Reproduce the Curve war and write a new narrative for DeFi 3.0

If we want to promote the revival of DeFi, we need to turn back and focus on serving those who can truly help us achieve our goals, namely the community.

If we want to promote the revival of DeFi, we need to turn back and focus on serving those who can truly help us achieve our goals, namely the community.Author: knower

Compiled by: DeFi Path

Introduction

Economics tends to lean towards the view that market participants are acting rationally at almost all times. While economic models may sometimes reflect slight deviations from the best interests of actors, they do not account for the frequency of these irrational behaviors. Humans are so complex, engaged in infinitely different lives, that any model is almost impossible to show these behaviors in a rational or effective way—this is precisely the problem with economics. In this first paragraph, I want to clarify that I do not have extensive research in the field of economics, but I can say that I have read quite a few books, and if I receive some angry DMs, I can easily argue what I said—let's continue.

I will not attempt to explain examples of irrational market behavior, as we are all very familiar with the latest developments in retail investor frenzy. Whether this can be attributed to the Dogecoin/Elon Musk effect or the rise of Robinhood is irrelevant—more people than ever are trying their luck with personal investments, leading to collective net worth losses. Rather than delving into a series of endless posts on WallStreetBets about -75% accounts, I would prefer to explore the biases that economists unknowingly adopt, which have led to the great birth of the Ponzi economy.

We are all familiar with the concept of a decision tree. Each of us faces countless choices in everything we do in a day. Choosing one over another can have impacts that extend to the scale of an entire life. No one is perfect. We constantly make mistakes and hope our lives reflect what might be in our minds. The desire to achieve something greater than oneself is human nature. Whether it is the ambition to rule a country or to realize an idealized fantasy in your mind, this drive is innate. You might be an accountant from Ann Arbor or a sixth grader from Japan, but your life is unique, dreaming of the different scenarios that could unfold on any given day.

While the environment in front of you may require you to have a home, pay bills, and buy necessities for your family, these are decisions made out of necessity—they do not require calculation, as it can be assumed that the vast majority of market participants would prioritize these needs without hesitation. Unless there are unforeseen circumstances, such as job loss or natural disasters, it can be assumed that this situation will remain normal.

Clearly, there are economic models to determine the probabilities of these events and measure any irrational impacts, but most economists focus on determining the outcomes of future events and inferring current models to fit market conditions years down the line. If that is not obvious enough, (to put it another way) I am not complaining about the lack of thought regarding black swan scenarios. None of us are as smart as Nassim Taleb (haha), so when someone like him is so well-versed in the impossible, why should we care about predictions? To be clear, I am actually complaining about the lack of creativity in economics.

I think I should say that my anger towards economists is less than my anger towards economics as a whole. The fact is, these people are misled, performing these mundane calculations to divert attention from the following fact: it is almost impossible to generalize the irrational behaviors and desires of a market aimed at satisfying and fulfilling the needs of over 7 billion people. No matter how you spin it, a small group of Ivy League graduates cannot deconstruct the massive hive we call the global population, no matter how many times they break things down into supply and demand assumptions.

Since economic models are crucial for any country participating in international affairs, these models may be hastily pieced together without considering "what if" or "how about this," which would actually help with anything significant in the global economy. If it satisfies a country's leader, then the job is done, and you can move on to the next issue. Since economists can just do what they are asked to do, why would they seek the impossible?

Like others, these people are paid to do what they are supposed to do, and doing the impossible is a waste of time that satisfies no one. The Ponzi economy has risen from the ashes of economics, providing a new alternative to a dull social science that, for some reason, still exists today. Economics is boring and lacks everything that makes the Ponzi economy interesting. I am not saying that fields like economics need all the features of rebase tokens or Safemoon clones, but a little something like that wouldn’t hurt. We have moved past a collective respect for government, as it has become increasingly clear that the emperor has no clothes, and you might as well throw your annual Roth IRA contributions into Tetranode's storage locker. In recent years, the trust we once had in authority has waned, and anyone should see this very clearly, which is also reflected economically, giving us gems like TSLA, GME, and DOGE. The Ponzi economy has encountered TradFi, although it plays a slightly different Ponzi game than what we engage in within the crypto space.

