Meng Yan: A Brief Overview of the Balance Sheet in the Web3 World

The balance sheet reflects the status of a company's assets, liabilities, and equity at a specific point in time.

The balance sheet reflects the status of a company's assets, liabilities, and equity at a specific point in time.Original Title: [Popular Science Article] Balance Sheet in Web3

Source: Meng Yan's Blockchain Thoughts

Author: Meng Yan, Founder of Solv

Learning in a new field presents a significant challenge in finding an efficient framework for thinking and a common language for communication. Web3 involves many topics related to token economics and finance, and in relevant discussions, the balance sheet is a very useful tool. It not only helps clarify thoughts and understand the essence of issues but also improves communication efficiency and can even help discover new innovation opportunities. I have personally benefited greatly from it. However, in practice, I find that there are not many peers who understand this tool and can actively use it to analyze problems, which I find regrettable. Therefore, I am writing this article to introduce and advocate for it. Additionally, in future articles discussing Web3, token economics, and monetary economics in this public account, this tool will be frequently used, so this article also serves as a reference document for future citation.

Basic Knowledge of Balance Sheets

The balance sheet is a fundamental tool in corporate finance and accounting, and it is the most basic among the "three major financial statements" or "four major financial statements." In traditional business, junior managers generally care more about the income statement, while bankers, investors, and seasoned executives pay more attention to the balance sheet. When discussing monetary economics, understanding the balance sheets of central banks and commercial banks is a basic skill and starting point. In fact, learners of Web3 will gradually discover that the balance sheet used in discussions about Web3 is quite different from that of corporate balance sheets and is more similar to the balance sheets in macroeconomic accounting. The balance sheets used in DeFi research are also quite similar to bank balance sheets. Therefore, I believe that interpreting and using balance sheets should become a basic skill for Web3 practitioners.

Back in 2017, when I was studying monetary economics, I realized that this tool is very useful for discussing token economics. However, since I do not have a background in economics or accounting and have never systematically studied accounting knowledge, I only regarded the basic balance sheet as a tool for analyzing token economics. In fact, there are many valuable contents in traditional accounting knowledge, including some estimation, assumption, and adjustment techniques, which are worth borrowing for token economics. However, my understanding of this knowledge is quite superficial, and I need to continuously supplement it based on actual needs. Here, I will introduce some of the most basic knowledge points within my understanding, aiming to lay a foundation for the subsequent discussions.

