Sorting out the advantages and limitations of Synthetix: Will it lead the DeFi rebound?

You can have any opinion about Synthetix, but it is undeniable that they have one of the most hardcore project teams and one of the most active DAOs in the entire DeFi ecosystem.

You can have any opinion about Synthetix, but it is undeniable that they have one of the most hardcore project teams and one of the most active DAOs in the entire DeFi ecosystem.Original Title: 《The Case for SNX to go back to ATHs》

Author: Secret Salsa

Compiled by: 0x9F, 0x214, Rhythm BlockBeats

Introduction

Like any other OG DeFi project, Synthetix has experienced a crash in the past few months, with many being liquidated due to poor management of their sUSD debt positions. In fact, as the price of SNX collapsed, there was a need to increase SNX collateral or repay sUSD debt in response to margin calls to ensure the collateral ratio was appropriate.

The Synthetix debt model has always been a double-edged sword: during bull markets, degens use sUSD debt to buy other tokens or purchase more SNX, leveraging their SNX collateral positions.

As the price of SNX tokens rises, it brings them additional sUSD costs and more SNX inflation rewards, driving SNX up. But when the market turns bearish, the debt kills all speculators. They gamble and lose on their debts and cannot repay, leading to cascading liquidations of SNX.

Unsurprisingly, SNX has fallen from its all-time high (28.53 USD) to its current price (2.93 USD), a drop of 90%. However, it has risen 88% in the past month.

What Happened?

You can have any opinion about Synthetix, but it is undeniable that they have one of the most hardcore project teams and one of the most active DAOs in the entire DeFi ecosystem.

While the sUSD debt model has its drawbacks, it also has significant advantages, such as enabling atomic swaps, which allow whales to benefit from better prices by using Synthetix's synthetic assets (sUSD, sETH, sBTC, etc.).

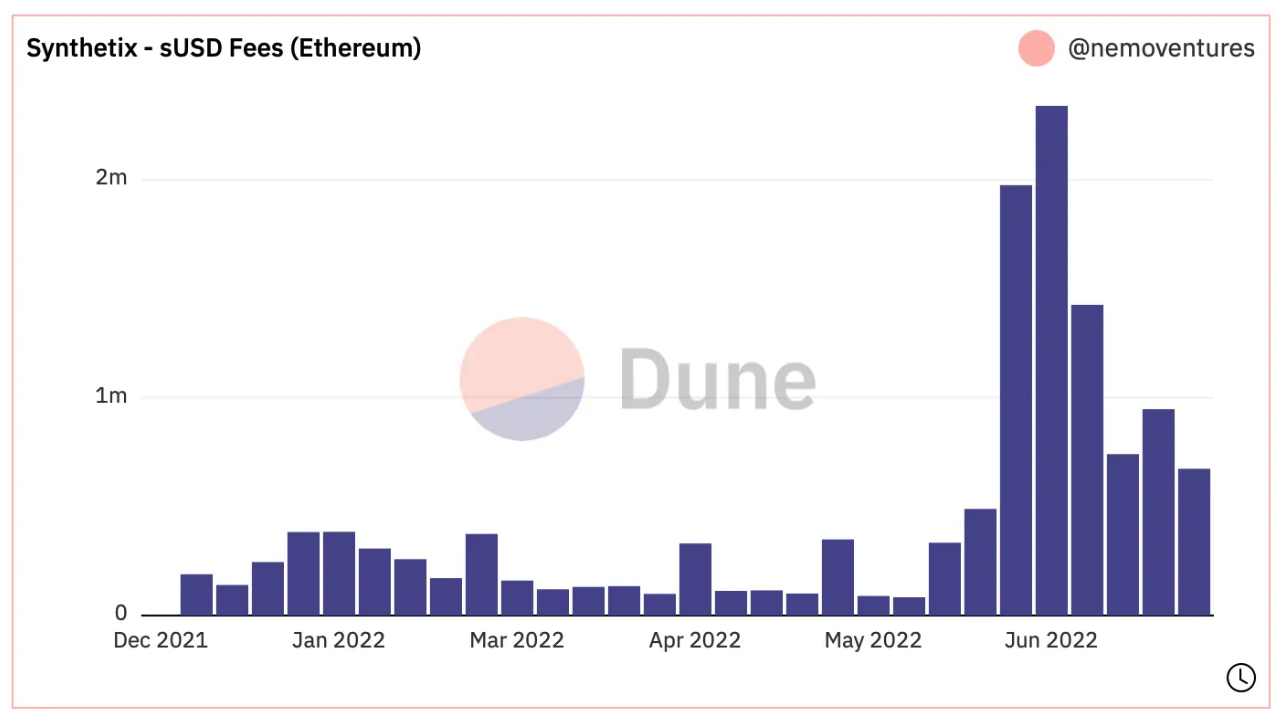

Atomic swaps have been implemented, and due to the presence of Curve liquidity pools and DEX aggregators like 1inch, they provide substantial sUSD returns to SNX stakers weekly.

In addition, Synthetix has begun to spin off other projects built on the infinite liquidity theory of sUSD, allowing large traders to trade on Synthetix without suffering slippage or spread losses as they would in traditional financial markets.

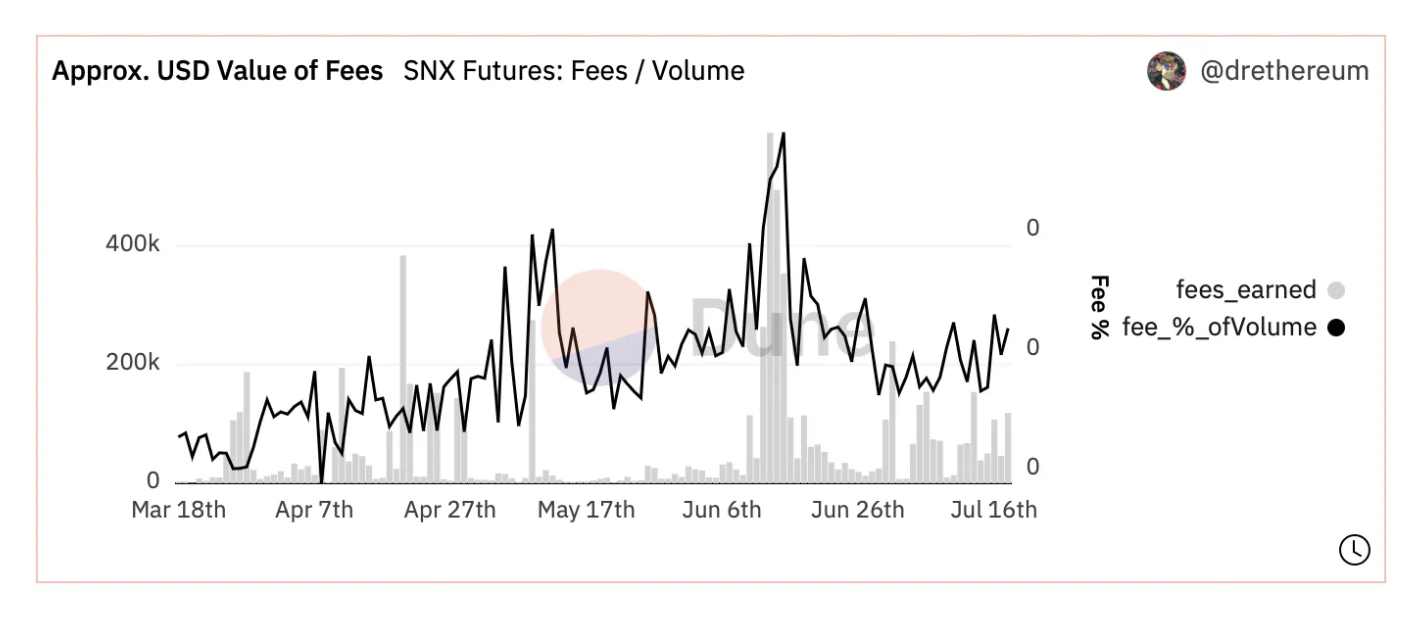

From a fee perspective, the most promising for SNX stakers is Kwenta. It has launched futures trading on Optimism L2, and trading volume has rebounded. Additionally, it has provided extra earnings for SNX stakers.

Therefore, from a fundamental perspective, these two factors are sufficient to justify the recent price surge.

But the question is, once the market stabilizes, is there enough momentum to bring SNX back to its all-time high? Because Synthetix's architecture is extremely complex and decentralized, and it is only built on Ethereum and Optimism L2.

Reasons for SNX to Return to ATH

Protocol Layer

Over the past few years, Synthetix has been in a constant state of transformation, as the project team has never settled: whether responding to crisis situations (leading early on) or implementing new features or ideas, such as atomic swaps.

Synthetix started as a DEX for trading synthetic assets, or simply put, a dApp built on Ethereum.

With the v3 launch planned for 2023, the project will be seen as a protocol layer upon which other projects can build dApps and utilize its liquidity. The more it is used and integrated with other DeFi Lego pieces, the more fees it generates. Thus, it brings fees from all over to SNX stakers.