In the realm of the Ponzi economy, fair competition knows no bounds. Crypto has indeed played its part in this game, but it is by no means the driving force of this school of thought. The Ponzi economy encompasses everything from 15-digit APY rebase OHM forks to metaverse catgirls. We are currently in a chaotic growth phase in the crypto space, as we often find ourselves categorized as a sandbox world filled with million-dollar JPEGs and dog coins, which is a disdain for anyone who has put a significant net worth into this magical internet currency. Many are annoyed by these jabs at cryptocurrency, as they are often exaggerated and frequently develop into personal attacks from people who have rarely looked at the space. Well, our critics are right. Look at us.

If everyone on CT who directly or indirectly uses fans as exit liquidity gave me a bag of junk coins, I would have to hire 10 employees to help me get rid of them. That’s just the way it is; the crypto market is still PvP, and you better realize that sooner rather than later. Are we going to gather together to lament and try to solve the problems we have caused? Of course not. This week, we will present a metaverse strip club project with veTokenomics and a unique revenue-sharing model to 50 venture capitalists, and no one will feel ashamed. It’s just business.

The Ponzi economy has brought substantial returns, and money in our own pockets is always better than in the hands of dirty capitalists. So what are we going to do? We will disrupt decentralized finance and implement some changes we plan to bring to the world. I will show you the theory of DeFi 3.0.

Who Pressed the Red Button?

It is clear that recently there have been more sellers than buyers. Everything is in panic, and the numbers are dropping. Unfortunately, this does not seem to be concluding anytime soon. Maybe we are in a bear market, maybe we are not. I am still excited.

When tokens are not rising, it is easy to feel that nothing is happening in the DeFi space, but just a glance outside the echo chamber reveals how strong this community actually is. There are so many projects currently being built, doing completely unique things, and if I wanted to describe all of them, I would go crazy. Instead, I will share this completely safe link that you should click to navigate to @fomosaurus's page. And this is just the beginning; there are so many builders putting in the work, so I feel that being bearish in the long term is absolutely low IQ. To define what DeFi 3.0 might be, perhaps we should trace back to our humble beginnings and how we got to this point.

DeFi 1.0 was characterized by the creation of AMMs and a summer of food farming. Uniswap is (and still is) the king, Sushiswap tried to overthrow the king but was knocked down, and yearn finance rose, with DeFi TVL skyrocketing from nothing. Liquidity mining and farming became the jargon, and protocols struggled to remain relevant in an increasingly saturated field. Even today, there are a few protocols that have existed since this period.

From a historical perspective, DeFi 1.0 can be seen as the wild west mixed with high APYs and 2-pools. What I mean is that no matter how bad DeFi was, there were some positives. These included a clean user interface (not necessarily a smooth user experience), the ability to swap token A for token B, yearn finance, and Curve wars (because they are fun). All of these were good performances in the space, and if we hope to eventually overthrow the TradFi beast, we need more of this.

The transition to DeFi 2.0 took longer than you might expect, as this narrative did not really kick off until around October or November 2021. We may all be too familiar with Curve wars and OHM forks, but let’s study it again to figure out why this narrative had such a significant impact on CT. The veTokenomics model was able to persuade countless speculators because tokens were essentially needed by all protocols, so they would rise. Additionally, the outrageous APYs of OHM spawned a million forks, but almost all of them failed. Ironically, the only OHM fork that actually did well was Wonderland, but once one of their founders was found to be a criminal and people realized that DAOs playing SPACs were not as cool as it sounded, everything collapsed. Sigh, even real SPACs do not do well, if you want to know, just look at some examples from Chamath. Protocol-owned liquidity (PoL) is a significant part of DeFi 2.0 because, even though not many protocols can use this money to drive value back to token holders, Olympus was able to secure over $500 million in massive funding.

Although the narrative of DeFi 2.0 quickly faded, I believe it was successful. Not because I sold CRV at the top, but because it was a perfect way to test CT's grasp of narratives.

After I started posting about Curve Wars on Substack, hundreds of writers much smarter than me began reporting on it, leading to a brief period of euphoria. The time I spent on all this is fuzzy, and I can hardly believe it is already 2022. I will not attempt to look back and see how long this narrative lasted, but it was popular, and it became popular quickly.

My entire TL and replies were filled with $20 CRV price targets and $5000 OHM price targets, even though veTokens do not offer much to the average person. Yes, protocols will pay them a lot, but why wouldn’t they? When they can direct the Curve Gauge to the pools of their choice, offering you a 40% annual interest rate on some veCRVglOHMcvxDPX token is an amazing deal. Although DeFi 2.0 eventually crashed along with the rest of the market, it was a very enjoyable time that got me into cryptocurrency—and I have not looked back since.

