A Detailed Explanation of Morpho: A Lending Protocol Aggregator Optimizing Capital Efficiency

Morpho builds an aggregator based on existing PLFs such as Compound and AAVE, aiming to optimize the capital efficiency of lending protocols. By implementing "Pareto improvements" on existing PLFs, it attracts more users to the Morpho protocol.

Morpho builds an aggregator based on existing PLFs such as Compound and AAVE, aiming to optimize the capital efficiency of lending protocols. By implementing "Pareto improvements" on existing PLFs, it attracts more users to the Morpho protocol.Author*: ** @jokenomicser, Defieye*

On July 12, the DeFi lending protocol Morpho completed a $18 million funding round, led by a16z and Variant, with investors including Nascent, Semantic Ventures, Cherry Crypto, Mechanism Capital, Spark Capital, Standard Crypto, and Coinbase Ventures.

The morpho protocol was co-founded by Paul Frambot, a student in engineering at the Paris Telecom and Polytechnic Institute, and Vincent Danos, a research director at CNRS, aiming to create a more efficient lending protocol. It is based on existing lending protocols and creates a new peer-to-peer mechanism that can provide higher returns for investors. What are the specific details? Let's take a look together.

1: The Current State of Peer-to-Pool Protocols

To understand the new lending protocol, we first need to understand what traditional lending protocols look like. We will introduce two established lending protocols, AAVE and Compound. If you are already familiar with this, you can skip to the second section.

The basic principle of AAVE or Compound is simple: lenders supply their crypto assets to the protocol's lending pool and receive an APY incentive (referred to as lender APY hereafter); these cryptocurrencies are sent to the corresponding contract in the pool, which returns corresponding interest certificates (such as Compound's cToken or AAVE's aToken). Borrowers, on the other hand, must first provide sufficient collateral, and under a certain collateralization ratio, they can borrow assets from the pool within a limited amount, for which they need to pay a certain interest (referred to as borrower APY hereafter).

It can be seen that on-chain lending protocols differ from traditional loans in two significant ways: ① On-chain, credit cannot be verified, so borrowers must first be lenders (i.e., over-collateralized), which reduces capital efficiency and limits use cases. ② There are no maturity limits on loans (no agreed repayment date); as long as the collateralization ratio requirements are met, borrowers can use the loan indefinitely by only paying interest.

Whether for borrowers or lenders, their interactions with the protocol are "peer-to-pool"; borrowers and lenders cannot be directly linked. The peer-to-pool model is a major breakthrough in DeFi, with many advantages:

① Instant liquidity. As long as there is liquidity in the pool, borrowers can borrow at any time, and lenders can retrieve their assets at any time.

② A stable earning environment. Lenders only need to inject funds into the pool to enjoy stable interest without worrying about whether their assets are actually being borrowed.

③ Transparent lending rates. The interest rates for both parties are defined by the utilization rate of the assets in the pool; if the utilization rate is low, borrowing rates will become very low to attract borrowers.

④ Permanent borrowing—no expiration date.

⑤ Allows individual liquidity swapping. Since lending protocols use over-collateralization, if users engage in borrowing and lending simultaneously, it is equivalent to swapping liquidity while "bullish" on the collateralized assets. For example, if A has 10 ETH and believes that ETH will rise from $1200 to $1600 in three months, he does not want to spend his ETH; at the same time, he urgently needs some liquidity, he can deposit these 10 ETH into the lending protocol and borrow $10,000 at a 120% collateralization ratio to meet his urgent needs.

Of course, the "peer-to-pool" model also has some issues:

① Low capital efficiency. Since "peer-to-pool" does not match lending demand, when borrowing demand is insufficient, a large amount of capital remains idle in the pool and is not effectively utilized; at the same time, over-collateralization itself has already reduced the utilization rate of funds. Similar to the real world, a large amount of borrowing demand based on the credit system cannot be discovered.

