Foresight Ventures: The decentralized NFT trading protocol will defeat OpenSea

What makes OpenSea afraid is not the next trading platform, but the aggregator Gem that addresses liquidity needs.

What makes OpenSea afraid is not the next trading platform, but the aggregator Gem that addresses liquidity needs.Author: Alex, Foresight Ventures

Abstract:

The decentralized NFT trading protocol for the NFT market is akin to AMM for DEX.

The core demands in NFT trading are liquidity and price, so the real moat of NFT exchanges should be built on liquidity and price advantages at the time of product sale.

The aggregator that changes the landscape merely addresses the issue of dispersed NFT listings as a front-end traffic entry point, without fundamentally solving the liquidity problem.

The most likely solution to the liquidity monopoly is not the next exchange or aggregator, but a protocol that supports shared listings, thereby breaking the boundaries between NFT tool platforms and NFT exchanges, allowing every front-end traffic source to become a trading platform and share its listings, forming a decentralized NFT trading ecosystem that addresses the dispersion and liquidity issues of NFT listings.

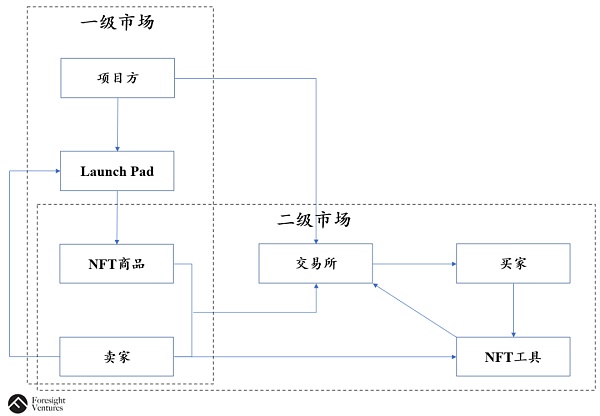

In the crypto world, one day equals a year in the human world, and in the NFT world, it may only be one hour after minting. The frenzy and FOMO surrounding NFTs are far crazier than in any other market, and as an infrastructure, NFT exchanges have already gone through several cycles, yet only a few remain, because most exchanges fail to meet the needs of all parties in secondary market NFT trading (as shown below), instead clinging to pseudo-needs in search of breakthroughs. Therefore, I will attempt to analyze the demands of NFT trading and the evolution of trading venues to explore better solutions for the future.

1. Market Environment and User Needs:

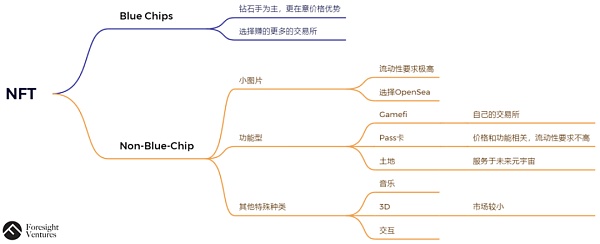

Currently, mainstream traded NFTs can be divided into blue-chip and non-blue-chip categories, with non-blue-chip roughly classified into three types: PFP, functional, and other special types. (Some blue-chip NFTs also belong to functional or special categories)

For blue-chip NFTs, due to their high prices and the fact that most blue-chip holders prefer to hold onto them, the demand for liquidity is not as high; instead, they care more about price. Functional NFTs like Pass cards and Gamefi, which have practical application scenarios, also do not have a high demand for liquidity, so they are more price-driven.

However, over 90% of NFTs in the market are small images without any empowerment, essentially a game of hot potato, which places a high demand on liquidity. At this point, users will choose to use the exchange with the best liquidity, OpenSea, rather than others. Other special types of NFTs currently have no application scenarios or demand, and the market is still primarily centered around PFPs, making further discussion meaningless.

Thus, we can conclude that the demands of buyers and sellers ultimately boil down to two points: Liquidity & Price (as shown below)

2. NFT Exchanges - Building Core Competitive Advantages to Meet Demand

We need to explore what kind of exchanges are excellent, discussing from the following five dimensions:

- Brand

Most exchanges are severely homogenized, with the core barrier being the traffic brought by first-mover advantage, creating brand effects and positive cycles. OpenSea utilizes its attraction of most NFT market liquidity to form a moat.

- Number of Trading Users

In a situation where the overall user base in the NFT market is not large (recently, the total daily active users of the Top 10 platforms did not exceed 100K in May 2022), whoever has more users can seize market share and influence.

- Trading Volume

Users can be divided into quality users and non-quality users, and the trading volume contributed by quality users may be dozens or even hundreds of times that of ordinary users, which is why whales currently dominate the market.

- Growth Rate of New Users and Transactions

The NFT market still exhibits a clear Matthew effect, so we can directly observe the future development of exchanges by focusing on the growth rate of new users and transaction volumes. The future NFT market is a huge incremental market rather than a stagnant market.

- Profit Distribution

By using tokens as a medium, all participants and platforms in the bilateral market become a community of interests, reasonably incentivizing holders with tokens, rather than slicing user and platform interests to earn more profit as traditional platforms do, which can win users' trust and support. Platforms will gradually evolve into forms more beneficial to users, and the speed of this evolution will vary depending on the industry.

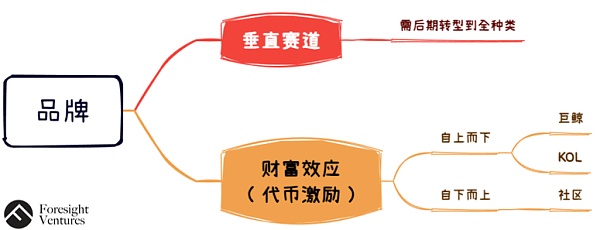

From the analysis of the above five points, we can conclude that for NFT exchanges to break through, they must pursue both vertical tracks and wealth effects.

- The first-mover advantage of brands is significant, which also makes OS enduring, but there are still emerging players who can vertically cut into the market.

SuperRare initially targeted artists' NFTs, creating a high-end brand image through a strict invitation system, while NBA Top Shot targeted a specific group using basketball, gaining significant exposure.

However, we need to note that if one chooses a vertical track, they may only establish their core advantages within that track, which is insufficient to compete with OS. Additionally, the current NFT world is still in its early stages, with too few users to support an overly narrow vertical track, which is a major reason why some NFT exchanges that were popular in 2021 have now disappeared.

- Besides cutting into vertical tracks, another more feasible approach is to leverage wealth effects.

One of the characteristics of Web3 is the ability to change profit distribution, which is also a point of contention for OS, unwilling to share results with Web3 users. LooksRare initiated a "vampire attack" and trading mining model, collaborating with whales and KOLs to embark on a top-down journey.

Although criticized for fake trading, it ultimately managed to seize market share; X2Y2 also engaged in a "vampire attack" and listing mining model, working with the community in a bottom-up effort, and despite some coding challenges, it ultimately achieved impressive results, even recently surpassing Looks to become the second-largest exchange globally.

From the successful cases of these two challengers, we can see that initial incentives for C-end users are essential; either by attracting upper-level KOLs and whales for endorsement or by rallying grassroots users through community promotion, both models ultimately formed a certain influence in their respective fields, rather than being limited to a specific group or small circle, leading to significant trading volumes and new users, gradually expanding the entire NFT market.

In this process, they are willing to share their cake with supporters and participants in the ecosystem, connecting everyone through Web3 tokens, which is why they could attract supporters. Human nature is profit-driven; without a reasonable incentive mechanism, no one is willing to try a new exchange, which is one of the key factors for their successful challenges.