While some have tried to continue the narrative of DeFi 2.0 (remember solidly?), they have also failed, mainly because the tokens of DeFi 2.0 have experienced significant dilution, and no one cares about them anymore. This brief phase could be called DeFi 2.25 because the narrative was merely hanging by a thread of on-chain derivative protocols and ve(3,3) tokens that no one really asked for. For my sanity, we should leap from DeFi 2.5 or 2.75 directly into 3.0, as that would make sense.

If DeFi as a whole did one good thing, it taught the entire community of degens how to continuously improve the process of siphoning funds from investors. We have been able to create increasingly complex protocols that can almost immediately attract everyone's attention. Whether it is a new DEX on Fantom operating as a fork of Trader Joe or a 23-digit APY rebase token on Harmony, we can do it. And let’s not act like DeFi protocols have not gotten better at marketing, as there are many protocols that are very interesting and offer visually appealing websites. If we want to drive a revival of DeFi, we need to look back and focus on serving those who can truly help us achieve our goals, namely the community.

No, this is not the kind of NFT project that asks you to provide your social security number to get whitelisted, but a community that genuinely supports DeFi and tries to innovate on the traditional concepts that TradFi gives us, allowing everyone to participate.

Fat Protocol Base Paper and Main Ideas

Most of this section will focus on the base paper written by my good friend @0xSami_ and the ideas he expands upon in this brilliant piece. For beginners, I will briefly introduce the Fat Protocol paper that was first discussed by Joel Monegro in 2016 (or so it is said).

The Fat Protocol paper describes the relationship between a system and its applications. Monegro uses the internet and its largest applications as an example, pointing out that Web2 is characterized by the situation where Fat applications > Fat protocols, with giants like Google and Facebook accumulating trillions in market value while the infrastructure of the internet merely exists. Applying this to the crypto space, Monegro proposed the Fat Protocol theory—blockchains like Ethereum and Bitcoin (I know it’s an old post) can accumulate value like never before, establishing an infrastructure for small applications that will benefit from the success of the protocol.

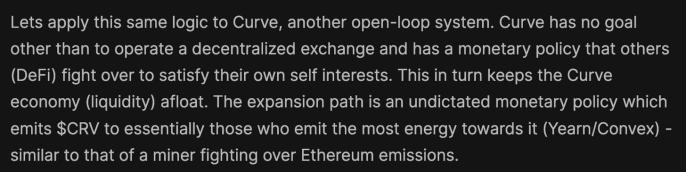

In Sami's words, protocols focus too much on value creation rather than value capture. One example of this is Curve Finance and their ability to capture value and bring it back to the protocol and token holders, while protocols try to accumulate TVL without means of expansion. Curve can serve as a springboard (or base) for protocols like Convex, providing opportunities to accumulate value while still bringing it back to Curve. Sami describes this as the difference between open-loop systems and closed-loop systems. It could be said that what we are looking forward to is a loop without an opening.

I find all of this very interesting because I had never thought about the philosophy behind Curve and how they became so powerful. Of course, the incentives are good, but anyone can incentivize over a certain period and maintain relative stability. Curve has maintained their moat and kept pace with Uniswap, becoming the go-to place for stablecoin swaps. Deep liquidity and a boatload of incentives are the reasons for their success, but Curve has now surpassed another application status—they have become a base.