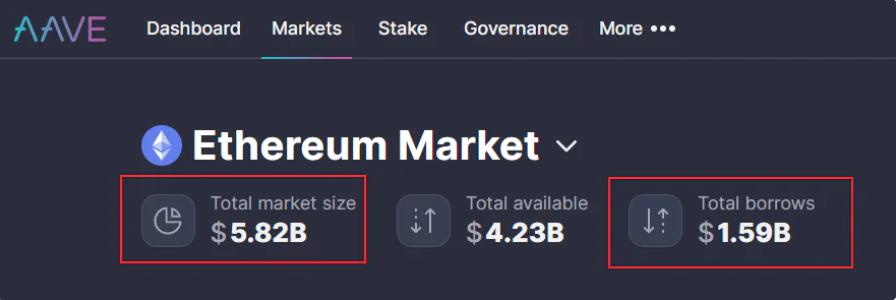

AAVE's lending pool on ETH has a utilization rate of less than 30%

AAVE's lending pool on ETH has a utilization rate of less than 30%

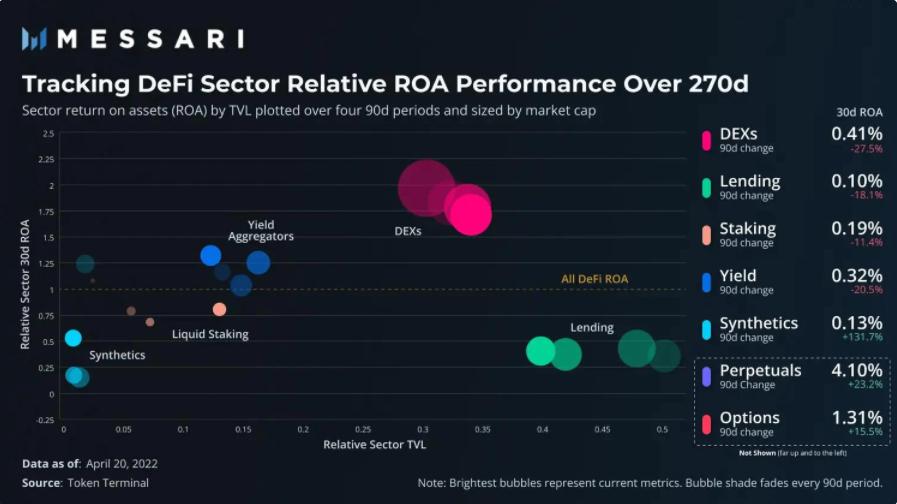

Lending protocols lock up over 40% of DeFi liquidity, about 1.5 times that of DEX, yet their 30d-ROA is only 1/4 of that of DEX.

② Large borrowing-lending spread. Most lending protocols have borrowing APYs that are much higher than lending APYs, largely due to low capital utilization—lenders face the lending pool equally, and regardless of whether funds are idle, they will receive rewards, which can only come from the "sharing" of the interest paid by borrowers.

③ Lack of market adjustment for interest rates. Most existing lending protocols use known algorithms to determine interest rate formulas and adjust them through DAO governance (such as Compound), making it impossible for lending rates to correctly match market supply and demand—there is no competition among lenders, and borrowers do not benefit.

2: The Current State of Peer-to-Peer Protocols

Before the emergence of the "peer-to-pool" model, ETHLend attempted a "peer-to-peer" lending model as early as 2017, but it did not succeed until it was integrated into a new company: AAVE (and joined the "peer-to-pool" army).

So why did "peer-to-peer" fail?

