Parsing Nirvana: Innovative Algorithm Stablecoin of Virtual AMM on Solana

The current actual demand for NIRV still comes from the internal nesting of Nirvance, and the real use cases are still unknown. Whether it can be extended externally remains to be further tested over time.

The current actual demand for NIRV still comes from the internal nesting of Nirvance, and the real use cases are still unknown. Whether it can be extended externally remains to be further tested over time.Author: Wu Says Real

Nirvana Finance is a dual-token algorithmic stablecoin architecture protocol built on Solana, consisting of a quasi-stable token: ANA and a stablecoin token: NIRV. With the claim of zero-risk lending through the algorithmic stability of NIRV, it has attracted user participation, while ANA gradually transitioned to regular pricing after experiencing a "reverse" auction similar to Copper LBP, followed by a community FOMO that drove its price up.

Upon first encounter, the innovative algorithmic spirit is striking, revealing shadows of LUNA/UST, MakerDAO, and Olympus, synthesizing their essence and innovating further. The relationship between ANA and NIRV is akin to Luna and UST, where the valuation of ANA increases with the growing demand for NIRV; meanwhile, ANA serves as collateral for lending NIRV, similar to depositing ETH in MakerDAO to mint and lend DAI. The liquidity of ANA is entirely controlled by the protocol, akin to Olympus, which can generate continuous trading revenue. The realization of all this hinges on innovations in the AMM mechanism, carving out a shortcut in mainstream constant asset ratio pools.

Perspective and Path of Nirvance Finance

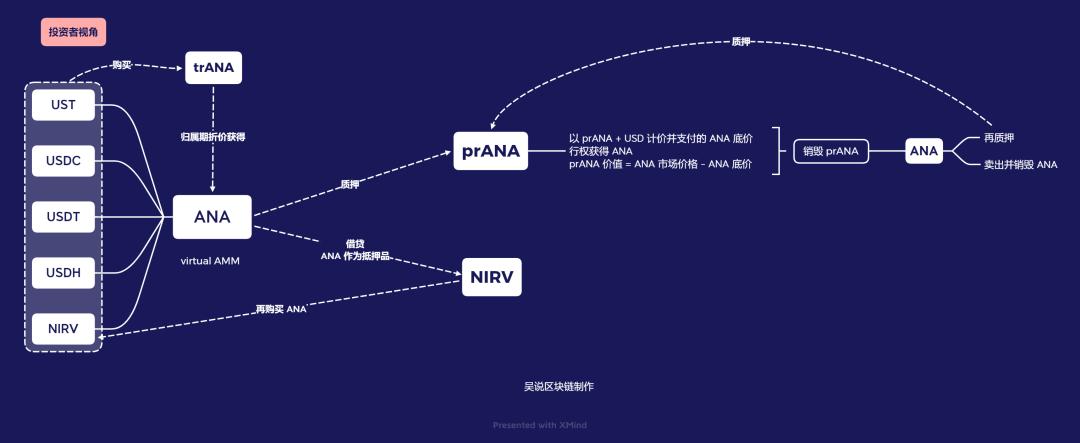

From the user's perspective, investors buy ANA using UST, NIRV, USDC, USDT, or USDH, stake ANA, and earn staking rewards paid in prANA; they use the floor price of staked ANA as collateral to mint and lend NIRV, then continue to buy ANA with NIRV in a cyclical manner. Here, prANA is akin to an option, allowing investors to exercise their right to convert prANA into ANA at any time by paying the floor price of ANA (in USD) and destroying prANA. The value of prANA, which represents the staking profit for investors, is the market price of ANA minus the floor price of ANA. Additionally, investors can purchase trANA using USD stablecoins, similar to discounted bonds, to receive ANA after the vesting period.

From the protocol's perspective, rather than saying the protocol controls the liquidity of ANA, it is more accurate to say that the protocol directly controls the minting and burning rights of ANA. New ANA is only minted and exchanged for the USD stablecoins in users' hands when investors convert their USD stablecoins into ANA, thus obtaining liquidity for stablecoins in exchange for newly minted ANA. In this exchange process, part of the liquidity obtained by the protocol from stablecoins will be used to form the floor price of ANA, and during transactions, a fee of 0.1% for buying and 0.3% for selling, paid in ANA, will be charged. The transaction fees flow directly into the treasury rather than the AMM pool. When ANA is sold, stablecoins will be withdrawn from the AMM pool, and ANA will be burned. Therefore, this AMM pool contains only stablecoin assets and no ANA.