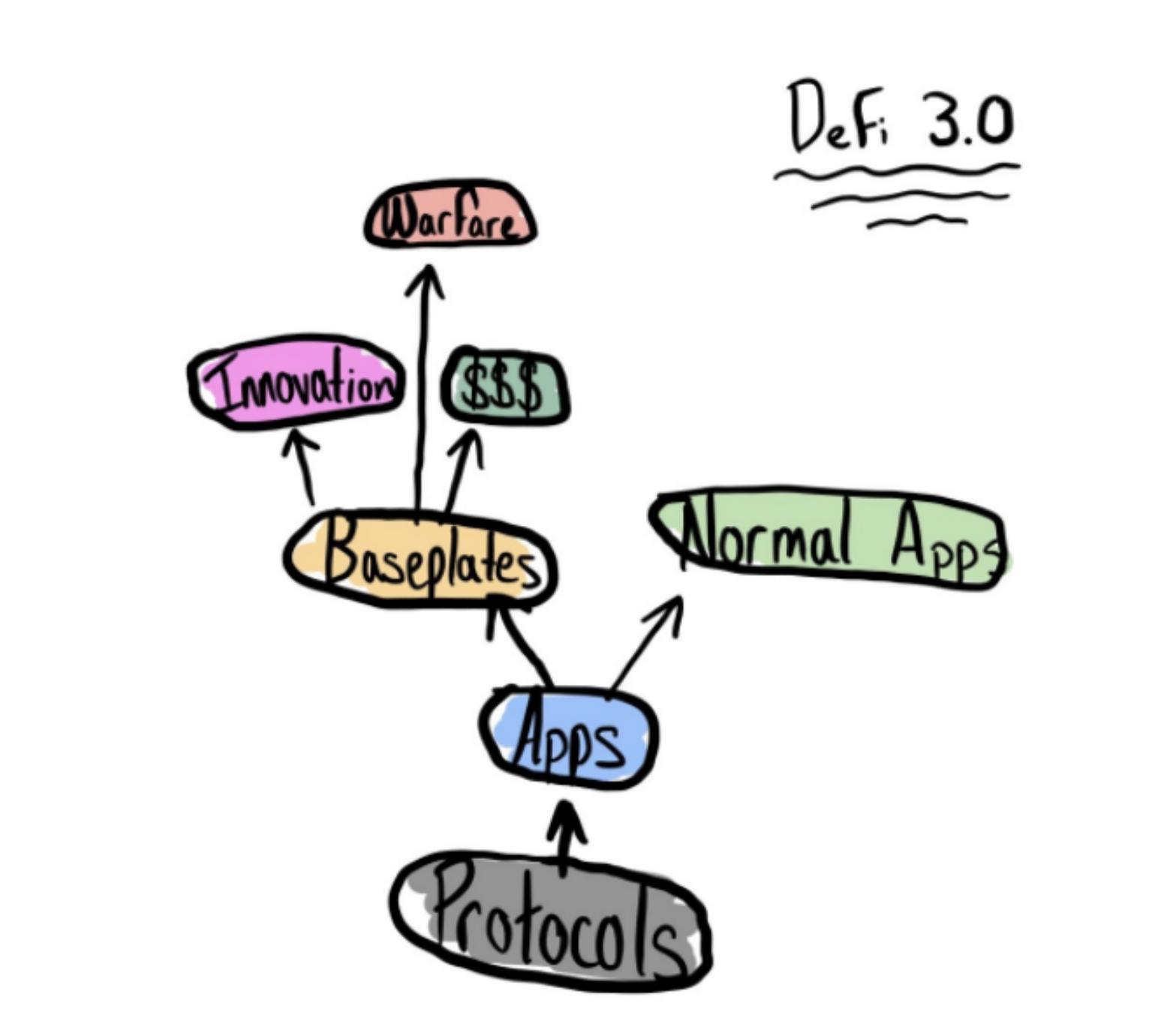

If you have played with LEGO bricks before, you know that the bottom of a base cannot connect to the top of any other brick. This is intentional, as bases are usually very large and designed to support other structures. Curve Finance changed the game, leading me to inevitably send this article to LEGO, requesting some updates on their bases—but let me explain.

Imagine a major base sitting on a table. Let’s call this the protocol layer, and to simplify further, let’s call this first-layer base Ethereum, because everyone loves Vitalik, and DeFi started on Ethereum. On top of the base, you might have some blocks stacked together, with more on top, forming a small fortress—these are our applications, existing on the protocols on Ethereum (the base). While many protocols can happily exist forever and maintain profitability and high TVL, some protocols can transcend this state and become the base itself—that is Curve Finance. Imagine Curve as its own base, stacked on the LEGO bricks we placed on the previous base.

"Wait, you just said that was impossible—"

I know, but we are breaking barriers and writing history, give me some time to explain. Curve has transcended the status of an application and become its own protocol because we have seen Convex and yearn hitching a ride on Curve's success and benefiting from Curve's deep liquidity and market share. Convex, yearn, and other protocols related to Curve are additional LEGO blocks built on the Curve base, all of which are built on the Ethereum foundation. Look at this beautiful image my graphic designer made for us, observing the separation between normal applications in DeFi and base applications.

Isn’t that amazing? Not only can one application evolve into its own protocol layer, but other protocols can also develop on top of it and eventually replicate this process if they can generate open loops themselves. Here is a passage from Sami's article that describes this situation better and more coherently than I can.

So, what is the next step for DeFi protocols? I propose an idea for a non-liquid governance token.

