Finance × Metaverse: A Financial System Advancing Through the Integration of Virtual and Real Worlds

This article discusses the rich possibilities and related challenges of the integration and development of the financial system and the metaverse from a practical perspective.

This article discusses the rich possibilities and related challenges of the integration and development of the financial system and the metaverse from a practical perspective.Author: CICC

In recent years, "DeFi," cryptocurrencies, and other related concepts have rapidly developed in some overseas countries, but they have also sparked many controversies. Some viewpoints suggest that with the gradual maturity of the metaverse concept, a financial system based on cryptocurrencies and "DeFi," integrating decentralized ideas, may emerge. Others argue that cryptocurrencies are a worthless bubble and that the integration of the metaverse and the financial system must be grounded in reality. This article discusses the rich possibilities and related challenges of the integration of the financial system and the metaverse from a practical perspective.

Abstract

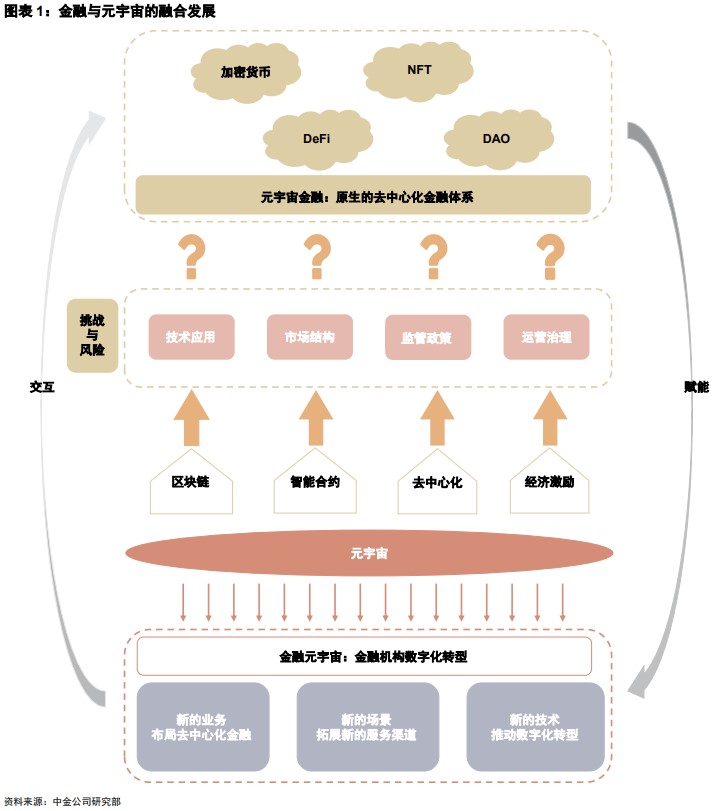

Two paths for the integration of the metaverse and the financial system: "Metaverse Finance" vs. "Financial Metaverse." The metaverse is a digital world built on technologies such as mixed reality and digital modeling, characterized by decentralized ideas and a new economic, identity, and institutional system. The "virtual world of the metaverse" represents our desire for a "new life" and our infinite imagination of the unknown world. In our visions, we make it all-encompassing to meet everyone's expectations. However, for traditional financial institutions wishing to participate in the construction of the metaverse, such a virtual world may seem too distant and the entry points too vague. From a realistic perspective, we believe that the integration of the financial system and the metaverse is more likely to stem from the development of underlying technologies of the metaverse and the extension of scenarios, bringing new development opportunities to the financial system based on technology and scenarios, with two development paths: "Metaverse Finance" and "Financial Metaverse."

"Metaverse Finance": Supporting economic activities in the metaverse within a decentralized narrative framework. Based on our definition of the metaverse, we believe that the financial system within the metaverse will be grounded in decentralized ideas and distributed ledger technologies (such as blockchain), starting with payments and gradually developing into various subfields of financial activities such as lending and trading, and further expanding into dimensions like asset rights confirmation and social organization, thereby supporting economic activities in the metaverse under a decentralized framework. Currently, due to varying degrees of acceptance of "Metaverse Finance" across different countries and regions, its development faces challenges and risks from multiple aspects, including technology, market, operations, and regulation. Looking ahead, we believe that under the current national sovereignty and social structure, a fully decentralized metaverse financial system is unlikely to exist widely. However, its decentralized concepts, blockchain and smart contract technologies, and some innovative models can still provide beneficial references for the development of the financial system.

"Financial Metaverse": The metaverse concept and technology provide imaginative space for the digital transformation of financial institutions. On one hand, as the metaverse gradually advances, the application of its underlying technologies, such as modeling and rendering, interaction technology, the Internet of Things, network computing power, blockchain, and artificial intelligence, is expected to accelerate, and we believe that financial institutions will benefit from the rapid development of these technologies, better achieving digital transformation goals such as business innovation, process reengineering, and organizational change. On the other hand, the metaverse paints a picture of a virtual world with digital-native capabilities, even possessing a complete economic and social system. We believe that the immersive experience and the realism of virtual elements brought by the metaverse will provide richer imaginative space for financial institutions in aspects such as online collaboration, online business development, and customer experience upgrades.

Risks: Uncertainty in industry policy regulation; technology development falling short of expectations; commercialization processes not meeting expectations.

Main Text

Two paths for the integration of the metaverse and finance: "Metaverse Finance" vs. "Financial Metaverse"

Referring to the CICC TMT group's report "Metaverse: Spatial Elevation, Temporal Extension, Social Reconstruction," the metaverse is a digital world built on technologies such as mixed reality and digital modeling, characterized by decentralized ideas and a new economic, identity, and institutional system. The "virtual world of the metaverse" represents our desire for a "new life" and our infinite imagination of the unknown world. In our visions, we make it all-encompassing to meet everyone's expectations. However, for traditional financial institutions wishing to participate in the construction of the metaverse, such a virtual world may seem too distant and the entry points too vague. From a realistic perspective, we believe that the integration of the financial system and the metaverse is more likely to stem from the development of underlying technologies of the metaverse and the extension of scenarios, bringing new development opportunities to the financial system.

In recent years, decentralized financial systems represented by cryptocurrencies have developed rapidly in some overseas countries, but they have also sparked many controversies. Some viewpoints suggest that with the gradual maturity of the metaverse concept, a financial system based on cryptocurrencies and "DeFi," integrating decentralized ideas, may emerge. Others argue that cryptocurrencies are a worthless bubble and that the integration of the metaverse and finance must ultimately be grounded in real-world development. Meanwhile, we also see an increasing number of financial institutions treating the metaverse as one of the levers for digital transformation, exploring new financial services around the development of the metaverse on one hand, and focusing on leveraging metaverse-related technologies and scenarios to empower their digital transformation and expand new channels on the other.

Therefore, we believe that the integration of finance and the metaverse can be divided into two paths: 1) "Metaverse Finance": Based on our definition of the metaverse, we believe that the financial system within the metaverse will be grounded in decentralized ideas and distributed ledger technologies (such as blockchain), starting with payments and gradually developing into various subfields of financial activities such as lending and trading, and further expanding into dimensions like asset rights confirmation and social organization, thereby supporting economic activities in the metaverse under a decentralized framework; 2) "Financial Metaverse": Against the backdrop of the ongoing acceleration of digital transformation in financial institutions, the maturity of the underlying technologies of the metaverse and the continuous extension of its scenarios are expected to further promote the digital transformation of financial institutions, bringing more possibilities for their digital transformation paths and ultimate forms.

