How did DeFi protocols perform under this round of stress testing?

Some mortgage lending liquidations are incapacitated, and some credit loans face repayment difficulties.

Some mortgage lending liquidations are incapacitated, and some credit loans face repayment difficulties.Author: Qin Xiaofeng, Odaily Planet Daily

Recently, the prices of Bitcoin and Ethereum have continued to decline, both hitting new lows for the past year. The entire crypto market has been affected, and DeFi is no exception. Data shows that the total amount of locked assets on-chain has halved from $163.5 billion in early May to the current $81.8 billion.

Today, Odaily Planet Daily will analyze the performance of major projects in the decentralized lending and decentralized trading sectors under extreme market conditions. Overall, leading projects like MakerDAO, Aave, and Compound have remained calm and orderly, with governance and liquidation processes running smoothly; emerging projects like Solend and Maple have faced frequent issues, exposing their shortcomings and revealing persistent problems in their respective fields. We hope that these experiences and lessons can provide references for DeFi practitioners and promote the advancement of DeFi.

DeFi Lending: Liquidation Challenges

As the market declines, DeFi lending is particularly affected and faces liquidation. Some DeFi protocols have recently exposed several significant issues during liquidations that deserve attention:

First, oracle failures have led to improper liquidations. Liquidation processes rely on on-chain oracles for accurate pricing. During the LUNA crash on May 12, Chainlink paused LUNA price updates due to a failure, causing the lending protocol Venus to miss timely liquidation, resulting in losses exceeding $14 million.

Similarly, half a month later, the same oracle pricing vulnerability reappeared. On May 30, with the launch of the new Terra chain, the oracle for Anchor, the largest lending protocol on the Terra chain, mistakenly reported the price of LUNC (Luna Classic) as $5 (Note: the actual price of LUNC is $0.00001, while the new coin LUNA is $5); users on the platform exploited this pricing error to successfully arbitrage, and fortunately, the team reacted promptly, resulting in only an $800,000 loss.

Regardless, these bloody lessons have served as a wake-up call for DeFi protocols: choosing multiple oracles as pricing sources can more effectively avoid single points of failure.

Second, there are design flaws in the liquidation procedures that fail to respond in a timely manner. During the Terra collapse, the issuer of the algorithmic stablecoin MIM (Abracadabra) also incurred $12 million in bad debts, primarily because one of the collateral assets backing MIM, UST, became unpegged, and Abracadabra's liquidation process did not start promptly, leading to slow liquidation speed.

Liquidation procedures are an important aspect that DeFi lending protocols need to design in advance. For example, during liquidation, should collateral be auctioned off off-market or directly sold on the market? If the latter, should it be on a DEX or CEX, and which platform(s) should be chosen?

For instance, MakerDAO used to auction some liquidated assets at a discount, while currently, the vast majority of DeFi lending protocols choose to liquidate directly through DEXs. A retrospective summary reveals that Abracadabra did not have a preset plan in place initially, as it did not anticipate the possibility of UST significantly unpegging.

Third, poor liquidity and high volatility of collateral can exacerbate bad debts. It is important to note that liquidation speed is not only related to the design of the product but may also be directly linked to the "quality" of the collateral. For example, some altcoins exhibit high volatility, with price drops of 20% or more, and poor liquidity, making liquidation more difficult in a downward market; even Ethereum's yield-bearing asset (stETH) faced a run recently, leading to severe discounts, with the current exchange rate of stETH to ETH on Curve being 1:0.9368.

In fact, leading DeFi lending projects have established a strict set of collateral screening criteria. Taking Compound as an example, it accepts a total of 20 types of collateral, of which 7 are stablecoins. Among the top five collateral assets by locked amount (USDC, ETH, WBTC, DAI, USDT), three are stablecoins, which have been tested for both liquidity and stability, with controllable risks.

Even with certain preparations and plans, it does not mean that lending protocols can reduce or avoid liquidations. Liquidation is a routine operation in DeFi lending, and leading projects are no exception.

In the past week of decline, MakerDAO's treasury liquidated nearly 100,000 ETH; data from OKLink shows that on-chain liquidated assets reached $398 million in the past week, with Aave accounting for approximately $160 million, or 40%.

"Credit Loans" Facing Repayment Difficulties: Is a Crisis Imminent?

Currently, the most common form of DeFi lending is over-collateralization, meaning that a borrower wanting to obtain $100 of DAI needs to put up $150 (for example) of ETH or other cryptocurrencies as collateral. However, some products are attempting to offer under-collateralized loans to enhance capital efficiency, known as "credit loans" or "credit combined with collateral."

Unlike AAVE's "flash loans," platforms like TrueFi and Maple offer unsecured credit lending based on a review system, opening loan applications only to borrowers who pass the review, and primarily serving institutional users. For example, TrueFi launched its first single-borrower pool for Alameda Research in March this year, providing up to $750 million in operating capital; in April, it launched a single-borrower pool for Blockchain.com, providing up to $100 million in liquidity.

However, recently, there have been short-term repayment difficulties with credit loans. On June 21, Maple announced that its liquidity pool might face liquidity issues this week, and lending users may be unable to withdraw funds, having to wait for borrowing users to repay in the coming weeks before they can withdraw.

Rumors quickly spread, with market views suggesting that Maple might be affected by Celsius and Three Arrows Capital, leading to a break in its funding chain. In response, the official statement clarified that Celsius and Three Arrows Capital had never borrowed through Maple. However, the platform acknowledged that Babel Finance had a $10 million loan position in the USDC pool of Canadian hedge fund Orthogonal Trading on the platform; since Babel halted withdrawals, Orthogonal has been in contact with Babel's management, focusing on protecting lenders' interests.

