Haberg Tax, Crypto Economy and 21st Century Economics

The Harberger tax is a fascinating economic model that trades off investment efficiency for distributional efficiency, resulting in significant welfare gains. In practice, it is indeed challenging to implement, but blockchain provides us with the ability to test its effectiveness and usefulness.

The Harberger tax is a fascinating economic model that trades off investment efficiency for distributional efficiency, resulting in significant welfare gains. In practice, it is indeed challenging to implement, but blockchain provides us with the ability to test its effectiveness and usefulness.Author: Simon de la Rouviere

Translator: zik, The SeeDAO

The Habermas tax is an economic policy aimed at balancing pure private ownership and complete public ownership to increase overall social welfare. It helps ensure that society utilizes property more effectively, enhancing overall economic productivity and social welfare. It retains the power of the market while reducing the use of currently inefficient property distribution methods. It reduces the monopolistic phenomena that exclude overall social welfare from the capacity for capital wealth creation at the relative cost of investment returns.

Recently, with the profound description in Glen Weyl and Eric Posner's book and paper "Radical Markets," the theory that "property is just another name for monopoly" has gained popularity.

It introduces two definitions to illustrate how property ownership operates:

Citizens value their own property and pay taxes based on that value: a self-assessed tax.

At any time, others can purchase that property from you at this price, and you must sell.

Investment efficiency is defined as the owner's ability to invest in their property to increase its value. Under the Habermas tax model, the possibility for everyone to invest in assets decreases because anyone can force you to sell your assets.

Distribution efficiency is defined as the extent to which property is allocated to the most productive individuals. Deadweight loss refers to the reduction in social net economic efficiency due to misallocation of resources (e.g., setting prices too high or too low). This is particularly true in property ownership, as illustrated by the bargaining problem proposed by Myerson and Satterthwaite: The root of the mismatch in all these examples is the same: private property owners "hold out" for a price that a buyer may not be able to afford, leading to delays or failures in transactions, even when the buyer's use of the property could be more efficient than that of the owner. Sellers always quote prices higher than their minimum acceptable price, which is in the seller's interest, while buyers always quote prices lower than what they are willing to pay, which is in the buyer's interest. Due to these bargaining issues, depending on who decides the quote, if the reservation price is not understood, it can lead to ineffective turnover of assets.

With the Habermas tax, asset owners cannot set excessively high monopolistic prices (which are costly for them), nor can they introduce additional costs for bargaining (as prices are always set by the seller), making it easier for the market to allocate property to productive owners.

The Habermas tax reduces investment efficiency but increases the efficiency of ownership allocation. It represents "partial common ownership."

It is estimated that due to the secondary losses from private ownership monopolies, as well as the benefits gained from increased allocation efficiency due to reduced investment efficiency, there will be tremendous benefits to welfare (and society as a whole). In most calibration models, the Habermas tax achieves a maximum possible allocation welfare gain of 70% to 90%, while investment losses only erode these gains by 10% to 20%. In addition to more effective utilization of assets, it can also generate significant additional revenue. In the paper, they introduce various ways to use this new revenue.

1: 21st Century Economics

A century ago, the global population was estimated to be less than 2 billion.

A century ago, after World War I, the world moved away from monarchy as the primary form of human social governance, with democracy establishing its dominance only in the 1990s.

The history of the World Wide Web is 30 years.

In many ways, we are living in the greatest period of transformation in collective history. Almost everything is different compared to previous generations, which is an extraordinary social change.

Extreme poverty is sharply declining globally: from an estimated 80% in 1820 to less than 10% in 2018. Despite this astonishing growth, we still face a range of issues, including increasing inequality, worsening climate change, and imminent technological unemployment. Although emerging economies are growing rapidly, global inequality has worsened since 1980: the income growth of the top 1% is twice that of the bottom 50%. This inequality is largely due to the transfer of public wealth to private wealth.

While the growth of the world economy has lifted all boats (for the poorest), it has also exacerbated inequality. As technology increasingly provides more leverage (e.g., a top tech company controls all the cars on the road), inequality may continue to widen. This is particularly evident in the global middle class, which has seen the least growth over the past few decades.

