An Analysis of the Operating Mechanism and Economic Model of the Decentralized Stablecoin Protocol Reserve Protocol

As more and more real-life assets are tokenized, they may be used as collateral and to support such stablecoins. Participants in the system may hold physical assets or even traditional stocks.

As more and more real-life assets are tokenized, they may be used as collateral and to support such stablecoins. Participants in the system may hold physical assets or even traditional stocks.Author: James Chung, ConsenSys

Compiled by: Biscuit, Chain Catcher

The Reserve Protocol has launched its basic stablecoin ($RSV) on Ethereum, consisting of fiat-backed dollar tokens, non-functional governance tokens ($RSR), and the Reserve application. The project also plans to launch a complete Reserve Protocol on the Ethereum mainnet this year, where users can check its progress on the official website. However, since the protocol has not yet "gone live" on the Ethereum mainnet, this article will review its expected behaviors and outcomes.

Similar to how anyone can deploy new Uniswap trading pairs, Reserve will allow anyone to mint decentralized stablecoins by aggregating a basket of ERC-20 tokens on Ethereum. The value of these stablecoins is backed by $RSR holders and earns returns from the underlying assets. Similar to how a DAO manages a treasury, each stablecoin can be governed independently through its own governance system.

The governing body can be a DAO, a multi-signature wallet, or a single Ethereum address, and can freely create methods for managing parameters, such as the time delay for unstaking RSR. If one or more collateral tokens default, the system will rebalance by utilizing staked RSR or other collateral tokens. If the total amount of staked $RSR is insufficient to cover the defaults, stablecoin holders will ultimately bear the corresponding losses. Reserve aims to facilitate the asset-backed minting of currencies in a non-fiat monetary system, with more assets participating over time.

Overview

Stablecoins have issued over $180 billion and settle trillions of dollars in transactions annually, highlighting their importance in the crypto industry. However, many current protocols rely on centralized stablecoin issuers with the authority to freeze assets. Recently, top centralized stablecoin issuer Tether froze over $1 million worth of USDT, rendering it unusable. Such actions are inconsistent with the spirit of crypto and pose significant risks to the crypto ecosystem. Additionally, regulatory uncertainty has been increasing, and history shows us that governments are not successful in deploying digital services. For these reasons, Reserve believes that community-owned decentralized stablecoins will play a crucial role in the future of global finance.