"Metaverse Finance": Supporting economic activities in the metaverse within a decentralized narrative framework

Overall, Metaverse Finance has developed rapidly in recent years, characterized by rapid user growth, continuous innovation in product functions, and ongoing expansion of service dimensions. However, compared to traditional financial systems, its scale remains relatively small, and its penetration into the real economy is still low, currently unable to widely serve real-world financial needs, leaving its future prospects somewhat uncertain.

At the same time, Metaverse Finance also faces challenges and risks from multiple aspects, including technology, market, operations, and regulation, such as: 1) Defects in technology application leading to structural issues within Metaverse Finance; 2) Over-centralization of power and inefficiency in operational governance causing Metaverse Finance to lose competitiveness and attractiveness; 3) Excessive speculative trading and high leverage in market structure potentially triggering systemic risks, impacting the trust and consensus in Metaverse Finance; 4) Significant differences in regulatory policies across countries, leading to fragmentation in the development of Metaverse Finance.

Looking ahead, we believe that under the current national sovereignty and social structure, a fully decentralized Metaverse financial system is unlikely to exist widely. However, its decentralized concepts, blockchain and smart contract technologies, and some innovative models can still provide beneficial references for the development of the financial system.

At the same time, we believe that the future of Metaverse Finance may be built on central banks and other regulatory institutions, with centralized and decentralized financial institutions as operational entities, creating a more transparent, efficient, and inclusive financial system. In the process of integrating the metaverse with traditional financial systems, Metaverse Finance may gradually be incorporated into regulatory frameworks, establish compliance entry points, enhance the stability of the financial system, and empower traditional financial systems, continuously optimizing the efficiency and experience of traditional financial services, reducing intermediary issues, lowering operational costs, and lowering user entry barriers.

"Financial Metaverse": The metaverse technology and scenarios provide more possibilities for the digital transformation of financial institutions

From a practical perspective, as the digital transformation of financial institutions continues to accelerate, we believe that the "metaverse" holds more realistic significance for traditional financial institutions, stemming from the continuous maturity of its underlying technologies and the imaginative space brought by the continuous extension of its scenarios, which is expected to further promote the digital transformation of financial institutions and provide richer possibilities and imaginative space for their digital transformation paths and ultimate forms.

On one hand, as the "metaverse" gradually advances, the application of its underlying technologies, such as modeling and rendering, interaction technology, the Internet of Things, network computing power, blockchain, and artificial intelligence, is expected to accelerate, and we believe that financial institutions will benefit from the rapid development of these technologies, better achieving digital transformation goals such as business innovation, process reengineering, and organizational change; on the other hand, the metaverse paints a picture of a virtual world with digital-native capabilities, even possessing a complete economic and social system. We believe that the immersive experience and the realism of virtual elements brought by the metaverse will provide richer imaginative space for financial institutions in aspects such as online collaboration, online business development, and customer experience upgrades.

Metaverse Finance is developing rapidly but still faces many challenges; in the future, it may integrate with centralized systems.

The development of the Metaverse financial system is rapid, but there is a trend of "detaching from reality" and asset bubbles.

Within the decentralized narrative framework, the Metaverse financial system starts with basic payments and gradually develops into various subfields of financial activities such as lending and trading, further expanding into dimensions like asset rights confirmation and social organization. Overall, Metaverse Finance has developed rapidly in recent years, but compared to traditional financial systems, its scale remains relatively small, and its future prospects are still somewhat uncertain.

Payment and settlement: "Detaching from reality" of cryptocurrencies

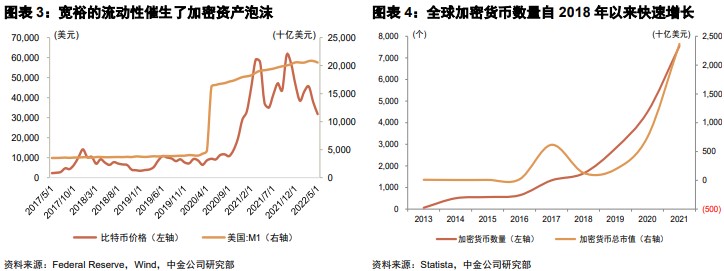

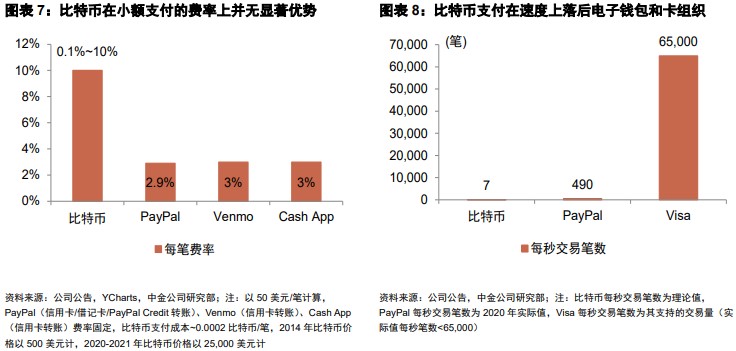

Bitcoin, as the starting point of cryptocurrencies, was designed to operate as a peer-to-peer electronic cash system that could function without intermediaries. However, although the number of cryptocurrencies has exploded in the past decade, with the overall market value growing to $2.37 trillion by the end of 2021, their use has primarily been concentrated in speculative trading within the crypto economy, with little empowerment of the payment and settlement processes in the real economy, presenting a trend of "detaching from reality" and forming a significant price bubble.

We believe that the decoupling of cryptocurrencies from payment and settlement activities is primarily due to: 1) The lack of intrinsic value and the absence of centralized institutional endorsement make it difficult for them to fulfill monetary functions; 2) The decentralized payment and settlement system faces the "impossible triangle," making it challenging for cryptocurrencies to ensure security while achieving scalability; 3) The current digital payment and settlement system is already quite efficient, with a well-established bilateral network and user habits, making it difficult for cryptocurrencies to compete.

First, cryptocurrencies exhibit significant price volatility, and most lack intrinsic value, making it difficult to fulfill basic monetary functions. Cryptocurrencies primarily rely on unstable "consensus" without intermediary endorsement to form prices. However, since most cryptocurrencies are decoupled from the real economy and lack intrinsic value, the "consensus" of their investors is difficult to maintain, leading to significant price fluctuations and making it challenging for cryptocurrencies to fulfill basic monetary functions. The subsequent influx of speculative investors further drives speculative trading, creating a vicious cycle that detaches cryptocurrencies with peer-to-peer decentralized payment functions from real payment and settlement demands.