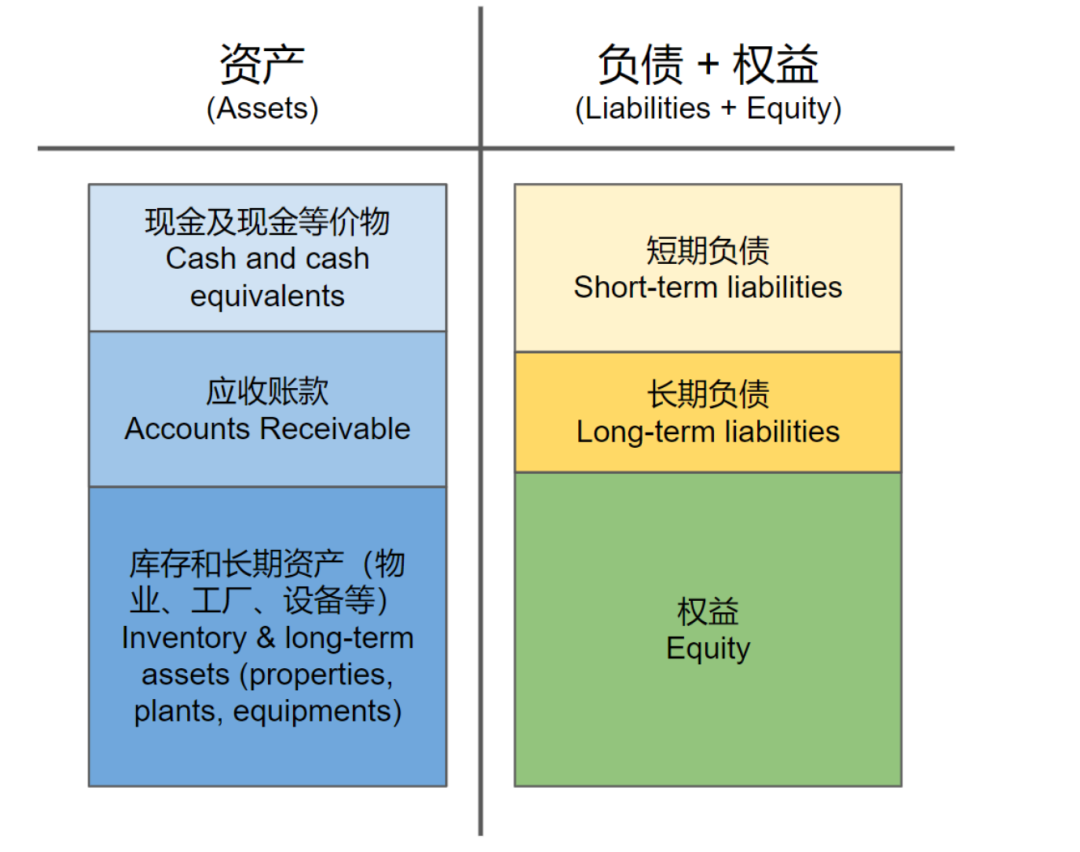

The balance sheet reflects the state of a company's assets, liabilities, and equity at a specific point in time. It looks like this:

Figure 1. Schematic of a Traditional Corporate Balance Sheet

From observing this diagram, we can derive several key points about the balance sheet:

- The balance sheet is divided into two parts: the left side is assets, and the right side is liabilities and equity, separated by a vertical line, hence it is also called a "T-shaped table";

- There is an identity: Assets = Liabilities + Equity. In other words, the total values on the left and right sides of the balance sheet should be equal, which is balanced. This is the most important characteristic of the balance sheet and is why it is called a balance sheet in English;

- Under normal circumstances, a company's equity should be a positive value. If equity is negative, meaning that assets < liabilities, the company is insolvent and has fallen into a solvency crisis;

- The asset side can generally be divided into highly liquid assets (cash and cash equivalents) and low liquidity assets (short-term receivables and long-term assets), typically arranged from top to bottom;

- Liabilities are also divided into short-term debts and long-term debts, arranged from top to bottom. Companies should pay special attention to short-term debts to ensure that there is enough cash and cash equivalents on the asset side to cover the debts, otherwise, they will fall into a liquidity crisis;

- Equity is the true net worth of the company, and undoubtedly, according to point 2, equity = assets - liabilities.

In fact, the basic knowledge of balance sheets is just this little bit, and an ordinary person can learn it in a few minutes. However, in traditional finance, a lot of time is spent learning some complex concepts, especially how to fit complex real business into accounting rules, such as how to classify, value, and handle intangible assets (goodwill, intellectual property, etc.) on the asset side, as well as distinguishing the conceptual differences between "owner's equity" and "equity," etc. These contents have little value for the study of Web3 digital assets in the short term. On the contrary, what should be focused on is how to express different types of digital assets in the balance sheet.

