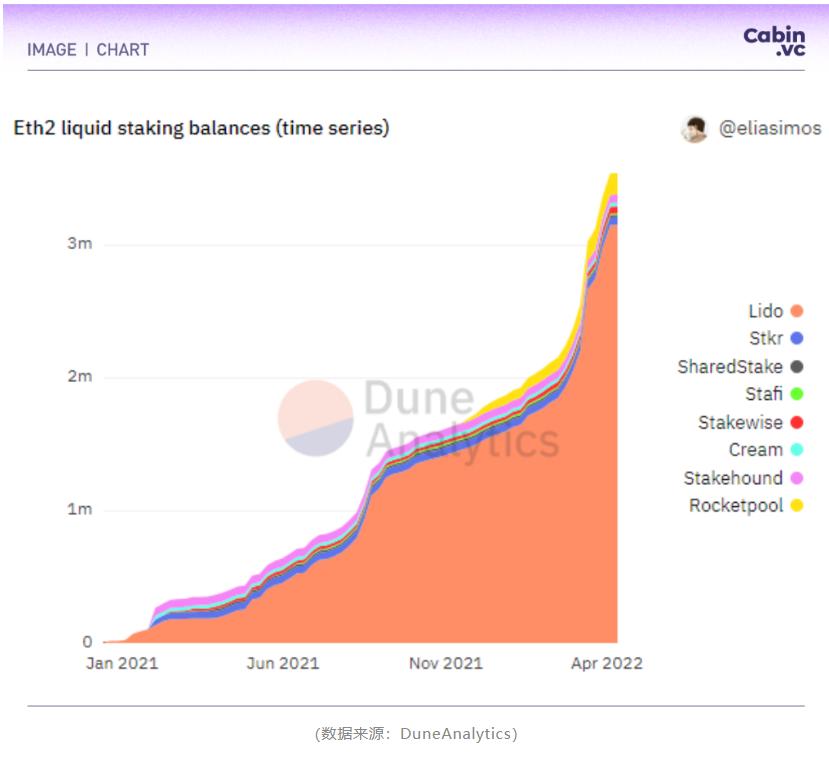

The Merge intensifies deflation expectations, with the amount of ETH in decentralized staking pools increasing by 89.52% in a single quarter

With the expansion brought by GameFi games, the metaverse, and Web 3.0, as well as the capacity of Ethereum Layer 2 to support a large user base, communication and interoperability between Ethereum and other ecosystems are extremely necessary.

With the expansion brought by GameFi games, the metaverse, and Web 3.0, as well as the capacity of Ethereum Layer 2 to support a large user base, communication and interoperability between Ethereum and other ecosystems are extremely necessary.Author: Cabin VC

In March 2022, the Federal Reserve's interest rate hike met market expectations, leading to an improvement in the macro situation of the crypto market and stabilization of the market. By the end of March, the total market capitalization of the crypto market returned to $2 trillion, with ETH rising back above $3,500, accounting for 17.9% of the market cap.

Ethereum is currently at a critical juncture before the merge of PoW and PoS. Ethereum ranks second in market capitalization in the crypto market, with a long-term market share between 17% and 22%, making it significant for the entire crypto market. This report comprehensively reviews Ethereum's Q1 data, application layer overview, and historical development cycles, observing the ecological status, application layer development, and trends of Ethereum for reference.

1. Ethereum: Before The Merge

1. Overview of Ethereum Q1 Data

In the first quarter of 2022, Ethereum's return on investment fell by approximately -10.8%, with monthly fluctuations of -27%, +8.4%, and +12.4%. ETH stabilized and rebounded in late March, returning above $3,000. In this quarter, BTC's market share was 40%, while ETH's market share was 20.1%, remaining flat compared to the previous quarter. The ETH/BTC exchange rate fell from a three-year high set in the previous quarter, decreasing from 0.0835 to 0.072, demonstrating a certain hedging effect when BTC experienced a rapid decline.