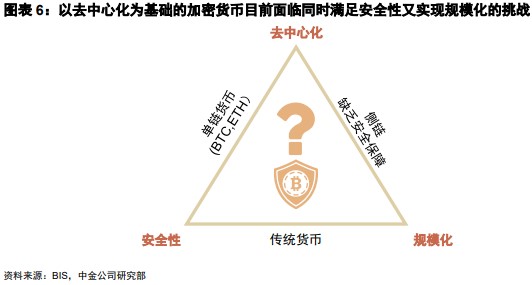

Secondly, based on decentralization, cryptocurrencies currently face challenges in ensuring security while achieving scalability. Cryptocurrencies built on public chains require reasonable incentives to attract participants (such as "miners") to support the operation of the public chain. As the scale of public chains expands and performance improves, their transaction costs may decline, leading to a decrease in economic incentives. Therefore, to achieve further scalability, decentralized public chains need to establish economic mechanisms that can support both scale expansion and performance upgrades while continuously providing high incentives. While cross-chain protocols can enhance interoperability between blockchains and increase the upper limit of blockchain transaction scales, there is still room for improvement in security guarantees.

Finally, the existing digital payment and settlement systems are already quite efficient, making it difficult for cryptocurrencies to achieve disruption in the payment field. 1) In terms of payment performance, since cryptocurrencies are designed primarily to ensure decentralized consensus and security, they still lag behind leading electronic payment companies; 2) In terms of bilateral network scale, the current penetration of cryptocurrencies into the real economy remains low, relying more on electronic payment companies (such as Shopify, Visa) for support, with payment transactions still operating within centralized systems; 3) In terms of user habits, bank cards and electronic wallets remain the preferred digital payment methods. Even if user experiences are similar, cryptocurrencies find it challenging to disrupt established user habits.

DeFi: An incomplete mapping of the traditional financial system

The concept of decentralized finance (DeFi) emerged in 2018, when Brendan Forster announced the birth of the DeFi concept in "Announcing De.Fi, A Community for Decentralized Finance Platforms": a financial system built on decentralized blockchain technology, fully open-source, and with a stable developer platform.

Overall, DeFi does not rely on centralized intermediaries such as brokers, exchanges, or banks, but instead utilizes smart contracts on the blockchain to complete financial transactions. The core feature of "idealized DeFi" is that no participant can unilaterally perform: 1) Control of accounts; 2) Review of transaction execution; 3) Review of protocol execution.

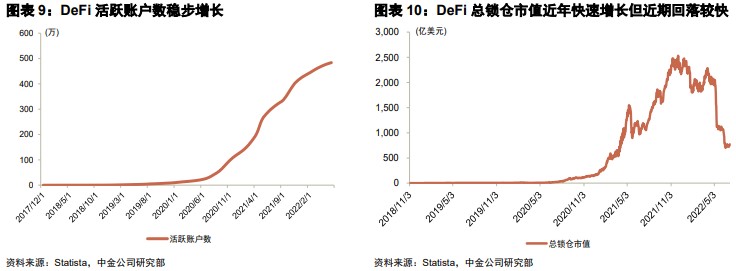

As of the end of June 2022, according to Statista, the total locked value (TVL) of DeFi reached $77.05 billion, with a total of 4.825 million active accounts. However, its penetration into economic activities and financial services remains relatively low, with TVL accounting for about 0.08% of last year's global GDP and 0.3% of the off-chain financial service system (approximately $26 trillion according to Business Research Company).

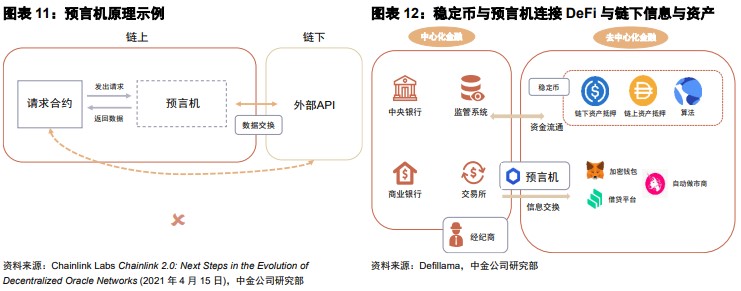

In terms of operational mechanisms, DeFi is not completely independent of the real world. It is linked to the off-chain financial system through stablecoins and oracles, allowing on-chain assets to effectively communicate with off-chain and respond to various variables in the real world.

► Stablecoins: The funding channel and value scale connecting the real economy and the crypto economy. Stablecoins serve as a medium of exchange between fiat currencies and cryptocurrencies, avoiding the restrictions of direct exchanges between cryptocurrencies and fiat currencies, facilitating the flow of funds on-chain and off-chain, while also relying on relatively stable values to become a "safe haven" for assets in the crypto economy. Depending on the object of anchoring and operational mechanisms, stablecoins can be divided into three main types:

Stablecoins collateralized by off-chain assets: These stablecoins typically use fiat currencies, precious metals, and other off-chain assets as collateral. A representative example is USDT issued by Tether. USDT is currently the largest stablecoin by market share, accounting for 43.64% of the total market value of all stablecoins as of the end of June 2022. For every unit of USDT issued, the company deposits $1 in its bank account, and users can exchange USDT for USD at a 1:1 ratio at any time. Issuers usually hire independent auditing firms to regularly verify the supporting assets in the custody accounts. Other large market-cap off-chain supported stablecoins include USDC, BUSD, etc.

Stablecoins collateralized by on-chain assets: These stablecoins use cryptocurrencies like ETH as collateral, with the collateral held by smart contracts. Users can deposit cryptocurrency collateral and receive stablecoins or redeem collateral by depositing stablecoins. Because the value of crypto assets often fluctuates more than fiat currencies, users typically need to over-collateralize at a ratio greater than 1:1. Examples of this type of stablecoin include DAI.

Algorithmic stablecoins without collateral: These stablecoins adjust the total market currency supply based on algorithms, increasing market supply when the stablecoin price is above the pegged price and recapturing supply when the stablecoin price is below the pegged price, or balancing the stablecoin price based on arbitrage trading, but they carry relatively high implicit risks.

► Oracles: The information channel connecting the real economy and the crypto economy. The blockchain itself is a closed-loop system, and smart contracts cannot actively obtain external data. Oracles can write external information into the blockchain, allowing smart contracts to respond to information from the real world, thus completing data communication between the blockchain and the real world.

Compared to the current centralized financial system, DeFi theoretically has advantages in cost, efficiency, transparency, security, openness, inclusiveness, and privacy protection. However, the current DeFi ecosystem is still in its early stages of development, and the financial system is not yet完善 and carries significant risks.

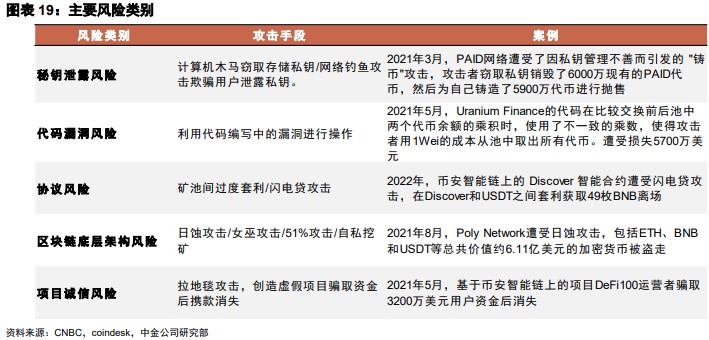

First, the DeFi ecosystem has relatively few restrictions on leveraged trading, and excessive leverage can trigger chain reactions of liquidations during sharp price fluctuations in cryptocurrencies, potentially leading to systemic crises in DeFi. For example, in May 2021, the sharp decline in ETH and the 2022 Luna crash saw the total locked value of DeFi shrink by -37.5% and -46% in a single day, respectively.

