The Trojan Horse of Cryptocurrency? What if USDC/USDT Leaves Ethereum

Stablecoins completely contradict the original vision and purpose of cryptocurrency.

Stablecoins completely contradict the original vision and purpose of cryptocurrency.Original Title: 《Bend The Knee》

Original Author: Emiri

Original Compiler: Block unicorn

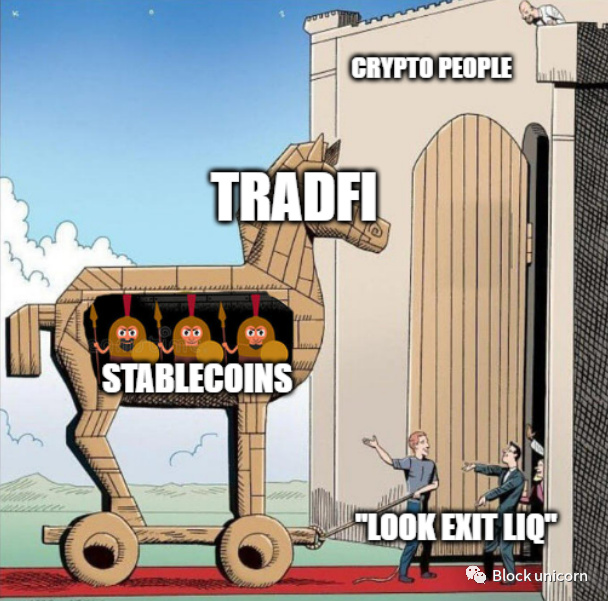

We have all heard the story of the Trojan Horse. The real danger of the Trojan Horse is that it makes you feel safe; you never expect any threats, and it is precisely when you feel the safest that you are the most vulnerable. Once the Trojan Horse is unleashed, there is nothing you can do but watch the chaos unfold.

While this may sound a bit cynical, our beloved stablecoins might be the Trojan Horse of cryptocurrency.

Don't get me wrong; I know the benefits that stablecoins bring. I have written extensively about stablecoins in the past. I apologize for this shameless self-promotion; for articles about other stablecoins, you can click here and here.

If you have read my previous articles, you might ask, "Emiri, you seem to have a high opinion of stablecoins; you seem to think they are a part of the system, so why do you say they are a Trojan Horse?"

Yes, the problem lies in its success. In my view, so far, the most useful thing in crypto technology is stablecoins, and USDC/USDT is currently the best use case for cryptocurrency. They facilitate the circulation of the dollar globally, simplify the trading experience, and have proven to be a better payment system, especially for international transfers.

But stablecoins completely contradict the original vision and purpose of crypto. Think about it: we are building an alternative financial system, free from any constraints of the traditional financial world, yet the best product that has emerged from it is a synthetic fiat currency (USDC/USDT).

The Hegemony of USDC

Everyone knows about the rise of USDC and how it has begun to become a very close competitor to Tether (the parent company of USDT). In fact, most people have started to prefer USDC and seem to believe it will surpass Tether, especially with the constant rumors about Tether's behind-the-scenes dealings. I mean, USDC has become so popular that there are bullish Twitter accounts surrounding it: @USDCbull1.

As we have seen, many decentralized stablecoins have collapsed in recent months. For the little fat guy in USDC, everything has been going smoothly. Uninterrupted in their lane, thriving and growing, focusing on their track, there seems to be no problems on the horizon. Circle continuously updates their USDC reserve status and even announced a euro stablecoin; everything is fine.

Currently, most of the funds in DeFi protocols are in USDC, and the most active liquidity pools in DeFi involve USDC in one form or another. A significant portion of the on-chain net worth of most cryptocurrency participants is held in USDC.

However, recent developments indicate that the Trojan Horse has begun to reveal its true self. After OFAC sanctioned Tornado Cash, Circle (the parent company of USDC) complied and blacklisted addresses associated with Tornado Cash. Now, many users and protocols that have had any interaction with Tornado Cash have a significant portion of their funds frozen. This is just a small example of the power that these centralized stablecoins hold. They can blacklist addresses at any time, which means relying on these addresses poses existential risks to the crypto ecosystem.

USDC was initially a small tumor ignored by most, but it has now transformed into a potentially dangerous cancer that plagues every part of the crypto economy, and all we can do now is watch these events unfold.

Where is the Cancer Now?

Let's start with the most important Dapp in this scenario, Curve Finance. The most important pool on Curve (CRV) is the 3pool, which, at the time of writing, has a TVL of $991 million and a trading volume of $95 million. Other large funding pools, such as the Frax pool, sUSD pool, and USDT pool, are related to the 3pool. In the 3crv pool, USDC accounts for 40% of the pool, which is about $400 million at the time of writing.

Let's look at Uniswap, where 4 out of the top 5 pools by TVL have USDC. These top 5 pools account for a total of $2.5 billion in TVL, with a total weekly trading volume of $5 billion. Therefore, a significant portion of Uniswap's activity relies on USDC.

On the AAVE lending protocol, USDC is the second most active coin after ETH. AAVE has a total supply of $1.4 billion in USDC, with $470 million in loans. On Compound, USDC is the second highest liquidity after ETH, with a total liquidity of $700 million.

When MakerDAO shifted to a multi-collateral model, the amount of ETH they held as collateral sharply decreased, while the amount of USDC in reserves sharply increased. Currently, 60% of DAI collateral is provided by USDC. 47% of the $10 billion DAI TVL is provided by USDC. Thus, the leading decentralized stablecoin in DeFi heavily relies on centralized stablecoins.

