Bloomberg "March Crypto Outlook": Bitcoin, Bonds, and Crude Oil

Did the dollar win the crypto war?

Did the dollar win the crypto war?Source: Bloomberg Intelligence

Author: Mike McGlone, Senior Commodity Strategist at BI

Compiled by: Odaily Planet Daily

Oil prices have once again surpassed the $100 per barrel mark after 14 years, which seems to be a bullish signal for Bitcoin in the later stages. However, for the oil market, it may replicate the pattern of rising and then falling seen in 2008, facing the fate of a crash and recession.

The last global financial crisis prompted the birth of Bitcoin and the transformation of North America from a net importer to the number one energy exporter. The current conflict in Ukraine could mark the end of the old world's dependence on oil, while the new world embraces new technologies, especially crypto assets.

At the same time, the surge in commodity prices is also fueling a global economic recession. Moreover, with the influx of cryptocurrencies, the supply of Bitcoin and Ethereum lacks elasticity and has not been widely adopted.

Bitcoin, Bonds, and Oil

As expected, Bitcoin may benefit from the confrontation between bonds and oil. The conflict in Ukraine may signify that Bitcoin is moving closer to becoming a global digital collateral. The surge in energy prices has made people aware of the benefits of embracing technology and the advantages of North America achieving net oil exports. Considering factors such as supply, demand, adoption, and human intelligence, Bitcoin is likely to regain an advantage in its competition with oil in 2022.

Bitcoin is competing with oil and bonds; despite the significant rise in oil prices, the yield on long-term U.S. Treasury bonds has not reached last year's highs, indicating that further deflation may drive up Bitcoin.

As of March, West Texas Intermediate crude oil has risen about 80% this year, while long-term bond yields remain around 2.2%. We believe this suggests that yields will decline further. The conflict in Ukraine has also triggered issues regarding the shift of safe investments, leading to a competition between bonds and Bitcoin.

The surge in energy prices is a typical sign before an economic recession, and the decline in long-term bond yields is another indicator. If the stock market continues to decline, Bitcoin will also face significant resistance; however, the trend for cryptocurrencies is expected to be stronger, with 2022's performance surpassing that of most stock indices.

Above: Bitcoin benefits from the rise in oil and bond prices.

The surge in oil prices, recession, and Bitcoin's performance. In 2022, oil may face a double loss, which presents a good opportunity for Bitcoin. About 14 years ago, oil prices first broke the $100 per barrel mark, and the resulting impact is very similar to what we see now.

Data shows that the current S&P 500 index closely resembles the decline model seen at the beginning of the 2008 financial crisis. The conflict in Ukraine, combined with rising oil prices, has dealt a heavy blow to the global economy.

If the 2008 financial crisis were to repeat itself, Bitcoin would face pressure for the first time. When the S&P 500 index drops rapidly, most risk assets are fully correlated, but cryptocurrencies are different, exhibiting better resilience than all other assets.

Bitcoin has performed very strongly in 2022. As of March 2, the S&P 500 index had fallen by 10%, and although Bitcoin's volatility over 260 days is about five times that of the index, its decline is less than half that of the latter.

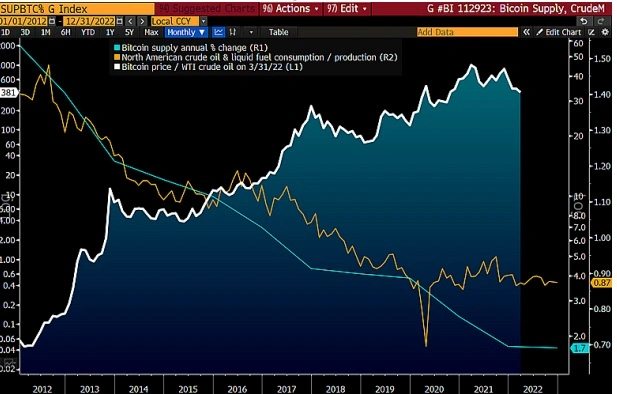

Bitcoin value vs. oil liabilities and the Ukraine conflict. A very important uncertainty regarding Bitcoin's future is its "adoption." We see that the benchmark cryptocurrency is gradually becoming a global digital collateral. Additionally, the use of oil and liquid fuels is decreasing, costs are dropping, production is increasing, and there is a strong possibility of being replaced by new technologies and new energy sources.