From an integration perspective, Synthetix is also the most advanced project on Optimism L2. As Optimism grows, Synthetix will also expand. When new projects launch on Optimism, they will use Synthetix to enhance their liquidity or activity, creating synergies in various ways and increasing the usage of the Synthetix protocol. Thus, more fees are generated.

Once Synthetix v3 goes live, it will allow for rapid deployment on other L2s and possibly other L1s, such as Polygon or Avalanche (if the DAO deems it worthwhile).

Universal Cross-Chain Bridge

Once Synthetix is deployed on other L1s and L2s, it can serve as a universal cross-chain bridge or synthetic teleporters, transferring tokens and stablecoins across chains in the most efficient way: compared to traditional cross-chain bridges that rely on liquidity pools for in-and-out, Synthetix delivers faster, safer, and cheaper transactions.

Kain describes it in SIP-204:

"The vast majority of token cross-chain bridges rely on a network as the 'native' network for each token. This means that when a token is bridged, the target network receives a 'wrapped' version of that token, while the native token remains stored in the cross-chain bridge contract on the source network. This is not ideal, as it requires constant assurance of the bridge's security to maintain the value of assets on the target network. Most of these cross-chain bridges rely on multi-signature for security, putting all assets on the target network at risk."

Synthetic teleporters are not cross-chain bridges; they are another type of protocol that achieves cross-chain transfers through the burning and minting of assets.

"This ensures that the total supply of each synthetic asset remains unchanged, and there is no need to secure two versions of the same asset. In terms of cross-chain messaging, there are generally two approaches: one relies on cross-chain interoperability protocols provided by Chainlink; the other uses signature information generated by teleporters on each network to authorize the teleporters of the other party to mint assets that were previously destroyed by the source teleporter."

