Messari Report: Comprehensive Analysis of Lido Liquid Staking

A detailed explanation of Lido's current development status, operational methods, and competitive situation.

A detailed explanation of Lido's current development status, operational methods, and competitive situation.Original source: Messari

Original compilation: memeswap#8864|SnapFingers DAO Builder

Key Points

Lido allows users to delegate any amount of assets to professional node operators, thus eliminating the challenges and risks associated with maintaining staking infrastructure.

Stakers receive liquid, tokenized staking derivatives (st assets, such as stETH) to represent their claim on the underlying staking pool and its rewards.

st assets effectively release liquidity and eliminate the opportunity cost of staking, as st assets can be used on some DeFi protocols to earn additional yields.

Node operators join Lido through DAO voting and are responsible for the actual staking process.

1. Current Development of Lido

PoS networks still have a high barrier to entry and opportunity cost for potential users (for example, Ethereum requires a minimum of 32 ETH), including significant capital investment, technical complexity of the validation process, and long lock-up periods (locked until after the merge). This has given rise to the "staking as a service" sector, where these platforms provide simple, flexible, and capital-efficient staking services for holders. The leader in this industry is Lido.

Lido is a non-custodial liquid staking protocol applicable to Ethereum, Solana, Kusama, Polygon, and Polkadot. Lido not only democratizes the entry conditions for PoS but also aims to achieve a more secure decentralized PoS network as its roadmap is gradually implemented. Lido currently ranks fourth in total value locked (TVL) across all protocols and accounts for nearly one-third of all staked ETH.

Recently, Lido DAO voted against deploying on Terra 2.0. Lido will continue to incorporate more node operators through governance to diversify its validator pool.

2. How Lido Works

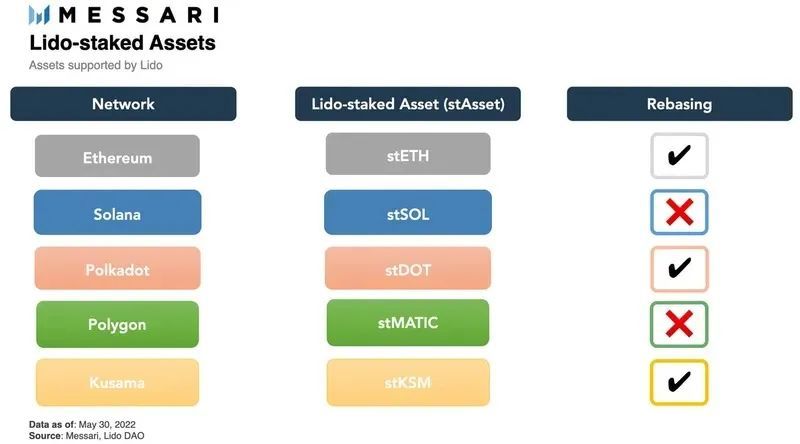

Currently, Lido DAO manages five Lido liquid staking protocols. Although the five supported PoS networks (including Ethereum, Solana, Kusama, Polygon, and Polkadot) are designed differently, the general mechanism of their liquid staking protocols is similar.

Source: @Leo_Glisic, Messari

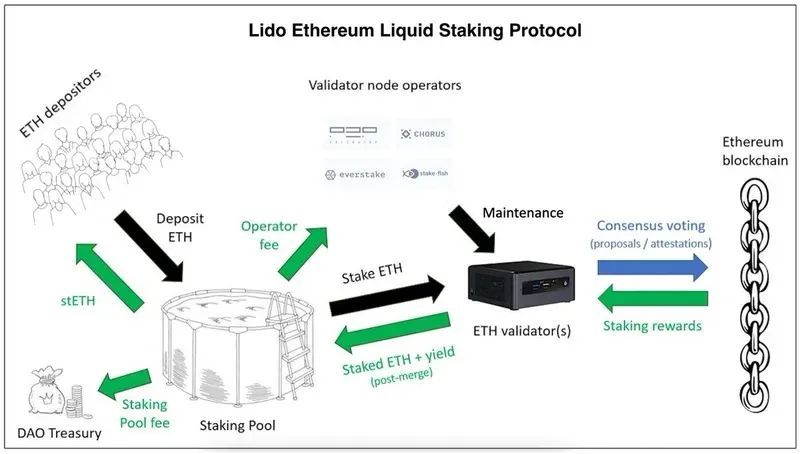

The two main components involved are users (stakers) and node operators (validators).