(https://cryptorank.io/price/ethereum)

This quarter, Ethereum's ecological development proceeded steadily. According to cryptomiso, over 100 contributors submitted 115 code updates this quarter, ranking 40th in terms of active developers. Additionally, according to stateofthedapps, there are 4,011 DApps operating stably in the Ethereum ecosystem, with over 7,220 smart contracts. Approximately 46 new DApps were added this quarter, remaining flat compared to the previous quarter.

In terms of TVL market share, Ethereum accounts for 60.98% among major public chains, with a quarterly growth rate of 27.18%, far exceeding the share of other public chains. However, chains like Terra, BSC, and Avalanche have seen faster growth rates. In early March, Ethereum's network TVL hit a historical low of 55%, indicating a clear trend towards multi-chain.

This quarter, the average number of active Ethereum addresses was approximately 578,732, a slight decrease of 3.92% from the previous quarter's average of 602,388. In late March, the number of active Ethereum addresses peaked at 875,201 (within 24 hours), indicating a rebound in user activity.

2. Progress of Ethereum 2.0

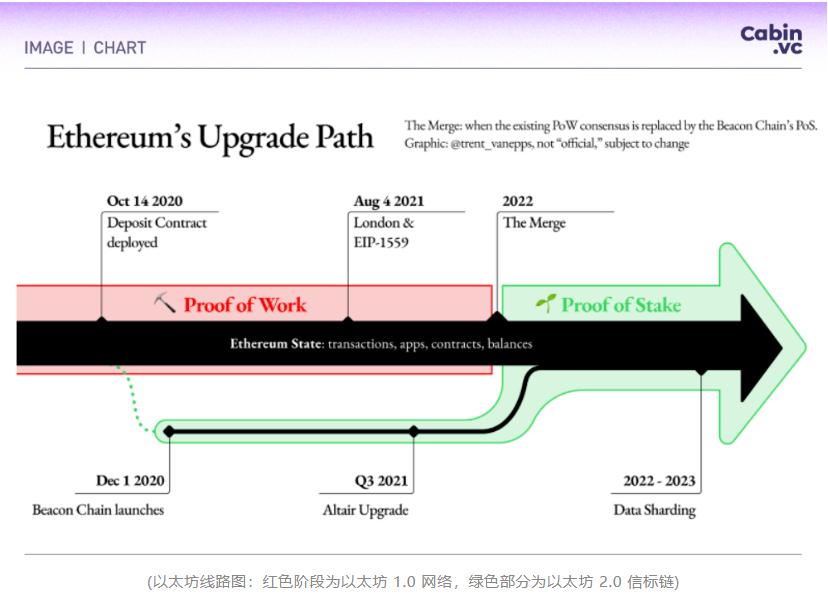

Ethereum is currently at a critical point in the progress of Ethereum 2.0. To realize its vision of a world computer, Ethereum has planned four development phases: Frontier, Homestead, Metropolis, and Serenity. The fourth phase is regarded as "Ethereum 2.0" (consensus layer), aimed at addressing scalability issues. The transition from PoW to PoS consensus mechanism is crucial in this phase.

According to Ethereum's roadmap, Ethereum 2.0 will be achieved in three phases. The first phase, the "Beacon Chain," was completed in December 2020: the Beacon Chain introduced native staking to the Ethereum blockchain, marking the entry into the Serenity phase. The second phase is "The Merge," and the third phase focuses on shard technology, the "Shard Chains."

(The Ethereum Foundation is phasing out the terms "ETH 1.0" and "ETH 2.0" in favor of "Execution Layer" and "Consensus Layer," meaning Ethereum will ultimately consist of an execution layer and a consensus layer.)

In the second half of 2021, Ethereum 1.0's "EIP-1559" upgrade and the Altair upgrade of the Ethereum 2.0 Beacon Chain prepared for the second phase, The Merge.

This quarter, market expectations for the merge of Ethereum 2.0's Beacon Chain with the Ethereum 1.0 network (The Merge) strengthened, with the market reacting in advance to the deflationary effects expected post-Merge.

