New Experiment in Token Issuance: A Deep Dive into the "Locking + Liquidity Guided Auction" Model

"Locking + Liquidity Guided Auction" aims to achieve a fair distribution favorable to long-term stakeholders, minimize volatility in the price discovery process, and provide ample liquidity to promote growth and adoption, while fully complying with the requirements of all major regulatory frameworks.

"Locking + Liquidity Guided Auction" aims to achieve a fair distribution favorable to long-term stakeholders, minimize volatility in the price discovery process, and provide ample liquidity to promote growth and adoption, while fully complying with the requirements of all major regulatory frameworks.Author: Paul Hoffman

Original Title: 《Towards Better Token Distribution》

Compiled by: Aididiao, Foresightnews

With the introduction of a new blockchain protocol, decentralized application, or DAO (collectively referred to as "protocol"), one of the main questions that needs to be answered is, "How should the native tokens be distributed?" This is not a very complex question, but finding the right answer while considering all variables is crucial.

LLBA makes the community fairer

Fair token issuance should achieve multiple goals. First, some legal frameworks need to be considered, as any serious protocol should comply with legal regulations to protect itself and the token recipients.

For example, since the U.S. legal framework treats Initial Coin Offerings (ICOs) as a form of securities issuance, only U.S.-accredited investors can participate, making ICOs an unpopular distribution model. A large portion of crypto-economic participants are excluded from this issuance model; instead, as many users as possible should be allowed to participate in a fair token distribution.

Second, tokens should be distributed to the "right people." The right people are those who engage and generally align with the interests of the protocol. They are the ones who support the community long-term, actively participate, and contribute value to the ecosystem. Issuers should also strive to exclude token distribution manipulators, such as whales (those holding large amounts of a single token who can manipulate the market through absolute weight) or bots (who exploit their wealth or speed to gain an advantage in token distribution).

What do you think is fair distribution?

The third element is the price discovery process, which should not severely damage the holders' portfolios. This requires sufficient liquidity (the number of tokens at a specific price) and circulation (defined here as the percentage of available tokens relative to the total supply) to meet market supply and demand from day one.

The benefits of ample liquidity and circulation are quite direct. When a new token is released into the broader crypto-economic system through trading, price discovery can be very unstable and may be manipulated by wealthy participants. When liquidity and circulation are low, whales have the ability to significantly raise or lower the value of the token.

Although volatility may attract market attention, it is undesirable for the long-term sustainability of the protocol, as many people may be harmed during this price discovery phase, and you may inadvertently harm those who would otherwise become long-term stakeholders.

Consider a scenario where demand is high but supply is low; suppose the market is ready to buy 10% of the token supply, but the circulation is only 1%. When demand far exceeds supply, the token price will initially skyrocket. For token holders, this frenzy phase can be very exciting, but since 99% of the tokens have not yet entered the market, the value is purely constrained by supply and cannot be sustained. Therefore, the long-term outlook for the price is not optimistic.

Take Yearn Finance as an example. After facing criticism for being overly centralized, founder Andre Cronje quickly cobbled together 30,000 YFI governance tokens and airdropped them to early users of the protocol. Andre quickly pointed out that these tokens were worthless, would not be listed on exchanges, and only allowed owners to participate in Yearn's decentralized governance. However, the market did not agree with his assessment of value.

During the "DeFi summer" of 2020, many protocols witnessed explosive returns from their community governance tokens, and the market's thirst for YFI was insatiable. This ultra-low supply DeFi token was created by one of the most renowned developers in the field, making it a perfect moonshot recipe. Since the protocol did not engage in market making, liquidity was very low. Initially, only those hoping to profit from the airdrop would provide liquidity to automated market makers (AMMs). Market demand was extremely high, and several major exchanges immediately listed YFI after the airdrop, allowing thousands of investors to purchase the token in a short period.

Uniswap exchange YFI token price chart, priced in ETH

Thus, we can see that the result of a high demand, low supply scenario is a significant price increase, followed by a long, slow decline. This harms those who participated in the speculation and demoralizes community members who want to hold the token. Furthermore, those who obtained the tokens early have a high incentive to sell during the initial frenzy phase, which may lead to a lack of further participation. Both aspects are undesirable for the long-term prospects of a project.