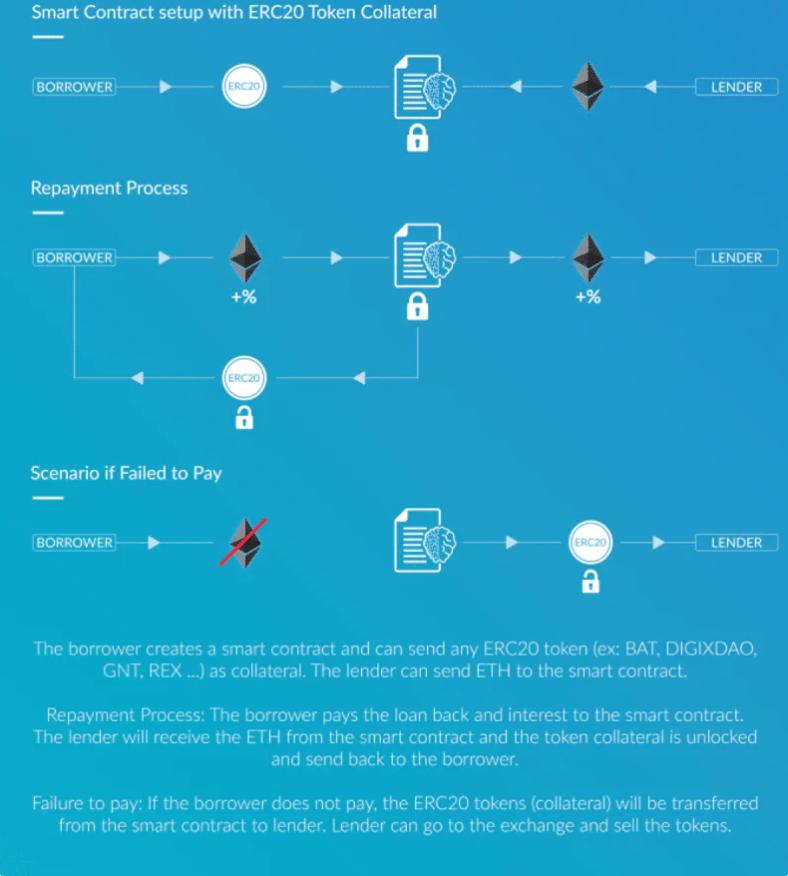

First, let's look at the workflow of ETHLend:

① Borrowers create smart contracts through the ETHLend interface to request ETH loans within predefined terms and interest rates. They then provide any ERC20 token of their choice as collateral. The collateral amount is defined by the borrower.

② Potential lenders can browse all pending offers and accept the ones they want. Once accepted, the borrower will receive the requested ETH, and their collateral will be locked.

③ Upon maturity, the borrower will repay the interest to the lender and retrieve the collateral. In the case of default, the lender will receive the collateral (instead of ETH).

Source: https://github.com/ETHLend/Documentation/blob/master/ETHLendWhitePaper.md

Source: https://github.com/ETHLend/Documentation/blob/master/ETHLendWhitePaper.md

This model is very close to the original lending market: borrowers first express their borrowing needs and provide collateral to find suitable lenders. As we perceive in daily life, those who want to borrow money always first state how much they want to borrow and offer what benefits they can provide to encourage others to lend to them, as well as what items they can pledge.

What are the benefits of this approach?

① High capital efficiency. The money lent by lenders is 100% used by borrowers, so the interest rate received by lenders is also relatively high.

② Unpermissioned collateral. Borrowers can pledge any ERC20 instead of being limited to the few pre-approved in the "peer-to-pool" model. This is because lenders have the active choice, and peer-to-peer matching does not require platform permission.

③ Free matching of demand and complete satisfaction. In this model, once the borrower and lender are matched, it means that both parties' demands are fully satisfied. Lenders can freely assess borrowers, and borrowers can offer different rates based on their urgency.

Similarly, ETHLend's "peer-to-peer" model has many drawbacks:

① Fixed-term loans. Borrowers must set reasonable conditions when posting borrowing needs to seek lender acceptance. If a borrower requests a permanent loan, it means they must offer high interest to attract lenders, which is unrealistic.

② If the borrower defaults, the lender cannot retrieve their assets and can only be compensated with the borrower's collateral.

③ Lack of a liquidation mechanism. The collateral setup requires lenders to predict the price fluctuations of the collateral; if the collateral falls below the loan amount, the borrower has an incentive to default, resulting in losses for the lender.

④ Waiting period for matching. Peer-to-peer matching is a lengthy process, while borrowers' needs are often immediate.

In summary, the year ETHLend was born, 2017, was still the early stage of DeFi, when there were even no DEXs, making it difficult for many infrastructures to keep up, such as price-providing oracles and liquidity-providing AMMs. This made ETHLend's failure an inevitable outcome of being out of time. It was not until the ETHLend team turned to the peer-to-pool model of AAVE that the lending giant of today was created.

3: Introduction to Morpho and Its Core Advantages

Comparing the "peer-to-pool" and "peer-to-peer" models, we can see that both have their strengths and weaknesses, summarized in the table below:

Is there a model that can effectively combine the advantages of both "peer-to-pool" and "peer-to-peer"?

Finally, we arrive at the main topic—this is where the Morpho protocol comes into play.

Morpho is essentially an aggregator based on existing lending protocols, which seamlessly matches users in a peer-to-peer manner while providing the same liquidity, improving the capital efficiency of lending pool positions and enhancing the experience for both borrowers and lenders.

