Messari: How does the Solana stablecoin protocol UXD solve the trilemma of stablecoins?

UXD has the potential to drive Solana's already thriving derivatives market into new realms by catalyzing the reduction of transaction costs and providing sufficient stable liquidity.

UXD has the potential to drive Solana's already thriving derivatives market into new realms by catalyzing the reduction of transaction costs and providing sufficient stable liquidity.Original Authors: Dustin Teander, Anirudh Tiwari

Original Title: 《UXD - Tackling the Stablecoin Trilemma》

Compiled by: Ze Yi, Chain Catcher

Stablecoins are one of the most important aspects of the crypto industry. On both CEX and DEX, all major trading pairs are priced in stablecoins, and the trading volume of stablecoins often exceeds that of BTC and ETH. As of now, stablecoins are the most borrowed assets in DeFi, with USDC borrowed on Aave being 27 times that of ETH. In Yearn, stablecoin vaults are the most popular yield vaults, and the most popular derivatives trades are almost all collateralized by stablecoins.

Stablecoins are the cornerstone of the entire DeFi world.

However, there are differences among various stablecoins, and each stablecoin's design involves trade-offs, reflected in three aspects: decentralization, stability, and efficiency. These three aspects constitute the trilemma that plagues stablecoin design, as optimizing one aspect often leads to the degradation of another.

Specifically, the implications of the stablecoin trilemma are:

- Decentralization: How much does the stablecoin depend on centralized systems?

- Stability: Can the stablecoin maintain its price peg without significant fluctuations? Especially during market volatility, when the demand for stable assets is high.

- Efficiency: How much capital is needed to back the stablecoin? The more capital required, the lower the efficiency, and vice versa.

Stablecoins can be primarily categorized into three types: fiat-backed stablecoins, over-collateralized stablecoins (Collateral Debt Position Stables, or CDPs), and algorithmic stablecoins.

Fiat-backed stablecoins are supported by corresponding fiat currencies (like the US dollar) from traditional centralized entities. For example, USDC is issued or redeemed by corresponding TradFi banks, which are responsible for maintaining the cash and cash equivalents held in custody to support the issued stablecoins.

Over-collateralized stablecoins are issued by decentralized protocols that accept collateral and issue debt in the form of stablecoins. The collateral supporting CDPs typically exceeds the amount of stablecoin debt issued to protect the protocol from the price volatility of the collateral tokens. In summary, over-collateralized stablecoins are backed by collateral deposited by individual users.

Algorithmic stablecoins have the broadest range of applications, with each algorithmic stablecoin exhibiting distinctly different properties, relying on a combination of game theory and mechanism systems to ensure the stability of the tokens.

Since fiat-backed stablecoins require a trusted centralized partner and over-collateralized stablecoins need excess assets as collateral, algorithmic stablecoins provide the best opportunity for DeFi to address the stablecoin trilemma, if a scalable, decentralized, and efficient stablecoin can be developed. Compared to last year, the decentralized market's demand for stablecoins that can solve the trilemma and maintain long-term viability has surged.