Conversely, when demand is low and supply is high, a similar outcome (downward price momentum) can occur, but without the initial increase. This is because, in a situation of ample supply and insufficient demand, prices will generally trend negatively.

In layman's terms, as a protocol, you want to release an appropriate number of tokens to as many core community members as possible at a price that has already been "discovered" (close to fair market value). In doing so, you hope to establish a price discovery process over time through the advantages of the protocol.

Token Distribution Models

Let’s look at several examples of token distribution models and analyze their pros and cons.

Venture Capital

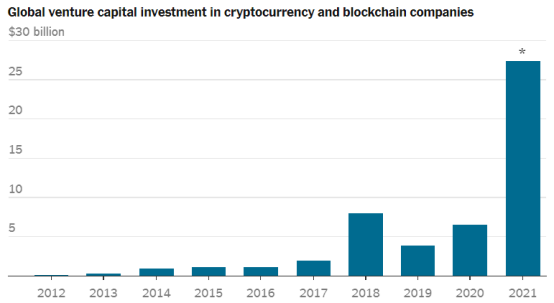

Considering the venture capital route, many protocols undergo Series A, B, or even C funding rounds before they are put into use (refer to this cool venture capital information source). Solana is an excellent example.

More money is flowing into cryptocurrency through VC than ever before

The benefit of the VC route is that Solana's developers can secure sufficient funding from the start, but equally important, VCs often have a network of experts, technicians, and developers to help develop products and provide feedback. With the support of VC funding and talent networks, Solana's developers can relatively quickly transition the project from idea to launch phase, focusing on the protocol rather than community building.

The downsides of this approach are also quite evident. VCs want a significant share of tokens for their investments. Given the enormous risks VCs take on a concept (Solana was just a white paper during its earliest funding periods), they also expect significant upside potential.

Solana's initial round sold at 4 cents per SOL, with over 16% of the initial tokens sold. The next batch was at 20 cents (13%), and the next at 22.5 cents (5%). In other words, a third of the existing Solana tokens cost between 4 and 22.5 cents, providing substantial returns for participating VCs.

I have no issue with people getting rich. The crux of the matter is that aggressive early seed investments can weigh down the protocol. Unlike those who buy because they believe in the project, these whales enter the market early at a significant discount, allowing them to sell at any price.

For VCs, no matter how visionary they are, those 1000x instant returns are a huge temptation. In fact, Solana has the largest "internal" token distribution ratio among all popular blockchains.

Then come ordinary users like you and me, who typically buy in at higher prices and then get dumped by the 1000x VCs. The result is poor, with ordinary users harmed, selling their chips at a loss. Consequently, they are less likely to use the platform or build on it, making it less likely to help establish a value-sharing community.

Here’s a bit of background: not all venture capitalists or angel investors are greedy whales or market sellers with bags full. Otherwise, the crypto world would be a loss-making place where only a few could profit. What I mean is that ideally, from the perspective of the protocol's lifespan, it is most desirable to have tokens in the hands of users who care most about the protocol.

The difficulty with the venture capital model is getting tokens into the hands of the "right people" without price discounts. However, the venture capital model is often a good way to kickstart, but it is difficult to sustain, and investors typically do not favor it.

Airdrops

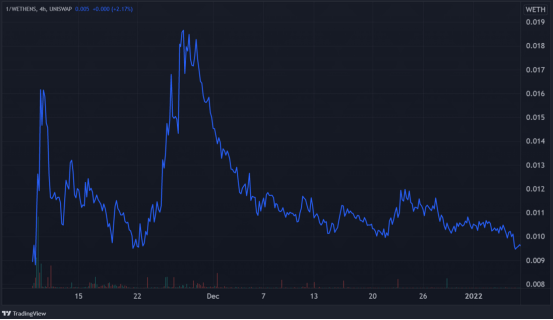

Another token distribution model is airdrops. The UNI of 2020, along with recent ENS, SOS, and LOOKS, has made this model quite popular. Each early user or ecosystem participant is allocated free tokens based on their ownership, participation, or similar metrics. Theoretically, this model is great because early users can try something and thus be rewarded.