Second, malicious vulnerabilities and hacker attacks have repeatedly challenged the security and trustworthiness of the DeFi ecosystem. For instance, in March 2022, the underlying cross-chain bridge Ronin of the popular game Axie Infinity was attacked, resulting in losses of $625 million, while according to an Elliptic report, the DeFi ecosystem lost $1.55 billion due to theft throughout 2021.

Non-fungible tokens (NFTs): The underlying infrastructure for asset rights confirmation and value empowerment

NFTs refer to digital tokens that record corresponding asset rights information on the blockchain using smart contracts. NFTs have characteristics such as immutability and traceability, but unlike fungible tokens like Bitcoin and Ethereum, each NFT is unique and cannot be exchanged or divided. Based on this, NFTs can carry functions such as asset rights confirmation, scarcity construction, identity identification, and transaction circulation.

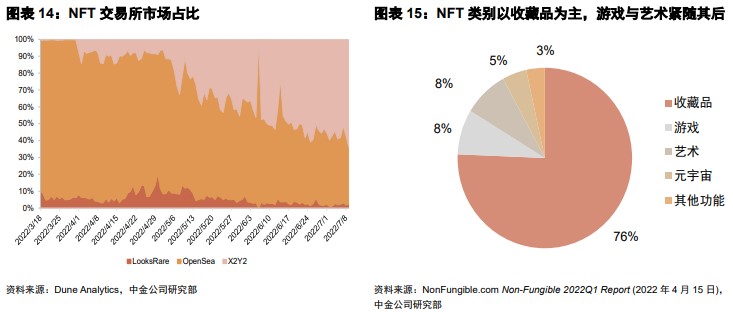

NFTs have developed rapidly in recent years. According to BlockBeats data, as of the end of June 2022, the total market value of NFTs was approximately $23 billion. Among them, based on different application scenarios and functions, NFTs mainly include collectibles, games, art, utility, and virtual worlds. According to Nonfungible statistics, in Q1 2022, NFT transactions were primarily concentrated in the collectibles sector, accounting for over 76%, followed by the art and gaming sectors, each accounting for 8%.

Currently, the NFT market is mixed, with a significant head effect. NFT projects issued by well-known artists often generate high enthusiasm and gain market value recognition. For example, in early 2021, "Everydays: The First 5000 Days" was auctioned for $69.35 million. In contrast, low-quality NFT projects often have short lifespans and struggle to sustain operations, with prices typically declining after initial sales.

In terms of trading platform models, NFT trading platforms can be divided into gallery-style and open-style. Gallery-style platforms require works to be screened by the platform before being listed, with higher entry barriers, primarily connecting high-value artworks, represented by SuperRare. In contrast, on open-style platforms, any creator can publish content, resulting in a wider variety of works but with relatively more differentiated quality, represented by OpenSea.

Based on the characteristics of NFTs, they can provide participants with value in four dimensions:

► Asset rights confirmation: Based on the immutability of the blockchain and the non-fungibility of NFTs, NFTs can record asset ownership and historical transaction flow information. For creators, they can trace copyrights during the circulation of NFTs to prevent infringement and continue to receive royalties in subsequent transactions, which helps incentivize their creative enthusiasm.

► Scarcity construction: In the digital world, anyone can freely copy and share digital content, with no distinction between originals and copies. NFTs, by recording the ownership of original digital content on-chain, differentiate the true owner of a digital content from the holder of a copy, artificially constructing digital scarcity.

► Identity identification: Due to the uniqueness and limited nature of NFTs, holding a certain type of NFT can itself serve as a form of identity identification. For example, the NFT avatars of the Bored Ape Yacht Club (BAYC) are not just artworks but can also serve as "club membership cards," granting exclusive access and participation rights to certain Ethereum dApps (decentralized applications) and offline BAYC events. In the future, NFTs could mark individuals' unique information, such as resumes and health statuses.

► Transaction circulation: Compared to traditional auction and private negotiation channels, the secondary market for NFTs is more transparent, allowing participants to trade and transfer NFTs more conveniently and customize profit-sharing rules, thereby enhancing the liquidity of the assets anchored by NFTs. However, excessive secondary trading has also, to some extent, fostered an NFT price bubble. In the future, we believe that the secondary market for NFTs will require more platform rules for protection or regulatory intervention.

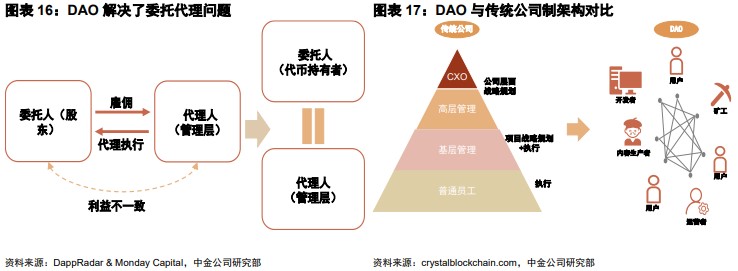

DAO: Decentralized organizational structure

DAOs (Decentralized Autonomous Organizations) are a form of decentralized organization that coordinates and governs through a set of shared rules executed on the blockchain. Compared to the traditional pyramid structure of corporate governance, DAOs adopt a more egalitarian structure, allowing everyone in the organization to vote on issues that affect their interests, thereby influencing decision-making.

DAO governance consists of on-chain governance and off-chain governance. On-chain governance involves codifying organizational rules and making voting decisions based on the number of governance tokens held by participants; off-chain governance occurs outside the blockchain, where the organization discusses and votes on non-binding common intentions through social platforms.

In the early stages of development, the on-chain token holdings and corresponding voting rights of DAOs were concentrated among project parties, thus typically reaching more potential users through off-chain governance. As projects mature and the distribution of token holdings becomes more decentralized, DAOs gradually shift towards on-chain governance as the main body, truly achieving decentralized autonomy under code constraints.

Based on their decentralized structure, DAOs have the following advantages:

► Greater transparency: The organizational rules of DAOs, the rights and obligations of participants, and the reward and punishment mechanisms are all publicly transparent and cannot be altered without the majority vote. Furthermore, every transaction and decision in DAO projects is recorded on the blockchain, allowing for historical records to be traced.

► More consensus: Since DAOs operate under organizational rules determined by participant votes, they can significantly reduce friction within the organization, making it easier to build consensus and trust.

► More openness: DAOs are typically built on public chains, allowing anyone holding governance tokens above a certain threshold to participate in governance, without entry barriers based on various identities. Therefore, compared to traditional corporate structures, DAOs are more likely to achieve global expansion.

Intrinsic problems restrict the development of Metaverse Finance, while external regulatory pressures impact decentralized principles.

We believe that Metaverse Finance faces risks and challenges from four major aspects: technology application, operational governance, economic systems, and regulatory policies. Among them: 1) Defects in technology application will lead to structural problems within Metaverse Finance; 2) Over-centralization of power and inefficiency in operational governance may cause Metaverse Finance to lose competitiveness and attractiveness; 3) Excessive speculative trading and high leverage in market structure may trigger systemic risks, impacting the trust and consensus in Metaverse Finance; 4) Significant differences in regulatory policies across countries may lead to fragmentation in the Metaverse financial system.

