Will Tokemak be the next liquidity battleground?

Liquidity is the lifeblood of DeFi applications.

Liquidity is the lifeblood of DeFi applications.Author: Tangyuan, Hive Tech

Recently, DeFi applications have entered a liquidity competition, with the stablecoin protocol Curve being one of the main battlegrounds. Various stablecoin protocols are vying for control of VeCRV to gain more CRV inflation reward weight, attracting more stablecoin funds into their respective asset pools to enhance asset exchange depth.

Overall, the "Curve War" is essentially a struggle for the inflation power of CRV to guide the flow of stablecoin assets. The recently launched Solidly by YFI's founder also aims to control the token reward weight of Solidly through the issuance of its VeNFT, which can help DeFi applications attract more assets and guide user funds.

Whether it is the occurrence of the "Curve War" or the emergence of Solidly, both suggest that there are unreasonable aspects of liquidity in DeFi applications, including low capital utilization efficiency, and some DeFi applications are facing liquidity exhaustion issues. How to improve liquidity and manage it reasonably has become an urgent problem for DeFi.

A liquidity management protocol called Tokemak has emerged during the liquidity competition, claiming to guide liquidity "to where it should go," aiming to become a liquidity provider and professional market maker for DeFi applications.

According to Tokemak's official website, its locked crypto asset value (TVL) is $1.63 billion. In contrast, Curve's TVL is $19.9 billion, indicating a significant gap compared to leading DeFi protocols. However, due to Tokemak's potential to control liquidity direction and its claim to provide a "simpler and cheaper" way for DeFi applications to provide and obtain liquidity, it has begun to attract attention from the DeFi community, even being predicted to become the next "holy land of liquidity competition."

Why is Tokemak most likely to become the battlefield for liquidity competition? What is its operational mechanism? How does it guide liquidity flow? This issue of DeFi Hive will take you through its origins and developments.

"Liquidity" Determines the Life and Death of DeFi Projects

Whether it is the "Curve War," Solidly, or Tokemak, "liquidity" is becoming their common goal.

In traditional securities markets, "liquidity" is defined as the ease with which an asset or security can be converted into cash without affecting market prices. Among various valuable assets, real estate is considered a less liquid asset, not only due to its long realization cycle but also because prices can change based on the willingness of buyers and sellers. In contrast, stocks or funds have better liquidity, as they can be converted into cash at market prices at any time.

Correspondingly, the "liquidity" of crypto assets often refers to the ease with which a certain crypto asset can be converted into another crypto asset without affecting market prices. Compared to centralized finance (CeFi), the liquidity of peer-to-peer decentralized finance (DeFi) is harder to control or manage.

In the DeFi world, asset liquidity can also vary in quality. For example, BTC and ETH, as "crypto hard currencies," are assets with good liquidity. Especially ETH, which has trading pairs with other crypto assets on various decentralized exchanges (DEXs), the openness of DEXs makes ETH trading pairs more abundant, allowing users to easily exchange ETH for other assets without affecting ETH's price.

In comparison to ETH, the liquidity of governance tokens in DeFi applications is relatively poor. This is reflected in the fact that ETH can be directly exchanged for any DeFi asset like UNI, SUSHI, or CRV without affecting ETH's price, but assets like CRV, UNI, and SUSHI cannot be directly swapped with each other; to exchange CRV for UNI on a DEX, the typical path is to first convert CRV to ETH and then convert ETH to UNI. This "two-step process" not only increases transaction costs but also risks price drops for CRV if its trading volume is too high and there isn't enough ETH available for exchange, leading traders to bear slippage losses from CRV price fluctuations.

Liquidity is the lifeblood for DeFi applications. If a DeFi application’s issued token lacks liquidity, it means that the token cannot be traded in the secondary market and will not have a price. Even if the project assigns liquidity to the token, if the token cannot be exchanged for other crypto assets, the price loses its significance.

For emerging DeFi applications, issuing tokens is not difficult; solving liquidity issues is key. Currently, DeFi projects often guide funds to inject liquidity into project tokens through "liquidity mining" incentives. Users deposit other crypto assets (often mainstream crypto assets) into the token's liquidity asset pool, forming "asset pairs" to supply exchange or lending demands, and users providing liquidity assets will receive token rewards from the project. For example, if A is a token issued by a DeFi project, its liquidity asset pool often consists of A-ETH, A-USDC, A-USDT, etc. The DeFi project will reward A tokens based on the amount of liquidity assets provided by users.

As the DeFi market has developed, DeFi applications have gradually discovered that "liquidity mining" has many issues. Projects need to expend significant incentive costs to attract liquidity, and the funds participating in liquidity mining are not loyal; they are highly profit-driven. When token rewards decrease or yields drop, these liquidity providers will withdraw their funds and shift to other high-yield projects.

In such circumstances, unstable liquidity brings a chain of negative impacts.