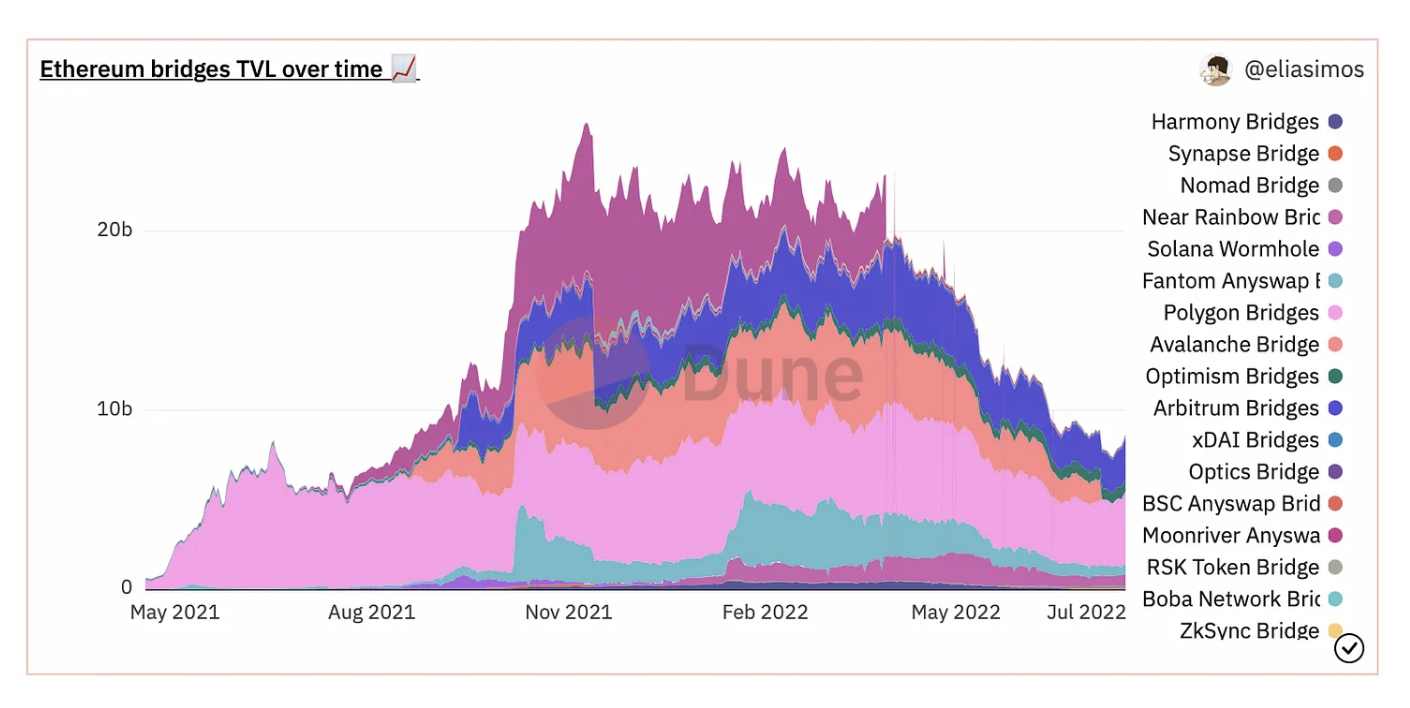

The cross-chain bridge market has immense potential, with a current TVL of 8.7 billion USD, peaking at 24 billion USD. By launching various tools, Synthetix will soon capture a share of this market.

Strong Trading Protocol

Whether for spot or leveraged decentralized trading, it has been popular for quite some time. There is significant competition among chains and protocols to attract traders.

So far, the most popular trading venue is likely dYdX, which currently operates on its own StarkNet-based L2.

dYdX has been the center of decentralized trading, or at least until recently. While having a good product is important, it is not everything. Having good token economics is equally crucial.

If this is not the case, friction will arise between users and holders. dYdX is a perfect example of "great product + poor token economics." The relative success of dYdX can be attributed to the protocol providing generous trading incentives to traders at the expense of DYDX token holders and VCs through a massive unlocking of tokens.

In contrast, both the product and token economics of Synthetix are attractive. It rewards SNX stakers through weekly dividends. Currently, the APY has remained above 100% for several consecutive weeks.

Most importantly, Synthetix is a protocol that not only supports Kwenta but also attracts many other teams willing to launch derivatives on Synthetix due to the absence of slippage, infinite liquidity, and fully customizable products.

Again, SNX stakers can earn more fees.

Two Shortcomings

sUSD Debt

It is well known that to participate in SNX staking, you need to stake your SNX and mint sUSD (which is the debt you owe to the Synthetix platform). Once you become an SNX staker, you are part of Synthetix's global debt pool.

In reality, for SNX stakers, they are counterparties to any trader holding synthetic assets provided by Synthetix (sETH, sBTC, etc.). This means that your debt position will fluctuate; if traders make money, your debt will increase, and if traders lose money, your debt will decrease.

The initial idea behind Synthetix was that traders would, on average, tend to lose money, thus allowing Synthetix to profit.

Therefore, when your debt amount changes with traders opening and closing positions, you are fully exposed to market volatility.