The key components of the protocol are the staking smart contracts, tokenized staking derivatives (st assets, such as stETH), and external DeFi integrations (such as Curve).

Node Operators

The first key component of the liquid staking protocol is the node operators, who are responsible for the actual staking work. Currently, node operators are added and removed through Lido DAO.

Lido's admission mechanism is initiated by the Node Operators Secondary Governance Group (LNOSG), which currently consists of representatives from 21 Ethereum node operators. When Lido launches on a new network, or the group believes it can handle a network and benefit from additional node operators, applications for node operators will be opened. The group evaluates applicants based on several factors, including reputation, past performance, and the security, reliability, and novelty they provide (irrelevant attributes). Once the group has assessed an applicant pool, it submits a recommendation list to Lido DAO for token holder voting. A good validator pool is crucial for Lido, as staking rewards and slashing penalties will affect all stakers through the liquid staking protocol.

Lido is also non-custodial, meaning node operators cannot directly access user funds. Instead, they must use a public validation key to verify staking asset transactions. To regulate incentive mechanisms, Lido node operators receive commission compensation from the staking rewards generated from delegated funds.

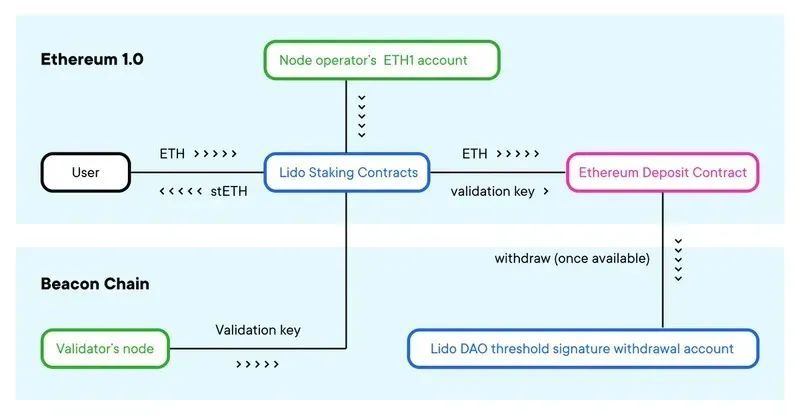

Staking Contracts

Users delegate their staking rights to node operators through Lido's smart contracts. The three main smart contracts are:

1. Node Operators Registry

The Node Operators Registry contract maintains a list of approved node operators.

Lido's Ethereum Staking Underlying Mechanism

Source: Lido Blog

2. The Staking Pool

The staking pool is the most important smart contract in the protocol. Users interact with this contract to deposit and withdraw crypto assets, mint or burn st assets. The staking pool uses the addresses and validation keys of node operators to uniformly allocate deposits to node operators in a round-robin manner. The staking pool contract is also responsible for distributing fees to the Lido DAO treasury and node operators.