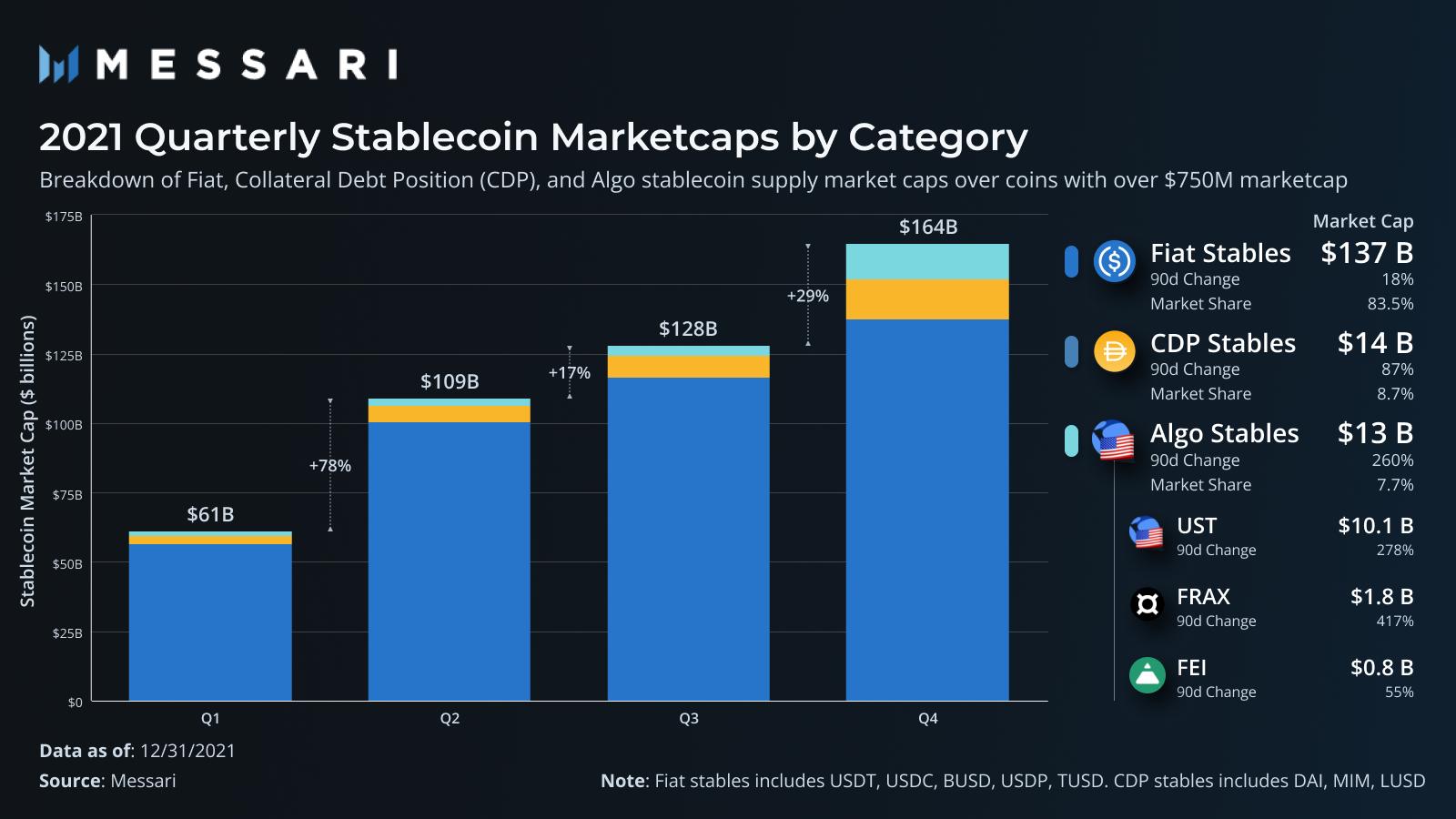

In the fourth quarter of 2021, the market capitalization of algorithmic stablecoins grew by 260%, far exceeding that of fiat-backed stablecoins and over-collateralized stablecoins, which grew by 18% and 87%, respectively. At this growth rate, algorithmic stablecoins are expected to surpass over-collateralized stablecoins in the first quarter of this year, becoming the second-largest category of stablecoins.

However, there is a significant difference in supply between fiat-backed stablecoins and algorithmic stablecoins, with the market capitalization of fiat-backed stablecoins being about 10 times that of over-collateralized and algorithmic stablecoins. This value gap presents a market opportunity for algorithmic stablecoins, and more efficient scalability is expected to emerge this year.

Currently, leading algorithmic stablecoins include UST, FRAX, and FEI. Each employs a redemption mechanism to balance supply and demand forces to maintain the stability of the stablecoin's price. For example, UST is exchanged for UST by minting or burning Luna, so when the trading price of the UST stablecoin exceeds the peg, Luna can be burned and exchanged for UST at a 1:1 dollar ratio, sold for a small profit. In this case, supply and demand forces will drive the UST price closer to the peg. This mechanism ensures that UST always maintains a price of 1 dollar, using Luna to absorb the supply and demand fluctuations that plague stablecoins.

Frax has a redemption mechanism similar to Luna's, but FRAX is algorithmically collateralized by a floating collateral factor. The collateral factor simply defines how much dollar value of collateral supports the stablecoin FRAX. When the collateral factor is 1, each FRAX is backed by one dollar. As the collateral factor decreases (designed to scale effectively), the amount of collateral required for each FRAX decreases.