Technology application aspect: Constraints from underlying mechanisms

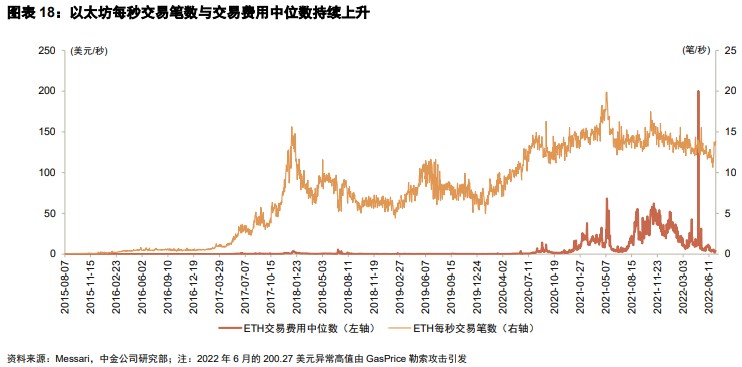

First, the underlying consensus algorithm has certain issues regarding transaction costs. Currently, major cryptocurrencies adopt proof-of-work (PoW) consensus algorithms, which consume a lot of electricity and incur high transaction costs. For instance, a single Bitcoin transaction consumes approximately 2,000 kilowatt-hours, and under relatively constant block generation speeds (~15 seconds/block), on-chain transactions may become congested during market volatility, requiring transaction initiators to pay higher costs to prioritize their transactions.

Second, the decentralized underlying consensus algorithm also limits transaction throughput and scalability. In the short term, developers have shifted the transaction computation process from the main chain to side chains through Layer 2 solutions, thereby reducing the load and limitations on the main chain, with theoretical throughput potentially increasing to 2,000-4,000 transactions per second. However, Layer 2 upgrades also bring more security risks. In the long term, the transition from proof-of-work (PoW) to proof-of-stake (PoS) consensus mechanisms and the introduction of sharding technology may enhance throughput limits and reduce energy consumption in transactions. However, PoS may exacerbate inequalities in incentive distribution and lead to excessive centralization of token distribution.

Finally, Metaverse Finance carries significant security risks. In 2021 alone, losses in the crypto economy due to hacker attacks exceeded $1 billion. To mitigate this risk, investors can hire professional auditing and due diligence firms to reduce potential vulnerabilities, but this approach not only increases investment costs but also contradicts the original intention of Metaverse Finance to reduce credit costs.

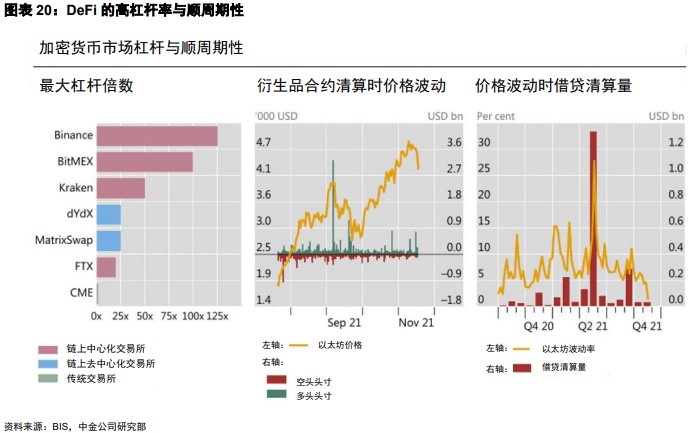

Market structure aspect: High-leverage speculative trading brings higher market risks

The economic system based on decentralized blockchain technology struggles to simultaneously meet the requirements of security and scalability, making it difficult for Metaverse Finance to widely serve the real economy, leading to its main activities being concentrated in speculative areas and bringing higher market risks.

Currently, the leverage ratio in the Metaverse financial system is far higher than that in the off-chain financial system, exacerbating its pro-cyclical characteristics. When the prices of cryptocurrency assets decline, investors will experience a passive deleveraging process, and the resulting asset sell-off will further drive down cryptocurrency prices, triggering a vicious cycle.

Furthermore, we believe that the current Metaverse financial system lacks the role of a lender of last resort, making it more vulnerable to liquidity crises compared to centralized financial systems. The characteristics of circular collateral and the inter-combinability of DeFi assets lead to a high correlation in the prices of various underlying assets in DeFi, further intensifying the transmission of market risks. For example, after the LUNA-UST collapse, lending protocols like Anchor, synthetic asset platforms like Mirror, and Ozone, which was responsible for compensation, all faced severe impacts.

Operational governance aspect: Power concentration and chaotic inefficiency caused by irregular governance

In terms of operational governance, due to being in the early stages of industry competition, some projects in the Metaverse financial sector currently face issues of excessive concentration of power and chaotic inefficiency due to their underlying distribution mechanisms. This leads to problems with the distribution of governance rights and governance efficiency, causing users to be more inclined to view governance tokens as profit tools rather than voting tools, and to focus more on financial returns than on participating in governance, making it easier to sacrifice the long-term development of projects for short-term returns.

In terms of governance rights distribution, although the goal of Metaverse Finance is to establish a decentralized financial system, in many projects, founding teams and early investors hold a high share of governance tokens, giving project parties and investors control over overall decision-making, allowing them to unilaterally modify project protocols based on their own interests, violating the principles of decentralization. For example, when Uniswap faced scrutiny from the SEC, its management team directly removed trading support for 129 tokens, including Mirror products, without going through a vote.

In terms of governance efficiency, some voters face information asymmetry regarding the strategic development plans of projects, hindering project development. Additionally, some participants hold tokens solely for speculative trading, and their choices may not necessarily benefit the long-term development of the project. Moreover, the process of voting to modify smart contracts is relatively lengthy, making it difficult for early-stage projects to flexibly change their development strategies.

Regulatory policy aspect: Impact on decentralized models

Decentralized Metaverse Finance, to some extent, breaks through the concept of territorial regulation, crossing national and regional judicial jurisdictions. On decentralized blockchains, protocols, accounts, and assets lose their territorial concepts, making it difficult to correspond with existing regulatory systems. Therefore, current regulatory focus is concentrated on the exchange of fiat currencies and cryptocurrencies and the exchanges providing such functions.

In June 2022, the cryptocurrency exchange Binance faced further investigation by the U.S. Securities and Exchange Commission. As early as September 2019, Binance was limited by regulatory restrictions to launch a functionally restricted Binance.US in the U.S., requiring KYC verification. In the context of ongoing regulatory tightening, some exchanges choose to actively communicate and cooperate with regulators, such as Coinbase collaborating with the U.S. Internal Revenue Service to provide user transaction records and striving to obtain cryptocurrency licenses at the state level.

However, as cryptocurrency exchanges move towards compliance, they effectively become part of the centralized financial system, fundamentally impacting the decentralized ideals of Metaverse Finance. Exchanges that refuse to cooperate with regulators face significant regulatory compliance pressures, making it difficult to stabilize and expand their business scale. On the other hand, without regulatory oversight, exchanges may face issues such as insider trading, and investors on the platforms may struggle to protect their rights through legal and compliance channels.