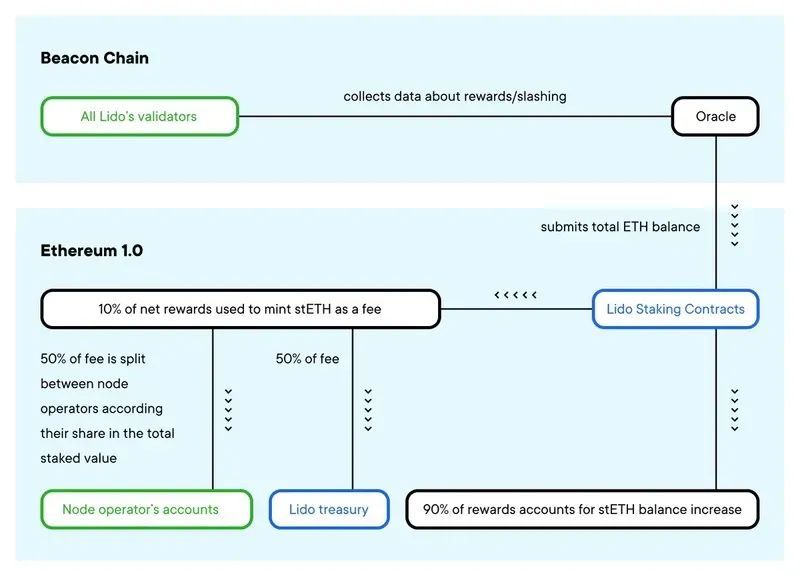

3. LidoOracle

LidoOracle is a contract that sends the balance of addresses controlled by the DAO to the ETH 2.0 side. LidoOracle is responsible for tracking staking balances. Net staking rewards (i.e., staking earnings minus the net gains from slashing penalties) are sent daily to the staking pool contract. The staking pool distributes 10% of the net staking rewards by minting proportional st assets: 5% goes to node operators, and 5% goes to the Lido DAO treasury. The remaining 90% of net staking rewards belong to st asset holders (i.e., stakers). Depending on the network, staking rewards may be reflected as an increase in the balance of st assets or an increase in the exchange rate.

How LidoOracle Interacts with the Ethereum Staking Pool

Source: Lido Blog

3. st Assets on Lido

Users who deposit assets into the Lido liquid staking protocol receive corresponding staking derivatives (e.g., stETH for staked ETH). Lido's tokenization of the staking pool effectively unlocks the liquidity of user assets, with st assets existing in two forms: rebase and shares.

The rebase form (such as stETH, stKSM, stDOT) refers to st assets minted on a 1:1 basis according to the deposited assets. To match the underlying assets, the balance of the pegged tokens changes daily with the accumulated staking rewards. Regardless of whether st assets are obtained from Lido staking, purchased from decentralized exchanges, or transferred from other holders, the balance of st assets will change daily based on accumulated rewards.

The shares form (stSOL, stMATIC) refers to st assets that capture staking rewards through appreciation, with rewards reflected in the growth of the st asset and staking asset exchange rate (for example, a stSOL:SOL exchange rate of 1.1 indicates a 10% staking reward for SOL). (Pegged tokens can be wrapped into share tokens.)

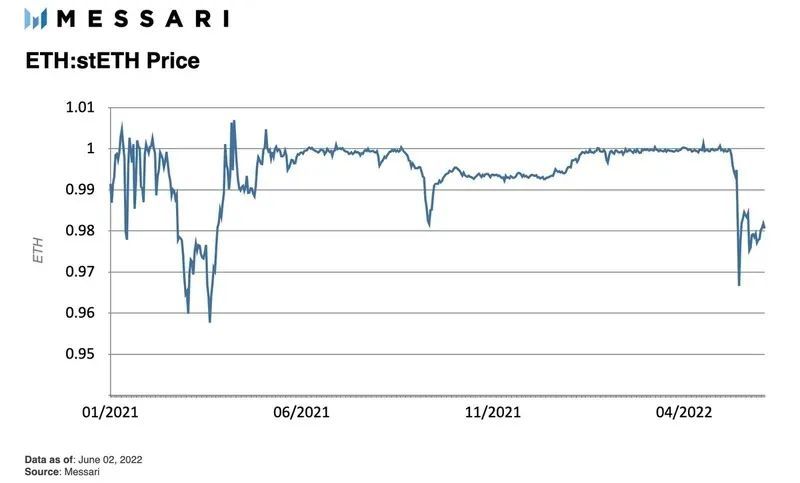

As of now, stETH accounts for over 98% of the total circulating value of st assets. stETH is currently a purely synthetic, closed derivative, as it can only be redeemed for the staked ETH after the Ethereum merge. Holders wishing to exchange stETH for ETH must rely on pricing and liquidity from exchanges (such as Curve, Uniswap, and FTX).

4. Lido's DeFi Integration

Lido and DEX Integration

To maintain the liquidity of stETH, Lido DAO incentivizes the Curve stETH:ETH pool, which is currently the deepest AMM pool in DeFi. Measures to incentivize Lido DAO tokens (LDO) and CRV by increasing the pool's APY (annual percentage yield) have attracted corresponding liquidity. Such pools on Curve, as well as Uniswap and Balancer, provide stETH holders the ability to exit before their staked ETH is unlocked.