Redemption will net 0.75 dollars from the protocol's collateral pool, along with 0.25 dollars worth of minted FXS, totaling 1 dollar for each redeemed FRAX. The Frax protocol also employs other mechanisms that contribute to the protocol's stability, utilizing collateral in market operations, such as liquidity reserves, investments, or loans, which Frax refers to as AMOs.

With the release of V2, FEI has also deployed a redemption mechanism as its primary stabilizing force for its algorithmic stablecoin. Unlike FRAX, FEI is over-collateralized by its protocol-controlled value (PCV), which consists of various assets, including stable assets like DAI and volatile assets like ETH and Ethereum DeFi tokens. PCV can fund 1:1 redemptions of FEI and inject liquidity into trading pools, ensuring that FEI can handle large transactions.

Due to the volatility of PCV collateral, FEI can transition from over-collateralized to under-collateralized, at which point redemptions will be funded by newly minted Tribe tokens. Redemptions ensure that the supply of FEI remains at least 1:1 relative to the collateral, while also providing a stabilizing mechanism for FEI, as market fluctuations affect the supply and demand ratio of the collateral and FEI.

Redemption is a key stabilization mechanism currently employed by algorithmic stablecoins, utilizing one or a combination of the following methods: volatile collateral (FEI), under-collateralization (FRAX), or a volatility absorption mechanism requiring supplemental tokens (UST).

Algorithmic stablecoins need this mechanism because these protocols do not have a consistent, guaranteed 1:1 collateral. Why do fiat-backed stablecoins not require complex stabilization mechanisms? Because regardless of market fluctuations, each stablecoin has 1:1 cash assets backing it.

So, why can't algorithmic stablecoins create the same guaranteed support without centralized cash backing?

UXD Stablecoin

UXD is a recently launched native stablecoin protocol on Solana. UXD aims to solve the stablecoin trilemma through a unique algorithmic design that supports stable-like assets at a 1:1 ratio, rather than relying on redemption methods to absorb volatility.

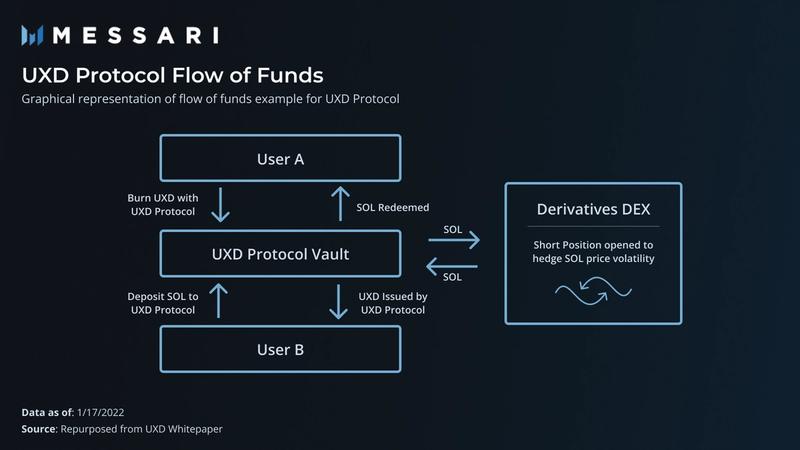

Each UXD token is backed by a perpetual derivative position that employs a delta-neutral strategy.

While it sounds complex, the design is actually quite simple. Users deposit collateral such as SOL into the protocol, and for every 1 dollar of SOL deposited, they receive 1 dollar of UXD in return. The SOL is then deposited into a perpetual trading protocol (Mango Markets) as collateral and is shorted at the same value as the deposited SOL. Therefore, if the price of SOL drops by 10%, the deposited SOL collateral will lose 10% of its dollar value; however, at the same time, the short position will gain 10% in dollar value, resulting in a net movement of 0 in dollar terms for the UXD collateral.

The net 0% movement relative to the underlying asset is the definition of delta-neutral. In practice, the UXD protocol simulates using stable assets as collateral, but with unstable assets, allowing it to support each UXD token with decentralized assets at a 1:1 ratio.

When users wish to redeem UXD for collateral, the process is reversed. Users destroy UXD on the protocol and receive SOL or their chosen collateral token at the exact dollar value in return. To return the user's SOL, the protocol closes the SOL short position on the perpetual trading platform to exchange for the exact dollar amount of the destroyed UXD, and the released SOL collateral is withdrawn back to the UXD protocol, at which point it is returned to the user.