The official preliminary reference time for the Merge is set for June to July, with the specific date yet to be determined. After the Merge, both mechanisms will run in parallel, ultimately transitioning to PoS. The initiation of The Merge signifies the gradual abandonment of the PoW mechanism, leading to the exit of the existing miner community from the Ethereum ecosystem and reshaping the landscape for deflationary currency, decentralized staking, and GPU mining.

Whether Ethereum 2.0 can smoothly occur in Q2 depends on the performance of The Merge on the Kiln testnet. The current progress of ETH 2.0 aligns with community expectations. On March 15, the Ethereum Merge public testnet Kiln went live, indicating a successful transition to a complete proof-of-stake (PoS) consensus mechanism. The next step for developers is to merge the existing PoW testnet, followed by the mainnet. According to official data, as of late March, there are over 106,000 validators on the Ethereum testnet that have transitioned to the PoS consensus mechanism, with 3.4 million testnet ETH.

The technical discussions among Ethereum core developers have shifted focus to the "Verge" phase after The Merge, with expectations that the implementation of The Merge will be relatively smooth.

In the Ethereum white paper, ETH's supply will increase annually by a certain percentage, and as the total supply increases, the proportion of new issuance to the total supply will decrease. Under the PoW consensus mechanism, the annual issuance rate of ETH is approximately 4.2% - 4.3%, with a daily issuance of about 12,000 - 13,000 ETH. After transitioning to the PoS mechanism, referencing the current PoS Beacon Chain's annual issuance rate of 0.6%, the daily output of ETH will be around 1,280-1,500, a decrease of 90%.

After the successful Merge, ETH's annual issuance rate will drop to 0.3% to 0.4%. In staking, stakers will no longer incur electricity costs, theoretically reducing selling pressure.

Currently, ETH is in an inflationary state, with an inflation rate of about 3%. The annual burning amount of ETH is approximately 1 million ETH, and the annual issuance of ETH post-Merge will be around 500,000. As of March, the total supply of ETH is approximately 118.5 million, of which the staking amount reaches 14.5 million, accounting for 12.2%, and the supply of ETH in contracts is 21.6 million, accounting for 18.22%. The expectation of deflation for ETH increases after the Merge. Compared to Bitcoin's current inflation rate of 1.73%, the inflation rate of ETH post-Merge will be four times lower.

Ultrasound simulated the changes in ETH burning, supply, and issuance after The Merge:

In Q3 of last year, the EIP-1559 proposal in the Ethereum London upgrade adjusted the fee mechanism, increasing the burning of the base fee of ETH, which has already reduced the circulation of ETH and objectively added a deflationary effect.

During the same period, the staking amount in the ETH 2.0 deposit contract has continued to increase steadily, with over 10,000,000 ETH staked (approximately over $27 billion), accounting for about 9% of Ethereum's current circulation. Among these, 66% of the funds were deposited by exchanges and staking service providers, with the largest deposit amounts coming from Lido (22%), Coinbase (15%), surpassing centralized exchanges like Kraken and Binance in staking share, indicating a clear trend towards institutionalization.

Under the PoS mechanism, the staking return rate of ETH in Ethereum is determined by the amount of ETH staked, and it is expected that after The Merge is initiated and stabilized, the scale of staked ETH will expand again. This portion of ETH will be locked and cannot circulate (except for staking derivatives).

Considering the technological improvements and performance enhancements after Ethereum's PoS mechanism, the demand from developers will increase, leading to increased scarcity of ETH as a consumer product. The increasing amount of ETH in staking and the ETH burned both contribute to the scarcity of ETH, and the arrival of The Merge will more intuitively showcase this through data.

3. Before The Merge: Intensified Deflationary Expectations, Staking Protocols in Focus

The deflationary expectations for ETH after The Merge are intensifying, which is an important logic behind the recovery of Ethereum's market capitalization in Q1 2022. The relevant data on ETH supply and demand in Q1 2022 is summarized as follows:

In the current crypto market, the asset attributes of ETH are more complex. The early white paper described its main value as:

- The currency attribute in the crypto market;

- Gas consumption;

- Interest-bearing asset;

- The staking introduced by Ethereum 2.0 has made ETH a "productive asset" in the ecosystem (ETH holders have the right to earn income), which has first enhanced the scarcity of ETH. Regarding The Merge, as exchanges, DeFi protocols, wallets, and ETH staking services deepen their participation, the market and community have raised expectations for staking returns post-Merge, generally believing that "20-25% of ETH's circulating supply" is a reasonable range for the scale of ETH staking. Considering that more ETH will be locked and the circulation of newly generated blocks will be limited in the short term, supply constraints will further emerge.