The price of 1 stETH should not exceed 1 ETH significantly. This cap exists because 1 ETH can always be minted as stETH through the Lido staking protocol. However, the arbitrage mechanism for stETH is not as clear-cut as other arbitrage methods.

Since stETH cannot be burned on the Lido protocol in exchange for staked ETH, the current exchange rate relies on market price discovery within the cap. stETH has poorer liquidity, less utility (e.g., cannot be used to pay gas fees), and more technical (smart contract) risks than ETH. However, the price of stETH typically does not fall too far below the 1:1 exchange rate with ETH, as a low price would attract arbitrageurs to buy and hold, waiting for the unlock after the merge to profit from the spread.

Translator's note: This situation has changed, as the demand for holders to exchange crypto assets for stablecoins has increased with the decline of ETH, combined with the impact of events on the Celsius platform, leading to an imbalance in the stETH/ETH pool asset ratio, resulting in a significant drop in the stETH to ETH exchange rate. As of the time of writing, the exchange rate is approximately stETH:ETH = 0.95.

For other st assets, DEX liquidity remains useful, as it gives holders more choices: to exchange for liquidity or to stake and wait for unlock.

Lido and Lending Integration

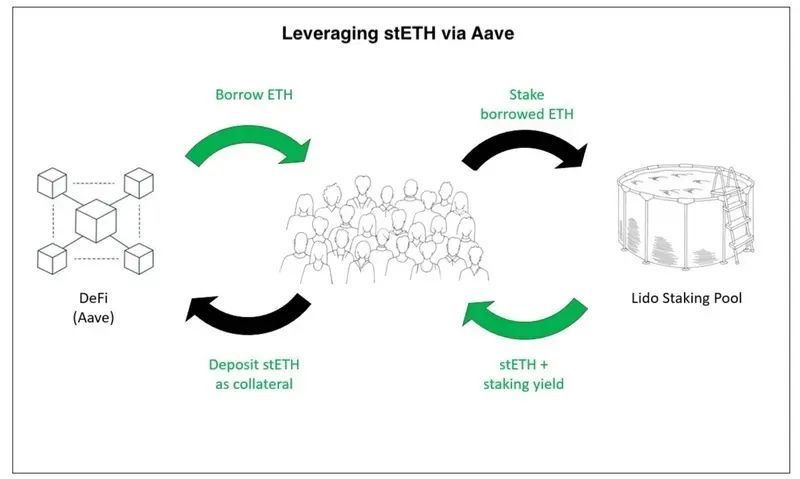

While Lido stakers can hold stETH or provide low-risk liquidity to DEX (with risks stemming from impermanent loss), they can achieve higher yields if they use st assets as collateral. For example, Aave and MakerDAO allow stETH to be used as collateral, while Solend allows stSOL to be used for loans. For instance, Aave can lend up to 70% of the value of stETH, and some individuals cycle borrow and then stake to achieve relatively high yields, but they also bear greater risks.

Source: @Leo_Glisic, Messari

Recent structured products, such as Index Coop's icETH, have started to provide stETH leverage through Aave while reducing some risks associated with managing collateralized debt. Nevertheless, events such as hacker attacks, governance attacks, slashing of multiple node operators, or overall market liquidity tightening could lead to consecutive liquidations and significant imbalances in the stETH/ETH trading pair. However, leveraging borrowed assets is a core capability for capital efficiency and is a method Lido attempts to address liquidity shortages and staking lock-up dilemmas.

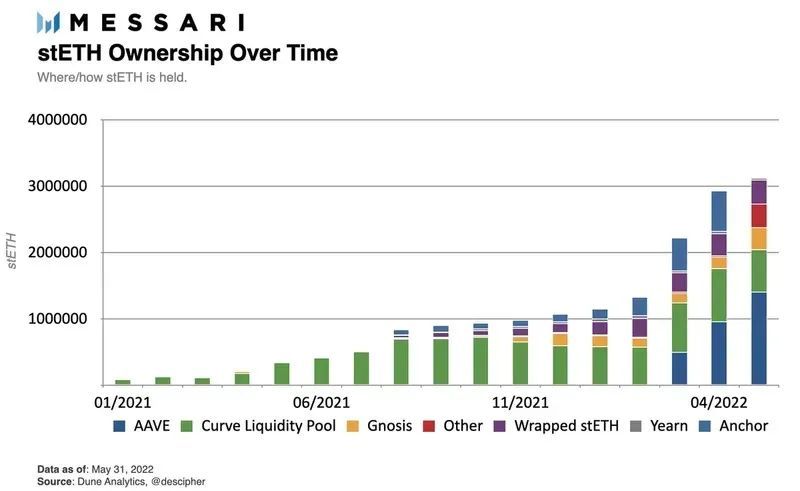

As shown in the figure, since Aave's integration at the end of February 2022, the scale of stETH has significantly increased. As of the time of writing, nearly 45% of circulating stETH is stored on Aave. The second-largest stETH pool is the Curve stETH:ETH trading pair. About two-thirds of the liquid stETH is divided between these two major protocols.

5. Competitive Landscape of the Staking Market

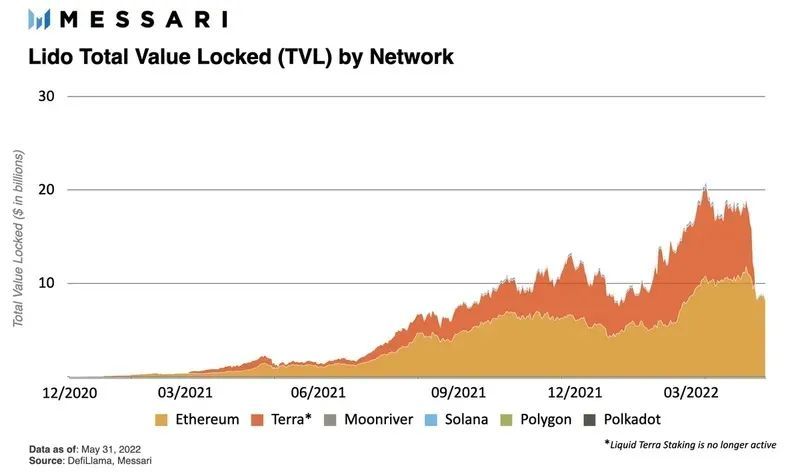

In early May, Lido briefly surpassed Curve to become the DeFi protocol with the largest TVL. Since the UST depeg, Lido's overall TVL ranking has remained around fourth.

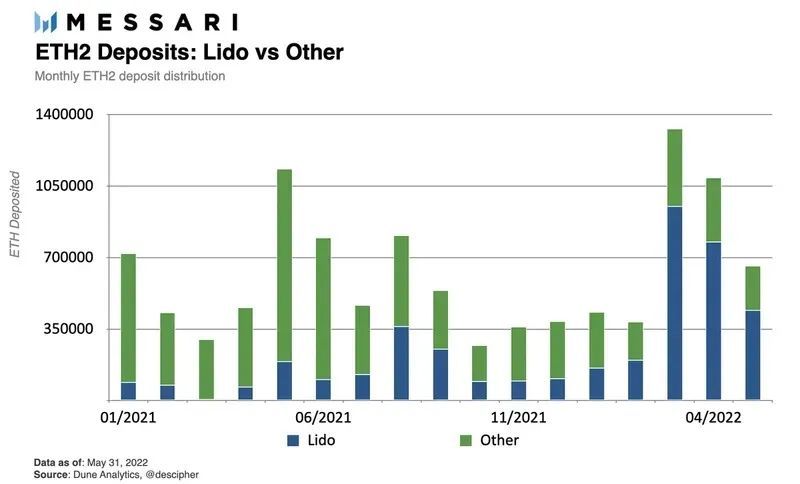

Entering May 2022, approximately 70% of new ETH2 staking deposits came from Lido. Overall, Lido's staking ratio accounts for 32.5% of the total ETH staked across the network.