Subsequently, investors stake ANA and receive prANA rewards, with the staked ANA exiting market circulation. When investors convert prANA back to ANA, they will pay the protocol prANA and the corresponding floor price of ANA in USD, allowing the protocol to gain stablecoin liquidity again and burn prANA. When investors cancel their ANA staking, the protocol will charge a 0.5% unstaking fee in ANA, which flows into the treasury. If investors obtain ANA at a discounted price by purchasing trANA, a 0.2% purchase fee in ANA will also be charged and flow into the treasury.

If investors use the floor price of staked ANA as collateral to mint and lend NIRV, a 3% loan fee in NIRV will be charged and flow into the treasury. The maximum exposure for investors obtaining NIRV in a single transaction, i.e., the borrowing limit, is the quantity of ANA * the floor price of ANA * 97%. Thus, the cyclical exposure that investors can obtain approaches 1 + 1/n + 1/n² + 1/n³ +… < 1/(1-1/n), where n = 1/(quantity of ANA * floor price of ANA * 97% * 1/market price of ANA). Based on the current market price of ANA at 13.71 and a floor price of 3.4, the maximum obtainable exposure is approximately no more than 1.32 times.

From different perspectives, it can be seen that Nirvance Finance's unique AMM mechanism not only provides trading but also supports the floor price of ANA, allowing it to be used as collateral to mint the corresponding NIRV. NIRV is a stablecoin backed by multiple stablecoins, algorithmically pegged to 1 USD, but as the depth of stablecoins in the AMM pool increases, NIRV will become more stable and secure.

Thus, it is evident that the special AMM mechanism in Nirvana Finance is a crucial engine in the entire process, and this unique AMM mechanism is named "virtual AMM." The next section will focus on discussing the details of the issuance, operational mechanisms, and liquidity of vAMM.

Innovative virtual AMM Mechanism of Nirvance Finance

At the launch of Nirvance, the protocol had no ANA; only when USD flowed into the AMM pool would ANA be minted. NIRV is algorithmically pegged to $1, which means the floor price of ANA must first be at $1. Therefore, during the initial phase of USD liquidity injection, the market price of ANA will inevitably be above $1. Of course, at the project's launch, liquidity was cleverly guided into the market through a "reverse" auction similar to Copper LBP, with the market price of ANA rising or falling exponentially until it reached 0 and entered a normal pricing phase. However, regardless of how the market price of ANA changes, it will always be above $1. Similarly, it is during this process that a portion of USD liquidity can be excessively accumulated, providing assurance for the subsequent rise in the floor price of ANA.