There are concerns that these trends will not stop. Capital owners will gain more growth than others. When automation occurs, technological unemployed individuals will struggle to find new jobs. Technological leverage will benefit only a few. There is a sense that this trajectory of development is not very optimistic for the majority of society. Our recent "savior," the so-called "sharing economy," is entering new markets at lower prices, but ultimately, most of its value ends up in a few companies on the U.S. West Coast.

While this may not be a bad thing in itself: our current economic model has indeed brought about tremendous economic growth. Even considering the costs, overall, this may be our best option: because we are improving the lives of the general public, the fact that that 1% continues to gain more growth than other members of society seems not to matter much.

While this may not be a bad thing in itself: our current economic model has indeed brought about tremendous economic growth. Even considering the costs, overall, this may be our best option: because we are improving the lives of the general public, the fact that that 1% continues to gain more growth than other members of society seems not to matter much.

However, increasing inequality is correlated with rising social dilemmas. Writers like Thomas Piketty, Joseph Stiglitz, and Richard Wilkinson have demonstrated the problems society faces as inequality increases. People lose trust, happiness, social mobility, and economic growth.

How can we reduce the power of capital in widening this equality gap? Progressive taxation has been recommended in the past and is considered one of the reasons for the relatively stable inequality in Europe.

What I like about the Habermas tax is that it proposes a very intriguing alternative. Like UBI (which itself is a complete blog post), it is an idea that allows more people to have more choices. While progressive taxes can ensure that inequality does not widen, they do not truly provide more people with the opportunity to create wealth. Progressive taxes also rely more on an effective state to allocate income appropriately in productive ways.

2: From Cadastre to CadAstra (To the Moon!): Building a New Economic System Using Blockchain and the Habermas Tax

Theoretically, the Habermas tax is very interesting, and there are reasonable criticisms of it, but I believe it is absolutely worth exploring and experimenting with. The problem is that, even with political resistance, it will inevitably be difficult to operate without more research in practice.

For example, when people are forced to sell property, the idea of "forced eviction" can be countered; is the practice of constant self-assessment really "fair"? Most of these issues can be alleviated (as described in the paper), and ultimately may not be a big problem in practice: we are always accustomed to maintaining the status quo, only seeing the negative aspects of change.

When the Habermas tax was first proposed, one of the biggest problems was the lack of tools and technologies for implementation, but with the development of modern technology, we now have more options to try. Everything indicates that a significant reason for not using the Habermas tax in the past was that without modern information technology, implementation would be difficult, requiring relatively low tax rates, and the welfare gains generated would be limited, with real benefits only growing in the coming years. Our framework provides a way to understand and predict the co-evolution of market technology (produced by the private sector) and property rights (produced by the government). Fortunately, we now have the ability to experiment with this on a new scale, to verify whether the Habermas tax is practical.

For example, the use of cadastre mentioned in the paper: a global record of property and related prices, which is very suitable for implementation using blockchain. But in the 1960s, when the Habermas tax was first proposed, the situation was not at all like this.

Moreover, blockchain is a mature breeding ground for experimenting with closed-loop economies, as anonymous assets on the chain can be executed using only ledgers. This is particularly true in the new and growing NFT space, such as CryptoKitties. Jacob Horn has previously explained the value of conducting continuous auctions in this field: you can always know what others are willing to pay for your collectibles. We will see continuous auction forms on NFTs, imagine Ebay, but you can see the market without actively putting your possessions on the shelf.

We will have a trustless, highly liquid market where anyone can bid on what you own (even if you are not actively selling).

Whether you like it or not, you can know the price trends of these unique assets. You also know that the buyer's bid is legitimate because it has all been signed, and all you have to do is click "accept." The right to price information shifts from the buyer to the seller. This has now become possible.