However, there are also some issues here. First, a large number of airdrops come out of nowhere, and the price discovery process becomes highly volatile. ENS is a great example:

Chart showing the price of ENS tokens on Uniswap in the first two months, priced in ETH

Typically, airdrops are not announced in advance, so there is little time for the community to organize. These new stakeholders are expected to figure out the issues and immediately start governance. This creates a frenzy of energy after the token distribution, but as governance difficulties arise and the initial new energy fades, the enthusiasm behind the project can quickly dissipate.

While token airdrops are often accompanied by significant volatility and the community struggles to organize, they do yield some interesting outcomes. For example, designing a large and widely distributed circulating token is relatively easy, and it is also straightforward to reward the right users through their wallet interactions. After all, the blockchain stores an immutable record of these transactions. If you are a heavy user who has frequently used a particular protocol in the past, it is easy to be identified and receive appropriate rewards.

One potential downside of the airdrop model is the lack of mechanisms to secure early development funding. Since tokens are minted out of thin air and given away rather than sold, developers need a separate funding source to kickstart the project. Typically, this is done through retrospective token allocations to the development team, meaning all work done before the airdrop is compensated through sweat equity (labor without funding, to be repaid later when the protocol is launched and operational). Depending on the scale or complexity of the protocol, this may not be a practical way to start.

Both the venture capital and airdrop token distribution models have their pros and cons. In the project launch phase, VCs provide assistance but often lead to an uneven token distribution. On the other hand, airdrops are easier to balance token distribution but come with unpredictable price volatility, making it difficult to create an orderly environment.

New Competitors in Token Issuance Models

Lockdrop + Liquidity Bootstrap Auction, or LLBA for short. LLBA is touted as an innovative token issuance strategy proposed by Delphi Digital. Delphi is a reputable research institution focused on leveraging this model to serve early projects. If this issuance method is deemed successful, it will be emulated by other blockchain projects.

Next, we will detail Delphi's LLBA distribution model, how it theoretically works, how it is implemented, and its pros and cons compared to other models.

Lockdrop + Liquidity Bootstrap Auction

The "Lockdrop + Liquidity Bootstrap Auction" (LLBA) is divided into three phases. The first phase is the lockup phase, also known as the distribution phase. In this phase, tokens are distributed to stakeholders of the protocol, but these tokens cannot be circulated immediately.

The second phase is the liquidity bootstrap auction, which is the price discovery and liquidity establishment phase. Here, token recipients can submit their tokens to a liquidity pool composed of launch tokens and stablecoins. The second phase is essentially a two-step auction phase based on market price discovery. This mechanism is crucial for reducing risk, and we will spend more time detailing this mechanism later.

Finally, the third phase is the unlocking of airdrops and the beginning of public trading of the tokens.

In short:

First phase: Distribution

Second phase: Auction (composed of two parts)

(1) Part one: Accept all token and stable deposits, only allowing stablecoin withdrawals.

(2) Part two: No further deposits accepted, available stable withdrawals are limited, and the auction ends with a tapering down to 0%.

- Third phase: Public trading

First phase: Distribution

Assume a protocol with a native token "TOKEN." Remember, the first phase distributes tokens to users and stakeholders of the protocol. Here, tokens need to be distributed to users who bring the most value to the protocol. How to measure this value is entirely according to the protocol's requirements.

For the recently launched Astroport, tokens were distributed to users providing liquidity in key trading pairs. For Altered State Machine, tokens will be allocated to users holding genesis NFTs (ASM brains and AIFA All-Stars).

The airdrop distribution method is also regulatory-friendly because it does not require the protocol to sell tokens to fund operations (ICO model). The LLBA distribution phase is similar to an airdrop because users can earn rewards by using the protocol, holding NFTs, or providing services. This is what I consider a retrospective airdrop. In other words, this airdrop rewards users for past contributions to the protocol or ecosystem. However, an interesting twist of the LLBA distribution model is that it also includes a forward airdrop, in a sense rewarding users for their long-term commitment to using the protocol.