"But wait, non-liquid is bad because—"

Ah, give me a moment. We have seen the evolution from liquidity mining incentives to high APY rebase tokens converting to PoL—what if we combine these into a token that offers users absolutely no way to cash out? Whales control DeFi because they can migrate from protocol to protocol, thanks to the liquidity of reward tokens like cvxCRV or liquidity pools that can easily dry up. But this is not good for small fish, as they do not have the scale of a portfolio to play at that level and get caught in an upstream battle of information asymmetry. If protocols can adjust incentives between stakers by offering revenue-locking (rl) or governance-locking (gl) tokens, then users can easily demonstrate their trust and long-term belief in the protocol. These tokens can still accumulate value, providing future income shares for those brave enough to take the plunge and succeed through many waves of wealth and pain. Protocols will promote a high APY to attract investors, only to reveal that they are not about making anyone quick money—they are for those who truly care about the technology. This could perhaps be called ve(3,3)\^2, as protocols could implement a valve mechanism, or maybe we should completely abandon ve(3,3).

Currently, you can lock your CRV for up to four years, but the rewards are liquid, and users can choose to exit and reinvest, creating a slight incentive misalignment. I believe the solution to this is to weed out those who only want money.

Yes, I know the crypto space is a place where 99.9% of people are here to get rich, but what if we could do both in the long term? Locking tokens in protocols you believe in instead of opening 25 tabs and constantly refreshing Dexscreener to ensure your protocol isn’t getting wrecked or losing 75% of its TVL in a single trade feels much better, doesn’t it? Yes, before you rush to my DMs, four years is a long time for anything, especially when it involves locking your tokens in a protocol that hasn’t even existed for four years. I am absolutely sure that protocols can allow users to choose shorter time frames or even see locked token markets, like what happened with the JEWEL token in the DeFi kingdom.

While all of this may seem exaggerated, I do not think it is beyond the realm of possibility. DeFi lacks new narratives, and restoring the community-oriented aspect of DeFi would absolutely draw people’s attention back to the entire space. Maybe my dreams are too big, but I believe that by replicating the Curve model and creating something for protocols to compete for, we can actually start building something larger than ourselves. With that in mind, perhaps we should rename DeFi to something like OpenFi, as recent developments indicate that we have not yet reached the level of decentralization we should have. If that is a name for a protocol, then I apologize; it just rolls off the tongue, and I like it.

In summary, maybe this is all just a daydream of mine. The Curve Wars were an interesting time that made a lot of people money, the timeline was more optimistic, and my Substack era is at its peak. DeFi 3.0 has the potential to be something extremely different from what I have discussed, but I would be happy to see anything new emerge. If you are a protocol struggling to adapt to narrative shifts, perhaps you could adopt some new symbolic principles and emphasize community. This seems to work well for NFT projects too.

There’s No Such Thing as a Free Lunch

Unfortunately for all of us, this is now just a string of thoughts. Considering that 99% of CT believes everything will go to zero, none of this may come true. Cough, don’t listen to them.

If I could offer you a 100x new stock, I probably wouldn’t do it due to SEC reasons. But, hypothetically, if I could give you some severely overlooked DeFi token codes from the past month, would I????

Regardless of whether this argument holds, I am very optimistic about the future of DeFi, perhaps more than ever before. I see a lot of innovation happening in AMMs and derivatives, with more people than ever supporting DeFi, and the general lack of bullish sentiment on the timeline means we should have pumped long ago—but I guess we will have to wait and see.

I was worried that due to the pressures of school and other writing work, I had started to drift away from crypto, but somehow I became invigorated and excited again within days. It’s incredible. A significant portion of this article was written around 4 AM, and I have done my best to put together my current thoughts and opinions, although I inevitably missed some things I wanted to say.

As a whole, DeFi needs to return to its roots. We have received too much money and have become disconnected from our true mission—to democratize finance for everyone. If recent events in Canada have not awakened you to the urgency of our situation, I really don’t know what will. If you do not feel a serious unease about citizens’ bank accounts being frozen, perhaps DeFi is not for you. That is all I want to say.

At the end of the day, everything is a Ponzi scheme. Crypto is just a smaller Ponzi scheme where anonymous whales can sell you their tokens at any time, while we argue about which protocol can provide the highest yields, even if those yields can last in a terrible PvE environment. If we can ultimately achieve democratized finance for everyone, that would be fantastic. We have a long way to go, and until then, I guess we can only continue to use each other as exit liquidity until DegenSpartan destroys us all.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles