DappRadar May Report: Terra Collapse Causes DeFi Market Value to Drop by 45%; NFT Trading Volume Decreases by 20% Month-on-Month

The price of altcoins has dropped by 90% from the peak in November last year; the activity of DApps has fallen to the lowest point this year.

The price of altcoins has dropped by 90% from the peak in November last year; the activity of DApps has fallen to the lowest point this year.Original Title: 《 May 2022 DappRadar Blockchain Industry Report》

Original Source: DappRadar

The blockchain industry has demonstrated its resilience amid the cryptocurrency winter exacerbated by the collapse of Terra. NFTs and gaming continue to show signs of growth and maturity, while DeFi seems to be starting a recovery.

The collapse of Terra, the former second-largest DeFi ecosystem, along with the related LUNA token and UST stablecoin, has intensified the bear market in the crypto space.

Bitcoin has dragged down the entire cryptocurrency market, closing below $30,000 for the first time since December 2020. Some altcoins have seen prices drop by 90% from their peak in November last year.

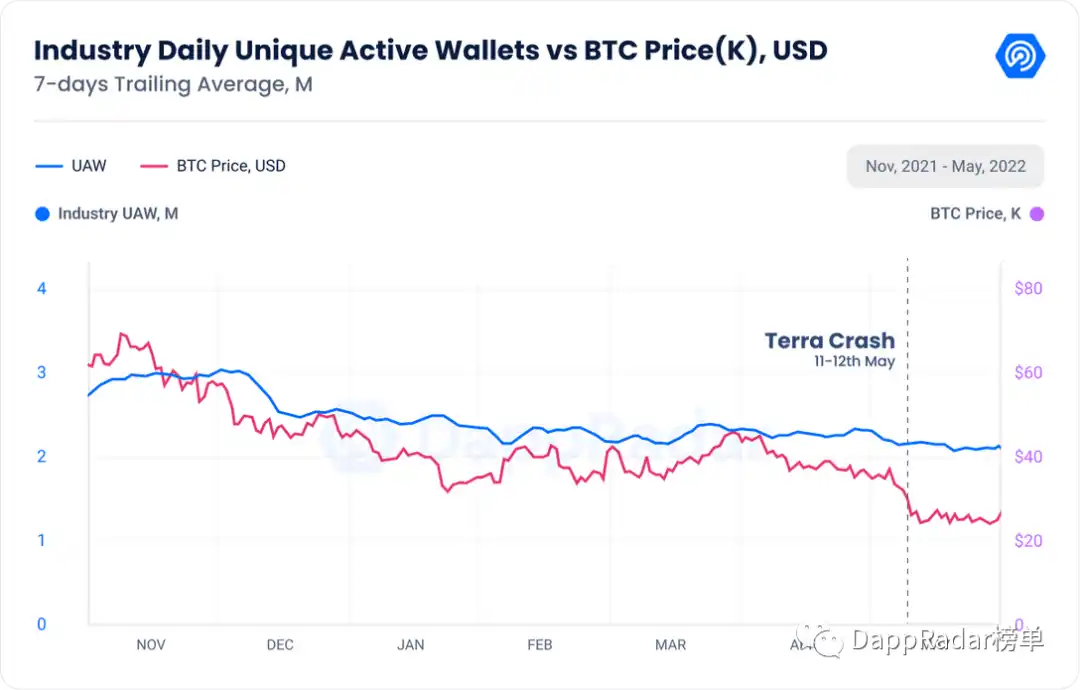

DApp activity has fallen to its lowest point this year, with 2.22 million unique active wallets (UAW) connecting to blockchain DApps daily in May. This figure represents a 5% decrease month-over-month but is still 32% higher than in May 2021.

However, despite ongoing infrastructure issues that typically disrupt networks, Solana's daily UAW count surpassed 200,000 for the first time in the network's history.

On a positive note, not everything is pessimistic. Despite the prolonged bear market, the DApp industry has become quite resilient. The NFT market continues to evolve with refreshing projects like Goblintown and Otherside, while also driving the development of virtual worlds.

User activity in blockchain gaming has declined, but the continued influx of venture capital maintains a bullish momentum. Most importantly, leading DeFi networks are competing for the market share left by Terra.

Key Points

In the collapse of the Terra blockchain, DeFi lost 45% of its value; Uniswap's historical trading volume exceeded $1 trillion while expanding its functionality to Polygon and Optimism.

The NFT market generated $3.7 billion in May, a 20% decrease from April's dollar trading volume; however, the trading volume measured in tokens showed only a 6.5% decline.