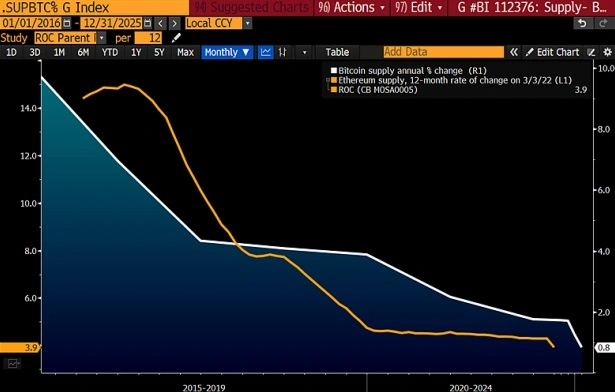

The charts show the declining trend of Bitcoin supply and the oversupply trend of North American oil and liquid fuels, with an expected surplus of 13% by 2023. The U.S. has transformed from a net importer to an increasingly large exporter—this is the number one killer of commodity prices.

Above: Oil energy prices vs. digital reserve asset prices

For most commodities, rising prices hinder demand while driving supply increases, but Bitcoin is the opposite. In the cryptocurrency market, despite increasing competition, over 17,000 cryptocurrencies have emerged, yet Bitcoin, Ethereum, and crypto dollars (stablecoins) remain resilient.

Will the Ukraine conflict be a turning point for Bitcoin?

Can Bitcoin, at $40,000, and the Nasdaq, at 14,000 points, continue to rise as "digital gold"? After a significant rise in 2021, Bitcoin is now facing "deflationary pressure," yet it still shows remarkable resilience. Bitcoin may be moving towards becoming a global digital collateral, and with the outbreak of the Ukraine conflict, Bitcoin's price has reached $40,000, while the Nasdaq has touched 14,000 points.

Compared to the Nasdaq, Bitcoin has shown different strengths. On March 2, the Nasdaq 100 index fell about 13%, and if the market continues to decline, it may affect other risk assets (especially cryptocurrencies). However, what many did not expect is that Bitcoin only fell by 5%.

Historically, stock market performance usually does not surpass that of cryptocurrencies. Bloomberg Intelligence analyzes that Bitcoin may stabilize in the $40,000 range, while the Nasdaq 100 index may decline further.

Above: Bitcoin quickly rebounds after entering the $30,000 range, but what about the stock market?

If the securities market recovers, it will help Bitcoin rebound more quickly. Importantly, Bitcoin has "held the line" at key support levels, while the stock market continues to sink.

Bitcoin's relative volatility is decreasing, performing better than traditional securities markets. In 2022, the correlation between Bitcoin and traditional securities markets is actually not high, and its performance is better than that of traditional securities markets. Bitcoin has experienced brief periods of underperformance compared to the securities market, but it is noteworthy that Bitcoin's volatility is beginning to decline.

Bloomberg Intelligence has identified two key trends for Bitcoin: one is its performance surpassing that of the Nasdaq 100 index, and the other is the decrease in relative volatility. Data shows that Bitcoin's relative volatility is currently about three times that of the Nasdaq 100 index's 260-day volatility, whereas in December 2017, when Bitcoin futures were launched, this figure was nine times.

Above: Performance trends of Bitcoin and the U.S. securities market

As Bitcoin gradually becomes mainstream, some large asset management companies are beginning to consider allocating part of their funds to Bitcoin. Bloomberg Intelligence expects that in 2022, this trend may face challenges; if the traditional securities market enters an elusive bear market, Bitcoin seems poised to gain an advantage.

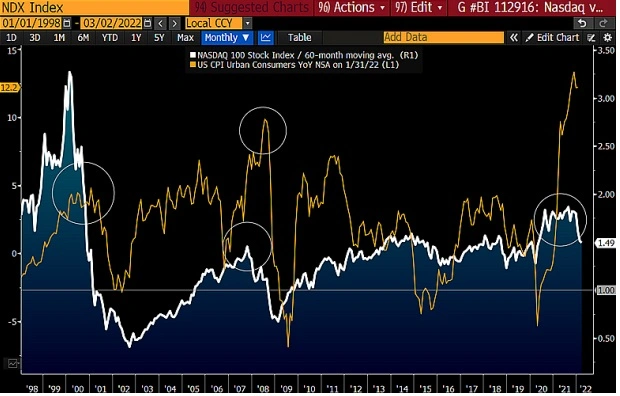

All assets will be affected by inflation. In 2022, the value of most assets will shrink, as U.S. inflation has reached its highest level in nearly 40 years. However, in this scenario, it may drive Bitcoin prices to achieve new milestones.