On the other hand, the prosperity of the DeFi ecosystem, the entry of mainstream institutions, and the explosive market for public chains all emphasize the "asset" attribute of ETH. ETH is used as a trustless collateral in DeFi transactions, providing liquidity to the market. At its peak, nearly 10 million ETH were locked in DeFi, with Q1 data showing approximately 4.907 million ETH. These collateral assets are indispensable in the DeFi ecosystem.

Institutional investors view ETH as a means of value storage. Grayscale's ETH holdings reflect institutional optimism well:

Various factors are driving the increased scarcity of ETH. While the macro situation in the crypto market stabilizes, the evident lack of follow-up from hot topics like NFTs and DeFi, The Merge, as an important step towards the upcoming consensus mechanism shift, has pushed Ethereum's deflationary expectations to a peak in the short term. The original relationships within the ETH ecosystem are being restructured, and as the miner community gradually exits, this change is giving rise to new tracks that are expected to capture market hotspots:

(1) Staking Derivatives

Staking derivatives represent staking ETH and obtaining ERC20 tokens for normal trading, providing liquidity for ETH, usually with a certain premium.

Centralized Staking

Centralized staking mainly includes ETH 2.0 staking service providers. Currently, centralized exchanges, mining pools, wallets, or custodians all provide ETH 2.0 staking services. These platforms already have a large reserve of liquid ETH and can provide this service without increasing user costs. It is expected that these platforms will integrate these services in the future, becoming an important share of new business.

Currently, trading platforms represented by Kraken and Binance charge about 15% or more in commissions for custodial services; for institutional users, the service commissions from custodial services such as Coinbase, Midas, SwissBorg, and Bitcoin Suisse AG are also mostly over 15%. In ETH 2.0 staking services, providers like Stakefish, P2P Validator, and Stakewise, which have not yet issued tokens, charge around 10% in commissions.

However, centralized staking platforms face issues of excessive centralization, such as the potential for collusion in early stages.

Decentralized Staking

In decentralized staking pools, users can deposit ETH into a specific Ethereum smart contract and receive receipts or proof tokens, earning a share of the staking rewards from the contract, with user balances adjusting over time. According to incomplete statistics, the amount of ETH in ETH 2.0 decentralized staking pools increased by 89.52% this quarter.

Lido is currently the largest decentralized staking pool in the market, allowing users to earn staking rewards without locking assets or maintaining staking infrastructure. Currently, Lido accounts for over 80% of the entire ETH 2.0 staking market share. Lido adopts a multi-chain expansion strategy, providing liquid staking for LUNA, SOL, KSM, and MATIC in addition to ETH. Lido has raised approximately $140 million in total financing, primarily led by a16z and Paradigm.

RocketPool

RocketPool is one of the earliest Ethereum staking protocols and has seen rapid growth recently. Rocket Pool's model aligns the interests of the protocol and node operators by requiring node operators to stake RPL tokens, minimizing trust assumptions through the automated process of joining the network. The protocol focuses on Ethereum, with known investors including ConsenSys Ventures.

SSV.network

SSV.network is a fully decentralized open ETH 2.0 staking network based on Secret Shared Validator (SSV). This platform provides open infrastructure for users, staking pools, and large institutions that need to run Ethereum validators. SSV has received $188,000 in grants from the Ethereum Foundation. Additionally, it has secured $10 million in funding from investors including Coinbase, Lukka, and DCG.

(2) GPU Mining

Existing miners and mining machine manufacturers may seek new GPU mining projects, continuing to use GPU graphics cards as the core of their mining machines.