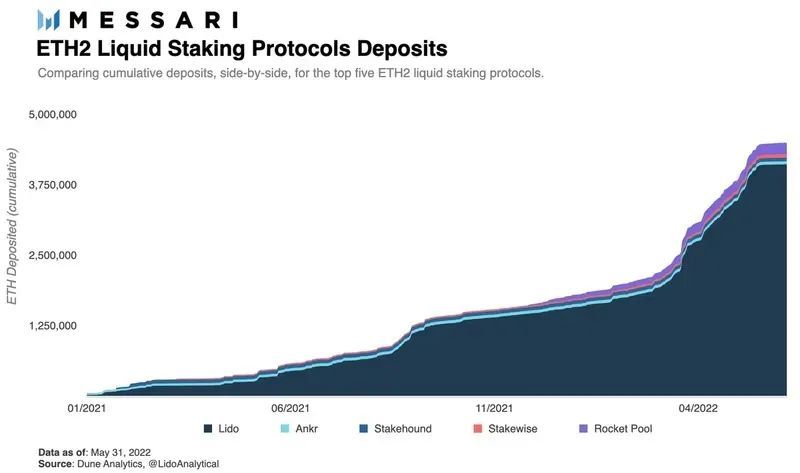

Lido holds over 90% market share in the non-custodial, decentralized liquid staking sector.

Lido's first market competitor, Rocket Pool, has gained some market position and publicity since its launch in November 2021. Although ETH staked on Rocket Pool has tripled, its market share in this niche remains below 4%.

Two differences between Rocket Pool and Lido:

1. The biggest difference is in the setup of validators. Lido's approach is to concentrate validators among professional, carefully selected node operators, while Rocket Pool aims to establish a permissionless validator set, ensuring staking security through economic incentives rather than the reputation/past performance of validators. While Rocket Pool's system does allow for broader participation in the validation process, it also leads to capital inefficiency (e.g., requiring node operators to provide 16/32 ETH for each validator), making expansion difficult.

2. The second major difference is in liquidity. Lido DAO currently spends over 4 million LDO monthly to incentivize liquidity across various chains and DEXs, with most of the spending focused on the stETH:ETH trading pair. Rocket Pool has no expenditures for liquidity incentives. Lido's incentive system promotes demand for stETH by reducing slippage and creating inherent basic yields for stETH holders.

Rocket Pool's later start, relatively poor liquidity, and lower rETH price (the asset received after staking on Rocket Pool) make it difficult for Rocket Pool to catch up with Lido. Therefore, stETH has become the default choice for users in the non-custodial liquid staking ETH market.

Another major participant in liquid staking ETH is Binance.

Binance's custodial nature makes it not a direct competitor to Lido. Moreover, while Binance has indeed issued liquid tokenized derivatives (bETH), this token does not generate additional value outside of the staker's Binance wallet, which is significantly inferior to stETH and rETH.

Overall, the three largest custodial staking solutions (Kraken, Coinbase, and Binance) have collectively deposited nearly 2.7 million ETH, about 60% of Lido's staking amount. Looking ahead, this gap is likely to widen, as the recently added staking amounts from Lido account for the vast majority of new ETH2 staking (70%).

ETH staking rewards are undoubtedly Lido's primary source of income, while Solana staking reflects Lido's multi-chain expansion aspect. First, Lido is not the winner in the liquid staking niche on Solana, where Marinade is the dominant player. SOL staked on Marinade is currently about 2.5 times that of Lido. However, from a broader perspective, liquid staking on Solana is just a small market that is easily overlooked, with the two largest protocols accounting for only 2.5% of the total staking amount. In ETH2, the two largest liquid staking protocols, Lido and Rocket Pool, account for 36% of the total staking amount.

The reason behind this may be Solana's native delegation feature and the higher liquidity brought by the 2-3 day staking cycle on that chain. While this complicates Lido's multi-chain expansion prospects, in terms of competition and product market fit, Lido's brand, cross-chain synergy, and dominant position in the massive Ethereum market still make its overall outlook promising.