According to Bloomberg Intelligence data, the U.S. Producer Price Index has surpassed levels seen in 2008, and the Nasdaq 100 index's performance is similar to that of the 60-month moving average, increasing the risk of mean reversion. If risk assets do not decline and alleviate some price pressures, the Federal Reserve may have no choice but to raise interest rates more aggressively.

Above: The U.S. inflation issue may not be resolved in the short term.

Since the market recovered from the financial crisis in 2009, the Nasdaq 100 index has never traded below the 5-year average line, but now the market seems to be on the brink of collapse.

The Dollar Wins the Crypto War

The Ukraine conflict paves the way for the popularization of cryptocurrencies, especially further solidifying Ethereum's market position. During the Ukraine conflict, the values of Bitcoin and Ethereum, as leading digital currencies, as well as the value of crypto dollars (stablecoins), will be further enhanced.

As the first and second largest digital currencies by market capitalization, although Bitcoin and Ethereum seem to perform better than traditional securities markets, they also show different strengths. However, with energy prices continuously surging, Bitcoin and Ethereum may face greater recession risks, and ultimately, the dollar's dominance may be further enhanced through cryptocurrencies amid the Ukraine conflict.

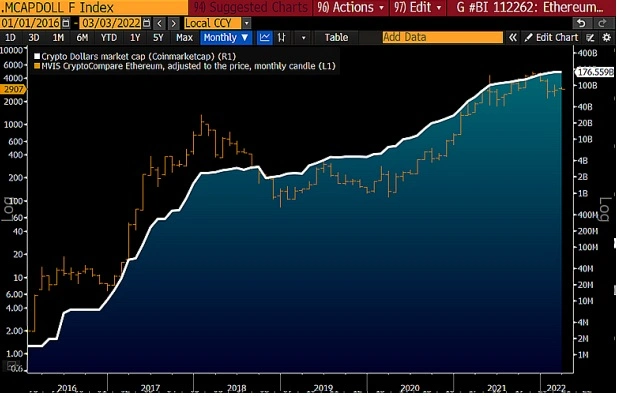

Will crypto dollars (stablecoins) and Ethereum usher in a new bull market? During the Ukraine conflict, the dollar is proving its lasting value; moreover, the dollar is winning in the cryptocurrency space. Many stablecoins have emerged on the Ethereum blockchain, and these dollar-based stablecoins further solidify Ethereum's price, while more and more other cryptocurrencies are traded in dollars.

On March 2, the market capitalization of the top six cryptocurrencies on Coinmarketcap reached $176 billion, growing about five times since early 2021. Bloomberg Intelligence believes it is almost impossible to stop the market capitalization of leading cryptocurrencies from reaching trillions of dollars.

Above: Focus on the trends of Ethereum and crypto dollars (stablecoins)

From the above chart, we can see a close relationship between Ethereum's price and the overall performance of the cryptocurrency market. If the Ukraine conflict continues to develop, it may further highlight the value of decentralized, fixed-supply digital assets. If the Ukraine conflict is resolved quickly, most risk assets should also gain upward value, and Ethereum can continue to rise.

Compared to the Nasdaq, Ethereum still shows an advantage. In the current context of the Ukraine conflict, Ethereum's superior performance relative to the Nasdaq 100 index may be further expanded.

Before the Ukraine conflict, as the cornerstone of decentralized finance (DeFi) and NFTs, Ethereum's rise was mainly due to two reasons: one is the relatively stable market performance, and the other is the decreasing risk compared to stock indices. Ethereum's 260-day volatility peaked in 2018, when it was about 11 times that of the Nasdaq 100 index's volatility.

However, since then, this risk measure for Ethereum has been declining, and currently, Ethereum's 260-day volatility is less than three times that of the Nasdaq 100 index's volatility. Of course, the increase in the Nasdaq 100 index's volatility is mainly due to geopolitical conflicts increasing the risk of economic recession and stock market fluctuations.

Above: Compared to the Nasdaq, Ethereum's volatility is actually decreasing

In fact, we find that the market performance so far in 2022 is very similar to that in the first quarter of 2008, when oil prices first broke the $100 per barrel mark, but then entered a period of financial crisis and a sharp reversal of risk assets.