3. NFT Tools - The Turning Point for Changing the Competitive Landscape

With the emergence of more NFT exchanges, NFT listings are scattered across various exchanges, and users' core demand is to buy the cheapest NFTs. At this point, aggregators emerged as unexpected winners in this battle of NFT exchanges, changing the market landscape.

What may defeat desktop computers is not another desktop computer, but more convenient and faster laptops and smartphones.

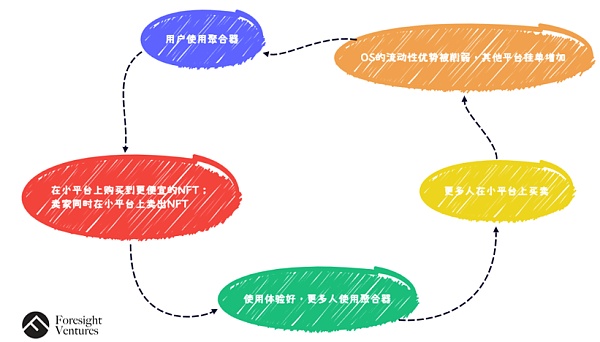

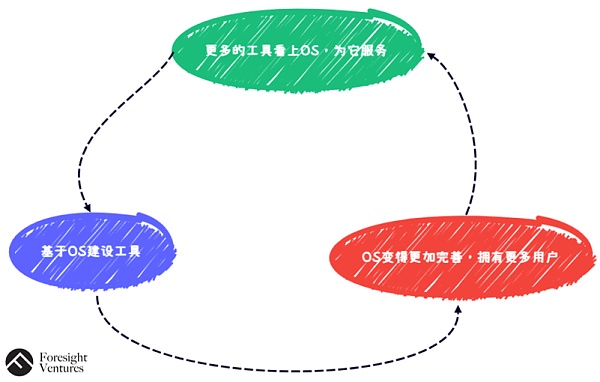

The launch of Genie and Gem met players' needs for multi-market shopping, allowing users to quickly find the cheapest NFTs and forming a positive cycle with smaller platforms (as shown below). At this point, exchanges became the backend providing orders, while aggregators served as the interactive frontend, increasing users for both.

When users purchase cheaper NFTs on aggregators, more users will flock to the aggregator; users of smaller platforms, due to increased NFT liquidity, will also be more willing to use smaller platforms for cost savings. As the number of users on aggregators and other platforms increases, the liquidity advantage brought by OS as the market leader is gradually broken, which will further accelerate the development of other platforms and aggregators. This is why X2Y2, Looks, Gem, and Genie have achieved results.

However, other established platforms have not been so fortunate, such as Rarible and Foundation. Due to the timing of their emergence, there was no aggregator platform at the time that could occupy the market, causing most trading platforms to be fleeting or even born to fail, unable to unite to counter OS; and during their transformation, they did not successfully expand into all categories, with a slow product iteration speed that failed to retain users, ultimately losing market share due to liquidity issues and falling into OS's "flywheel effect" (as shown below).

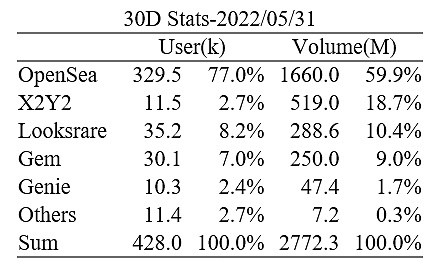

Thus, aggregator tools for NFT trading have become the new favorites of NFT users, breaking the liquidity monopoly and reshaping the competitive landscape. Under the positive cycle of aggregators, the top three exchanges and two aggregators have captured 99.7% of the market share (assuming the Top 10 trading volume represents the total market), with OS holding only 63.5% of the share, breaking the myth of invincibility. (Note: The impact of wash trading by Looks and X2Y2 has not been excluded.)

Resource: 2022/5/31 https://dappradar.com/rankings/protocol/ethereum/category/marketplaces

(Note: The above data lists Gem and Genie separately, not included in the exchange data.)