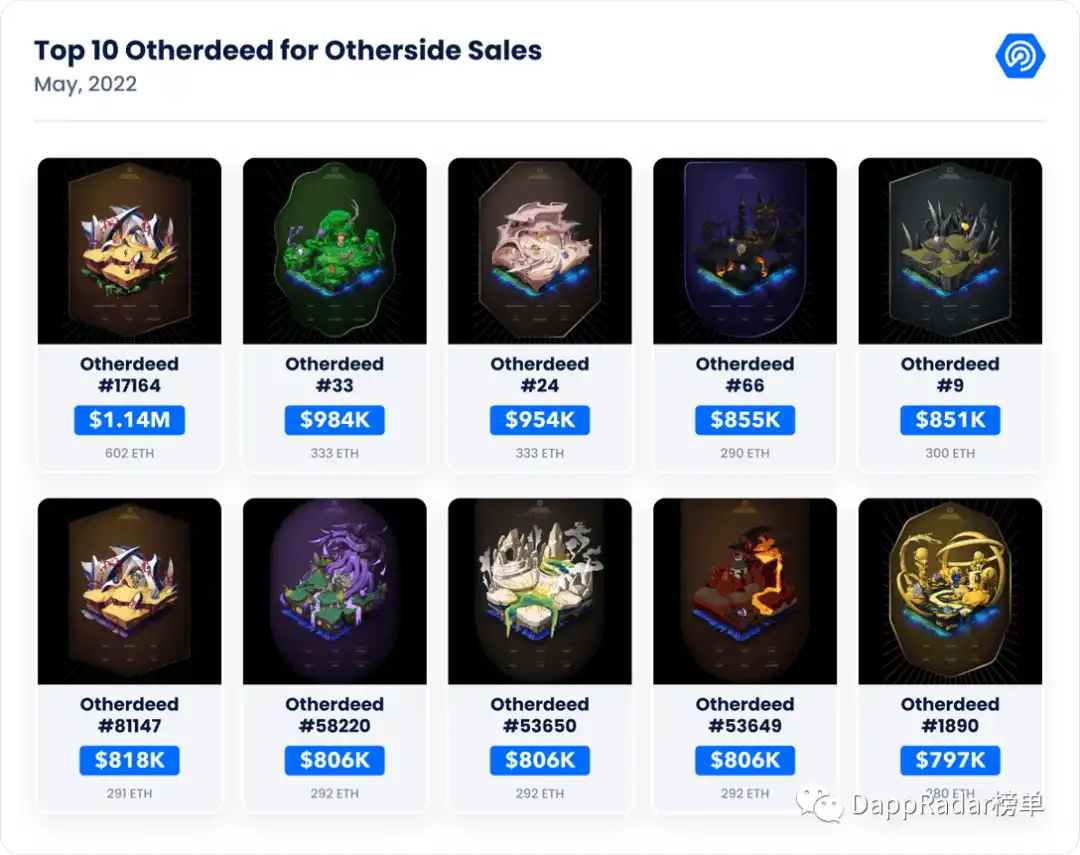

Otherside's trading volume reached $750 million, propelling the virtual world to over $850 million in May.

Investment in blockchain gaming continues to rise. The gaming category is resisting the cryptocurrency collapse, with active volume down only 5%, year-on-year growth of 197%.

The Collapse of Terra Dealt a Huge Blow to the Industry

The collapse of Terra on May 9 is a memorable moment in the timeline of crypto history. At that time, the third-largest stablecoin, UST, plummeted to $0.35. As a result, this drop affected the entire industry, causing most stablecoins to temporarily decouple from the dollar. The Luna Foundation Guard (LFG) used approximately $3.5 billion worth of 79,687 bitcoins to maintain the value of UST.

This move did not work for the ecosystem, and clearly, LUNA (Classic), ANC, and other related tokens did not have enough value to help UST re-peg.

Ultimately, on May 12, the Terra blockchain was halted. The collapse of Terra resulted in a loss of $60 billion, marking one of the most significant wealth losses in modern history. The event exerted downward pressure on the price of BTC and generated fear across the entire cryptocurrency asset class, exacerbating the bear market the industry was already experiencing.

Subsequently, Terra's co-founder Do Kwon announced a revival plan, which included a hard fork called Terra 2.0, that emerged on May 28. On that day, holders of LUNA Classic tokens received airdrops of the new LUNA, but its value had lost 99%. Nevertheless, Do Kwon's situation is far from over, as South Korean authorities are conducting an in-depth investigation into the severe impact on thousands of investors.

At the end of April, Terra was an emerging DeFi ecosystem with a TVL exceeding $25 billion, second only to Ethereum. It will be difficult for Terra to regain its position as Ethereum's runner-up in the DeFi space. On the other hand, peer blockchains will take advantage of this situation to capture the development talent and audience left behind by Terra.