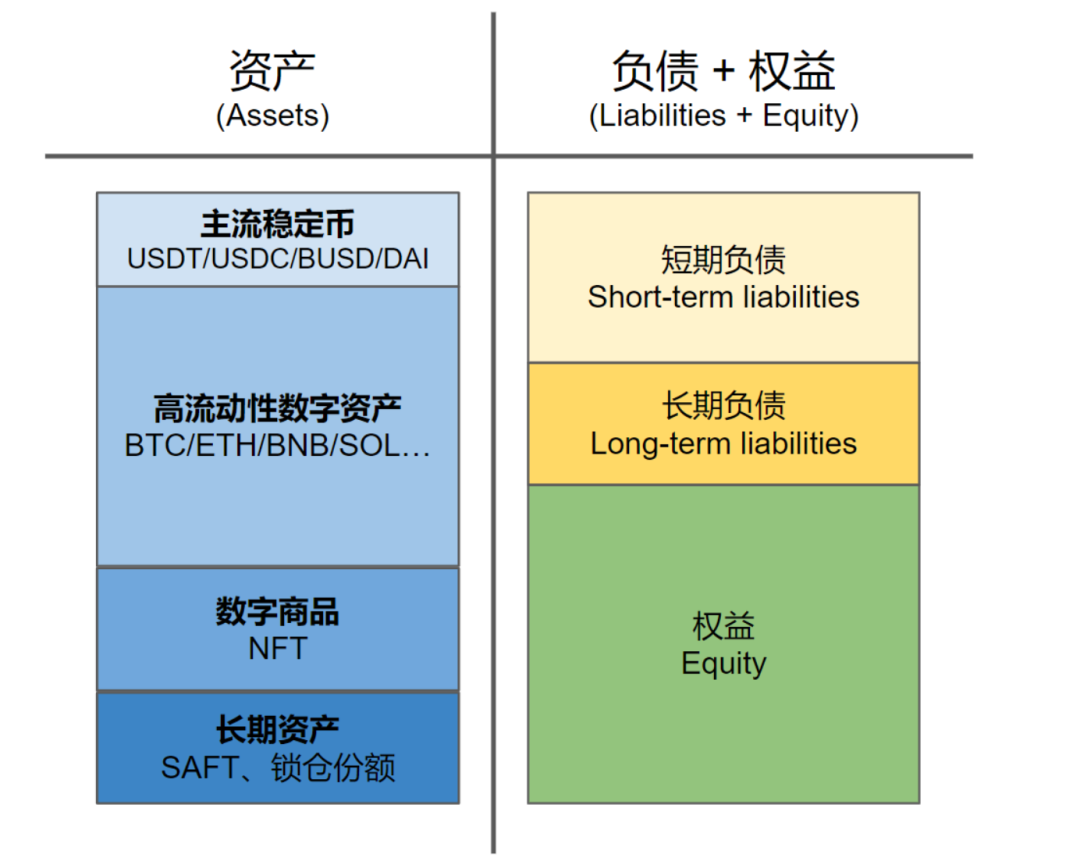

Digital assets mainly appear on the left side. Due to their diverse forms and the constant emergence of new categories, it is difficult to list them all. Following the principle of arranging from top to bottom with decreasing liquidity, we can arrange the current main digital assets as follows:

Figure 2. Arrangement of Digital Assets

Figure 2 may represent the balance sheet of a purely digital DAO organization. Our subsequent discussions can take this as a starting point.

In addition, there are some additional tools that are very important.

Incremental Balance Sheet

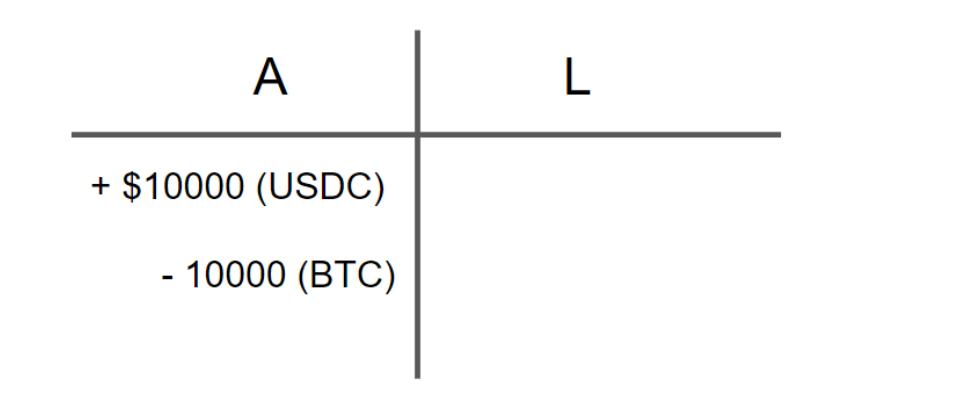

A commonly used extension tool in practice is the incremental balance sheet, which describes the impact of a transaction on the balance sheet. In the incremental balance sheet, we only list the items affected by the current transaction, while those not affected are not listed. This method not only highlights the issue but also simplifies the chart drawing, making it easy to use and facilitating communication.

