it must also convince the market that it is very secure and that its legitimacy can be guaranteed. This is only possible if the protocol's security budget is sustainable in the long term, which can only be achieved with a PoS system that has a large and lasting fee pool. The most likely candidate for this system is ETH, which is one of the only two L1s with a large fee pool; the other is the highly centralized BNB.

Credible decentralization is the second crucial feature of a successful store of value. Gold does not rely on anything else, and this independence is one of the keys to its success as a store of value. Another asset, if it is to be widely adopted as a store of value, must also be credible and neutral. For cryptocurrencies, credible neutrality is achieved through decentralization, and the most decentralized cryptocurrency is undoubtedly Bitcoin. This is primarily because Bitcoin's development work is minimal, and the protocol is largely static, but it cannot be denied that it is the most decentralized protocol to date.

However, as long as there is a realistic path to achieving this ultimate state, focusing on the end state is more important than focusing on the current state. Ethereum has a clear roadmap, and although it is currently only in the middle of this roadmap, ultimately (in about 8-12 years), the importance of the core development team will gradually diminish.

ETH will be more decentralized than BTC and will have long-term security. Contrary to popular belief, PoS promotes decentralization more than PoW. Larger PoW miners have a significant advantage from economies of scale, which actually drives centralization. The correlation of economies of scale with PoS is much lower because the cost of setting up nodes is far lower than the cost of PoW hardware, and the power required for PoS is over 99% lower.

So far, there are 400,000 unique ETH validators, with the top 5 holders controlling only 2.33% of the stake (excluding smart contract deposits). This level of decentralization and diversity distinguishes ETH from all other PoS L1s. Additionally, the top 5 mining pools in Bitcoin today control 70% of the hash rate. While some critics may point out that liquid staking providers control the vast majority of Ethereum's stake, these concerns are exaggerated. These issues can be prevented through liquid staking protocols and the implementation of additional checks.

In summary, PoS is fundamentally a better consensus mechanism for a crypto store of value. This is why the merge will be an important milestone on Ethereum's roadmap, marking a key moment when Ethereum becomes the most attractive cryptocurrency store of value. This is the fundamental reason we support ETH/BTC trading long-term, especially before and after the merge.

Although ETH currently has a smaller market cap, its issuance is about 3 times larger on a market cap-weighted basis, making it difficult for ETH's market cap to exceed Bitcoin's. Market cap is the product of the number of tokens issued and the token price.

When Ethereum's token issuance variable decreases by 90%, it does not mean that the price should increase by 10 times to offset this decrease, as the impact is not necessarily linear, but this growth relationship is worth considering.

Staking Derivatives

As Ethereum is a very large ecosystem, many other areas will benefit positively from the merge. As an investor, considering the second and third-order effects of certain catalysts to find opportunities that may be mispriced in the market is often profitable. There are many areas worth paying attention to regarding the merge, such as L2s, DeFi, and Liquid Staking Derivative (LSD) protocols.

Liquid staking protocols will become the largest fundamental beneficiaries of the merge, even more so than ETH. The revenues of LSD protocols are directly affected by the price of ETH and various other positive impacts related to the merge, and these effects will compound. Additionally, shortly after the merge, their largest expenditure, which is subsidizing the liquidity pool between their staking derivative tokens and native ETH, will effectively drop to zero. Optimistically, ETH protocol revenues could increase 4-7 times (assuming ETH prices rise moderately), and maximum expenditures could decrease by 60-80%.