For example, the recent GPU mining project Aleo:

Aleo is a recently popular GPU mining project that uses zero-knowledge cryptography to build a privacy-focused and highly scalable underlying blockchain. Aleo shifts smart contract execution off-chain to support various decentralized applications, allowing applications to be fully private while maintaining scalability. Aleo miners do not need to rerun every transaction, only verify its correctness.

Aleo raised $28 million in Series A funding, led by a16z; in Series B, it raised $200 million, led by Kora Management LP and SoftBank Vision Fund 2, with participation from Tiger Global, Sea Capital, Samsung Next, Slow Ventures, and a16z. This became the largest round of funding in the zero-knowledge proof space, with a valuation of up to $1.45 billion. In the most recent testnet activity, it had over 10,000 test nodes.

(3) ETC (Ethereum Classic) Ecosystem

ETC is a forked currency that emerged after Ethereum's hard fork at block 1,920,000, functioning similarly to Ethereum. It follows Ethereum's original chain and adheres to the PoW consensus without transitioning to PoS, having modified its token supply policy based on Bitcoin's mining reduction and cap mechanisms.

Mining machines originally used for ETH can be directly used for ETC mining. In the week from March 16 to March 23 of this quarter, ETC surged by 87.65%, with the upcoming halving and expectations of idle mining machines transitioning being the main reasons for this increase.

2. Development Status of the Ethereum Ecosystem

1. Review of Ethereum Cycles

The ETH white paper was born in 2013, making it the first blockchain smart contract platform. Its market capitalization has gone through cycles from 2013-2014, 2017-2018, 2020-2021, and from 2021 to the present. Combined with the historical development of public chains, Ethereum's ecological development process and incentive mechanisms serve as the best reference for other public chain ecosystems.

Key development nodes and driving factors in Ethereum's history:

- End of 2013: The Ethereum white paper was born, making Ethereum the first blockchain smart contract platform.

- 2014: The non-profit Ethereum Foundation was established.

- 2015: Consensys, founded by Ethereum co-founder Joseph Lubin, first entered the market.

- 2016: Ethereum hard fork. The Ethereum development team split.

- 2017: ICOs propelled Ethereum's market capitalization to over $100 billion.

- 2018: The technical focus shifted to scalability issues, with an increase in core protocol developers.

- 2019: Constantinople upgrade;

- 2020: Ethereum 2.0 mainnet deposit contract. In 2021, Ethereum reached new highs; the London upgrade (including the EIP-1559 proposal);

- Q2 2022: The Merge is expected to be delivered in the second quarter of 2022;

The rotation of Ethereum's ecological sectors and changes in ecological support:

2013 - 2014

In 2013, the crypto market reached its first peak, with a significant increase in developers and crypto startups during this cycle, with Ethereum being one of them.

2017 - 2018

At the end of 2015, Ethereum proposed the ERC20 standard, which directly led to the bull market triggered by ICO issuance in 2017. In 2017, the issuance of smart contracts expanded the boundaries of blockchain technology, bringing blockchain into mainstream view as an underlying technology. During this cycle, Ethereum's second-place market capitalization laid the foundation and drove the valuation of other smart contract platforms and infrastructure sectors; within the ETH ecosystem, the number of DApps exploded, with notable upward effects in the NFT, blockchain gaming, and forked coin sectors, establishing ETH as a benchmark target in the altcoin market.

2020 - 2021

During this cycle, the total market capitalization of cryptocurrencies peaked at $3 trillion, with Ethereum network transactions exceeding $3.6 trillion. Ethereum's market share rose from 11% at the beginning of 2021 to around 20%. The rotation of sectors within the Ethereum ecosystem during this cycle included DeFi (DEX, AMM, liquidity mining, collateral lending), NFTs, Meme, GameFi, and the Metaverse.

From 2021 to the present

In the small cycles of the crypto market, aside from the continuation of NFT and DeFi hotspots, the market's reconstruction of public chain valuation logic has driven the upward trend of public chains.

Throughout these cycles, projects emerging in the Ethereum ecosystem during each round will experience reshuffling in bear markets, with only 10%-20% of projects surviving and growing to become important blue-chip projects and commonly used infrastructure in the next cycle.