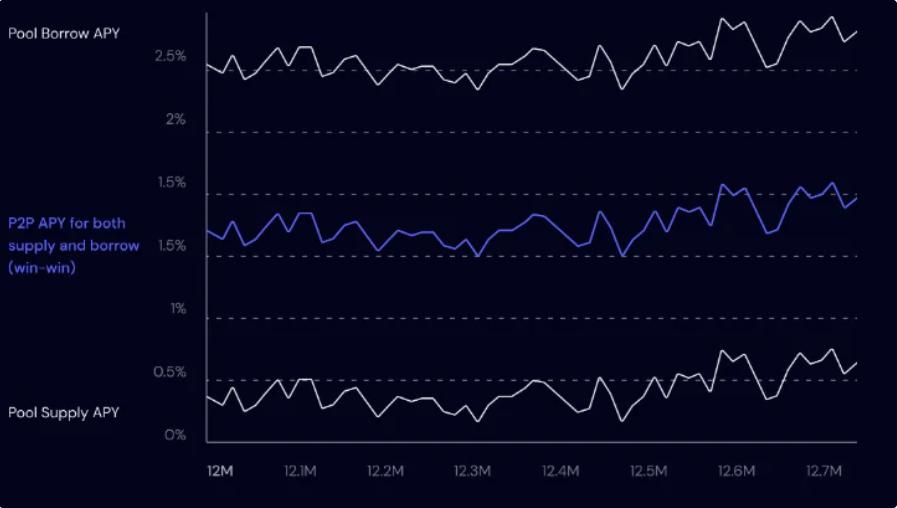

Taking the underlying lending pool of Compound as an example, whether users directly use Morpho or deposit assets into Compound to obtain cTokens and then deposit them into Morpho, they can normally receive lender APY. At the same time, Morpho will match the borrower for that user, and when a borrower is matched, both parties will receive an improved P2P APY, which is higher than the lender APY and lower than the borrower APY, providing better incentives for both sides.

Morpho protocol interface. P2P APY becomes an attractive option for both borrowers and lenders

P2P APY can be seen as the average of borrower APY and lender APY.

Debt Tracking Mechanism

To simultaneously track all users' debt and deposit balances, Morpho separates deposit balances and borrowings into two variables: onComp and inP2P. onComp is measured in cToken/aToken, while inP2P is measured in similar mToken to describe debt.

For example, suppose 1 ETH = 100 cETH, A deposits 1 ETH into Morpho, and his balance is:

onComp: 100 cETH; inP2P: 0 mETH;

Now B borrows 1 ETH (matched with A), assuming 1 ETH = 100 mETH, A's balance will change to:

onComp: 0 cETH; inP2P: 100 mETH;

A year later, if the P2P APY remains at 1.5%, then the price of mETH at that time will be 1 ETH = 98.5 mETH.

Matching Engine

P2P still cannot fully balance supply and demand; there will always be situations where the number of depositors n is greater than the number of borrowers k. To address this, Morpho has designed a "matching engine," which will select k depositors to enjoy P2P APY, while the remaining n-k will still remain in the underlying lending pool to enjoy the original interest rate. This means that even if users are not matched, Morpho can still ensure that the rate is at least not lower than that of the underlying lending pool like Compound.

Token Economics

The protocol has its own token $MORPHO, and currently, only the use cases of $MORPHO are known. $MORPHO can be used to participate in protocol governance, influence the matching engine, and incentivize certain behaviors beneficial to the protocol, such as liquidity mining programs.

For example, regarding the influence on the matching engine, a well-behaved user can receive a better rate experience than an ordinary user; another example is the matching rule known as the "spectrum model," where users can stake their $MORPHO tokens to have "bandwidth" proportional to their staked share, and whenever a borrower initiates a loan, the protocol will select depositors to match based on "bandwidth" proportions.

Morpho has defined numerous use cases for its token to highlight its practicality. Regarding token flow, token distribution, release, etc., the protocol is still in its early stages, and the official website has not disclosed relevant information.

Core Advantages of Morpho

Thus, Morpho establishes its core advantages:

① Instant liquidity. Morpho is built on top of the underlying lending pool, allowing both borrowers and lenders to enter and exit the protocol at any time, regardless of whether they are matched in a peer-to-peer manner.

② Stable earnings, with a higher expected return than existing peer-to-pool models.

③ Transparent lending rates, determined by the market. In future versions of Morpho, a lender competition mechanism will be introduced, which will lower costs for borrowers and also promote increased capital efficiency.

④ Perpetual borrowing. This continues the advantages of the peer-to-pool model.

⑤ Convenience. As an aggregator, users can completely avoid interacting with various underlying lending pools and only need to perform simple operations in Morpho.

⑥ High capital efficiency. Lenders' funds are either in the lending pool or matched (fully utilized).

⑦ Ample liquidity support. This will occur as more lending protocols are aggregated.