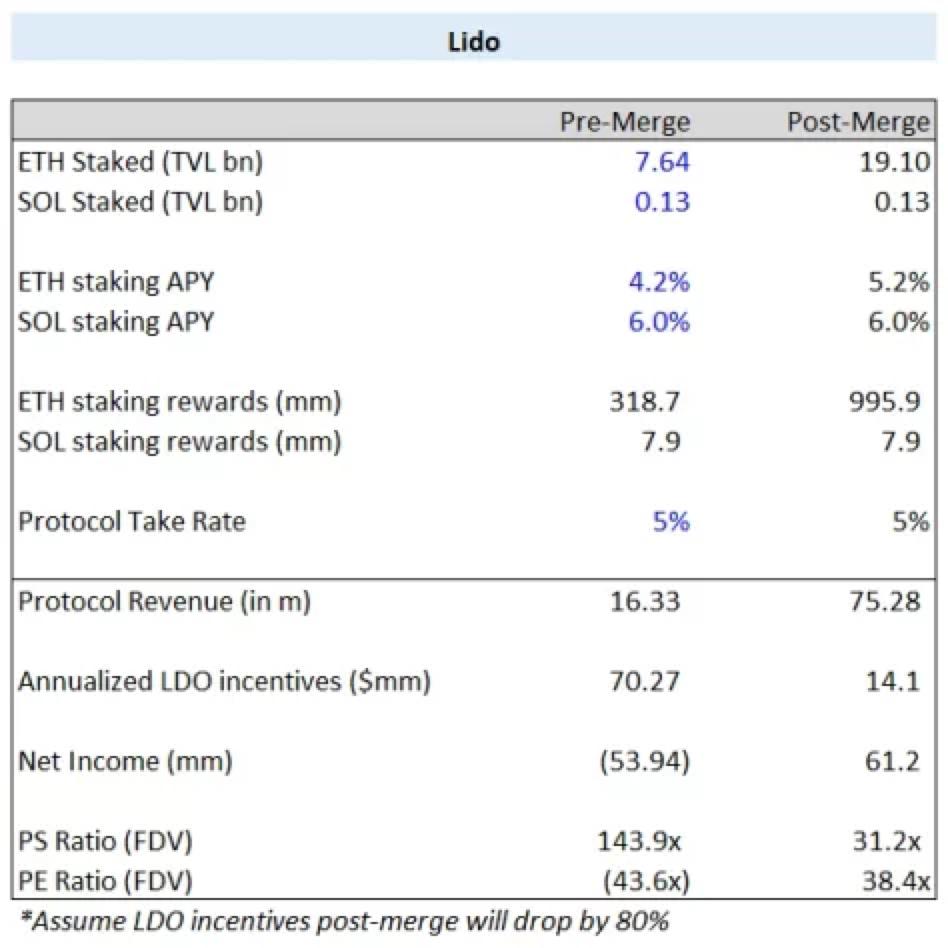

A deep understanding of the revenue and fee models of these protocols is essential to fully grasp this conclusion. Taking the largest LSD protocol, Lido, as an example.

Lido receives 5% of all staking rewards generated. If a user deposits 10 ETH for 10 stETH and generates an additional 0.4 stETH within a year, the user retains 90% of the 0.4, the validator retains 5%, and Lido retains another 5%. It can be seen that Lido's revenue is purely a function of the staking rewards generated on its LSD. These staking rewards are a function of four independent variables: total ETH staked, staking rate, LSD market share, and ETH price.

Importantly, staking rewards are the product of all four variables. If multiple variables are affected, their impacts will compound. Aside from market share, all variables are directly influenced by the merge.

The total amount of staked ETH could sharply increase from the current 12% to nearly 30%, representing a 150% increase. As mentioned earlier, the staking rate could increase from 4% to about 5%, a 25% increase. There is no reason to believe that the merge will significantly impact LSD market share, so we can assume this remains unchanged and has no effect. Assuming ETH prices rise by 50%, the total impact of these different variables would be 250% * 118% * 150% = 444%. This means revenues could increase by approximately 4.4 times.

Staking fees will also decrease significantly. The largest expense for these LSD protocols is incentivizing the liquidity pool between their LSD and native ETH. Given that there is currently no support for withdrawals, creating deep liquidity to manage the large flows between LSD and native ETH is crucial. However, once withdrawals are enabled, these incentives will no longer be necessary. If there is a significant discrepancy between the two, arbitrage opportunities will arise, and the presence of speculators will keep them relatively pegged. This will allow LSD protocols to significantly reduce their issuance (fees), which will also greatly reduce the selling pressure on the tokens.

LDO was trading at 144 times revenue before the merge, and this number has dropped to about 31 times after the merge. While this may not seem cheap by traditional metrics, it is attractive for growth strategy investments that typically have higher valuations, and this is the actual revenue generated by the protocol. Common criticisms of LDO are that this revenue does not return to holders, leading to frequent comparisons with Uniswap. While it is true that there is currently no revenue passed on to token holders, this should not be a concern; just because token holders do not receive cash flow today does not mean they will not receive it in the future.

LDO is still a very early-stage business and should not be returning cash. They need to raise cash regularly and are currently burning cash at their operating rate (which will change post-merge).

Raising funds from investors to burn cash and then distributing protocol revenues to token holders to increase the funds needed for burning is unwise. This is akin to a startup paying out distributions to investors based on early revenues, even though it does not generate enough revenue to cover expenses, which would never happen in traditional capital markets.

Many participants are also concerned about Lido's dominant market share, as they hold 90% of the LSD market, with stETH accounting for 31% of total staked ETH. Lido should maintain a stake below 33% of staked ETH to eliminate any doubts about Ethereum's credible neutrality. As for the investment case for the protocol, the 33% market share cap is not significant. Lido has many other growth points aside from market share, and its current share is already quite competitive.

In summary, Lido is a key infrastructure in the Ethereum ecosystem that has established product-market fit and dominant market share, which will continue to be a rapidly growing market segment. Considering its past and expected future growth prospects, it is one of the most investable assets in the space. While Lido is the market leader and largest player, there are also two other LSD protocols, Rocketpool and Stakewise, worth considering. Each LSD has many unique aspects and scalable complexities. RPL and SWISE should benefit from any share that Lido loses due to centralization concerns. While we believe any loss of Lido's shares will be moderate, even a moderate loss for Lido will equate to significant gains for smaller players.

For example, if LDO loses 4% of market share, RPL gains 2.5%, and SWISE gains 1.5%; if LDO loses about 12% of market share, RPL could gain about 50% and SWISE about 125%.

The second-largest player, Rocketpool (RPL), has a unique staking mechanism and token economics. To stake through RPL, validators must pair RPL with native ETH and maintain a minimum ratio between the two. As ETH staking participation increases and more validators adopt this solution, this dynamic creates predictable and guaranteed demand for RPL.

Another benefit of RPL is the practice of pooling funds with other users, allowing the ETH required to set up staking nodes to be reduced from the normal 32 ETH to just 16 ETH. This reduced minimum allows smaller operators to set up nodes and further incentivizes decentralization. This makes RPL a perfect complementary participant to LDO, which will facilitate an increase in RPL's market share, making them the primary beneficiaries of Lido's effective market share cap.

Stakewise is another alternative to LDO. Their model is very similar to LDO, but they are increasingly gaining institutional attention, allowing them to adapt well to the post-merge market. They have a highly driven and professional team with a strong track record of execution. Notably, they have discussed implementing a token economics plan that is friendly to token holders, which would allow token holders to directly receive additional protocol revenue.

Additionally, SWISE has gained significant traction, with large accounts looking to diversify their staking products (one recent proposal was approved by Nexus Mutual, which will increase their TVL by 20-25%). As they are the highest-valued smallest participants, they may represent the highest risk/reward investment in this category. LDO is the cheapest and safest but has the least room for market share growth. SWISE is the most expensive but has the most room for market share growth, while RPL is in between, with unique token economics and decentralized staking mechanisms. Relative valuations are reasonable, indicating that the market is effectively pricing different opportunities. We choose to hold all three.

LSD tokens may be one of the investable assets worth considering before and after the merge, as they may outperform ETH, but investors should expect higher volatility and lower liquidity.

Conclusion

The merge is set for September 15 or 16, marking the largest structural change in crypto history, and investors need to consider more factors. What are the key points? The merge has not yet been priced in.

Risk warning

Risk warning Risk warning

Risk warning