To retain liquidity providers, DeFi applications have to release more token incentives, leading to token inflation. As token prices drop, the yields for liquidity providers are affected, and withdrawing liquidity and selling tokens become common practices.

The withdrawal of liquidity harms projects. When a token's liquidity worsens, its price experiences high volatility, and users exchanging the token face slippage losses, directly impacting user experience and leading to user exodus.

Moreover, when token prices fluctuate significantly, the impermanent loss for liquidity providers also increases, further prompting their withdrawal.

It is akin to entering a death spiral; when a DeFi application's liquidity management is poorly designed, the application will die as liquidity depletes.

To maintain token price stability, DeFi applications need to address token inflation and sell-off issues. Drawing from the "single-coin mining" approach, some DeFi applications have introduced staking incentives, encouraging users to lock up tokens to obtain yield-bearing assets with governance rights. VeCRV is a yield-bearing asset obtained by users staking CRV in Curve, allowing holders of VeCRV to earn CRV rewards and vote on the yield rates of asset pools in Curve.

However, this method only temporarily stabilizes the token price without resolving issues such as high liquidity acquisition costs and impermanent losses faced by liquidity providers. With the coexistence of multiple chains and the explosion of DeFi applications, the number of public chain assets and project tokens is increasing, and applications are not interoperable, leading to further fragmentation of asset liquidity and deepening the difficulties for projects to obtain liquidity, while the choices for liquidity providers also become complex.

These pain points remain unsolved mysteries, leading to the emergence of applications focused on this issue, with Tokemak being one of them.

Is Tokemak Born for "Liquidity"?

Tokemak defines itself as a liquidity management protocol, claiming to be "born for many liquidity issues." It can be seen as a "decentralized market-making platform" that can decompose liquidity and provide it to DeFi applications in need.

If we distinguish according to the To B or To C logic of internet products, Tokemak should be classified as a To B product, serving the liquidity needs of DeFi applications. It claims to provide a "simpler and cheaper" way to obtain liquidity for DeFi applications, but how does it achieve this?

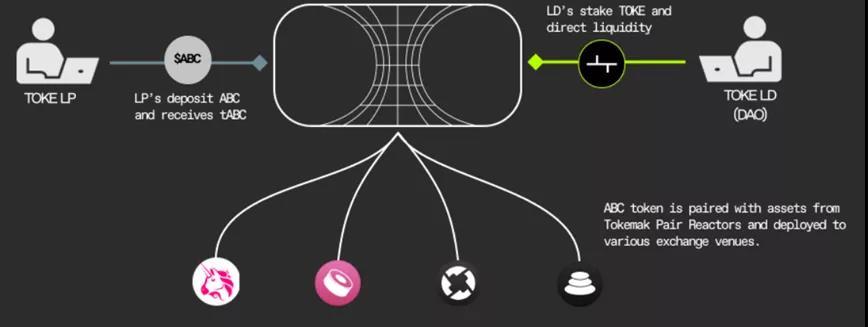

According to Tokemak's introduction, it has created a concept of a "reactor" to guide liquidity. This "reactor" is an asset pool created by Tokemak for each liquidity asset. Unlike the previous LP (A-B) pairing model, the "reactor" asset pool consists of two roles: "Liquidity Providers (LP)" and "Liquidity Directors (LD)." LPs mainly provide assets, while LDs primarily guide the flow of liquidity.

In previous DeFi applications, users providing liquidity needed to hold both A and B assets. If they only held a single asset A or B, they often needed to pair A and B according to the price ratio of the two assets, such as converting 30% of asset A into asset B and then pairing them as A-B to provide liquidity. If the prices of assets A and B fluctuate, users providing liquidity must bear impermanent losses, meaning that upon withdrawal, the quantities of A and B assets will be less than what was initially provided.

Tokemak eliminates the need for a single user to pair A and B to provide liquidity, instead allowing different clients to deposit their held assets into the "reactor," which will pair various assets to form liquidity pools and supply liquidity to DeFi applications. It appears to have the "single-coin mining" function of a liquidity pool, but the destination of this liquidity is determined by LDs, not the liquidity pool itself.

Tokemak Reactor Workflow

According to the image above, the left side represents Liquidity Providers (LP), while the right side represents Liquidity Directors (LD).

LP only needs to deposit a single token ABC into the "reactor" to obtain a certificate tABC; upon withdrawal, 1tABC = 1ABC. During the liquidity provision period, the profits generated from the "reactor" providing liquidity externally will be directly deposited into the Tokemak application, managed by a dedicated community organization. The rewards LPs receive for providing liquidity are solely the platform token TOKE of Tokemak.

LD controls the direction of liquidity by staking TOKE, i.e., staking TOKE into different asset "reactors" to obtain staking rights. These rights come with voting rights, allowing LDs to decide which DeFi applications can access the liquidity assets in the "reactor." LDs will also receive TOKE rewards. The above "reactor" diagram shows that LDs can guide liquidity into Uniswap, Sushiswap, Balancer, and the 0x protocol.