For example, users who agree to lock their tokens for a longer period may receive a larger share. This approach is similar to how Yearn Finance and ve(3,3) reward users who lock their respective tokens for longer periods, with the difference being that it applies to airdrops rather than staking programs.

The way the LLBA first phase distribution works is similar to conventional airdrops, with the added functionality that those making forward commitments will be rewarded. The goal is to reward the right users, namely those committed to long-term use of the protocol.

Additionally, users making forward commitments are incentivized to contribute to the protocol and community in its early stages to help ensure its success.

Second phase: Auction

The second phase is the liquidity bootstrap auction. The core function of this phase is price discovery, and secondly, to create deep liquidity at the discovered price.

Here’s how it works: users who received tokens in the distribution phase can choose to deposit some or all of their tokens into the liquidity pool. Typically, this is a token/stablecoin trading pair, but other liquidity pairs can be considered. Assume in this example, TOKEN is paired with the stablecoin DAI.

Adding tokens to the liquidity pool increases their supply relative to the deposited DAI, thereby lowering the price. On the other hand, market participants who missed the airdrop (or anyone wishing to buy more tokens) can increase DAI liquidity in the trading pair and gain exposure to the tokens before they are listed; this raises the inferred price of the tokens and creates demand. During the auction phase, a natural balance of supply and demand will form, establishing a fair price.

As more tokens and stablecoins are added to the liquidity pool, the TOKEN-DAI ratio will adjust to reflect the new reality. Simply put, if more tokens are added (increasing supply), the price will drop. If more stablecoins are added to the liquidity pool, the price will rise (increased demand).

The more bidders, the higher the price

In our simplified example: if the auction collects 100 TOKEN and $100 of DAI in the liquidity pool, the price of 1 TOKEN is $1. If another 100 TOKEN are added to the pool, increasing the total number of TOKEN to 200, the price will be $0.50 each. Conversely, if there are 100 tokens and $200 of DAI in the pool, the price of each TOKEN will be $2.

Additionally, it is crucial that the auction phase is actually divided into two parts. In Part A, anyone can deposit as many tokens and stablecoins as they want, but can only withdraw stablecoins.

Delphi's team explains why individuals can only withdraw stablecoins. The simple reason behind this is that it makes the pricing mechanism less complicated, making it easier for users to use and predict.

In Part B of the auction phase, the percentage of stablecoin liquidity that can be withdrawn from the pool is restricted over time, gradually locking this liquidity into the pool.

For example, in the early throttling phase, you might be able to withdraw up to 50% of DAI. Later it might reach 65%, so you can only withdraw 35% of DAI. On the last day, in the final hour, throttling might reach 99%, allowing you to withdraw only 1% of the stablecoin deposit.

In addition to this restriction mechanism, only one withdrawal can be made during this period. This is clearly to prevent users from withdrawing 50%, then 50% of the remaining 50%, and so on, thereby gaming the system.

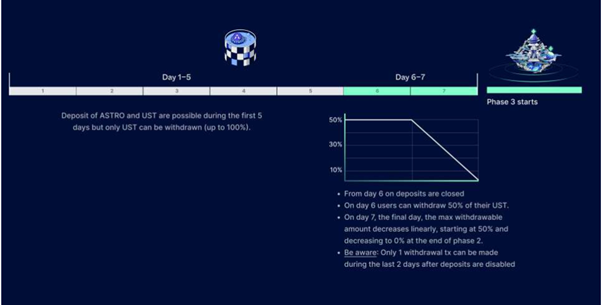

Here is a practical example of the two-part Phase 2 auction implemented by Astroport:

Using Astroport: the auction is split, with Days 1-5 being Part A: deposits, and Days 6-7 being Part B: limited withdrawals.

The goal here is to achieve price discovery in a very reasonably predictable manner. The throttling and single withdrawal are designed to ensure that whales cannot game the token price discovery by dumping tokens into the pool or withdrawing all stablecoins at the last moment. I will discuss this issue further in the critical analysis section.