For example, if a user sells BTC worth $10,000 and exchanges it for $10,000 USDC, this transaction only affects the user's quantities of BTC and USDC, without affecting other asset and liability items. Therefore, expressed as an incremental balance sheet, other items are not listed, and only the increases and decreases of BTC and USDC need to be expressed:

Figure 3. Incremental Balance Sheet for Selling BTC Transaction

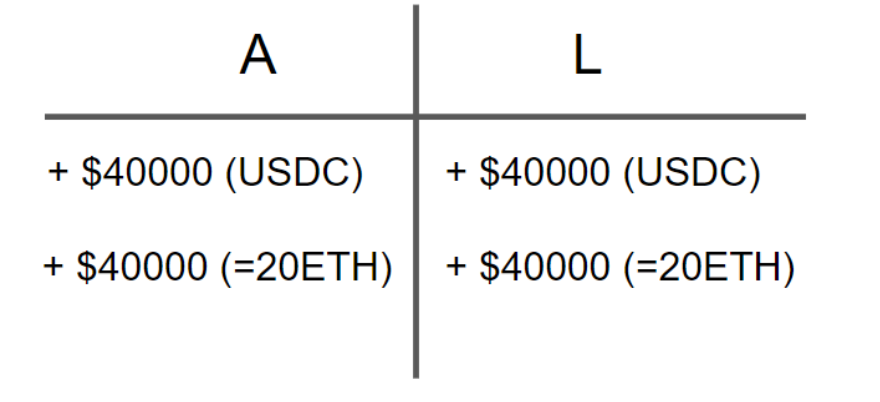

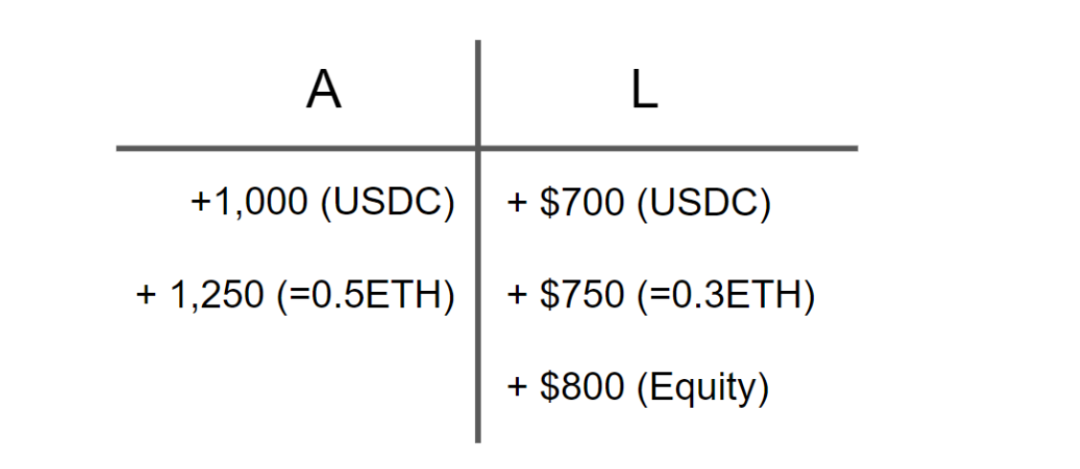

Another example: Suppose when ETH is worth $2,000, a user borrows 40,000 USDC and 20 ETH of equivalent value for market making. The incremental balance sheet shows as follows:

Figure 4. Funding for Market Making

Assuming that after a period of time, he earns 1,000 USDC and 0.5 ETH from market making, but at the same time, the accumulated unpaid interest reaches 700 USDC and 0.3 ETH, while the price of ETH rises to $2,500, the incremental balance sheet shows as follows:

Figure 5. Profit from Market Making

From the above examples, it can be seen that since the balance sheet is always balanced, the impact of a transaction is also balanced. The quantity changes triggered by a transaction in the balance sheet must also be balanced on both sides, either by offsetting increases and decreases on the asset or liability side, or by simultaneous increases or decreases on both sides.

