The "UST Defense War" has begun. Can Terra cope with this "de-pegging" test?

Price stability in extreme market conditions is an inevitable important growth test for stablecoins like UST, and it is also a sign of the project's maturity and sufficient anti-fragility.

Price stability in extreme market conditions is an inevitable important growth test for stablecoins like UST, and it is also a sign of the project's maturity and sufficient anti-fragility.Author: Terry, Plain Language Blockchain

Starting from May 8, the rumors of "UST decoupling" began to ferment significantly in the market, and the severity of the situation can be seen from the UST stablecoin exchange rates on centralized CEX:

The price of UST against USDT on Binance once approached 0.98, while UST in the substitute market was completely swept away. Accompanied by the spread of panic, UST and LUNA seem to indeed be facing an unprecedented new test.

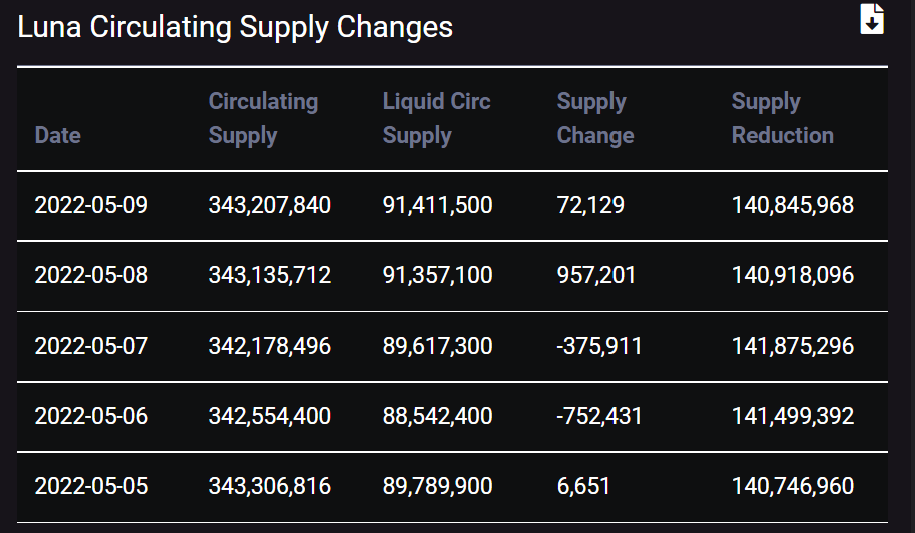

According to Terra Analytics data, on May 8, the circulating supply of LUNA increased by 957,201 coins in a single day, reaching a total of 91.357 million coins, setting a record for the largest single-day increase in circulating supply since April 8.

The Dual Peg Mechanism of Luna and UST

The core design philosophy of the Terra ecosystem revolves around how to expand the use cases and payment needs of the stablecoin UST, and the operation of UST employs a dual-token design:

Luna, the governance, staking, and validation token; UST, the native dollar-pegged stablecoin.

Simply put, every time a UST is minted, an equivalent value of one dollar in LUNA must be burned, and LUNA helps maintain the peg of UST to the dollar through an arbitrage mechanism:

Whenever the UST exchange rate is above the peg, users can send LUNA worth 1 dollar to the system and receive 1 UST; conversely, when the UST exchange rate is below the peg, users can send 1 dollar worth of UST to the system to obtain 1 dollar worth of LUNA.

In both cases, users are incentivized to engage in arbitrage, thereby helping to maintain the peg of UST to the dollar. This dual-token arbitrage stablecoin design, along with typical over-collateralization requirements, can easily lead to catastrophic large-scale liquidation events during severe fluctuations in the crypto market.

Previously, during the "5.19" crash in 2021, UST experienced a price "decoupling" due to a spiral liquidation, even decoupling by more than 10% at one point, nearly entering a confidence collapse and vicious cycle.

Whether it was the ETH liquidation during "3.12" in 2020 or the ETH "queue execution" during "5.19" in 2021, both validated the potential for massive destruction in extreme situations.

This is also a test that algorithmic stablecoins can hardly avoid, thus, in extreme market conditions, the stability of prices relative to the overall market is an unavoidable important growth test for algorithmic stablecoins like UST, and a sign of the project's maturity and sufficient anti-fragility.

Data Risks: From a data perspective, UST has reached a critical moment that far exceeds the "5.19" decoupling crisis of 2021.

The Inversion Risk of UST Market Cap and LUNA Market Cap

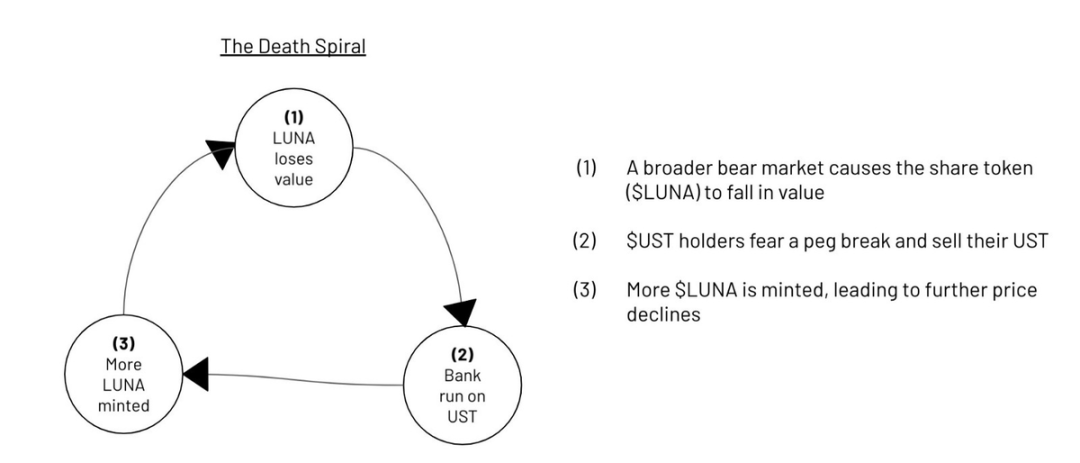

The main reason is the inversion risk between UST's market cap and LUNA's market cap: Previously, LUNA's market cap was always significantly higher than UST's market cap, which meant that when LUNA fell, there would generally be enough liquidation space to avoid extreme situations of insolvency, thus preventing a death spiral after a confidence collapse.

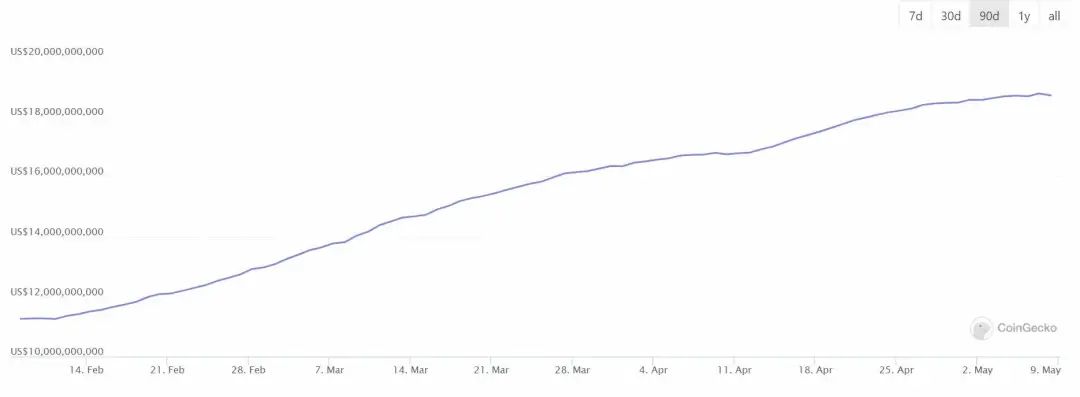

However, in the past six months, the circulation of UST has rapidly surged, exceeding 18.7 billion dollars as of May 9, with an increase of over 11% in the past 30 days.

This puts it in a delicate and awkward position------LUNA currently has a market cap of 22.4 billion dollars, while UST's circulating market cap is 18.6 billion dollars. If LUNA's secondary market price continues to fall, UST's circulating market cap may exceed that of LUNA.

Based on corresponding prices, if LUNA falls below 55 dollars, UST's circulating market cap will surpass LUNA's, likely leading to extreme panic in the market, triggering a "death spiral."

Intensifying Outflow Sentiment for UST

Confidence is more critical than gold, especially for algorithmic stablecoins like UST that rely on their ecosystem for growth.

However, the net outflow of UST from Anchor in the past two days has been about 2.3 billion dollars, with 1.3 billion UST flowing out on May 7, setting a new single-day record.

Compared to the peak of 12.7 billion dollars on May 5, the current UST deposits in Anchor have dropped by nearly 20%, triggering widespread panic among investors about UST's decoupling, and the redemption wave further increases the risk of a panic sell-off.