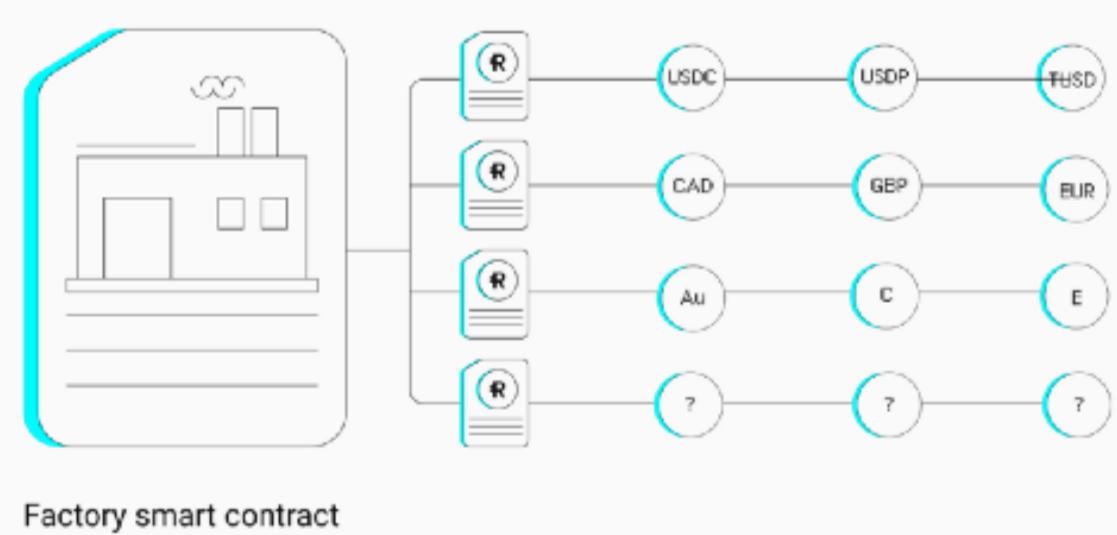

At launch, in addition to the existing $RSV stablecoin, there will be two types of stablecoins. One is a dollar-pegged token without insurance or income (e.g., USDC), while the other is a DeFi dollar token that generates income for $RSR stakers (e.g., cUSDC). These stablecoins are intended to kickstart the project and incentivize others to deposit similar stablecoins. As more real-world assets are tokenized, they may be used to collateralize and support such stablecoins. Participants in the system may hold physical assets or even traditional stocks, as shown in the diagram below:

The platform allows anyone to mint stablecoins, which will be referred to as RToken. Similar to how Uniswap operates today, the smart contracts deployed by Reserve allow anyone to mint stablecoins backed by a basket of tokenized assets. Like ETFs, these tokens have a one-to-one relationship with the underlying assets. However, due to synchronization speed limits per block, the efficiency of issuance is unclear, as minting stablecoins takes time. Although attacks can be prevented by default, if demand for RToken is high, users may have to wait in line for a long time to complete the minting exchange.

RToken can earn income in three ways:

- Lending collateral tokens: Similar to Aave, collateral tokens can be lent out through over-collateralization.

- Revenue sharing with collateral token issuers: Tokenized assets may generate interest.

- Transaction fees: Each RToken transfer incurs a fee.

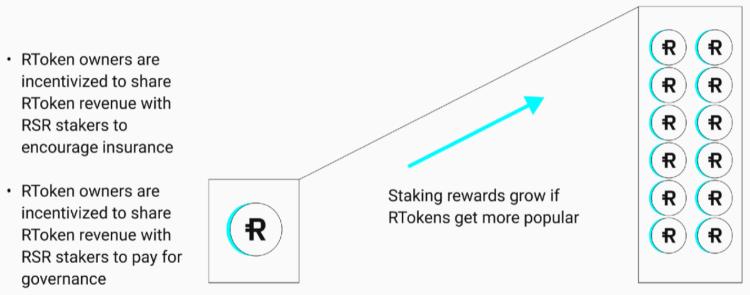

Most of this income is expected to be distributed to $RSR stakers and the RToken treasury. $RSR stakers are rewarded based on their share of the total staked $RSR, the amount of income generated by RToken, and their participation in governance. Unstaking $RSR is expected to require a waiting period of 7 to 30 days, which benefits all $RSR holders by allowing the system to cover losses in the event of defaults. This is the accrued income in RToken, which is purchased from the market and then distributed to $RSR stakers. This mechanism will create more demand for $RSR in the market and play a significant role in the demand aspect of token economics.

When considering the equity return rate of RToken, some interesting dynamic scenarios need to be taken into account. If a person stakes assets worth four times the market value of RToken and their staking reward is 2.5%, then the earnings for other $RSR stakers will be 0.625% (2.5%/4). However, if RToken is heavily promoted and the ratio of RToken to other assets flips, meaning that assets worth 1/4 of RToken's market value are staked in $RSR, then assuming the same 2.5% staking reward, the rewards for $RSR stakers will be 10%.

Another interesting dynamic scenario is the impact of price changes in $RSR. In the case where RToken earns a 10% staking reward, if the purchase price is 1/10 of the price at which the user ultimately stakes, it will yield a 100% annual return relative to the user's initial expenditure.

If a user defaults and the system does not have enough $RSR to cover the losses, RToken holders will need to bear the corresponding losses. Therefore, for those looking to mint RToken, it is crucial to ensure that the expected losses from potential defaults are less than the expected gains from staking rewards.

The governing body of RToken can be a DAO, a multi-signature wallet, or even a single Ethereum address, and can set and choose the token components that support RToken, including backup assets by default. Here are several example scenarios that governance can refer to when setting up RToken:

- Delay time for redeeming $RSR.