Let's look at Frax, which has a $911 million dollar reserve, of which 33% is made up of USDC or USDC derivatives. Even though FRAX is highly collateralized, with 90% of the collateral being USDC, it sometimes becomes almost a proxy for USDC.

I could go on, but I think you get the point. USDC is deeply rooted in all foundational parts of DeFi. The total TVL of DeFi is $65 billion, with the top five protocols being MakerDAO, Lido, AAVE, Uniswap, and Curve. Out of the $65 billion TVL, USDC accounts for a cumulative $36 billion, just over half, and the TVL of four of these five protocols is largely comprised of USDC.

Doctor: I can't say for sure, but it looks like stage 3 cancer.

What Do Oncologists Recommend?

(Advice on USDT/USDC)

"Bro, you need to diversify to solve the concentration issue," seems to be a common solution proposed on Twitter. All treasuries and protocols should move away from supporting USDC and start looking for more decentralized, censorship-resistant alternatives.

This is certainly something everyone would love to do, but it has to become that simple. We need to consider what it actually looks like to diversify away from these centralized stablecoins for DeFi.

People love to talk about DeFi as a Lego-like structure. However, if you look at the foundational protocols mentioned above, you will find that the DeFi ecosystem relies on them (USDC/USDT) to some extent. They either build on top of these foundational protocols, executing strategies on these protocols, or hold a significant amount of native tokens in their treasuries. Therefore, the ripple effect of moving away from USDC could be catastrophic; the collapse of the foundation could lead to the entire structure collapsing immediately. Unfortunately, many new protocols with real potential may have to shut down prematurely, and many existing protocols that have been growing steadily may also have to close.

In my view, if you want to move away from USDC, there are two paths to choose from. One is for protocols to diversify into other stablecoins, and the other is to diversify into a basket of other crypto assets.

When it comes to diversifying into other stablecoins, let's assume you diversify into other decentralized stablecoins. At this point, the best options are DAI and FRAX, but as we have seen earlier, they are both heavily reliant on USDC right now. Therefore, diversifying away from USDC could lead to some severe volatility in DAI and FRAX themselves. When it comes to other options, they have proven to be very risky, as most of them have not undergone sufficient stress testing. We know that stablecoins can easily collapse, which is why relying on newer stablecoins is not a good move.

Even something like RAI, a truly decentralized stablecoin that is not pegged. This seems like the optimal solution, but the issue lies in user adoption. Psychologically, it is difficult to get people to accept such a stable coin and start pricing in RAI, and moreover, it integrates poorly with other parts of DeFi.

Thus, the transition from centralized stablecoins to decentralized stablecoins must start with decentralized stablecoin protocols, and this transition will initially hurt decentralized stablecoins, with some possibly surviving. This, in turn, will seep into other parts of DeFi, leaving a wasteland in its wake.

Another approach is to diversify from USDC into a basket of crypto assets. While this makes sense from a "decentralized" perspective, it makes no sense from a business perspective. This would lead to a situation similar to before the emergence of stablecoins, where every protocol treasury and every protocol reserve would hold high-risk and highly volatile crypto assets, which could lead to the closure of most protocols under adverse market conditions.

So what should we do? Will developers provide breakthrough solutions? Or will we just bend the knee?

Do We Really Need Stablecoins?

All this discussion about stablecoins raises the question of whether stablecoins are really necessary. There are many decentralized experiments, but they are either not truly decentralized or end up imploding. There has yet to emerge or potentially emerge meaningful competition for centralized stablecoins.

In short, stablecoins have three main benefits: trading, payments, and access. Two-thirds of these can be solved, but any unprecedented access to dollars (or other currencies) can only be achieved through stablecoins pegged to fiat.

Payments and trading can be solved by ETH itself. If you think of cryptocurrency as the financial layer of the internet or the metaverse, then ETH has already shown signs of becoming the base currency. Admittedly, it is very early, and it will take time for people to price ETH wealth in non-dollar terms, but it is a gradual process. All NFTs are already priced in ETH, and all newly listed Shitcoins are priced in ETH.

One way to look at stablecoins is to view them over a very long time frame. In this case, they are merely a temporary solution, serving as a bridge between fiat and cryptocurrency. Once a significant portion of global liquidity is funneled into cryptocurrency, something like ETH or whatever is popular at the time can begin to serve as the base currency, simply because all cryptocurrency transactions will be priced in them.

Final Thoughts

This is not the only insider threat in our system; almost all protocols rely on oracles that are typically centralized, and key infrastructure participants, such as Infura (a suite of infrastructure development tools and APIs for decentralized protocol unicorns like UNI, COMP, Metamask, etc.), are also centralized. As trust is placed in so many different cancerous spaces (centralized spaces), the more likely outcome is a complete abandonment of decentralization, censorship resistance, and permissionless transactions.

We hope there is a way to shift our dependency on these centralized entities to something more aligned with the original spirit of crypto. If we succeed in this task, considering how entrenched these entities are, we may experience extreme pain in the medium term. Despite the pain, I am confident that crypto will not die; it has proven its resilience time and time again, and it is likely to do so again.

In the meantime, I just hope that someone much smarter than me will solve the problem, and if they do, I will continue to report on it here. If not, I will still be here, because what else can I do?

Thank you for reading, and I hope you enjoyed it.