Thus, the supply of UXD can scale faster and more efficiently than CDP stablecoins, as they require more dollar value in collateral than the issued stablecoins. With 1:1 stable asset backing, UXD should be closer to the stability of fiat-backed stablecoins, but with the added benefits of decentralization and censorship resistance. This same stability attribute is an additional advantage compared to other algorithmic stablecoins that rely on redemption and secondary tokens to absorb volatility. Mechanisms like this are very complex, and in the past, during periods of high volatility, there have been instances of liquidation.

Building the UXD token framework to address the stablecoin trilemma:

- Decentralization: UXD utilizes decentralized assets to form a stable dollar position (delta-neutral), and the UXD protocol itself is designed to be decentralized, with its overall decentralization depending on the perpetual contract protocol it utilizes.

- Stability: The collateral in UXD is traditionally unstable, but through the synthetic stability of derivatives, it recreates the reliability of fiat-backed stablecoins without relying on central suppliers. Moreover, the protocol's design relies on 1:1 support collateral for the collateral assets, rather than involving complex redemption mechanisms with non-collateralized assets (FXS and LUNA), which have only a short history of combating volatility.

- Efficiency: The ratio for UXD is 1 dollar of collateral deposited for 1 dollar of UXD issued, which is much more efficient than over-collateralized stablecoins. While the 1:1 mechanism favors stability, its efficiency is not as high as that of floating collateral factor stablecoins like FRAX, which can have less than 1 dollar of collateral for each dollar of stablecoin. A sufficiently large perpetual market is the main constraint on UXD's scalability, rather than the collateral.

To ensure the long-term viability of the protocol, a source of income is needed to adjust incentive mechanisms and fund growth. The UXD protocol does not intend to charge users fees but instead absorbs cash flow from a component of the perpetual trading platform—the funding rate.

Funding payments on perpetual trading platforms occur because traders on the exchange trade on behalf of tokens rather than the actual tokens. Since there are no actual tokens involved, the market price on perpetual exchanges may deviate from the true market price of the underlying token. To maintain price consistency, a funding payment is introduced, which varies with trading imbalances.

If traders on the perpetual exchange are overly weighted on the long side (which often happens in cryptocurrency), the funding payment will be positive, with long traders paying a certain percentage of fees to those holding short positions. This mechanism incentivizes traders to take the less popular side of the trade, effectively pushing the price of the perpetual contract trading platform back to the true market price.

Historically, funding has been positive in cryptocurrency markets, meaning that traders holding short positions, like the UXD protocol, will receive funding payments from those holding long positions. However, this is not always the case; when funding turns negative, the UXD protocol needs a mechanism to pay funding payments without affecting UXD holders. To this end, an insurance fund has been established, which was well-funded during the IDO sale of the UXP token (57 million dollars).

Overall, like many stablecoin projects, UXD aims to drive the practical application of stablecoins. The use cases primarily revolve around financial purposes rather than speculation or reward tools. For example, debt priced in stablecoins drives actual usage, as borrowers subsequently use stablecoins in exchanges and continue to hold stablecoins since their debts are denominated in tokens. This drives demand for deep currency market pools (lending) and liquidity AMM pools (exchanges). Less productive uses involve collateral and yield farming, which drive liquidity but ultimately represent unstable, short-term facades of adoption. The roadmap for UXD's release focuses on promoting long-term healthy development through more applications of stablecoins.

UXD Token Model

The UXD protocol is governed by the UXP token. UXP was sold in a public IDO that ended on November 14, raising over 57 million dollars from 3,676 investors. The funds raised in the IDO are directly used for the insurance fund, which is responsible for supporting any negative funding payments and protocol vulnerabilities that occur on the perpetual trading platform. According to the UXD documentation, the current size of the insurance fund will be able to sustain 500 million dollars of UXD for a year at an interest rate of -11.4%. Managing the insurance fund will be the responsibility of the upcoming UXP DAO.

In addition to IDO funds, UXD also raised 3 million dollars in seed funding from notable investors in the Solana ecosystem, including Multicoin, Alameda Research, Defiance Capital, CMS Holdings, Solana Foundation, Mercurial Finance, Solana founders Anatoly Yakavenko and Raj Gokal, and Saber DEX founder Dylan Macalinao.

UXP holders will be the sole governing body of the UXD DAO. Therefore, holders are responsible for managing the insurance fund and participating in governance actions. Potential governance actions may include adding new exchange integrations, adding new types of collateral, managing protocol revenue, and overall improvements to the protocol.