The Ethereum Foundation has played a significant guiding and supportive role in the development of these quality projects, providing prize support and incubation assistance for community projects. The foundation is also responsible for some employment work related to community infrastructure and major Ethereum software, as well as expenses for developer and user experience and market education, but it does not control the technical direction of the network.

The foundation's annual budget is around $30 million, and its launched Ecosystem Support Program (ESP) can provide additional non-financial support, supplementing the Grants (self-service) program.

The Ethereum Foundation places great importance on developer resources and is the organizer of the annual developer conference (DevCon). Through conference promotions, foundation support, hackathons, and other means, new project waves have emerged within certain time periods. The community portals targeted by the foundation include various channels such as the official website, Reddit, blogs, Twitter, YouTube, and Facebook, with the Ethereum Reddit subforum being the most comprehensive Ethereum forum and the most active place for core developers.

The Ethereum ecosystem has consistently maintained a dominant position in developer activity. On GitHub, the number of repositories referencing the term "Ethereum" far exceeds that of other blockchains. With relatively mature documentation, infrastructure, and other developer tools, the development speed on Ethereum often surpasses that of other chains.

Economic assistance is the primary means by which the Ethereum Foundation supports the ecosystem and can guide project developers to focus on specific areas. The foundation's support themes are closely related to the phased development of the Ethereum ecosystem. For example, it proposed a subsidy plan in 2018 to incentivize developers to provide scalability solutions for Ethereum.

In 2018, the Ethereum Foundation funded emerging projects in the DeFi and NFT sectors, with the experimental project Uniswap receiving $100,000 in funding that year; during the bear market of 2019, the foundation's ecological focus was primarily on ETH2.0 clients, ETH1.0 upgrades, Layer 2, and zero-knowledge proofs (privacy track); in November 2020, the Ethereum Foundation launched the "Ethereum 2.0 Staking Community Grant"; the above themes have all become hot sectors in the next rising cycle.

Later, the Ethereum Foundation eliminated the distinction between official internal teams and external contributors, with internal teams also needing to compete for resources.

Another organization, ConsenSys, has also provided significant support in aggregating resources within the Ethereum ecosystem and industry. Its business mainly includes the development of Ethereum's foundational platform and tools, consulting, training, and services, acting as an enterprise-level technology provider and incubator, becoming an important link in the collaboration between Ethereum and enterprise-level institutions.

ConsenSys also plays a significant role in the global industry standard organization, the Enterprise Ethereum Alliance (EEA), which promotes the implementation of Ethereum-related technologies in the enterprise sector. The EEA encompasses over 3,000 global developers across 45 countries and more than 300 companies, including well-known institutions like Intel, JPMorgan, Microsoft, and IC3. In terms of industry structure, banks or financial enterprises account for about 24%, blockchain enterprises account for 5%, and crypto-native projects account for 17%. All of these have become quality resources within the Ethereum ecosystem.

2. Ethereum Application Layer Ecosystem

Ethereum's technical layer adopts a layered architecture. From top to bottom, it consists of the application layer, contract layer, and protocol layer. The protocol layer includes basic components such as the EVM virtual machine, block management, KV database, consensus algorithm, and P2P network. The smart contract layer builds a rich DApp ecosystem on Ethereum.

The various smart contracts in Ethereum's contract layer can be categorized into 21 major types based on application scenarios:

DApps can be divided into multiple categories based on their functions and nature: gaming, finance, development, trading platforms, storage, wallets, governance, property, identity, media, NFTs, DeFi, social, security, energy, health, insurance, and storage.

Currently, the trustless and transparent nature of DApps has achieved the most significant implementation in the DeFi (decentralized finance) application scenario. In 2017, this sector reached a maximum market capitalization of $6.291 billion, which later retraced to $999 million. After 2020, the DeFi sector experienced several breakthroughs, with its market capitalization first exceeding $10 billion in August; by September 2021, the market capitalization of DeFi reached a historic high of $143.953 billion.