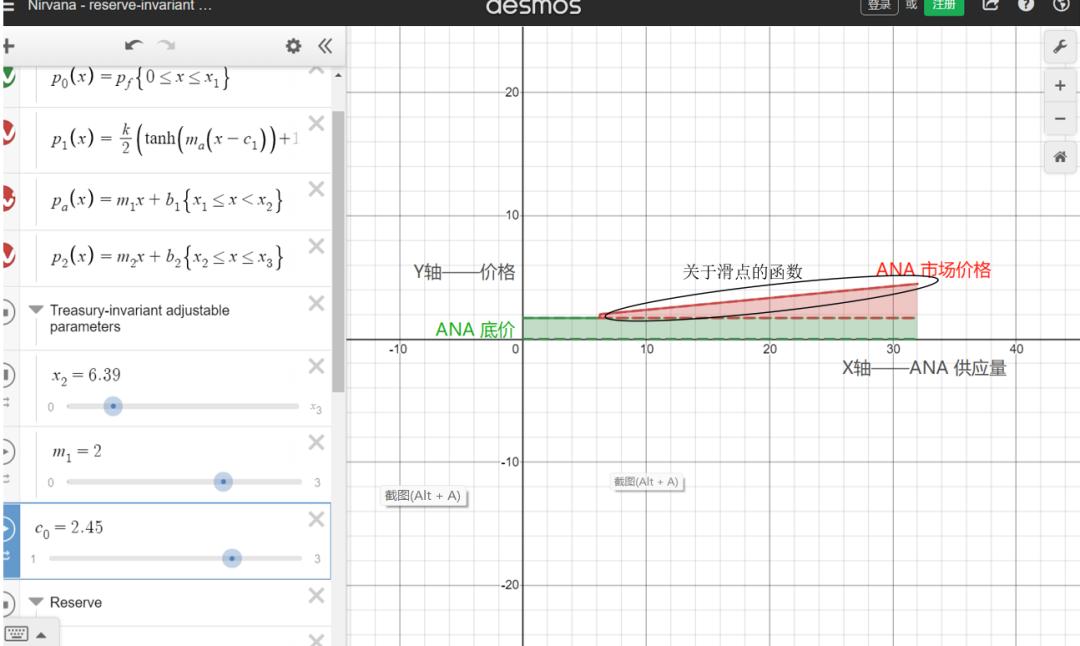

From the user's perspective observed in the previous chapter, it can be seen that the vAMM mechanism differs from mainstream constant asset ratio pool AMM mechanisms. In mainstream AMM mechanisms, there are two types of tokens in the liquidity pool, and the ratio of these two tokens is approximately maintained at 1:1 at genesis, with the price of Token A quoted by Token B. If Token A gains more market favor, investors are willing to spend more Token B to acquire Token A in the AMM pool, leading to a relative decrease in the supply of Token A in the pool, thus driving up the price of Token A. Therefore, in mainstream AMM pools, the AMM price curve is a function of the relative supply of tokens.

In contrast, the vAMM mechanism does not have any liquidity of ANA; ANA is only minted when purchased with USD. When selling ANA for USD, the AMM pool pays investors the corresponding USD stablecoin liquidity, and ANA will be immediately burned. Purchasing ANA through the AMM pool brings more liquidity to the AMM and allocates a portion of that liquidity to the floor price of ANA to ensure that the floor price continues to rise under the premise of being able to repay and allowing users to exit at any time; conversely, selling ANA returns stablecoin liquidity without affecting the floor price of ANA. It is the immediate minting and burning that ensures ANA always receives support for its floor price. With the existence of the floor price for ANA, no one can acquire any ANA at a price lower than the floor price, thus the price curve of vAMM is a function with a minimum value.

It is worth mentioning that since liquidity has existed in the protocol since its inception, the protocol owns the market itself, thus eliminating the need for any LP incentives or treasury management. The management and taxation of liquidity in the AMM pool are fundamentally allocated by the protocol's algorithm, truly achieving decentralization and permanent liquidity.

Source: https://www.desmos.com/calculator/8ke6glnrut?lang=zh-CN

The issue of slippage caused by liquidity is also an innovation of the vAMM mechanism. In mainstream AMM models, when buyers are more bullish on the underlying asset, making Token A in the liquidity pool scarcer relative to Token B, smaller transaction volumes may lead to larger fluctuations. This price-changing slippage results from the disruption of the balance between the supplies of both sides in the liquidity pool. In vAMM, Nirvana slippage is encoded in the function concerning the minimum value itself; this price curve can be viewed as the slippage of buy and sell orders for ANA, independent of actual liquidity. Simply put, from an intuitive perspective, when buying ANA, the price function will quote a higher price to execute the transaction; when selling ANA, it will transact at a price slightly lower than the current market price. The final result is that as the demand for ANA grows and the floor price continues to rise, more trading volume is required to drive up the price.

Risk Points of Nirvance Finance

To some extent, the relationship between ANA and NIRV is similar to that of Luna and UST, but UST is an important part of the entire Terra ecosystem, and the adoption rate of UST by on-chain projects will increase with the development of the Terra ecosystem. However, the actual demand for NIRV currently still comes from internal nesting within Nirvance, and real use cases remain unknown. Whether it can extend outward still needs further time to test. Additionally, when NIRV expands to other Solana projects, it still faces the ceiling of Solana, and there are significant challenges in extending to heterogeneous chains.

Moreover, for early participants in ANA, the earlier they participate in staking, the greater the dividends they enjoy, and with the community FOMO surrounding ANA, the market price of ANA has already exceeded four times its floor price.

Risk warning

Risk warning Risk warning

Risk warning