In practice, incremental balance sheets are used far more often than complete balance sheets.

Combined Incremental Balance Sheet

Transactions occur between multiple parties, and in many cases, we also need to consider the impact of the transaction on the balance sheets of other relevant parties. At this time, we can place the incremental balance sheets of the relevant two or more parties together to gain a clearer understanding of the nature and impact of the transaction.

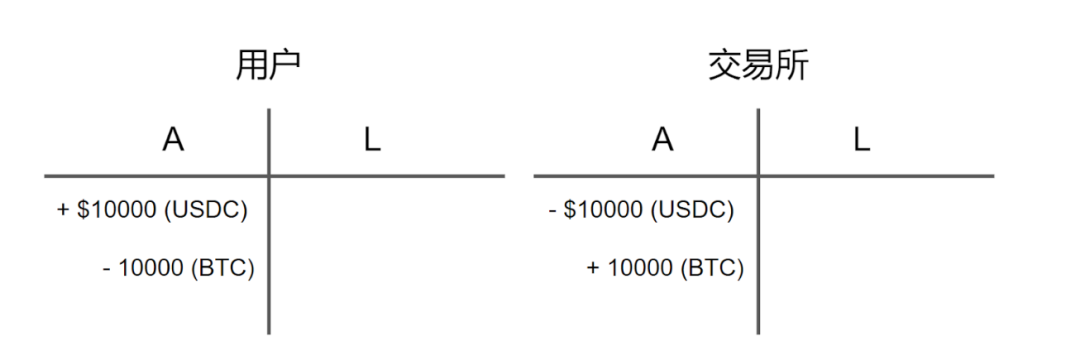

For example, in the case of Figure 3, if we place the incremental balance sheet of the counterparty (e.g., an exchange) alongside that of the user, we can obtain the following combined incremental balance sheet:

Figure 6. Combined Incremental Balance Sheet for Bitcoin Transaction

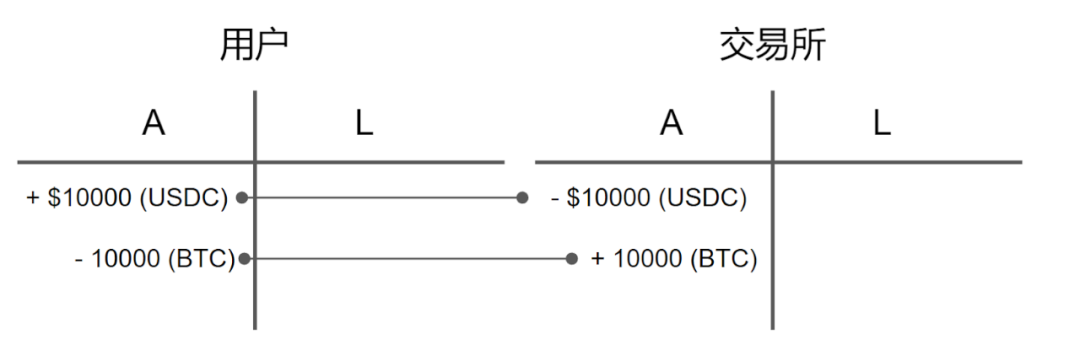

In practice, corresponding changing items are often connected with lines to indicate "they are the same money." For example, the above example can be connected as follows:

Figure 7. Combined Incremental Balance Sheet with Lines

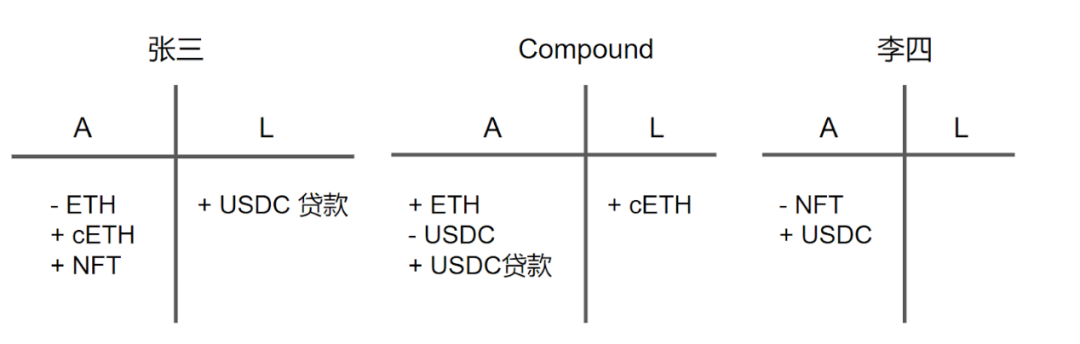

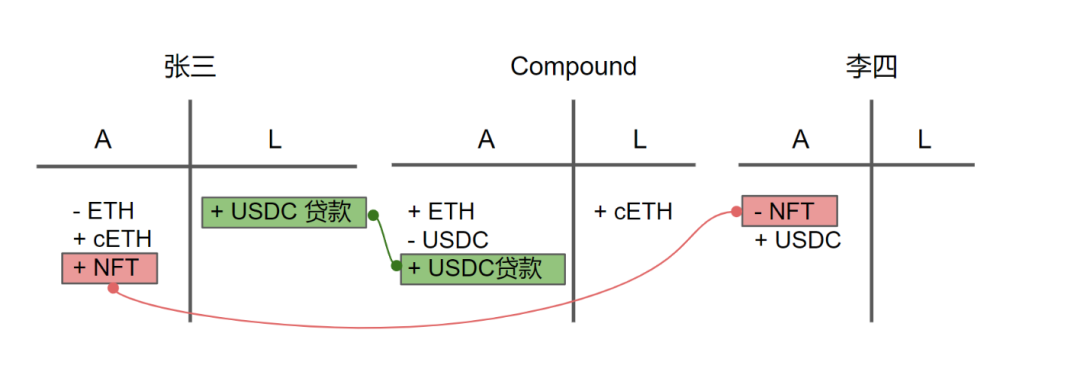

Many times, we are not concerned with the quantity of assets but rather qualitatively study the changes in the asset-liability relationships of the parties involved in the transaction. In such cases, numbers can be ignored. For example, suppose Zhang San pledges several ETH to Compound to borrow USDC and then purchases an NFT from Li Si. If we are not concerned with the specific amount of this transaction and only want to analyze qualitatively, the combined incremental balance sheet is as follows:

Figure 8. Combined Incremental Balance Sheet for Pledging, Borrowing, and Purchasing NFT

The above table demonstrates the ability of the combined incremental balance sheet to describe transactions, clearly outlining the flow of funds and the destination of assets. If lines are added, it becomes even clearer.

Figure 9. Combined Incremental Balance Sheet with Some Lines Added

In the combined table, each incremental item must have a corresponding item. For example, if one party's asset increases, it must correspond to a decrease in another party's asset or an increase in a liability item. This is the basic principle of using a combined table.

The above is the basic content of the balance sheet. Of course, these are just some of the simplest examples. In reality, the flexible use of balance sheets can describe many complex scenarios and help us solve many complex problems.

Advantages of Researching Issues Based on Balance Sheets

Many people may question why we need to use balance sheets to study simple transactions like buying and selling or pledging and borrowing. What are the benefits?

Based on my long-term learning and usage experience, there are at least three benefits.

First, it helps deepen our understanding of financial transactions and events. The balance sheet provides a magnifying glass for gaining deep insights into financial behavior. The same event, if you only understand it roughly as a transaction, may lead to very superficial views. However, if you draw the corresponding balance sheet, you can see the essence of the matter.