Moreover, in recent years, major economies have had significant differences in their regulatory philosophies regarding cryptocurrency trading and other Metaverse financial activities, positioned differently on the spectrum of encouraging technological innovation, preventing systemic risks, and protecting investor rights. Ultimately, these regional regulatory policy differences may constrain the development of Metaverse Finance.

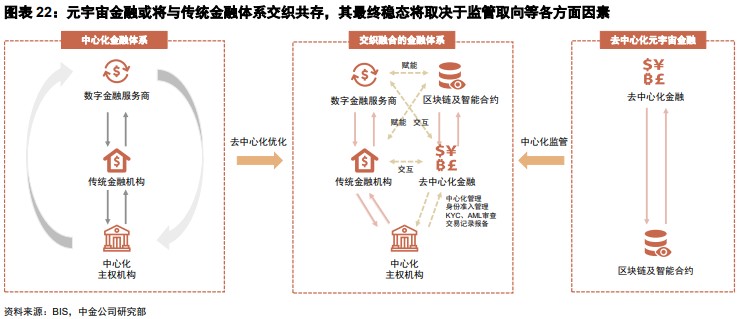

Integrating with the centralized financial system, Metaverse Finance may provide beneficial references.

Under the current national sovereignty and social structure, a fully decentralized Metaverse financial system is unlikely to exist widely. We believe that the future of Metaverse Finance may be built on central banks and other regulatory institutions, with centralized and decentralized financial institutions as operational entities, creating a more transparent, efficient, and inclusive financial system.

In the process of integrating Metaverse Finance with traditional financial systems, we expect that Metaverse Finance may gradually be incorporated into regulatory frameworks, establish compliance entry points, enhance the stability of the financial system, and empower traditional financial systems, continuously optimizing the efficiency and experience of traditional financial services, reducing intermediary issues, lowering operational costs, and lowering user entry barriers.

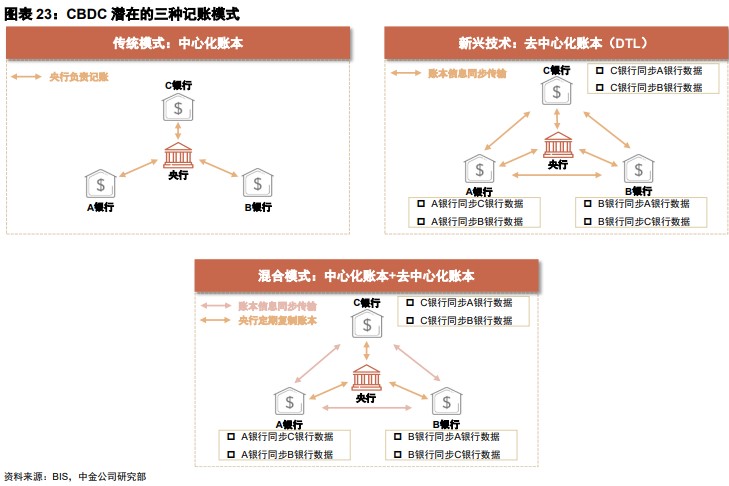

Taking central bank digital currencies (CBDCs) as an example, they are, on one hand, fiat currencies backed by national sovereignty, with operational frameworks and monetary policies set by central banks and relevant regulatory institutions. On the other hand, they incorporate technologies such as distributed ledgers and smart contracts into their operational mechanisms and functions, while also absorbing decentralized ideas to some extent, focusing on protecting user privacy and enhancing service accessibility.

Currently, retail (individual-facing) CBDC projects dominate globally. Among them, China's digital yuan (e-CNY) ranks among the world's top in terms of transaction scale and user numbers. Additionally, countries like Japan, South Korea, and Russia have begun CBDC pilot projects, while developed countries represented by Europe and the U.S. are still in the early stages of research and development.

We believe that CBDCs are expected to become an important infrastructure for the payment systems of Metaverse Finance and are likely to apply features such as smart contracts and payment-on-settlement in various scenarios, enhancing payment system efficiency, promoting the integration of digital and real economies, and empowering the real economy.

The concept of the "metaverse" provides imaginative space for the digital transformation of financial institutions.

From a realistic perspective, the original intention of the "Financial Metaverse" is the digital transformation of financial institutions.

In the previous chapter, we described the "Metaverse Finance" system while exploring the risks and challenges faced by "Metaverse Finance" in terms of technology application, operational governance, economic systems, and regulatory policies. Due to various limitations such as regulatory environments and technological maturity, different countries and regions around the world exhibit varying degrees of acceptance of "Metaverse Finance," represented by "cryptocurrencies," "DeFi," "NFTs," and "DAOs." Therefore, in this chapter, from a practical perspective, as the digital transformation of financial institutions in China continues to accelerate, we believe that the "metaverse" holds more realistic significance for traditional financial institutions, stemming from the continuous maturity of its underlying technologies and the imaginative space brought by the continuous extension of its scenarios, which is expected to further promote the digital transformation of financial institutions and provide richer possibilities and imaginative space for their digital transformation paths and ultimate forms.

The continuous improvement of concepts and underlying technologies related to the "metaverse" can provide richer possibilities and imaginative space for the digital transformation of financial institutions in China. On one hand, as the "metaverse" gradually advances, the application of its underlying technologies, such as modeling and rendering, interaction technology, the Internet of Things, network computing power, blockchain, and artificial intelligence, is expected to accelerate, and we believe that financial institutions will benefit from the rapid development of these technologies, better achieving digital transformation goals such as business innovation, process reengineering, and organizational change; on the other hand, the metaverse paints a picture of a virtual world with digital-native capabilities, even possessing a complete economic and social system. We believe that the immersive experience and the realism of virtual elements brought by the metaverse will provide richer imaginative space for financial institutions in aspects such as online collaboration, online business development, and customer experience upgrades.

Overseas "Metaverse Finance" and "Financial Metaverse" are both developing, while domestic focus is on digital transformation.

Observing overseas: Financial institutions' innovations in the "metaverse" present three levels.

Overseas financial institutions are actively exploring the metaverse, which can be divided into three levels based on the decision tree formed by two judgment factors: whether business channels have expanded to metaverse platforms and whether business innovations are related to decentralized finance. Due to differences in regulatory environments, financial systems, and the maturity of "metaverse" scenarios, we believe that the exploration of Level 3 by overseas financial institutions holds more reference value for the initial "metaverse" exploration of financial institutions in China.

► Level 1: Exploring and laying out decentralized financial businesses in the metaverse. For example, the head of JPMorgan's Onyx project stated in June 2022 that they plan to engage in institutional-level DeFi business by tokenizing U.S. Treasury bonds or money market fund shares to potentially serve as collateral in DeFi pools. JPMorgan has already participated in the Monetary Authority of Singapore's Project Guardian pilot and is conducting related exploratory work. The National Bank of Korea is also exploring a hybrid digital wallet (which can store multiple tokens, NFTs, and central bank currencies) that has completed testing.