Tokemak allocates liquidity to DeFi applications by coordinating LPs and LDs. LPs provide assets to the system through single-coin staking, simplifying the process of calculating fund pairing when providing liquidity and avoiding impermanent losses; while LDs guide liquidity into DeFi applications through staking TOKE and voting.

Have you noticed that the existence of TOKE rewards leads to an overlap between the roles of LP and LD? ------ LPs provide liquidity to earn TOKE rewards, and they can stake TOKE to become LDs to guide liquidity. Of course, they can also choose not to do so and sell TOKE, which could lead to a lack of responsibility for LDs.

For Tokemak to effectively coordinate LPs and LDs in fulfilling their respective roles, it needs to balance TOKE incentives and TOKE staking. To this end, it employs a "dynamic yield (variable APY)" balancing mechanism.

SUSHI Reactor

If a large amount of assets is deposited into the corresponding left-side asset "reactor," while the amount of TOKE staked to guide that asset's liquidity on the right side decreases, the yield (APY) for staked TOKE will increase, encouraging LDs to stake more TOKE to participate in guiding the liquidity of that asset. Similarly, if a large amount of TOKE is staked in a particular asset's "reactor," while the left-side deposited assets are low, the yield (APY) for LPs will increase to incentivize the deposit of liquidity assets.

For example, if a new DeFi project wants to increase the liquidity of SUSHI, in the traditional model, the project might increase SUSHI incentives to stimulate liquidity providers' funding enthusiasm. However, if SushiSwap chooses Tokemak, the application can hold and stake a certain amount of TOKE in the SUSHI asset "reactor," and the increase in APY for the LP reactor will attract users to deposit SUSHI to provide liquidity. Thus, SushiSwap can guide liquidity as needed; the more TOKE staked, the more SUSHI and long-term liquidity providers it can attract.

Tokemak locks its incentive model into the liquidity supply-demand relationship of various DeFi applications, preventing liquidity from fluctuating due to the varying mining rewards of a particular application, thus addressing the liquidity dilemma faced by DeFi applications to some extent.

Tokemak's Problems and Risks

Recently, the "VeCRV control" dispute that occurred on Curve is, in fact, a liquidity competition among various stablecoin protocols on Curve. If stablecoin project A goes live on Curve, A can achieve direct exchange with mainstream stablecoins like USDT, USDC, and DAI on Curve, solving A's liquidity problem. However, for A to go live on Curve, it needs to gain support through VeCRV voting.

The recently launched liquidity management protocol Solidly also draws from Curve's operational mechanism, allowing new DeFi applications to attract liquidity funds by obtaining VeNFT certificates issued by Solidly. Solidly is also more open, allowing any DeFi application token to be listed in the asset pool. However, since Solidly has just been launched, its liquidity solution capabilities remain to be observed.

As a liquidity management protocol launched in 2021, Tokemak has been operating for some time without any vulnerabilities, and it proposes an alternative solution to liquidity compared to Curve and Solidly.

For example, if a new DeFi project wants to issue B Token, it can first purchase and hold a certain amount of TOKE and allocate a certain amount of B Token into Tokemak as "reserve pool" assets to cover potential impermanent losses for LPs. At this point, Tokemak will establish a reactor for B assets, and the project will become an LD.

The more TOKE the project stakes, the higher the LP's yield will be adjusted according to the "reactor" dynamic yield, thereby attracting LPs to deposit B Token assets to provide liquidity.

At this point, the "reactor" LD will guide B assets to pair with B-ETH, B-USDC, etc., and distribute them to the required DEXs. Tokemak can earn liquidity rewards from B-ETH and B-USDC, which are B assets, and this income will enter the Tokemak protocol.

Tokemak's ambition is significant, as while it provides and guides liquidity for DeFi applications, it is also continuously earning governance voting rights for that application by acquiring a certain DeFi asset. These voting rights are likely to guide more DeFi assets into Tokemak. Meanwhile, users providing liquidity funds to Tokemak will only receive TOKE rewards, not rewards from liquidity demanders.

Through this operational approach, Tokemak gathers the liquidity mining rewards of various DeFi applications into its own coffers. Once the accumulated various DeFi assets reach a certain quantity, it may become an independent operator, no longer needing third-party LP providers, thus becoming a "liquidity kingdom." At that time, it will determine the direction and allocation of liquidity.

In other words, whoever controls TOKE can control the liquidity direction of assets on Tokemak. DeFi applications can also restrain Tokemak's decision-making power by holding more TOKE. The taste of mutual competition and conflict arises.

Although Tokemak provides an alternative solution for liquidity management in DeFi applications, it also carries certain risks, as TOKE can be sold. If TOKE is not recognized by the market, leading to price depreciation or even dropping to zero, then this protocol will also fail.

Risk warning

Risk warning Risk warning

Risk warning