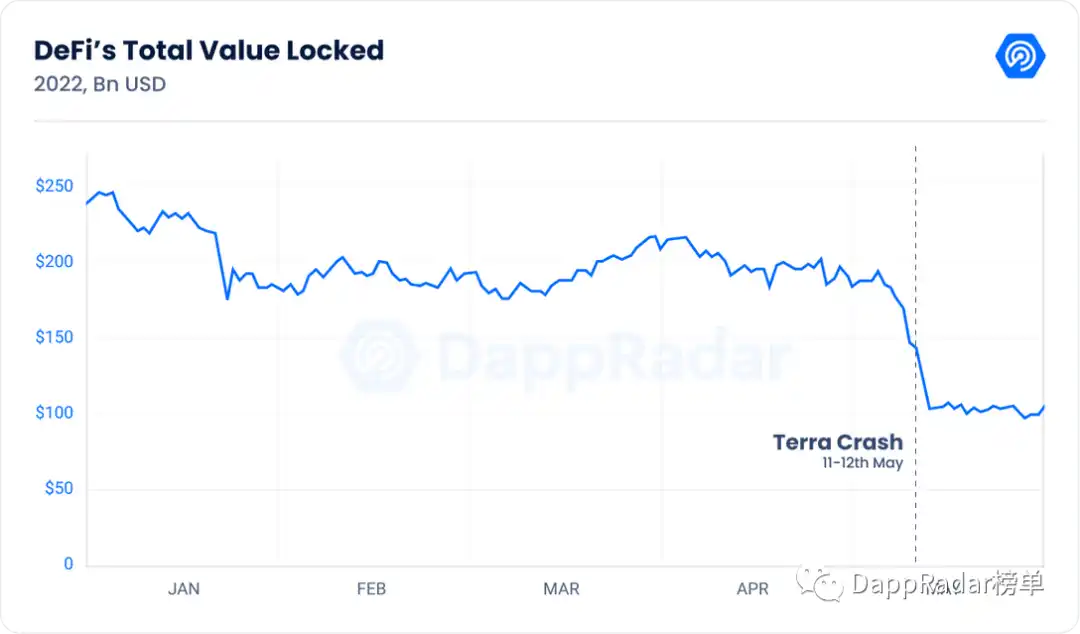

DeFi Lost 45% of Value Due to Terra's Collapse

Undoubtedly, DeFi is the vertical blockchain most affected by the bear market due to the direct impact of cryptocurrency prices. In the first four months following the emergence of new DeFi blockchains like Avalanche, Cronos, Near, and of course Terra, the DeFi space was still able to keep operating. Although DeFi tokens lost 25% to 40% of their value during the same period, the TVL in the industry only declined by 15%.

Then, the Terra event occurred. Since Terra's halt, BTC and ETH have lost 25% and 40% of their value, respectively. Similarly, since the end of April, the industry's TVL has dropped by 45%, currently estimated at $117 billion. However, in the long run, the locked value in the DeFi space has grown by 11% since May 2021.

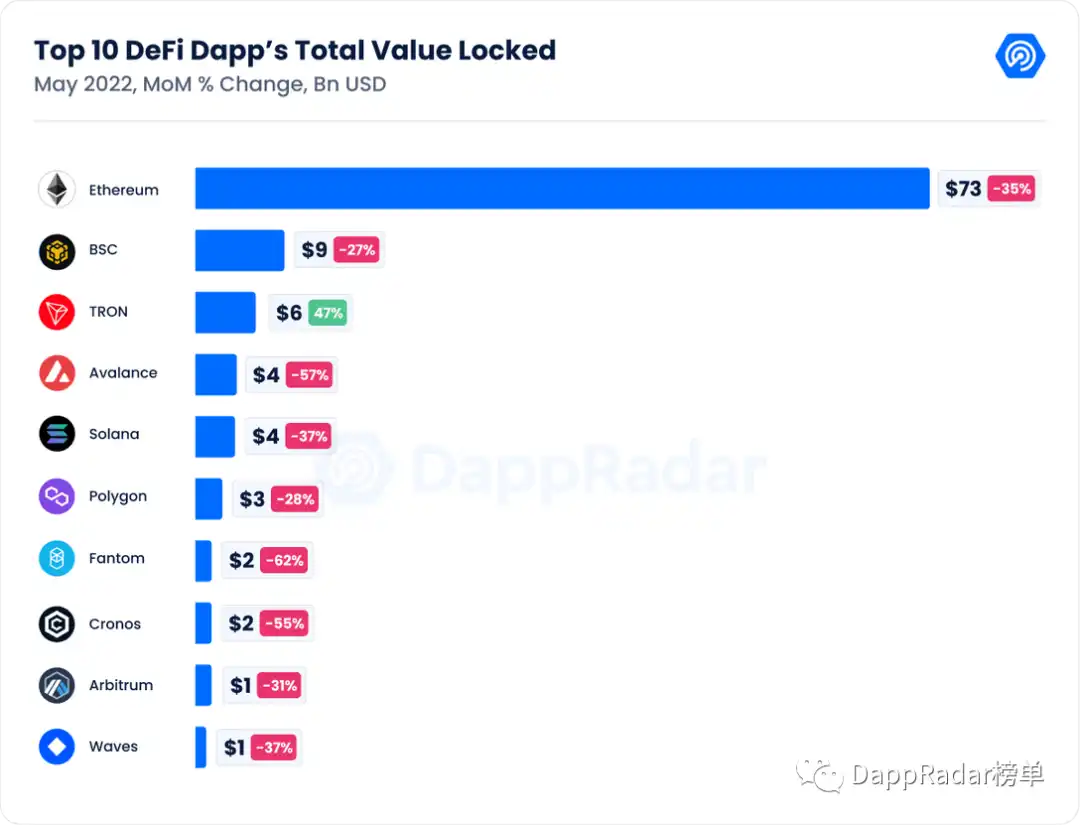

Tron became the only blockchain with a positive TVL, growing by 47% month-over-month. The native token prices of Ethereum, BNB, Polygon, and Solana fell by 27% to 38%, with similar declines. Avalanche, Cronos, Fantom, and Near lost 60% in key DeFi metrics.

In a more positive trend, Uniswap reached a significant milestone. The leading DeFi DEX's historical trading volume surpassed $1 trillion. Meanwhile, despite ongoing technical issues, the usage of Solana DeFi DApps (Orca, up 77%), Saber (33%), and Solend (11%) continues to rise.

The coming months will be crucial for the future of this relevant blockchain category. Which blockchain ecosystem can replace Terra as Ethereum's runner-up remains to be seen. Or can a second-layer scaling solution like Optimism challenge the established first-layer blockchain ecosystems through its token airdrops? This remains to be observed.

The NFT Market is Far from Extinct

During turbulent times, the NFT category remains a significant contributor to the DApp industry. The interest and publicity generated by this category are easily overlooked intangible factors. The exposure the blockchain industry gains from NFTs places today's crypto market in a position entirely different from the 2018 crypto winter. Back then, the entire industry's participation and enthusiasm were astonishingly low. While mainstream media continuously called for the bursting of the NFT bubble, the market conditions in the NFT space were quite different.

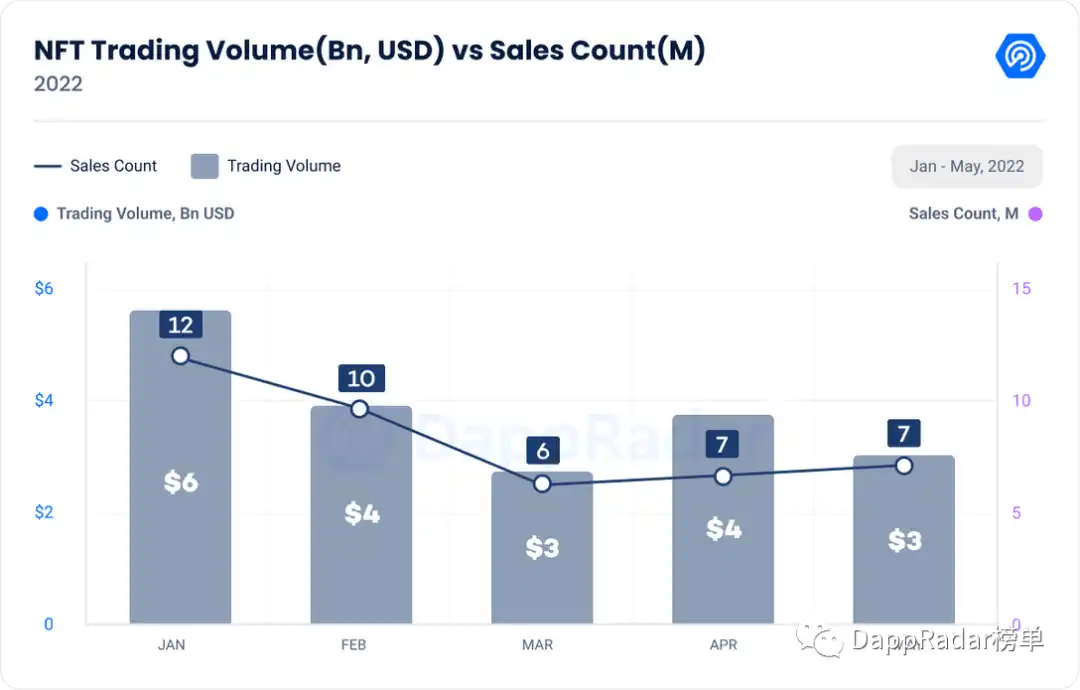

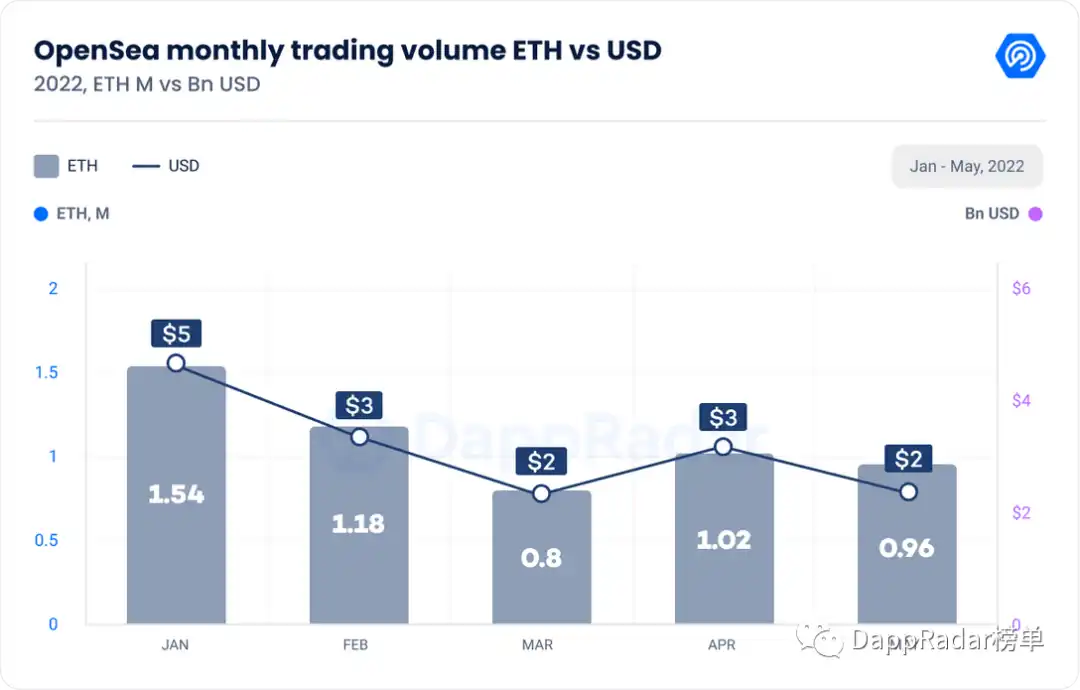

The NFT market generated $3.7 billion in May, a 20% decrease from April.

While the dollar-denominated trading volume initially suggests a shrinking market, analyzing the market trading volume of its native tokens indicates a different situation.

For example, the largest NFT marketplace, OpenSea, had a trading volume of 950,000 ETH in May, down only 6.5% from April. Since the price changes of ETH have a weighted impact on the metrics, the dollar trading volume presents a different perspective. The dollar-denominated trading volume of OpenSea decreased by 25% month-over-month. The comparison of the two perspectives shows an 18.5% difference between the dollar and ETH trading volumes.

Similarly, Solana NFTs were unaffected by the bear market trend, achieving the best trading month in the network's history. Solana NFTs generated $335 million across all markets, a 13% increase from April.

Despite the negative sentiment across the industry, the NFT market is clearly contracting, but this sector continues to evolve, generating billions in trading volume. Almost every month, the NFT space witnesses how new collections change the narrative of the entire field.

Blue Chips Struggle as Goblins and Otherdeeds Deplete Liquidity

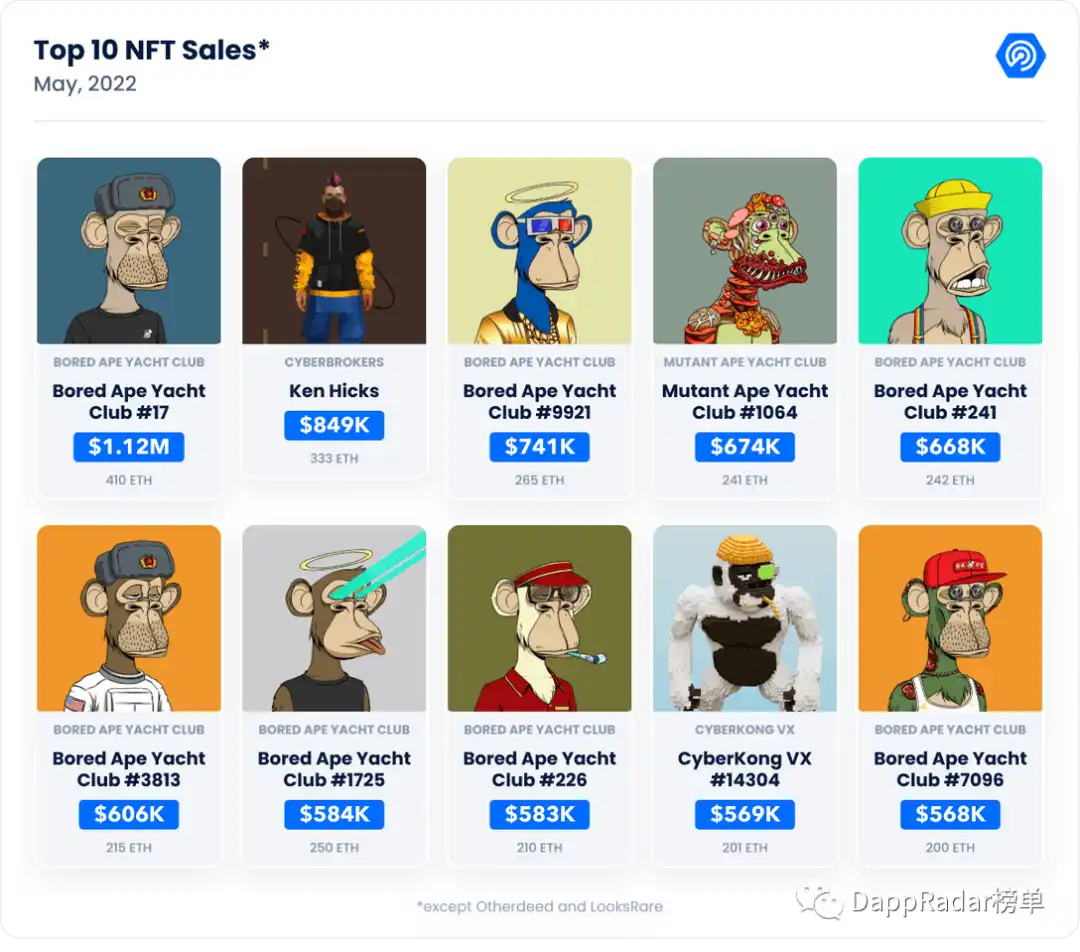

Last month, Moonbirds and Solana's Okay Bears successfully drove up NFT sales amidst unfavorable market trends, placing them at the forefront of their respective markets. In May, Otherdeeds propelled the virtual world to its best month in history. Additionally, since its launch on May 22, Goblintown has generated $31 million in revenue. Furthermore, after the 10K Club launched an exciting season around these Web3 domains, ENS completed 41% of its historical sales this month.

The high demand for these projects has driven their prices significantly higher. Goblintown transformed from a free release to a floor price of 6 ETH, with rumors suggesting that Yuga Labs is backing this mysterious project. Similarly, ENS's average sale price rose from 0.07 ETH in April to 0.11 ETH in May, with the floor prices of the 10K Club and 999 Club reaching 0.7 ETH and 8 ETH, respectively.

Meanwhile, several so-called "blue chip" collections saw significant declines in value last month. The hype surrounding some new collections undoubtedly hoarded liquidity from the market. Nevertheless, several specific events related to these blue chip ecosystems were also major factors in the price drops.

The events surrounding BAYC and MAYC were directly related to Otherside. Holders of these collectibles were airdropped Otherdeeds NFTs, creating a hype cycle before the snapshot at the end of April, resulting in record values. Once the issuance project was completed, the floor price began to drop. The low price of BAYC fell by 38% from April 30, from 150 ETH to 93 ETH. MAYC dropped 57% during the same period, trading at 18 ETH. Doodles experienced a similar situation, with its price dropping from 23 ETH to 12 ETH, a decline of 48% after launching Dooplicator.

However, each NFT collection has a different story. In May, the anime-inspired Azuki collection lost 75% of its value due to a scandal involving the project's founder's connections to three Rug Pulls (malicious acts where project teams entice early investors to inject funds and then abandon the project). The floor price fell from 31 ETH to 8 ETH, although with the help of Beanz, the project managed to recover to its current floor price of 12 ETH.

Overall, the value loss of top NFT projects has led to a decline in the market capitalization of the top 100 Ethereum collectibles. Since the end of April, the price of ETH has dropped by 37%, but the crash of blue chip projects has caused this metric to fall by 45% from $18 billion in April to $10 billion.

Despite the continuous decline in numbers, blue chips remain one of the highest trading volume NFT collections, indicating that their respective ecosystems are merely undergoing a consolidation phase. Additionally, despite the price drop in cryptocurrency values, the rate of decline in the value of these assets over the past few months has been slower than that of the underlying cryptocurrencies. Similar to the Art100 index during the 2008 recession, which fell by 26% while the S&P 500 dropped by 56%, NFT trading seems to be becoming an asset that could potentially decouple from financial markets to some extent.

Will OpenSea Be Replaced by Emerging Markets?

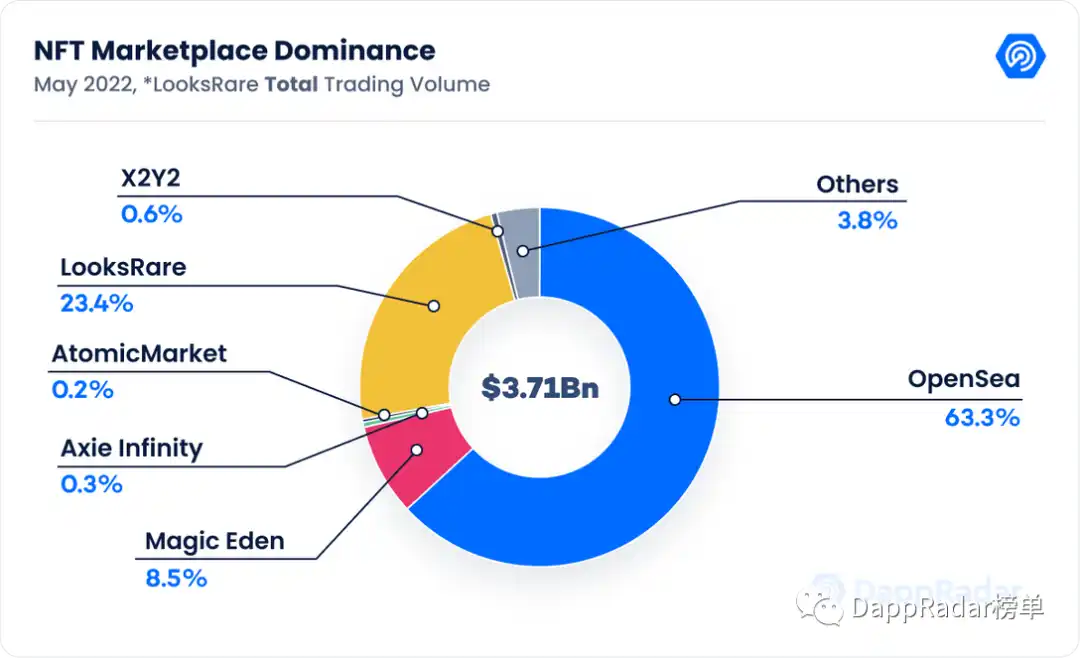

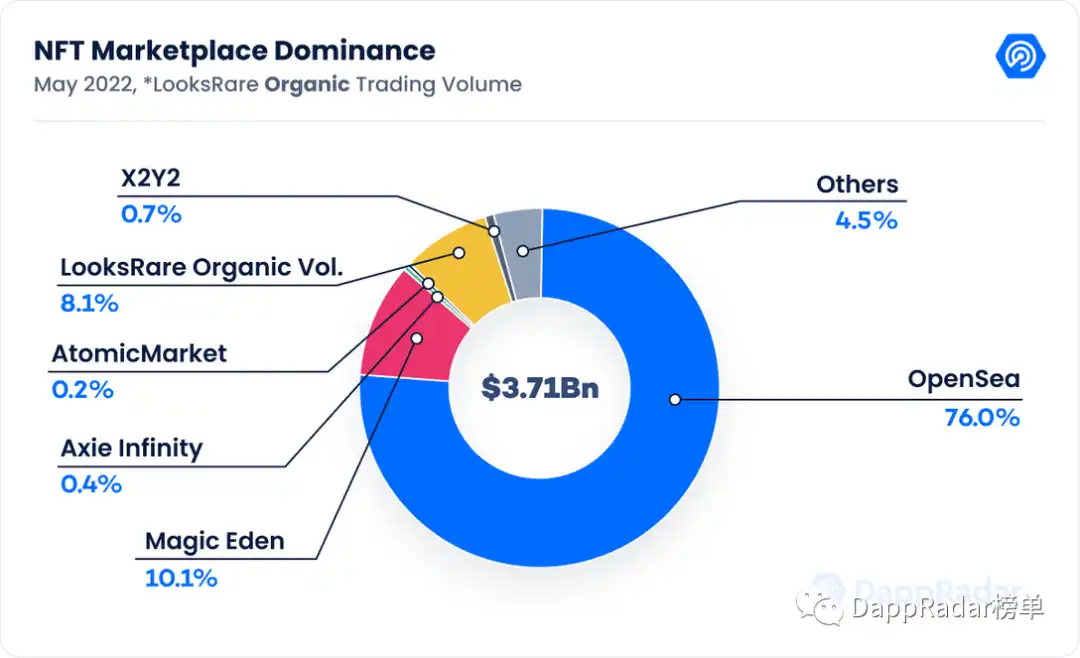

Another interesting trend in the NFT market is the increasing competition among marketplaces. OpenSea remains the dominant market, but the rising active data from other competitors shows signs of maturity and development in the NFT space.

OpenSea's dominance in sales has decreased from 90% in the first four months of this year to 84% in May. Although the number of UAW interacting with the market increased by 2% month-over-month (398,000 in May), the aforementioned situation still occurred. To some extent, marketplace aggregators like Gem and Genie provide an overall view of the NFT market, making LooksRare and X2Y2 more visible.

In May, LooksRare attracted 30,000 UAW, with the user count increasing by 22% compared to April. Using Hildoby's (a renowned Web3 data scientist) formula to filter and clean trading activity*, we see that trading volume in community-driven markets grew by 473%, reaching $250 million in May.

Similarly, the Ethereum market X2Y2 operates with a 0.5% trading fee, and its user count grew by 93% in May, attracting 11,500 UAW users. The market's transaction volume reached $22 million, a 286% increase from the previous month.

As the NFT space becomes more mature and competitive, OpenSea's dominance has undoubtedly declined, while the volumes of Solana's Magic Eden, Wax's Atomic Hub, and Ethereum's art-focused Foundation are on the rise. However, it is certain that OpenSea will remain dominant in the coming months. The marketplace has improved its interface with a new layout, providing a new user experience. Additionally, the company acquired Gem on April 27 and launched seport, an open-source platform to help creators publish NFTs.

Undoubtedly, the biggest loser is the Coinbase marketplace, which has only generated $2.5 million since its failed launch on April 20, 2022. In the coming months, we will continue to closely monitor the developments in the NFT market.

Can Blockchain Gaming Avoid the Market Collapse?

Blockchain gaming has been the most resilient category during the industry's bear market. The number of gaming transactions and the daily UAW connecting to gaming DApps have only decreased by 5% compared to April. Despite the decline, blockchain gaming has been the least affected compared to DeFi and even NFTs.

Top blockchain games continue to maintain their player bases, showing real user stickiness on the leaderboard. Furthermore, projects based on the metaverse and blockchain gaming are attracting increasing amounts of venture capital. In May, Dapper Labs announced a fund of $725 million to accelerate the growth of the Flow ecosystem, while A16Z committed to raising $4.5 billion for its fourth cryptocurrency fund, which will focus on developing blockchain projects.

Overall, blockchain gaming continues to attract more talent through DApps like STEPN or Genopets, embedding gamified elements into the move-to-earn trend, aligning with the trend. Lastly, on the other hand, in May, the revenue of the "play-to-earn" BAYC metaverse project reached $760 million, driving virtual world NFTs to generate $850 million in May.

For more insights on blockchain gaming, as well as trends in the virtual world, move-to-earn, and leading gaming DApps, be sure to read our upcoming BGA gaming report.

Conclusion

The macroeconomic situation and the Terra event have exacerbated the impact of the bear market, leading to a decline in the prices of crypto products and a slight decrease in enthusiasm for the industry. Nevertheless, user adoption rates and the number of Web3 developers are on the rise, which is a positive sign. Similarly, it is encouraging that the DApp industry has evolved into a multi-chain ecosystem capable of withstanding significant adverse events like Terra.

The NFT market has resisted this negative trend, and its data performance seems to be consolidating after the peak in January. New collections like Moonbirds, Goblintown, and Otherside help keep the NFT community engaged, while specific NFT collections continue to build interesting Web3 ecosystems.

Likewise, the NFT market shows clear signs of development. It is not uncommon for Solana NFT collections to rank highly in the NFT rankings. LooksRare's sales have grown from 2% in January to 35% in May. The popularity of NFT aggregators has reached its peak, while the leading market, OpenSea, continues to evolve.