► Level 2: Using metaverse platforms as new channels for existing financial businesses. In this development direction, financial institutions enhance their customers' service experiences based on existing "metaverse" scenarios. For example, HSBC opened a virtual sports field in the Sandbox to create a novel brand experience for new and existing customers; Fidelity Investments and Fidelity Metaverse ETF jointly launched "Fidelity Stack" in Decentraland to educate on investment basics; JPMorgan launched the Onyx lounge in Decentraland to showcase its blockchain business development history.

► Level 3: Utilizing metaverse-related technologies to promote digital transformation. Financial institutions leverage XR, digital twins, 3D modeling, artificial intelligence, and other metaverse-related technologies to further drive digital transformation, with the maturity of these technologies and the extension of scenarios synchronously developing alongside "metaverse" innovations. For instance, New Zealand's ASB Bank launched a virtual employee named Josie; BNP Paribas applied VR technology in retail banking, real estate, and insurance businesses in 2017 and further iterated its digital twin real estate project WIRED in 2022 to provide clients with historical recreations and future predictions of communities across Europe, assisting clients in decision-making; Fidelity Investments is continuously exploring how VR can promote service innovation; Citibank released a proof of concept for a holographic virtual financial trading workstation using Microsoft's HoloLens in 2016; Mastercard launched an AR app in 2020 to help users understand their rights; Bank of America uses VR technology for employee training; the National Bank of Korea opened an employee office area on the metaverse platform Gather; and Hanwha Life Insurance launched a metaverse virtual training platform called "Lifeplus Town."

Observing domestically: Development of "Metaverse Finance" is limited; "Financial Metaverse" has achieved preliminary exploration.

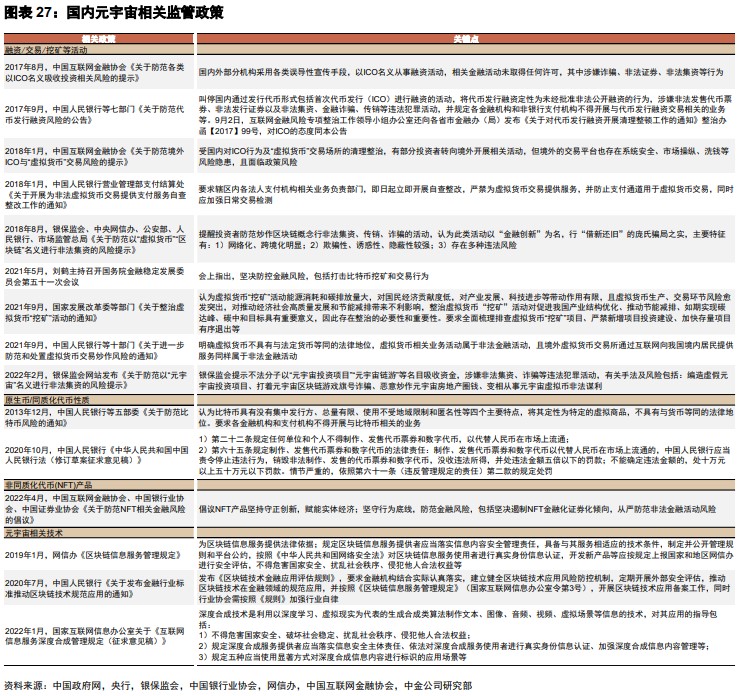

China's regulatory authorities maintain a cautious attitude towards the exploration and development of the metaverse by financial institutions to prevent financial uncertainties. The development of the metaverse has raised issues related to information protection and asset protection. For example, investors may suffer from hacker attacks leading to private key leaks and property losses, and the instability of cryptocurrency asset prices, along with the high leverage characteristics of DeFi, further amplify market risks. Therefore, activities involving "Metaverse Finance" (i.e., represented by cryptocurrencies, DeFi, NFTs, DAOs, etc.) face limited development space in China. Some policies have explicitly regulated financing/trading/mining activities, the nature of native coins/fungible tokens, NFT products, and the application of metaverse-related technologies, primarily aimed at mitigating risks and protecting investors' personal property and information security.

Under the cautious regulatory attitude, leveraging "metaverse" related concepts and technologies to enhance digital transformation is currently the main innovative direction for financial institutions in China to conduct preliminary explorations of the "metaverse." In addition to the already deeply applied "ABCDI" technologies, financial institutions have made certain breakthroughs in interactive and modeling technologies represented by virtual humans, digital twins, and XR through the concept of the "metaverse." Furthermore, we believe that the emergence of NFTs is also expected to help financial institutions further apply blockchain to empower supply chain finance.

► Virtual humans: Virtual humans integrate NLP, intelligent voice, computer vision, and professional knowledge graphs to build interaction capabilities and expertise, while shaping their appearance through modeling and motion capture technologies. They maintain a friendly service attitude and intelligent guidance in customer service across online and offline channels, while also assisting in business processing and helping enterprises establish trendy brand images. Virtual humans connect with data platforms, and the collected front-end business data can help financial institutions analyze high-frequency issues and business needs at various branches, further enhancing operational capabilities. Although as early as 2019, Nanjing Bank, China Everbright Bank, and Shanghai Pudong Development Bank launched virtual human digital employees, domestic applications of virtual humans have concentrated in the second half of 2021.

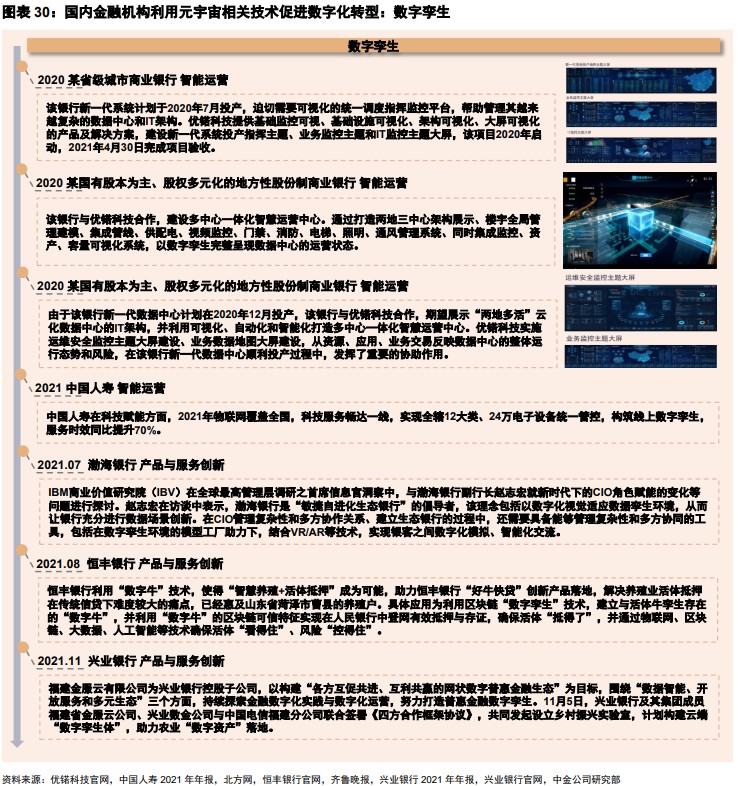

► Digital twins: Digital twin technology can help financial institutions enhance operational and innovative capabilities. In the field of intelligent operations, digital twins can provide services such as data center visualization, IT architecture visualization management, digital smart parks, digital operations, enterprise architecture asset management, financial technology information reporting systems, integrated financial operations, and financial security visualization. Between 2021 and 2022, plans utilizing digital twin technology to assist rural revitalization, bank-enterprise connections, and banking ecosystem construction have emerged, aiding in credit product innovation. As technology continues to develop and apply, we believe that the driving force of digital twins for business innovation is promising for the future.