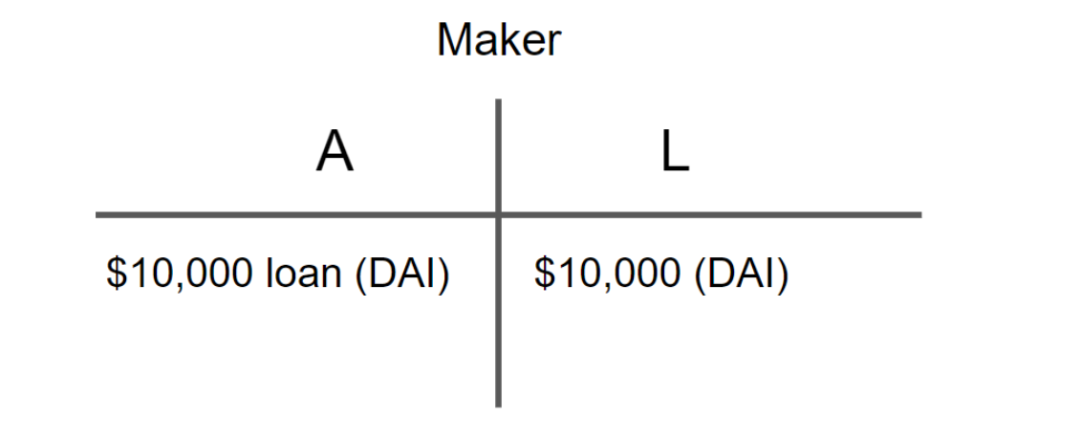

For example, recently the MakerDAO community voted to support using DAI to purchase U.S. Treasury bonds. If this event is only understood as a new use for stablecoins, it diminishes its significance. When we place the bond purchase behavior in the MakerDAO balance sheet, we arrive at a shocking conclusion.

Assuming that at this moment, Maker's users have collateralized excess assets (such as ETH) and generated $10,000 worth of DAI through borrowing, the following is MakerDAO's balance sheet before the bond purchase.

Figure 10. Hypothetical Maker Balance Sheet

Readers may wonder why the ETH collateralized in Maker does not appear on Maker's balance sheet. This is because collateralization is not a transfer of ownership but a contractual act to enhance loan credit. After collateralization, the ownership of ETH does not transfer to Maker and cannot be counted as Maker's asset. Maker's creation of $10,000 DAI is based on the loan, not the ETH collateralized.