4: The Current Status and Future of Morpho

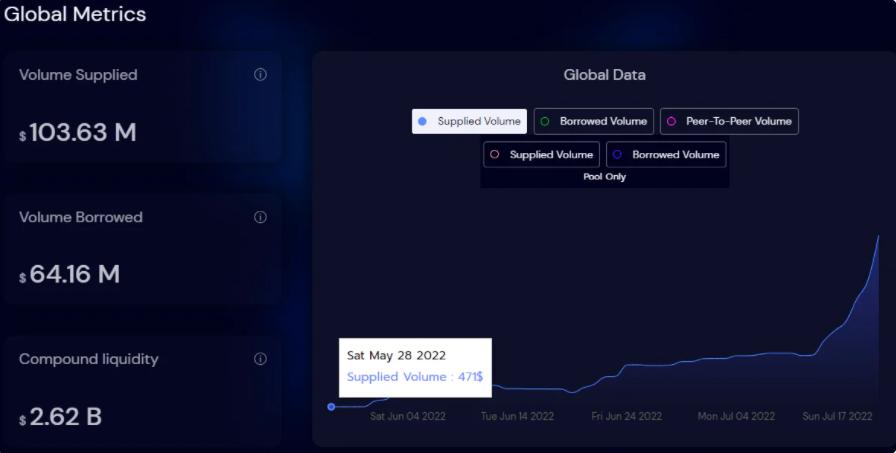

Morpho currently only supports the underlying lending pool of Compound. On Morpho's official analytics page, it can be seen that since the launch at the end of May, the liquidity absorbed by the Morpho protocol has been continuously growing and has recently surged, with liquidity provided by lenders exceeding $100 million. The borrowing amount has reached $60 million, with a utilization rate exceeding 60%, far surpassing AAVE's 30%.

Morpho's matching engine has also performed well, completing $20 million worth of peer-to-peer matching, with a matching efficiency exceeding 90%.

On July 14, Morpho's 【Epoch 1】 ended, and 350,000 $MORPHO tokens will be distributed to participating users. This token is in ERC-20 format and is currently non-transferable; governance will vote to activate its transferability in the coming months. Meanwhile, 【Epoch 2】 has begun, with a total of 1.7 million MORPHO tokens allocated to those who deposit and borrow on Morpho.

Morpho is actively integrating with AAVE's lending pool. According to the Compound official website, the total liquidity provided by lenders has reached $3.6 billion, while AAVE has $6 billion. Given the $100 million liquidity that Morpho has already absorbed, it still has enormous room for growth (Morpho does not compete with the underlying lending protocols).

In the initial white paper, three steps of protocol evolution are envisioned:

① Liquidity Optimizer (Caterpillar). Morpho currently only supports Compound, with plans to incorporate more underlying lending pools like AAVE in the future. After aggregating liquidity, Morpho will provide users with a better instant experience. Users will always be able to find the corresponding underlying pool to propose their liquidity; for example, users may not be able to withdraw funds from Compound but can do so from AAVE.

② Interest Rate Competitive Market (Chrysalis). A significant change that Morpho brings to the lending market is that lenders will be able to compete freely on rates, rather than being forced to accept the inefficient existing lending pool rates or intermediary rates. This was already seen in the ETHLend product, but at that time, the basic conditions were lacking; Morpho relies on liquidity aggregation to achieve this.

③ Ideal Order Book Model (Butterfly). Butterfly is the long-term vision of the Morpho protocol, at which point Morpho will break free from dependence on the underlying PLF and appear in a more universal order book form, with borrowers and lenders acting as buyers and sellers, proposing orders for the underlying assets. Each proposed position will be connected by Morpho in an instant, automatic, and efficient manner.

Morpho builds an aggregator based on existing PLFs like Compound and AAVE, aiming to optimize the capital efficiency of lending protocols by "Pareto improvement" of existing PLFs, attracting more users to switch to the Morpho protocol. Morpho's vision may be to become a key component of the future DeFi Lego tower; how far it can go, we will wait and see.

Risk Warning:

Liquidation risk. Borrowing that has entered peer-to-peer matching does not have liquidation risk; moreover, even if the borrower cannot repay, their collateral will be used in the underlying lending pool, ensuring that lenders can still receive protection from the liquidity pool. Therefore, Morpho's liquidation risk comes from the underlying lending pool.

Protocol risk. Currently, the protocol code has undergone multiple audits (the following are the auditors listed on the official website):

References

Official website: https://compound.morpho.xyz/

Documentation: https://docs.morpho.xyz/

Others:

Risk warning Risk warning

Risk warning Risk warning