► XR: XR refers to extended reality technologies, including VR/AR/MR/holography, which can help financial institutions build online channels with stronger experiences, immersion, and fun. Among them, AR technology has been applied earlier, focusing on credit card promotions, enriching online app experiences, data aggregation and display, and marketing during major holidays. The application of VR technology can be distinguished based on whether VR headsets are required or not. Without VR devices, VR displays on mobile devices can provide 3D spaces such as conference rooms and lounges, integrating various online service and marketing methods. Services utilizing headsets primarily appear in immersive experiences at smart bank outlets.

What value can the concepts and technologies related to the "metaverse" bring to the digital transformation of financial institutions?

The year 2021 marked the conclusion of the central bank's "Fintech Development Plan (2019-2021)." From the perspective of traditional financial institutions' "digital transformation" responses, their technological development paths primarily focus on 5G + "ABCD," while some leading institutions have gradually begun to explore innovative applications in niche technology fields. Looking ahead, we believe that the digital transformation of traditional financial institutions will mainly present three major trends: 1) Improving quality, increasing efficiency, and reducing losses; 2) Building a supportive foundation for digital transformation; 3) Technology for good. (For details, see CICC's non-bank group's report "Seeing the Microcosm: Digital Transformation of Financial Institutions - Original Intentions Remain, Progress with Stability")

We believe that against the backdrop of accelerating digital transformation of traditional financial institutions in China, the development of concepts and technologies related to the "metaverse" is expected to bring new directions for digital transformation in human resources, digital marketing, and operations, while also providing users with richer digital experiences.

In terms of human resources, it is expected to enhance employee work experience and training efficiency: 1) Enhancing the atmosphere of online work: The KB Financial City launched by the National Bank of Korea on the metaverse platform Gather provides a virtual office space displayed on a two-dimensional plane, allowing employees to feel the atmosphere of offline work and face-to-face communication despite being in different locations; 2) Improving employee work efficiency: Virtual digital employees utilize AI, one of the underlying technologies of the metaverse, to free up employee productivity. For example, digital employees at Waterdrop Company can use RPA and AI technologies to assist employees in handling routine tasks. 3) Enhancing the fun and knowledge retention of training: Bank of America established a VR training point in 2021, where employees can simulate customer interactions in various scenarios using VR headsets. The embedded real-time analysis technology allows supervisors to analyze training results, facilitating subsequent personalized guidance. According to Bank of America, among the 400 employees piloting the program, 90% found VR training to be an enjoyable experience, and 97% felt more confident in their work after VR training, believing it effectively enhanced knowledge retention.

In terms of marketing, it helps enhance the service capabilities and user experience of financial institutions.

► Enhancing service capabilities: On one hand, financial institutions can leverage metaverse-related technologies to improve their service methods and quality in data presentation and display, online user interaction, and providing 24/7 service through virtual employees. On the other hand, traditional institutions can also use interactive and modeling/rendering technologies related to the "metaverse" to create richer and more realistic images and web pages during service, as well as incorporate devices like VR/AR to effectively enhance service quality.

► Enhancing user experience: 1) Attracting young users with trendy UI design: Currently, young users show a preference for obtaining financial services through online channels. The financial metaverse is expected to use virtual humans/XR and other interactive, modeling, and rendering technologies to build trendy UI designs that capture the interest of young users. According to an iResearch survey, younger bank users in China visit offline branches less frequently, while NH Investment & Securities in South Korea stated that the MZ generation (Millennials + Generation Z) accounts for 52% of mobile trading services at brokerage firms, thus hoping to make investment activities simple and fun through diversified digital platforms; 2) Reducing users' overall costs: Financial institutions can use virtual humans for intelligent guidance online and offline, and utilize VR/AR technology to enrich the presentation of abstract data, potentially further reducing the time costs users incur for waiting and understanding delivered results; 3) Enhancing interaction experience and service accessibility: Currently, financial institutions have shown attention to the "persona" of virtual humans, aiming to create friendly service providers that can create a relaxed and pleasant atmosphere for users during online and offline interactions. At the same time, metaverse technologies can also enable users to obtain "offline-like" experiences through online channels, enhancing convenience. For example, an immersive online VR platform for insurance aims to replicate the offline insurance process, allowing users to access related services from the comfort of their homes.

In terms of operations, it helps enhance monitoring capabilities, analytical capabilities, and information protection capabilities. Among the technologies related to the "metaverse," digital twin technology can assist financial institutions in real-time monitoring of resource distribution and usage through charts and 3D models, overcoming the shortcomings of traditional ledgers and asset efficiency management systems, which are inefficient and lack real-time intuitive display capabilities. It allows for a better understanding of increasingly complex IT architectures and enterprise structures, enhancing the ability to understand and analyze operational processes, and improving standardized management and cross-departmental team collaboration. Additionally, through digital twins of infrastructure such as electricity, pipelines, power supply and distribution, lighting, elevators, and security systems, it can achieve real-time monitoring of the operation of data centers and other buildings, quickly identify anomalies, and enhance the ability to protect information security, employee safety, and property safety.

(This article is excerpted from the report "Finance × Metaverse: The Financial System Under the Integration of Reality and Virtuality" published on July 15, 2022.)

[1]https://www.coindesk.com/business/2022/06/11/jpmorgan-wants-to-bring-trillions-of-dollars-of-tokenized-assets-to-defi/

[2]https://www.ccvalue.cn/article/1389557.html

[3]https://www.ledgerinsights.com/hsbc-buys-nft-land-in-sandbox-metaverse-game/

[4]https://www.businesswire.com/news/home/20220421005259/en/FIDELITY-OPENS-%E2%80%9CTHE-FIDELITY-STACK%E2%80%9D-IN-DECENTRALAND-BECOMES-FIRST-BROKERAGE-FIRM-WITH-IMMERSIVE-EDUCATIONAL-METAVERSE-EXPERIENCE

[5]https://www.youtube.com/watch?v=54zs_mbUa1I

[6] "2022 Virtual Human Industry Research Report": SuTu Metaverse Research Institute, June 6, 2022

[7]https://www.uino.com/solution/finance/

[8] Lee, L-H., Braud, T., Zhou, P., Wang, L., Xu, D., Lin, Z., Kumar, A., Bermejo, C., & Hui, P. (2021). All One Needs to Know about Metaverse: A Complete Survey on Technological Singularity, Virtual Ecosystem, and Research Agenda. https://doi.org/10.13140/RG.2.2.11200.05124/8

[9] https://trainingindustry.com/articles/learning-technologies/how-bank-of-america-deployed-and-scaled-vr-to-advance-workplace-learning-a-case-study/

[10] https://report.iresearch.cn/report_pdf.aspx?id=3881

[11] https://www.koreatimes.co.kr/www/biz/2021/08/126_314385.html