4. Imagining the Future - Possible Solutions for Breaking the NFT Trading Deadlock: A Truly Decentralized NFT Trading Protocol

After analyzing the real pain point of liquidity monopoly and its resulting brand effect in NFT trading, let us imagine what solutions could potentially disrupt the future competitive landscape. One thought I propose is: Rather than being an upstream traffic port, it is more feasible to create a bottom-layer protocol.

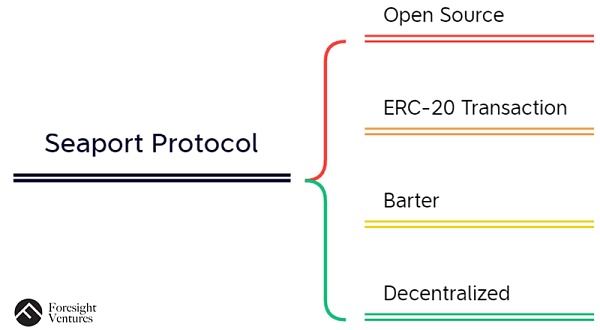

First, we can see that there is already a trend in this direction in the market. OpenSea officially launched the decentralized protocol Seaport Protocol in May 2022, aiming to make the NFT trading market more decentralized, with the main features shown below:

Essentially, Seaport only lowers the barriers for NFT exchanges, allowing most platforms to easily establish NFT exchanges without being coerced by existing exchanges like OpenSea, but it does not solve the liquidity problem in NFT trading, so the core demand still exists.

Its barter function will not make NFTs, which are already illiquid, more liquid; it merely provides users with an additional choice. In fact, there have long been platforms that have implemented this function: NFT Protocol (https://app.nft.org/ethereum) (as shown below), but its usage is extremely low, with almost no market share, proving that this demand is merely a beautiful pseudo-demand.

Using ERC-20 tokens instead of being limited to ETH payments has a considerable number of supporters in the market, which is closer to traditional users' shopping habits, benefiting new NFT users. I believe this is indeed an innovation, but from a technical perspective, the barrier is not high and lacks core competitiveness.

Existing NFT exchanges can quickly iterate and update, and the lack of iteration is more due to the fact that this demand has not yet been validated by the market. (NFT Protocol also has this function, but its performance remains poor.) This also explains why traditional crypto exchanges have struggled to enter the NFT space—the NFT community is ETH-centric, while the crypto community is mostly USDT and other stablecoin-centric, which is also one of the moats of NFT exchanges.

However, if we view NFTs as an incremental market with a changing perspective, assuming that many people from the crypto world enter the NFT space in the future, then exchanges that eliminate the step of converting ETH will certainly be more favored by the market; coupled with the current bearish trend of ETH, NFTs are also declining, increasing the demand for settlement in stablecoins, thus holding a positive attitude towards this function.

Inspired by Seaport, I personally believe that only a truly decentralized NFT trading protocol can fundamentally solve the liquidity problem. It allows every front-end traffic source in the market, whether an exchange, a tool platform, or even a project party, to become their own exchange and share each entity's listings, thus collectively forming the front end of this decentralized trading ecosystem, giving every order an equal opportunity to be seen and purchased.

Its main core features are as follows:

- Order Sharing Model

The order-sharing ecosystem allows each listing to appear on multiple platforms simultaneously. OpenSea monopolizes most orders due to its first-mover advantage, while other platforms have not formed their own ecosystems to unite against it, instead occupying territories individually, with users' listings not being shared, which greatly weakens the liquidity of NFT listings, which is not what users want to see. Therefore, if it is possible to enable NFT listings to be shared across multiple platforms from a technical level, such as from the protocol layer, I believe users would be more willing to try these smaller platforms, as small contributions can accumulate to form sufficient liquidity.