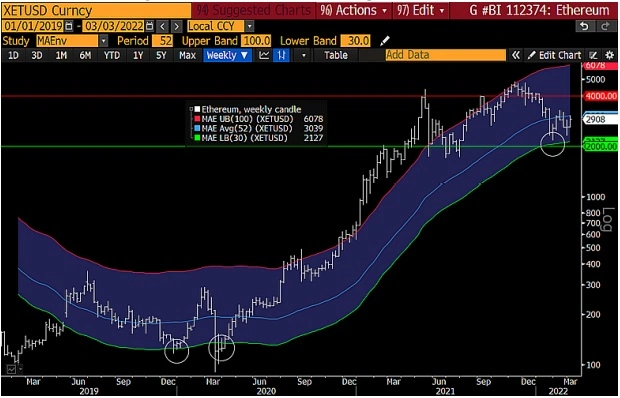

Ethereum's main risk? The tide recedes. Ethereum's demand is starting to rise, while Bitcoin's dynamic demand is declining, so it can be inferred that there will be an upward price trend. Generally speaking, the bullish fundamentals do not seem to have major issues, but it is important to note that we may still be in a mid-cycle adjustment period of a sustained bull market, meaning the market may still experience declines. If the stock market continues to fall, Ethereum may still return to lower levels.

Above: If the stock market declines, Ethereum can still return to the $2,000 range

If the stock market drops rapidly, Ethereum may even retrace to around $1,700, similar to the summer of 2021. However, if the traditional securities market performs well, Ethereum could reach the $4,800 range by November 2022.

Declining supply vs. rising adoption rate. Bitcoin and Ethereum are still in the early adoption stage, and an increase in demand coupled with a decrease in supply will have a certain impact on price trends. Unless there is a significant reversal in the market, it is difficult to resist the spread of emerging technologies, and it will not stop prices from rising.

By 2024, only about 900 Bitcoins should be mined daily, and then the daily mining volume will be halved. According to Bloomberg Intelligence's analysis, it is expected that by 2025, Bitcoin production will decline to 1% of total output.

Above: The supply of Bitcoin and Ethereum is on a downward trend

Ethereum's supply is also on a downward trend due to the implementation of EIP-1559 in 2021, which means Ethereum is burning ETH daily. In fact, Ethereum has become the foundation for revolutionary technologies such as NFTs and DeFi, while Bitcoin is becoming the "benchmark digital currency" for global digital collateral.

Talent and Stablecoins Support DeFi

DeFi growth is supported by stablecoins and developers, with this section provided by Bloomberg Intelligence special analyst Jamie Douglas Coutts.

In the DeFi space, "Intellectual Capital" (similar to "Smart Money") can operate without being affected by price fluctuations, and they will continue to solve complex problems that traditional finance has not addressed. As a volatility buffer and yield tool, stablecoins are attracting more and more users who are just entering the cryptocurrency and digital asset markets.

A bear market is unlikely to stop "Intellectual Capital" from entering. Although the prices of many leading DeFi protocol tokens have declined, the momentum of "Intellectual Capital" flowing into the DeFi market is unlikely to stop. In 2021, the number of developers working in DeFi increased by 76%, equivalent to an increase of 500 new developers per month.

Although the continuation of the bear market may slow this growth trend, the trend of increasing the number of developers is unlikely to reverse. During the last sustained bear market in 2018-19, the number of developers working in DeFi did not decrease. However, unlike the previous bear market cycle, the risks in the DeFi market have improved, and algorithmic stablecoins and on-chain derivatives are now essentially in production, having locked in billions of dollars.

Above: The growth of DeFi development and price trends are basically aligned

Crypto dollars (stablecoins) are playing the role of "DeFi gold." Over time, many who previously did not believe in DeFi have found that more and more fiat currencies are being "ruthlessly" exchanged for stablecoins.

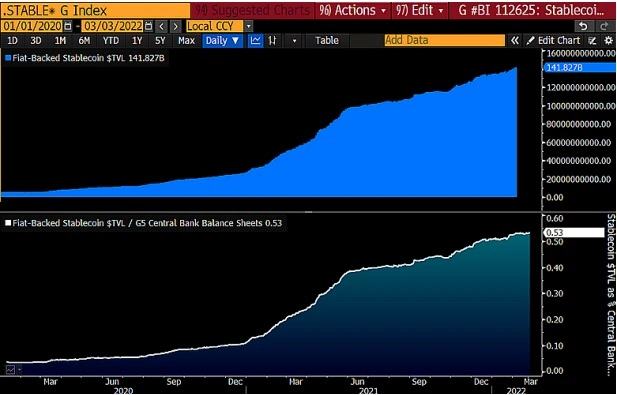

Data shows that the total amount of fiat-backed stablecoins in circulation has reached $141 billion, quadrupling since 2021. The main driver of this growth is the desire for higher yield returns in DeFi and seeking risk hedges during the bear market.