Insufficient Reserves in Anchor

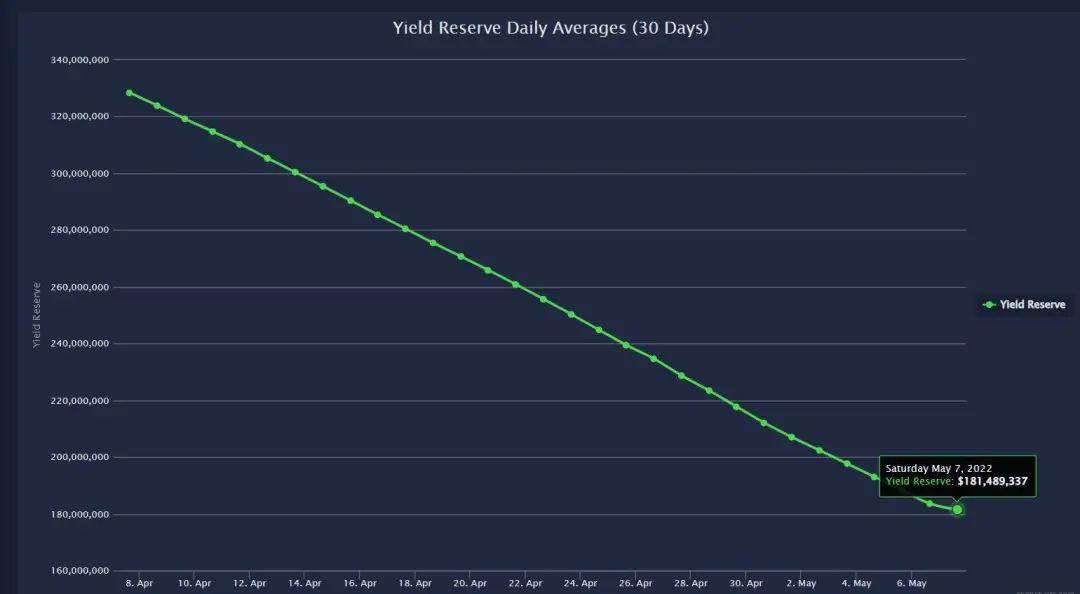

Currently, Anchor Protocol has a total daily expenditure of about 7.05 million dollars, total revenue of about 2.15 million dollars, and a net expenditure of about 4.9 million dollars, while Anchor's fund reserves still have 180 million dollars, which is expected to cover 35 days of expenditure needs.

What Resilience Does UST Have

The development confidence of UST and the Terra ecosystem is fundamentally supported by the Luna-UST pegging mechanism based on Anchor.

In the best-case scenario, it can maintain a scale of 1 to 2 billion, but the current issue is that UST's circulating volume has reached as high as 19 billion.

Support from Curve Pools

Thus, LUNA is also looking towards Curve to gain control over the "minting rights" in the crypto world, with the most direct approach being its 4pool scheme------a new Curve liquidity pool composed of UST, FRAX, USDC, and USDT.

By leveraging Curve as a minting rights market, it provides a peg guarantee in extreme situations:

veCrv ensures the stability of liquidity, preventing liquidity outflows when large asset exchanges occur; veCrv can serve as a governance tool for re-pegging after a decoupling, allowing hundreds of millions of dollars to re-establish the peg for billions of assets, something fundamentally impossible in Uniswap.

However, this construction has just begun and is facing this shock, with UST having only about 500 million dollars in liquidity on Curve, while there are over 10 billion dollars in deposits on Anchor.

Adjustments to the Anchor Model

UST deposits on Anchor are a double-edged sword for the life and death of the Terra ecosystem.

On March 24, the proposal by Anchor Protocol to "adjust the yield to a semi-dynamic interest rate based on the fluctuations of the yield reserves" was approved.

Starting from this week in May, its interest rate has been reduced from 19.5% to 18%. Subsequently, the Anchor Earn interest rate will also be dynamically adjusted monthly based on the appreciation or depreciation of the yield reserves, with a maximum adjustment of 1.5%, a minimum APY of 15%, and a maximum APY of 20%.

Meanwhile, at the end of April, Terraform Labs protocol researchers released a proposal suggesting that Anchor Protocol introduce the veANC model, and on May 7, the latest news indicated that the Anchor yield and governance platform Helm Protocol is about to launch, allowing users to deposit ANC into Helm to obtain the derivative token HELM of veANC.

In addition, Anchor has gradually added AVAX, ATOM, and SOL as collateral for borrowing, and according to the generally slow progress of the Terra ecosystem, the efficiency of Anchor has already been self-emergency extinguishing.

LFG's Bitcoin Reserves

As of now, the Luna Foundation Guard holds approximately 3.5 billion dollars in Bitcoin reserves, specifically for use in extreme situations------only to be used in emergencies, and will only be activated when LUNA's stabilization mechanism fails:

This means that in extreme situations where UST is being sold off in large quantities and LUNA's price is plummeting, Bitcoin, as a foreign exchange reserve with low correlation to the Terra economy, adds a policy tool for Terra to intervene in the exchange rate (maintaining the peg to the dollar).

Terra founder Do Kwon recently stated that the Bitcoin reserve mechanism of LFG to back UST will be deployed in a few weeks, and the Astroport team is currently implementing the design parameters of Jump Trading on Agora.

Conclusion

As a stablecoin anomaly that has surged rapidly in the past six months, with its market cap quickly approaching 20 billion dollars, the current "decoupling" test for UST will far exceed "5.19" in terms of both its intrinsic understanding and potential spillover impact.

Regardless of the final outcome, UST is destined to leave a significant mark in the competition for the holy grail of stablecoins.