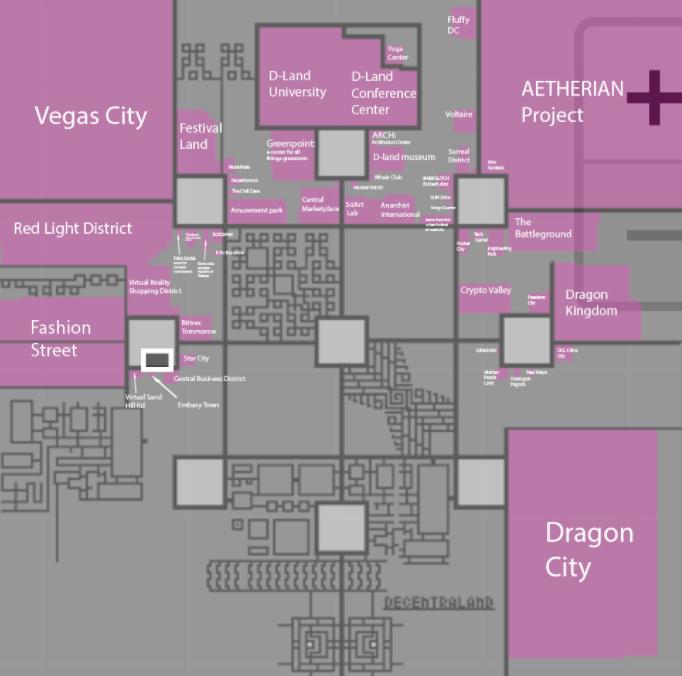

Additionally, projects like Decentraland already have provably scarce digital land in their virtual worlds. You can see people buying and selling parcels here: https://market.decentraland.org/

This also brings another value: these closed-loop ecosystems can use taxes to fund development and research, and can also redistribute through new redistribution mechanisms.

For example, as a new distribution scheme, taxes can be deposited into a curve bond, allowing the guidance of network effects and entering a public funding pool without the need for voting. If you pay taxes in this curve bond-based growth economy, you will be incentivized to continue holding rather than exiting immediately.

For example, as a new distribution scheme, taxes can be deposited into a curve bond, allowing the guidance of network effects and entering a public funding pool without the need for voting. If you pay taxes in this curve bond-based growth economy, you will be incentivized to continue holding rather than exiting immediately.

Let’s return to the beginning; there are even other possibilities, such as my idea of a Habermas pixel map: take a pixel image (like Reddit's The Place) and derive its ownership through the Habermas tax.

You set the price for your pixel and pay a 2% tax. If you do not do this, anyone can initiate a forced sale, meaning the pixel will be sold in a reverse Dutch auction.

Anyone can purchase pixels from you. You can change the color to whatever you want.

Taxes are distributed to pixel owners as their basic income from collective artistic creation.

What about the art generated by autonomous artists (Artonomous)? They earn income not only from the art they create and sell but also from taxes.

And when you extend the coordination capabilities of blockchain from closed-loop economies to the real world, the possibilities become even more exaggerated.

What would happen if you used the Habermas tax to sell your attention points? Is the tax your basic income?

What if the Habermas tax is applied in a community where members can buy and sell access to the community? Is the tax the basic income of this community?

In the most extreme case, we could adopt the Habermas tax in the real world. The tax generated by a more productive distribution system can only be obtained by those members who join the system. The implementation of this system has a prerequisite: if a member does not comply with the system's agreements, their shares will be forcibly sold. Projects like Delphi have achieved this. The system can only work if the cost of leaving the system is very high, which may ultimately mean that the cost of joining the system is also high. But at least theoretically, choosing to join such a tax ecological system is not without possibility, and of course, this remains to be further explored.

3: Conclusion

The Habermas tax is a fascinating economic model that trades investment efficiency for distribution efficiency, resulting in significant welfare gains. In practice, it is indeed difficult to implement, but blockchain provides us with the ability to test its effectiveness and usefulness.

You may have noticed that in many of my articles, blockchain has always been a way for me to face this new world, to explore new agency and authorization methods to cope with the rapid changes in economic, technological, and political challenges. It offers so many opportunities to reimagine how people work together and how to coordinate society as a whole. Curation Markets and Curved Bonding are examples of what I hope will empower content creators and communities to self-determine. The Habermas tax is another option among them.

The Habermas tax may just be another naive theory that is not feasible in practice, and choosing to participate in these blockchain experiments will enable us to better study and understand it. My intuition is that the Habermas tax will be widely used in the future.

I hope to see a future where we collectively try to choose to join new N-sided contracts to increase our own and each other's collective welfare. According to Coase's theory of the firm, lowering transaction costs allows us to form new organizations and create new wealth. Smart contracts and blockchain give us the opportunity to establish these new post-national collective coordination games. We can envision a world where funds transparently flow into competitive and effective ecosystems.

In these games, there may be a pathway for us to escape the impending social dilemmas. It is already a bit late; let’s get started.