The revenue of the UXD protocol comes from two main sources. First, it generates positive funding payments due to short positions on the perpetual exchange. Funding in cryptocurrency has historically been positive, meaning that, in the long run, UXD can rely on this revenue source as a primary source of cash income.

The second form of revenue for the UXD protocol comes from actively managing the insurance fund. For business operations, the insurance fund is typically idle and only used during periods of negative funding (when short-term traders are overweight on long positions at perp exchanges). To improve capital efficiency, UXD will explore asset management strategies for the insurance fund. However, ultimately, the management of the insurance fund will be decided by UXP holders.

Challenges Facing the Protocol

In addition to general smart contract risks, protocols like UXD face several key challenge areas that must not only function but also effectively scale to the size required for stablecoin protocols.

Perpetual Market Size—Currently, the open interest in Solana's perpetual trading protocols is about 30 million dollars, while the open interest for all L1 token markets on Mango is 17 million dollars, and Drift Protocol is 11 million dollars. The market capitalization of stablecoins needs to approach 1 billion dollars to be considered successful and to have sufficient liquidity for widespread use.

For UXD to reach significant adoption levels, the market activity of Solana's perpetual trading protocols needs to expand significantly. At the current perpetual market size, UXD will almost certainly push the funding rates of exchanges into negative territory, as it will create an imbalance of positions toward the short side. However, this will attract more traders to trade at cheaper funding borrowing rates, so there is a self-referential game rule that can simultaneously expand both the UXD and Solana perpetual contract markets.

Negative Funding Rates—Similarly, when the funding rates of perpetual exchanges turn negative, the UXD protocol itself will need to pay. Typically, due to the much greater demand for long positions on assets, funding rates in cryptocurrency are positive, in which case the UXD protocol will earn extra money by having traders pay it funding. However, if the scale of UXD exceeds the open interest of the exchange, there is indeed a possibility that funding could be driven negative, and the protocol would need to pay.

To address this possibility, sufficient funds have been stored in the insurance fund to cover negative funding periods (historically, this situation has not lasted long). In the unlikely event that the insurance fund is depleted while making funding payments, additional UXP will be auctioned to replenish the insurance fund. Even in this unlikely scenario, the insurance fund will not be rapidly depleted through funding payments (no flash crash, just predictably scheduled payments over known time periods), so UXD holders will almost always be able to redeem their collateral.

Exit Liquidity—Related to exchange scale, there needs to be sufficient reverse liquidity for UXD to unwind its short positions. By design, every time a user deposits collateral into the protocol, UXD will establish a short position, but when UXD holders wish to exchange their collateral for stablecoins, the short position needs to be unwound, and the collateral needs to be returned. To do this, the exchange needs to have liquidity (from users or market makers) willing to sell tokens to the UXD protocol at the required scale. This risk is more prevalent during market volatility.

Financial Management—The design of UXD as a protocol is not intended to make money from UXD users but rather to manage its collateral (positive funding rates) and the insurance fund. Since the insurance fund is deployed in asset management strategies, the benefits are clearly the capital appreciation of the fund's size. However, conversely, there are introduced risks, and the risks faced by the fund need to be considered. This is not a significant issue, as it is presumed that the fund will be deployed in low-risk strategies, with the only notable risk being smart contract risk.

UXD Supply and Demand—Every stablecoin is affected by demand fluctuations, which can cause prices to deviate from the benchmark. It is important for the protocol to have the ability to absorb price fluctuations through redemption mechanisms to maintain the peg or user confidence in future redemption capabilities (as with fiat stablecoins). UXD provides both avenues, but as a growing stablecoin, it remains susceptible to risks—especially in its early stages when the concentrated amount of UXD is larger than the supply of UXD, leading to more volatility pressure.

Looking Ahead

UXD offers a unique solution for the development of stablecoins. As Solana continues to build its DeFi ecosystem, having a truly decentralized native stablecoin will greatly benefit the entire ecosystem. The market demand for this type of solution is rapidly increasing, not only in Solana but across the entire DeFi space, as projects and users seek stable assets without centralized risks, benefiting the ecosystem synergistically. UXD has the potential to catalyze a reduction in trading costs and provide sufficient stable liquidity, propelling Solana's already thriving derivatives market into new realms.

Risk warning

Risk warning Risk warning

Risk warning