Above: The proportion of fiat-backed stablecoins in central bank balance sheets

The quantitative easing policy led by the Federal Reserve has reached unprecedented levels, which has made the role of stablecoins in the global liquidity system increasingly important.

Currently, the scale of fiat-backed stablecoins accounts for 0.53% of central bank balance sheets. If the stablecoin market grows in 2022 as it did in 2021, it is expected that by 2023, the scale of fiat-backed stablecoins will account for 2.3% of central bank balance sheets.

Stablecoin alternatives are reducing regulatory risks. Currently, decentralized stablecoins are still in their infancy, but the rise of these stablecoin alternatives can reduce regulatory risks. Issuers of fiat-backed stablecoins need to be regulated and should gradually be integrated into the banking regulatory framework, but doing so may affect the permissionless and open nature of DeFi.

Above: Performance of mainstream stablecoins in the market

Algorithmic stablecoins, such as UST issued by the Terra protocol, experienced rapid growth in 2021, with a market capitalization soaring to $10.7 billion, an increase of 5,323%; while the stablecoin DAI, based on crypto collateral, saw an increase of 791%, with these stablecoins accounting for 17% of the total stablecoin market. Among all fiat-backed stablecoins, dollar stablecoins are the fastest-growing, although Tether's market share has begun to decline.

Risks and Advantages of Crypto Tax Uncertainty

Many countries around the world may begin taxing cryptocurrencies, with mixed results for multinational companies, as provided by Bloomberg Intelligence special analyst Andrew Silverman.

For multinational companies like Tesla and Wynn Resorts, differing tax policies on cryptocurrencies across countries may pose financial risks. For example, Wynn Resorts may use the digital yuan, but the U.S. does not seem to recognize this digital form of central bank currency. Additionally, under the new global tax compliance policies, Tesla may face double taxation.

The digital yuan may pose risks for U.S. companies. Companies like Wynn Resorts, Las Vegas Sands, Qualcomm, and Texas Instruments have substantial operations in the Chinese market, and they may face tax issues.

From the U.S. perspective, Chinese customers using digital yuan instead of traditional yuan for transactions do not fall under the "cash payment" category. Moreover, the digital yuan allows for late fees after the triggering date, which may lead to issues such as currency depreciation, meaning businesses may need to track every digital yuan they hold to ensure their assets do not disappear.

Since the U.S. does not view the digital yuan as a currency, normal foreign exchange tax rules may not apply, and U.S. companies may have to account for it separately. Thus, the U.S. may treat the digital yuan as property, similar to Bitcoin.

Multinational companies may face more compliance and double taxation issues. Companies like Tesla, Square, and Coinbase hold large amounts of cryptocurrency on their balance sheets, and they may face tax compliance regulations in different countries, leading to double taxation. In fact, G20 countries find it difficult to reach a consensus on cryptocurrency taxation; however, a potential solution is to include cryptocurrencies in universal reporting standards. If regulators can obtain information about companies owning cryptocurrencies, they will tax them.

On the other hand, even if cryptocurrencies are not taxed, companies typically still need to fulfill tax reporting obligations, even in some countries/regions that do not tax cryptocurrencies; failure to report may lead to penalties.

Certain countries/regions may allow crypto tax avoidance. As cryptocurrencies are an emerging phenomenon, many countries need to understand them in depth, which means that certain tax rules may not apply to cryptocurrencies for a period of time, especially in some countries/regions that have not discussed taxing income categories, which may become a safe haven for crypto tax avoidance.

However, most countries have anti-avoidance rules, but whether they include cryptocurrencies is unknown. If cryptocurrencies are to be included, it may require renegotiation to prevent companies from avoiding taxes through cryptocurrencies.

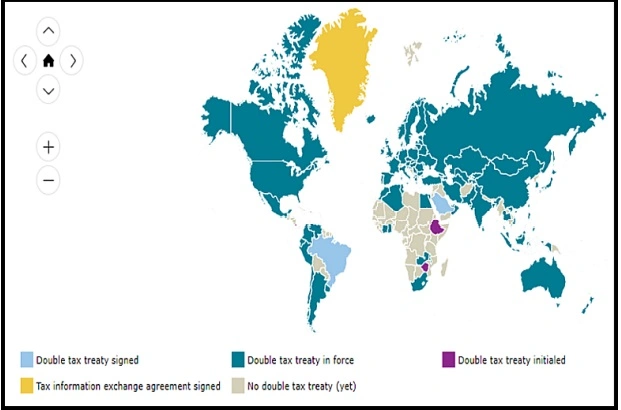

Above: Switzerland's tax treaty network (similar situations in the Netherlands and Luxembourg)