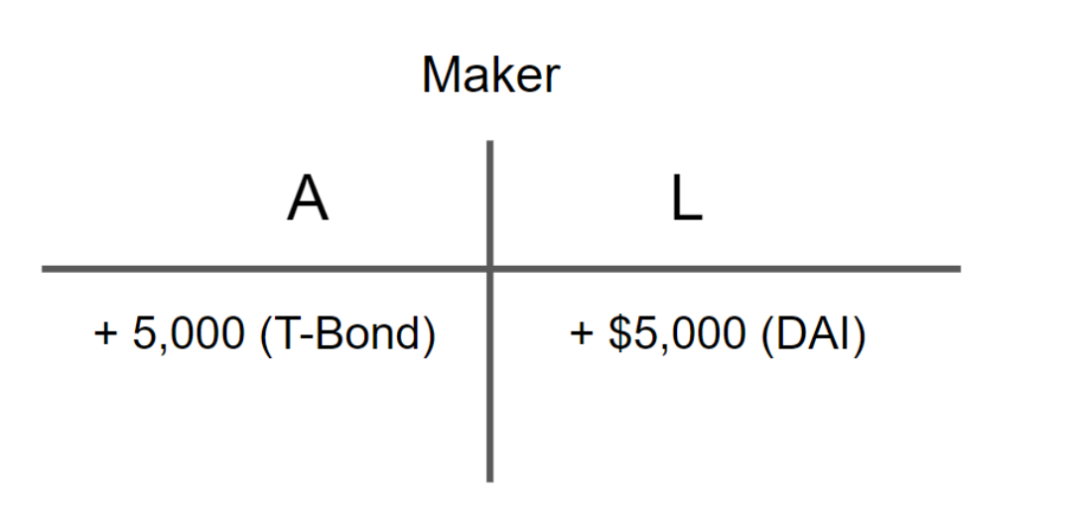

So, if Maker purchases $5,000 worth of U.S. Treasury bonds at this time, what kind of behavior is this? Here, Maker acts as an algorithmic central bank, and whether the 5,000 DAI needed for purchasing bonds is taken from the treasury or newly issued, the reflection in Maker's balance sheet is consistent:

Figure 11. Incremental Balance Sheet for Maker's Purchase of U.S. Treasury Bonds

What does this simple incremental table reflect? Anyone familiar with central bank balance sheets can see at a glance that this actually indicates that Maker is creating dollar stablecoins based on U.S. Treasury bonds. In other words, Maker is sharing the right to "create currency based on U.S. Treasury bonds," which was previously monopolized by the Federal Reserve. This is undoubtedly a far-reaching action.

It can be seen that using the balance sheet tool can help us gain deeper insights.

Second, it facilitates thinking and communication. In this regard, the balance sheet is like the vertical arithmetic we learned as children, helping us organize our thoughts more systematically and standardize them, making it easier to communicate viewpoints with each other.

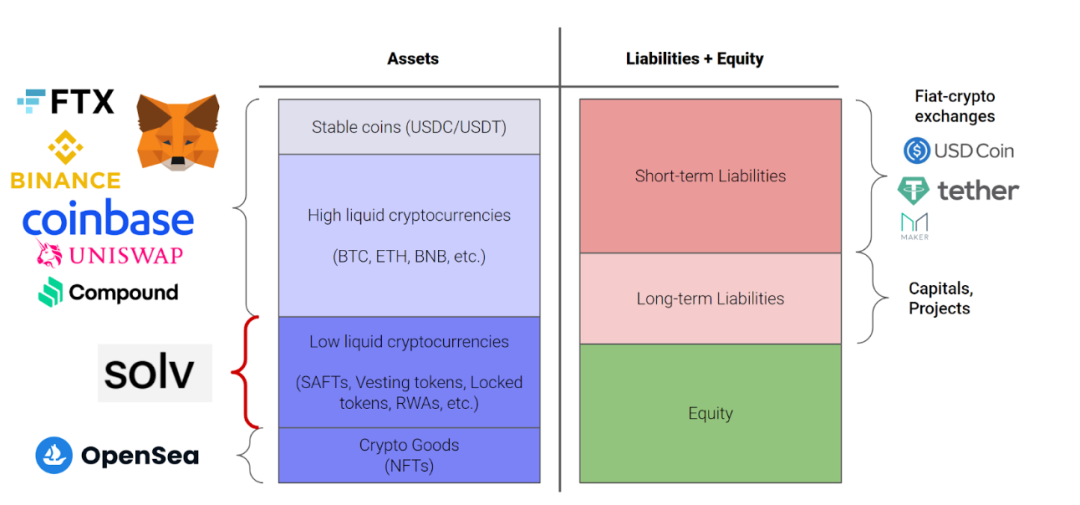

Third, it helps discover innovation opportunities and clarify business strategies. The asset insights provided by the balance sheet can sometimes help us identify market gaps and potential opportunities. Solv is such an example. As a platform supporting users to customize multidimensional assets, Solv has a clear long-term goal, but choosing the business entry point is quite challenging. During our strategic thinking, we created the following industry-wide balance sheet and identified the gap opportunities in low liquidity assets (SAFT, locked tokens, real-world assets, etc.), thus deciding to enter this field and achieving good results.

Figure 12. Balance Sheet Inspiring Solv's Business Strategy Decision

In conclusion, based on my practical experience, the balance sheet is a good tool for learning and researching Web3 digital assets, and I am happy to recommend it to everyone. I will also actively use this tool in my future articles to illustrate issues.