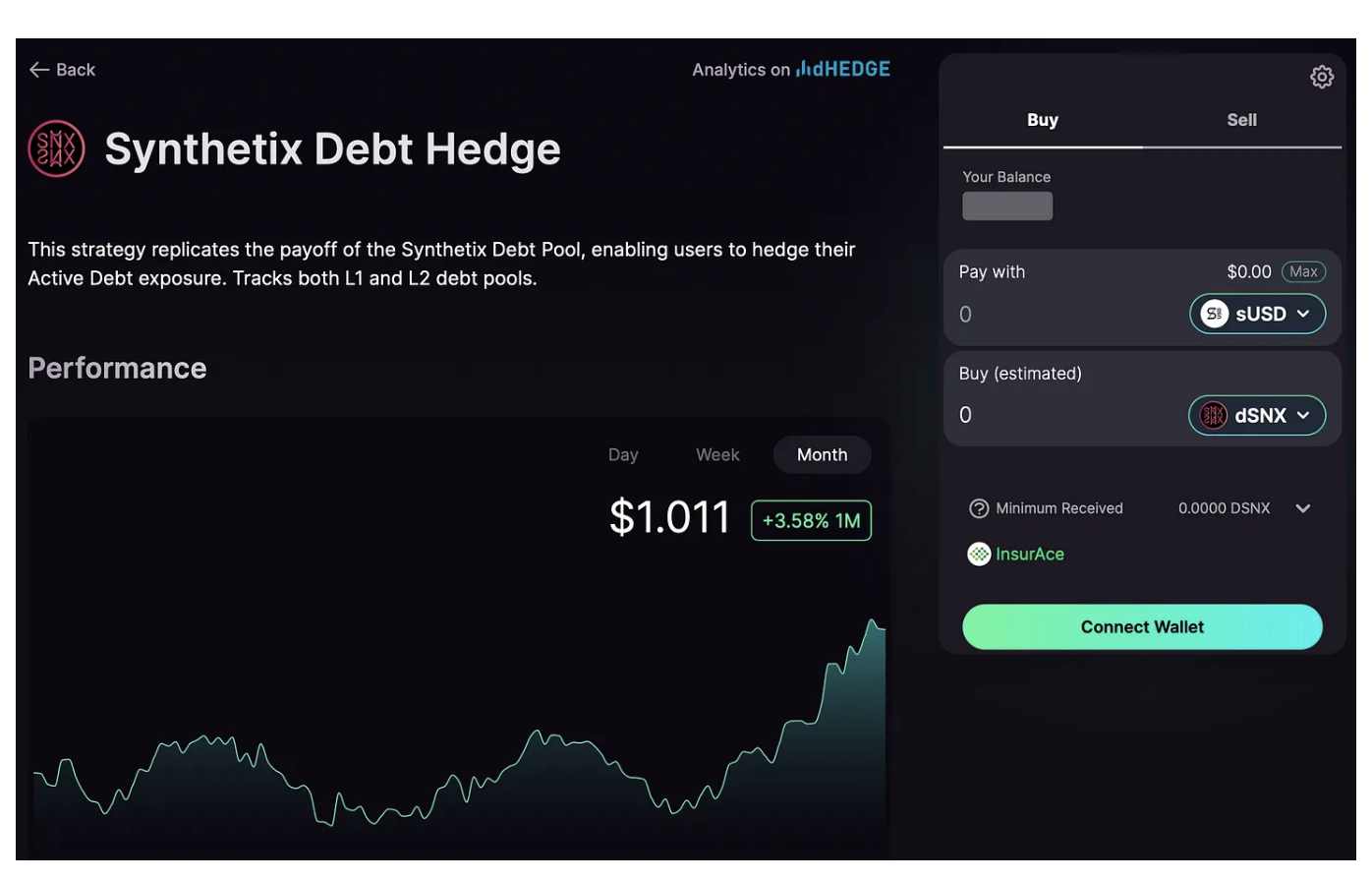

However, it is now possible to fully hedge your debt position on Optimism L2, thanks to dHedge and their spin-off, Toros. Toros allows you to purchase dSNX with the sUSD you minted, so you are not affected by market fluctuations, and your debt will not increase over time.

In practice, if you stake some SNX and mint 1000 sUSD, you now have a debt of 1000 USD, which will change with trading activity. If you want your debt to remain at 1000 USD, you can use your 1000 USD to purchase dSNX, and Toros will hedge your debt pool on your behalf. The Toros dSNX pool on the Optimism network can be accessed here.

From our perspective, the management of sUSD debt has been a major drawback of using Synthetix, as many users do not fully understand the concept or implications of sUSD debt.

Now that you can hedge your debt, Synthetix becomes more user-friendly for those who do not want to manage their positions 24/7.

sUSD Liquidity on Optimism

Do Kwon has a famous saying, "Your scale is not scale," and this is even more true on Optimism.

The liquidity of sUSD on Optimism is poor, so no whales can execute trades on Kwenta.

However, this is about to change, as Synthetix has launched an sUSD cross-chain bridge between Ethereum and Optimism, allowing you to purchase large amounts of sUSD on Ethereum and bridge it to Optimism to start trading. The only downside is that once you want to bridge back from Optimism to Ethereum, you need to wait 7 days. Synthetic teleporters are not available yet.

To see how to bridge sUSD, click to view the tutorial.

Risks

The main risks are well known:

- Regulation: If Mr. Gensler (Chairman of the SEC) is responsible for regulating DeFi worldwide and sets his sights on Synthetix.

- Hacks/Vulnerabilities: Synthetix is a complex protocol, so hackers may find a vulnerability. This is clearly not easy, as Synthetix has invested heavily in security and has not been truly hacked so far (perhaps except for front-end operational failures, which are issues with the system itself).

Conclusion

Synthetix has been tirelessly pushing the development of the protocol for years, and their dedication continues to amaze. Moreover, the protocol has a strong foundation, good token economics (which will change with the introduction of veSNX), and an ambitious roadmap.

The roadmap is grand, and the planned launch of Synthetix v3 in 2023 will undoubtedly bring more fees to SNX stakers. Given Synthetix's progress in various aspects and their strategy of generating fees for SNX stakers, it is hard to be bearish on Synthetix. Because this is clearly a winning strategy—more fees mean SNX stakers will receive more dividends.

We cannot predict the future, so we do not know whether the current bear market has ended or will last for another year or more. But we believe that later this year and in 2023, the trading volume related to Synthetix across all dApps will soar (once v3 goes live, the trading volume will be even greater).

If that is the case, SNX will eventually return to ATH.