For now, just understand that the auction phase achieves a market price without price discovery volatility, providing an opportunity for users who missed the initial distribution to purchase at a market-priced fair price, while suppressing market manipulators from gaming the distribution model.

Equally important is that since users are trading with other users rather than the protocol selling tokens to users, this is not considered illegal securities sales from the perspective of U.S. regulation.

Another important point is that participation in Phase 2 requires users to submit their tokens to the liquidity pool, which may expose users to impermanent loss; thus, users typically need incentives.

Liquidity providers can be incentivized in various ways, but generally, the fairest method is to share a predetermined number of tokens among liquidity providers (possibly 1-2% of the total supply). The benefit of this implementation is that it is easy to execute and proportionally rewards users based on the risk they take (fewer liquidity providers = higher returns), with no long-term adverse effects.

Of course, other incentive mechanisms can also be considered.

Third phase: Public Trading

This part is simple: Phase 3 opens the liquidity pool to a broader range of participants in the crypto-economic system. Historically, this milestone triggers a flurry of trading activity for significant protocols and may lead to price volatility. The LLBA model should slightly mitigate this volatility, as token holders are incentivized to lock their airdrop rewards, and the auction phase allows for early price discovery mechanisms. This makes the market release of the tokens less speculative, with lower volatility, and easier to enter or exit.

Critical Analysis

Lockdrop and Liquidity Bootstrap Auction (LLBA) is novel and has considerable advantages compared to other token distribution models.

In short, LLBA aims to achieve a fair distribution favorable to long-term stakeholders, minimize volatility in the price discovery process, and facilitate sufficient liquidity for growth and adoption, while fully complying with all major regulatory frameworks.

It can be argued that the decentralization of token holders is seen as an advantage of LLBA. "The potential impact of pre-release builders on post-release token-based governance is diluted, making governance more decentralized earlier than usual," writes Jose Maria Macedo.

However, in the sense of achieving an average distribution where all issuance participants receive equal shares, achieving this is not a core feature of LLBA. In short, wealthy market participants will not buy larger shares of available tokens during the distribution phase and before, so they can still play a significant role in the token economics and future of the protocol. Modern NFT releases can more easily achieve widespread and fair distribution.

This does not in any way tarnish the distribution method, as the goal is not to prevent whales from using their wealth to participate in token issuance; it is to prevent whales from manipulating token distribution. This is reinforced by refusing token deposits after a certain time and restricting the withdrawal of all stablecoins at the end of the auction phase.

To be precise: without these two functional parts of the auction phase, market manipulators could add large stablecoin positions to the pool in the early auction phase, thereby inflating the implied token price. The effect is that the token is perceived as overvalued (demand exceeds supply). In turn, overvaluation would entice more token holders to deposit tokens into the liquidity pool and deter other stablecoin depositors from participating. This effectively creates a situation where market manipulators are the buyers of most tokens because they have already outpaced competitors in the early stages.

The next step is for market manipulators to remove most of the stablecoins before the auction phase ends, thereby depressing the token's value without giving auction participants enough time to remove tokens from the pool (lower demand = lower price) or recognize the new pricing reality and add stablecoins to the pool. Another outcome of this situation is that once public trading begins, it can significantly lower the price, granting market manipulators a large number of the same tokens.

The LLBA model succeeds in curbing manipulation by ending token deposits in the second part of the auction phase and limiting the removal of stablecoins. Theoretically, this can prevent manipulators from causing volatility in token prices at the last moment, thus taking a step in the right direction toward establishing a fair price discovery mechanism, allowing all participants sufficient time to react.

Potential Downsides

The LLBA model requires a high level of trust in the development team, as users cannot access their tokens as part of the lockup. Unlike the airdrop model, which distributes all tokens from day one, the LLBA model requires users to trust that the team will not liquidate their tokens during the lockup period.

This capital inefficiency and inability to respond to protocol developments, broader market conditions in the crypto-economic space, or other news is one of the main drawbacks of locking tokens—this is a risk that early investors must weigh when deciding.