Currently, DeFi has become the most successful application scenario on Ethereum. According to incomplete statistics, the annualized revenue generated by DeFi applications is currently over $4.5 billion, with a clear revenue model for public chains, and the superior liquidity allows users and markets in the DeFi ecosystem to benefit from each other.

The NFT sector is another rapidly growing area, with the market capitalization of NFTs remaining below $300 million before 2017, but exceeding $40 billion by 2021. In Q1 2022, the daily sales volume of NFTs on Ethereum was at the billion-dollar level, with Ethereum-based NFT trading accounting for 90% of total NFT trading volume.

In several upward cycles of Ethereum, NFTs and blockchain games have been among the early explosive sectors, undergoing multiple upgrades, with Enjin and Opensea providing significant momentum for the emergence of this rich ecosystem.

New phenomena that emerge in each cycle are built upon the technological and market foundations of the previous cycle, and more than 50% of the top 20 projects will experience reshuffling. In this cycle, over 80% of blue-chip DeFi projects are based on Ethereum, and it is expected that the next cycle's hot sectors will still include blockchain games, DeFi, and social sectors.

3. Top Ten DApps in the Ecosystem

The top 10 DApps by usage in the Ethereum ecosystem are:

The top 10 DApps by user count are:

4. Overview of L2 Ecosystem

According to L2BEAT data, as of March 3, the total locked value on Ethereum Layer 2 was $7.399 billion, surpassing most public chains. Layer 2 is another important ecosystem for Ethereum. In September 2021, the daily transaction processing volume of Ethereum L2 exceeded that of Bitcoin.

Layer 2 is a scaling solution aimed at improving the operational efficiency of blockchains while reducing costs. Layer 2 has a separate execution layer and runs on L1 (Ethereum). Layer 2 significantly reduces data processing on the blockchain by running computations off-chain. The main scaling technologies currently include state channels, sidechains, Plasma, Optimistic Rollup, ZK Rollup, and Validium. The relatively mature Rollup is the mainstream scaling method.

After the DeFi explosion, many Layer 2 projects actively collaborated with DEX and DeFi projects to reduce transaction costs and improve user experience.

L2Beat data highlights the current market leadership of Rollups, which account for 70% of the total market value, with Arbitrum ranking first at $4.1 billion. The L2 application dYdX, which uses ZK-Rollup, ranks second with a market cap of $986 million. With the adoption of NFT markets like Immutable X and NFT games like Sorare, the adoption of Validium is also increasing.

Taking the Arbitrum ecosystem as an example, Arbitrum has a clear first-mover advantage, with 74 projects participating, including Uniswap V3, Aave, Curve, and MakerDAO, shortly after its early launch. The subsequent projects joining its ecosystem have been growing rapidly, including GMX, Dopex, Tracer, Premia, Umami Finance, Swapr, and Cap, all with locked amounts exceeding $20 million. Currently, Arbitrum's network transaction volume is steadily increasing.

3. Foundation Support Directions

Recently, the Ethereum Foundation's support direction for the market mainly focuses on Web 3.0, the Metaverse, and other areas. This observation is based on recent activities, events, hackathons, and funding recipients.

In Q2 last year, the Ethereum Foundation provided $7.794 million in funding to 40 ecosystem projects, mainly in market education, zero-knowledge proofs, Layer 2, and other areas; in Q3 and Q4, the Ethereum Foundation funded a total of $13.82 million, with hot topics including DAO Drops, Zero MEV, L2BEAT, EthStaker, and more.

During Q4, the Ethereum Foundation also launched a client incentive program, with eligible client teams including Besu, Erigon, Go-ethereum (geth), Lighthouse, Lodestar (50% stake), Nethermind, Nimbus, Prysm, and Teku.

In early March 2022, the Ethereum Foundation's Ecosystem Support Program announced a $750,000 academic research funding plan aimed at promoting academic research in Ethereum, blockchain, cryptography, zero-knowledge proofs, and related fields; in mid-March, the theme of the Ethereum Rio 2022 event was based on the Metaverse, digital currency, and Web 3.0.