- Income distribution to $RSR stakers and the RToken treasury.

- Price deviation threshold required for collateral tokens by default.

- Processing time required to declare a default.

- RSR staking incentive period.

- Minimum minting quantity.

- Issuance/redeem spread (can be set to zero).

- Global minting limit per block (to prevent hacking).

- Maximum RToken supply (to reduce risks for early users).

In summary, there are four unique attributes that distinguish RToken from other stablecoins:

- Backed by a combination of ERC-20 tokens on Ethereum.

- Backup tokens that automatically replace collateral tokens in case of default.

- Autonomous governance model.

- $RSR holders can stake and earn rewards.

Mechanism Design and Token Economics

$RSR is the native token of the protocol, primarily used to provide incentives and governance for RTokens. In short, it provides insurance and fund management for Reserve Protocol's stablecoins, allowing users to stake $RSR for additional $RSR.

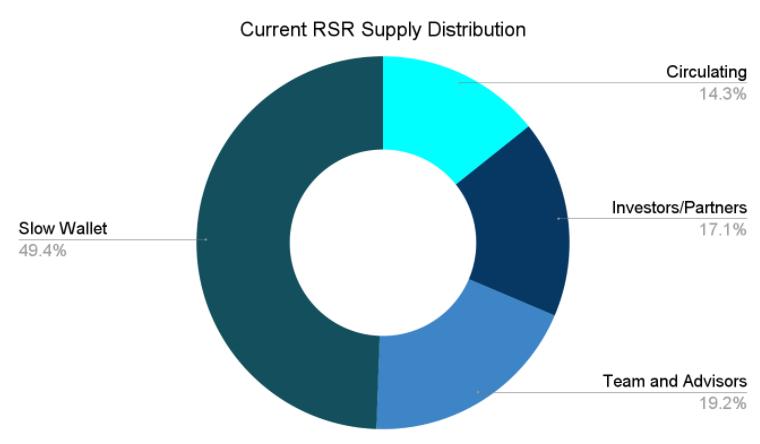

The total supply of $RSR is 100 billion, with a circulating supply of 14.3 billion. The distribution of the locked portion is as follows:

Slow wallets are funded by the RToken plan and controlled by the Reserve team. However, there will be a 4-week delay in receiving funds after initiating a withdrawal on the blockchain. If the community disagrees with the exit, this mechanism provides ample response time. The unlocking schedule for $RSR holdings of investors, partners, and team members:

● Tokens began unlocking in January 2022 but will still be held by Reserve.

● Any $RSR holder wishing to sell can submit a request.

● All orders will be sent to over-the-counter trading, where buy and sell orders will be restricted to mitigate the impact on the $RSR price.

● After six months, $RSR holders will receive all their unsold tokens.

Conclusion

Although the protocol has not yet launched on the mainnet, the Reserve application has surpassed 500,000 registered users as more merchants accept $RSV as a payment method, focusing on hyperinflationary countries like Venezuela, with plans to expand to Peru, Chile, and Mexico next.

As Reserve continues to maintain the rapid expansion of its application and its $RSV stablecoin, the team also provides savings account features, which will generate some income for existing users once the platform launches on the mainnet.

While the protocol is significant for countries experiencing hyperinflation, it does not diminish the appeal of decentralized stablecoins in countries like the United States. Concerns about the Federal Reserve's monetary policy and its contribution to the recent surge in inflation in the U.S. are growing, and as more countries weaponize fiat currencies through sanctions, the idea of de-dollarization may become a crucial factor supporting decentralized stablecoins.

Therefore, de-risking and creating a currency not controlled by a single government may create a more stable and equitable global monetary system. Finally, as mentioned earlier, one of the unique attributes of RToken is the ability to have its own governance model. Once Reserve and RTokens are run by a DAO, decentralized stablecoins will no longer be viewed as securities by the U.S. This will enable RTokens to achieve massive expansion in the decentralized stablecoin space.