Another factor to consider regarding extended lockup periods is that secondary markets may emerge where locked positions can be traded at lower costs. This has a significant impact on price discovery.

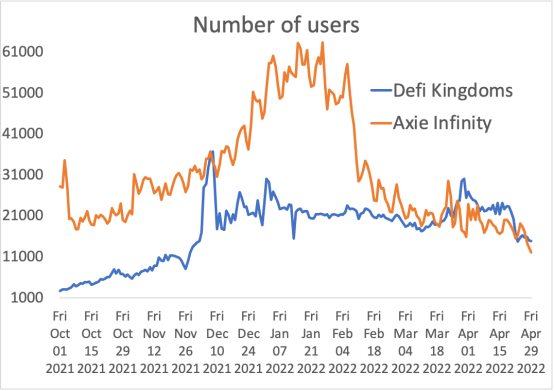

To illustrate how this can happen, I will use the recent developments of DeFi Kingdoms (DFK) as an example. In DFK, users are incentivized to stake, and once they bet, newly minted tokens unlock over time (up to 1 year). Users discover that these locked positions can be traded off-market, especially at lower prices.

DeFi Kingdoms was once one of the most popular games in the crypto space

As more users become aware of this price fluctuation, they begin to sell unlocked tokens for more locked tokens, causing the price of unlocked tokens to suffer greatly. For those seeking long-term value, buying locked tokens becomes much cheaper (for example, each JEWEL token locked for 10 months is $2, while the price of unlocked JEWEL is $17, although it is traded over the counter, I have no other evidence besides rumors). Consequently, DFK developers have proposed and passed changes to the smart contracts to stop this off-market trading behavior.

This example shows that tradable locked positions can harm the interests of lock and auction participants. Therefore, it helps to keep a close eye on tradable locked positions and carefully consider whether participating in locks and auctions is worth the risk.

Essentially, trading such derivatives of locked tokens creates an unexpected price discovery mechanism. In another example, Altered State Machine (ASM) will launch using LLBA, but the NFTs granting users fair shares will be publicly traded in the market. This undermines some of the important work LLBA does in price discovery and suppressing volatility.

This example is not the most controversial aspect of the LLBA model, simply because ASM NFTs provide additional utility on top of what is required for the airdrop, in which case price discovery does not suffer significant volatility. Additionally, for savvy investors, if the protocol succeeds, this mechanism can provide a favorable entry point.

When considering or studying the LLBA model from an investor's perspective, it is essential to critically analyze the mechanisms that determine who receives how much of the token distribution scale. Any project that initiates LLBA using NFTs or tokens (without additional utility) should be scrutinized, as this could undermine the legitimacy of the LLBA model.

LLBA is a Step in the Right Direction

Achieving perfection in token distribution is challenging. Distributing tokens to the right people, avoiding regulatory pitfalls, and ensuring the model is not manipulated is a daunting task.

LLBA aims to achieve this by adding forward incentives to airdrops through token lockup for additional rewards, hence the term "lockdrop." In turn, token holders can place these tokens into liquidity pools, where price discovery occurs from the moment LLBA transitions into Phase 3 of open trading, aiming to provide ample liquidity in a non-volatile, non-corrupt manner.

However, some criticisms are also valid. For example, the LLBA model is not all-encompassing, meaning that if token distribution is based on NFTs or secondary tokens without utility, price discovery before LLBA may be unstable. As demonstrated by the DeFi Kingdoms example, the current value of tokens can be significantly affected by off-market trading, which offers substantial price discounts on locked tokens (similar to reverse trading in futures markets). This undermines the lockup process and fair price discovery, negating many of the benefits LLBA initially offers.

While LLBA is complex, it ultimately seems to be a significant step in the right direction. It provides a framework where volatility is limited, but price discovery occurs naturally. Initial liquidity is high, tokens typically flow to the right users, and crucially, it does not violate U.S. securities laws.

It will be exciting to see how protocols iterate on the LLBA model to achieve successful token issuance. Observing where or how the model's future implementations succeed or fail, and how they can be improved, will also be interesting. Once some new case studies provide more insights into the art of token distribution, follow-up analysis will be due.