In the Ethereum Metaverse hackathon BuildQuest that ended in March, projects included the Metaverse game Parcels, NFT monster card game Clash Of Cards, NFT card game Ollie Verse, NFT chat platform NiftyGuilds, NFT MMORPG game Shake Shock, 90s-style RPG game Shattered Realm, location-based NFT collection game GeoNFT, 3D NFT generator NF3D, idle NFT destruction and carbon-neutral application NFT bonfire, and Metaverse music space MetaverseMusic.

The upcoming Ethereum Foundation hackathon will be held on April 22, 2022, titled "ETH Amsterdam," focusing on assisting global developers and promoting quality applications and projects that advance the Web 3.0 ecosystem, with expectations for increased attention on the Web 3.0 ecosystem.

4. Development Trends and Risks

For a long time, the Ethereum system has developed within the legal frameworks of Europe and the United States, with ecosystems like DeFi, NFTs, and dollar stablecoins flourishing. Ethereum has long been responsible for providing the most secure underlying technology for the entire crypto space. After The Merge, short-term deflationary data is expected to improve, bringing more confidence to the subsequent enhancement of blockchain performance. The next development focus of the Ethereum ecosystem in the short term will be on improving the underlying security and maturity under the PoS consensus mechanism, as well as the development of shard technology in the next phase.

ETH serves as a trustless collateral asset, essential as the underlying asset in DeFi protocols. As a leading settlement layer, its monetary circulation value within the blockchain ecosystem remains solid. With the expansion brought by GameFi, the Metaverse, and Web 3.0, as well as Ethereum Layer 2's capacity to accommodate large user groups, communication and interoperability between Ethereum and other ecosystems are extremely necessary.

This is also the thinking of many other ecosystems hoping to capture the overflow from Ethereum: for example, in the L2 direction, the early accumulation of the Polygon ecosystem has greatly benefited from close cooperation with the Ethereum community, allowing leading Ethereum projects to be quickly deployed on the Polygon chain.

The L1 public chain NEAR has adopted a "Ethereum-friendly" strategy: by ensuring EVM compatibility, it has reduced the difficulty of replicating existing code; Solana and Algorand have also lowered the barriers for developers to launch development on their blockchains through partnerships with cross-chain bridges and stablecoin providers, with these institutions collaborating with Circle to bring USDC into their ecosystems.

Currently, the development activity on Ethereum's blockchain remains active, but successful cases like BSC and Solana are increasing. As the security and performance of cross-chain bridges further mature, cross-chain bridges are expected to become important infrastructure for blockchains.

Among L1 platforms, the success of the Flow public chain is highly representative. Compared to Ethereum, Flow has more quickly met certain development needs in the NFT vertical application field. In addition to Flow's application scenarios, there are still many differentiated and vertical application needs, and the application layer of the blockchain market is entering a high-growth phase.

Ethereum's transition to the PoS mechanism represents that public chains are preparing for an explosion in application layers. After DeFi finance has become the landing scenario for Ethereum, based on its vision of a "world computer," Ethereum needs to enhance its performance to accommodate more application scenarios. It is expected that in the next 3 to 5 years, more demand refinement and scenario segmentation will emerge in the application layer, and Ethereum will continue to compete with other chains in terms of DApps and developers.

Risk points to note include:

Progress from PoW to PoS does not meet expectations.

Under the PoS consensus mechanism, the merging of miners and token holders' identities, and the absence of a competitive group (the miner community) in the ecosystem, will require time to verify the impact on the ecosystem.

The trend towards multi-chain has diluted the total locked value (TVL) share on the Ethereum network.

For a long time, the centralization issues within the Ethereum ecosystem and Ethereum staking nodes have been discussed by the community.

Risks of liquidity crises due to chain reactions in DeFi lending pools. On March 12, 2020, the overall cryptocurrency market experienced a sharp decline. As the underlying asset in DeFi protocols, Ethereum faced the risk of liquidity crises during periods of rapid price fluctuations.

The personal influence of Ethereum founder Vitalik Buterin on the Ethereum ecosystem is significant. Personal statements and positions may impact the ecosystem.