In addition to Maple, another platform, TrueFi, does indeed have Three Arrows Capital among its clients. Data shows that on May 21 this year, Three Arrows borrowed $2 million from TrueFi, with repayment expected in August. However, considering the current predicament faced by Three Arrows, this loan may ultimately become a bad debt.

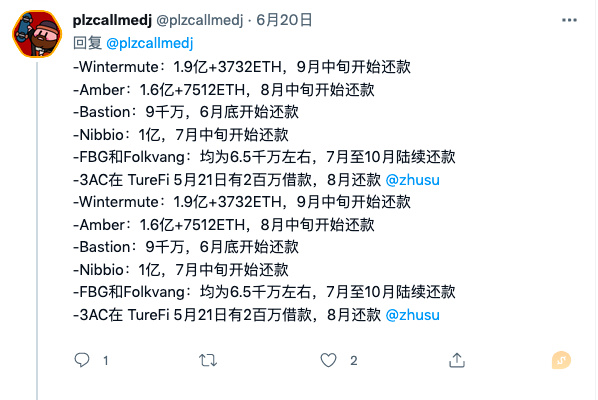

Additionally, according to statistics from Twitter user @plzcallmedj, institutions such as Alameda, Wintermute, Amber, Nibbio, FBG, and Folkvang have repayment deadlines concentrated in July and August. "I personally believe the risk is high; these companies that publicly claim to have hundreds of millions or billions are borrowing tens of millions or over a hundred million at nearly 10% annualized short-term loans, while collateralized loans only require 2%-3% interest, indicating that most of these institutions are quite cash-strapped. Moreover, TrueFi has already incurred bad debts from 3AC, which is bound to blow up; it's just a matter of time."

As the Three Arrows incident unfolds, more institutions have come forward to clarify their positions. The decentralized lending platform Clearpool removed the borrower pool for TPS Capital, a subsidiary of Three Arrows, claiming no financial losses; crypto lending platform Nexo tweeted that it rejected Three Arrows Capital's request for unsecured credit two years ago, with zero exposure to Three Arrows Capital.

This type of "credit loan" primarily serving institutions has, to some extent, avoided the generation of bad debts and filled the gaps in the DeFi lending market. However, as the market declines, DeFi markets are deleveraging, and institutional users are being liquidated one after another, raising doubts about their repayment capabilities, which may ultimately lead to liquidity exhaustion in the protocol and a chain reaction. Overall, under the conditions of an incomplete credit system, "credit loans" are relatively advanced and not yet ready for large-scale market promotion.

DEX: Price Decoupling and Removal of Impermanent Loss Protection

Recently, the liquidity issues of decentralized exchanges have also attracted significant attention.

First is Uniswap, currently the largest DEX, which has surpassed a cumulative trading volume of $1 trillion (as of May 24), yet still faces short-term liquidity shortages. On June 13, as MakerDAO liquidated ETH, a large amount of ETH flowed into Uniswap, causing the price to flash crash below $1,000, while the fair price was $1,350, with slippage reaching 25%.

Fortunately, the ETH price on Uniswap quickly recovered to the fair price. However, if we observe other ecosystem protocols, we find a hidden issue: the TVL of the largest DEX in the ecosystem is far lower than that of the largest lending protocol. Particularly in the Solana ecosystem, the TVL of Solend, its largest lending protocol, was more than twice that of Serum at one point. When the market declines, if Solend liquidates SOL collateral on DEXs like Serum, it may directly drain on-chain liquidity, significantly suppressing the price of SOL, which could trigger further liquidations of other accounts. This is also the core reason for Solend's recent proposal to take over.

Moreover, as the market declines, impermanent loss in DEXs has also expanded, and the fees earned by LPs may not even cover the losses, further reducing the incentive to provide liquidity.

Regarding impermanent loss, Bancor previously introduced a unique feature in V3 called “Impermanent Loss Protection”, allowing liquidity providers who meet certain conditions to receive 100% impermanent loss insurance from Bancor when withdrawing liquidity. However, recently, Bancor has suspended this mechanism. The fundamental reason is still the market downturn; if LPs withdraw at this time, Bancor would need to pay exorbitant insurance fees, which would also lead to reduced liquidity for Bancor, something it does not want to see.

"Withdrawals executed during this period will not qualify for impermanent loss protection, while users remaining in the protocol will continue to earn rewards and will be entitled to receive their fully protected value when impermanent loss protection is reactivated," Bancor stated.

Conclusion

Every extreme market condition serves as a significant test for DeFi protocols.

Overall, mature leading projects have delivered satisfactory results under this round of stress testing, while new projects have exposed some issues to varying degrees, which will be a necessary path toward maturity. In the past, MakerDAO also incurred $4 million in bad debts during the "312" crash but ultimately emerged from the shadow of failure to grow into today's "DeFi central bank."

Under the test of extreme market conditions, decentralized governance has also become a hot topic, and we have seen discussions about "procedural justice" and "resulting justice" (click to read “The 'DeFi Moral Paradox' Behind the Solend Farce”). In this regard, leading DeFi protocols have provided answers: since they uphold "Code is Law," they will act according to the rules, and liquidations will proceed as necessary; all governance will follow the process, allowing sufficient time for voting even in urgent situations.