6. Risks

Given Lido DAO's heavy reliance on Ethereum, any setbacks in the merge timeline or execution could lead to catastrophic consequences. While this article does not delve deeply into Ethereum 2.0, adverse events during the merge process could impact the ETH:stETH exchange rate, such as further delays in the transition period or trust crises surrounding the transition itself.

Given the re-collateralization of stETH, consecutive liquidations could exert further downward pressure on the price of stETH. However, if the merge proceeds smoothly, Lido will play a core role in the largest PoS chain.

The gradual decentralization choice allows Lido to optimize speed and scalability. While Lido has a first-mover advantage compared to competitors like Rocket Pool, the smaller pool of Lido's node operators has raised concerns about Ethereum centralization.

LNOSG is a committee composed of insiders that controls the initial planning process for selecting node operators. Even though the final list will be voted on by Lido DAO, the ownership of LDO tokens is concentrated among insiders. This has led to 21 professional node operators controlling all ETH shares of Lido on the Ethereum beacon chain, accounting for 32.5% of the total ETH staked. Additionally, the withdrawal credentials for ETH staked before July 15, 2021, are controlled by an 11-person multi-signature, which can be executed with just 6 signatures. If more than 5 signers lose their keys or act maliciously, approximately 600,000 ETH (about 15% of Lido's total ETH2 staking amount) could be locked. The Lido DAO team plans to migrate this portion of staked assets to 0x01 (upgradable smart contract) withdrawal credentials as soon as possible.

Furthermore, Lido has also developed relevant plans. Part of the plan involves adding permissionless validators. Distributed Validator Technology (DVT) will allow Lido to onboard new, unknown, untrusted node operators, pairing them only with trusted whitelisted node providers. These new validator groups will work together to propose and prove block production while maintaining mutual checks and balances.

The second part of the plan addresses the concentration of LDO ownership. This will empower stETH holders to oversee and veto DAO resolutions.

Conclusion

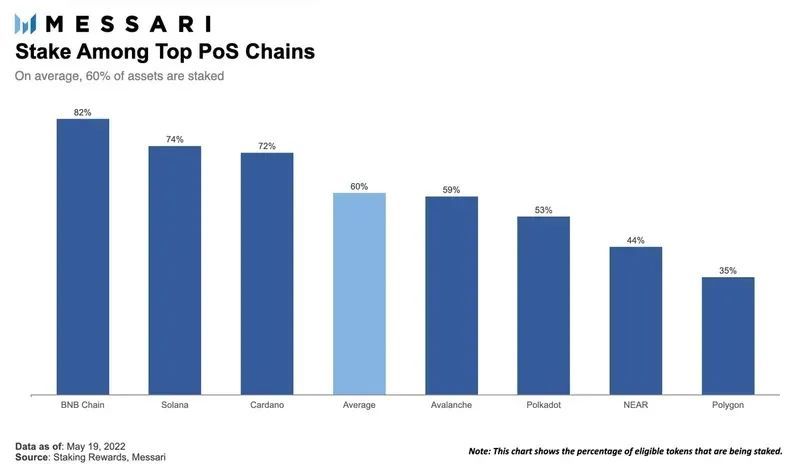

Currently, only about 10% of circulating ETH is staked. After the merge, stakers may choose to withdraw, and staking rewards could potentially double. If the staking ratio of ETH reaches the average level of the top PoS public chains, the overall staking of ETH could increase sixfold. In addition to benefiting from the upward trend, Lido will allow stakers to bypass the potentially months-long validator activation queue and start earning staking rewards immediately. Whether by providing lower yields or using part of its treasury assets to fill gaps, Lido is poised for another significant opportunity, which could solidify its position as the market leader in Ethereum liquid staking.

However, great power comes with great responsibility. Lido will play a core role in securing the largest L1 blockchain, directly or indirectly affecting the security of assets worth billions of dollars (as of the time of writing). Contrary to what critics may say, this is not inherently wrong. The long-term implications of Lido's dominance in the Ethereum network and the broader crypto ecosystem largely depend on how Lido DAO constructs a secure and truly decentralized protocol. In any case, Lido encourages ecosystem stakers to think in terms of years rather than days, weeks, or months, demonstrating the expected durability of the protocol. It is doing what combines a strong ecosystem with a powerful flywheel effect.