A real-world example is the emergence of Gem and Genie, which changed the competitive landscape. People are more willing to use such aggregators rather than a single platform, as listings from multiple platforms hold value, but the platforms do not interconnect, hence the demand for viewing NFT listings across different platforms simultaneously. Gem and Genie addressed this point, providing solutions that resolved pain points and attracted users. However, the solutions provided by Gem and Genie still rely on traditional NFT trading platforms like OpenSea, where API interfaces may be constrained by the platform, and the speed of order refresh may be subject to human limitations, making it difficult to achieve true real-time updates.

To further improve the aggregator model, it is more beneficial to create a bottom-layer protocol for exchanges rather than being an upstream exchange, enabling multiple platforms to share listings at the time of posting, so users do not need to switch back and forth, and any platform will have the same listings, thus enhancing NFT liquidity. Additionally, this resolves the risk of being coerced by large platforms and allows smaller platforms to unite against larger platforms; it also addresses the liquidity issues of long-tail assets listed on smaller platforms, reminiscent of the potential of Uniswap in its early days.

- Co-constructed Ecosystem Composability - Breaking Boundaries

Current NFT trading is still limited to NFT exchanges. Many excellent NFT tool platforms struggle without monetization paths, having user bases but when customers discover an NFT Alpha through tools, they often can only jump to a trading platform for buying and selling. Tool platforms can only serve as free traffic import interfaces, making others' clothes, but if NFT tool platforms can also trade NFTs directly and share profits, the efficiency of NFT trading will greatly improve. NFT tool platforms will no longer need to seek new monetization models, as they can monetize traffic through trading fees, forming a complete closed loop for the ecosystem, conducive to the healthy development of tool platforms.

Combining this with the first point of "order sharing model," since most users of tool platforms are also NFT users, the liquidity of these traffic orders will significantly increase, enriching the ecosystem. Rather than creating a divide between exchanges and tool platforms, which is unfair to tool platforms, they should receive a share of the income for directing traffic to exchanges, but currently, exchanges do not reward tool platforms for this traffic contribution, thus addressing the needs of tool platforms. The acquisition of Genie by Uniswap also indicates that in the future, when traffic platforms enter the NFT world, a model combining traffic and trading protocols may be a better way to integrate.

- Low Fees

There is still room for fee reduction. OpenSea's fee is 2.5%, while the paths taken by emerging players indicate that lower fees will be favored by the market, such as X2Y2, which currently has only a 0.5% fee, and this is one of the reasons many short-term speculative players firmly choose this platform. Therefore, future solutions are more likely to enter the market with lower fees, providing players with more profits, which will motivate them to try new solutions.

- Protecting Royalties

Currently, the rights to set royalties are delegated to the platform level, so if project parties want to collect full royalties, they need to set their royalties on each platform personally, which is obviously cumbersome. However, through the shared listing model, the royalties set by project parties will directly sync to multiple platforms, eliminating concerns about missing royalties, which is a huge benefit for project parties and will encourage them to shift from existing platforms to new ones for setting and incentivizing their users to list.

I believe that after achieving the above points, new players that disrupt the existing competitive landscape will emerge, and we will wait and see.

5. Conclusion:

For NFT exchanges, people are always envious of their vast market and the market share of individual exchanges, leading countless individuals to rise up, each borrowing the shell of pseudo-needs to paint one big pie after another. Ultimately, when the tide recedes, we will know who is swimming naked. If 2021 was the inaugural year of the NFT market boom, then 2022 is a year of fierce competition in the NFT market landscape; only by grasping core demands in the current environment can one swim against the current in a bear market and await the blooming of a bull market. What OpenSea fears is not the next trading platform, but the aggregator Gem that addresses liquidity needs; and what may disrupt Gem and trading platforms next is not another aggregator or trading platform, but a solution that fundamentally addresses the liquidity problem at the protocol level - the decentralized NFT trading protocol.

Risk warning

Risk warning Risk warning

Risk warning