Interpretation of the Four Pillars of Token Economics and the VE Token Model

In simple terms, the design of the Token economic model is all about creating methods that influence short-term and long-term supply and demand. Ideally, the best design is one that encourages demand while reducing supply, but this is easier said than done.

In simple terms, the design of the Token economic model is all about creating methods that influence short-term and long-term supply and demand. Ideally, the best design is one that encourages demand while reducing supply, but this is easier said than done.Written by: Captain BTC

Compiled by: 0xzshanzhan

Designing Token Economic Models is Difficult

For a project, the design of the Token economic model is crucial, and it is also one of the most challenging aspects of the project. This is essentially about creating a complete economic system from scratch, without any real-world experience to rely on.

A slight error in the design of the Token model can impact the entire project, even if other aspects of the project are well-designed. The immutability of smart contracts further emphasizes the importance of the initial Token design. Once the contract is released, a fork is needed to update the protocol.

Although Token economics is complex, it is still subject to the basic laws of economics, namely supply and demand. Simply put, the design of the Token economic model is about designing methods that influence short-term and long-term supply and demand. Ideally, the best design encourages demand while reducing supply, but this is easier said than done.

Four Pillars

Before delving into the complexities of "ve" Token design, this article will introduce the basics of Token economics. In my view, every cryptocurrency has four fundamental pillars of Token economics, which is the first thing investors should analyze before diving deeper into Token economics. Any design flaw in these pillars poses a risk to the Token economic model in the future; if the flaw is severe, it could lead to the collapse of the entire economic model or cause the project to bleed out slowly, like a rusting abandoned building.

Supply

Nothing is more fundamental and important than managing the number of Tokens, and part of that management is supply. We can categorize supply into:

Circulating Supply:

The number of Tokens in circulation in the market.

Max Supply:

The theoretical maximum number of Tokens that the protocol can produce.

Total Supply:

The number of Tokens that have been issued. This includes Tokens that have been burned and locked. Even if these Tokens are not part of the circulating supply.

The higher the supply, the lower the price. I believe you often see comments like, "Look at ADA, it's only $1, imagine how much I would make if it just reaches 50% of Bitcoin's price!" This is because they do not realize that ADA's supply is 45 billion, while Bitcoin's supply is 21 million. This is why market capitalization is a more accurate metric than just looking at Token prices, as it affects both price and supply.

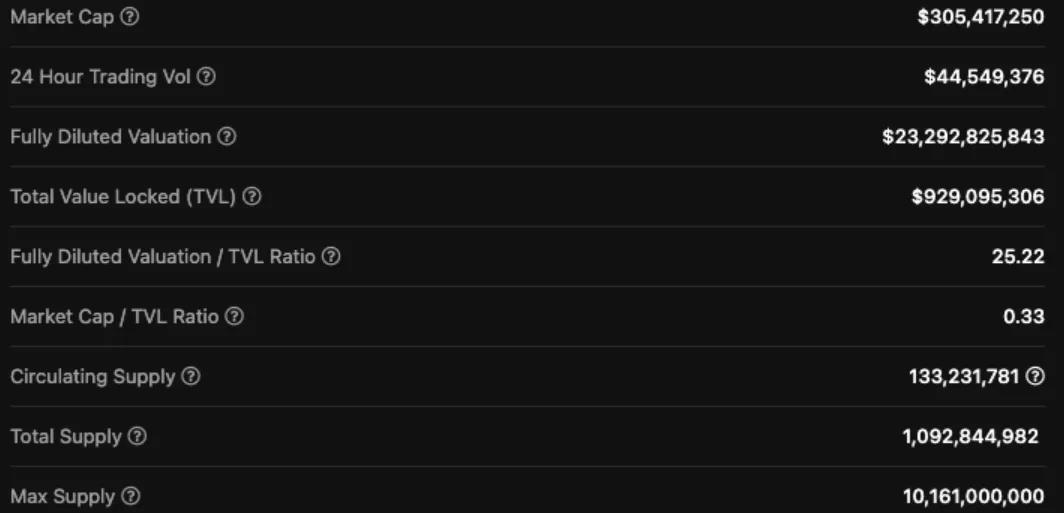

Comparing circulating supply with total supply and max supply reveals interesting phenomena. For instance, if the circulating supply is low while total supply and max supply are high, this is a huge danger signal because the value of your Token will be diluted, as shown in the image below:

This Token has a circulating supply of about 133M and a max supply of 10B. There is about an 8-fold dilution risk for your Token, which is a significant issue.

If all Tokens are released tomorrow, your Token's value will be 1/8 of what it was yesterday. Suppose you bought in at a market cap of $305 million today, expecting it to reach 100 times in 5 years. This would bring the market cap to $30B (quite high, but not uncommon in cryptocurrency), but the fully diluted valuation would reach $2.3T (higher than today's cryptocurrency market cap).

Moreover, even if the market cap increases, the regular issuance of these Tokens will increase the circulating supply, putting downward pressure on the price. This is not to say that everything about this Token is bad; they may even have ways to offset supply pressure, but this is a risk factor that long-term investors should be aware of. Short-term investors are less concerned about max supply because they may have already exited by the time the Tokens are unlocked.

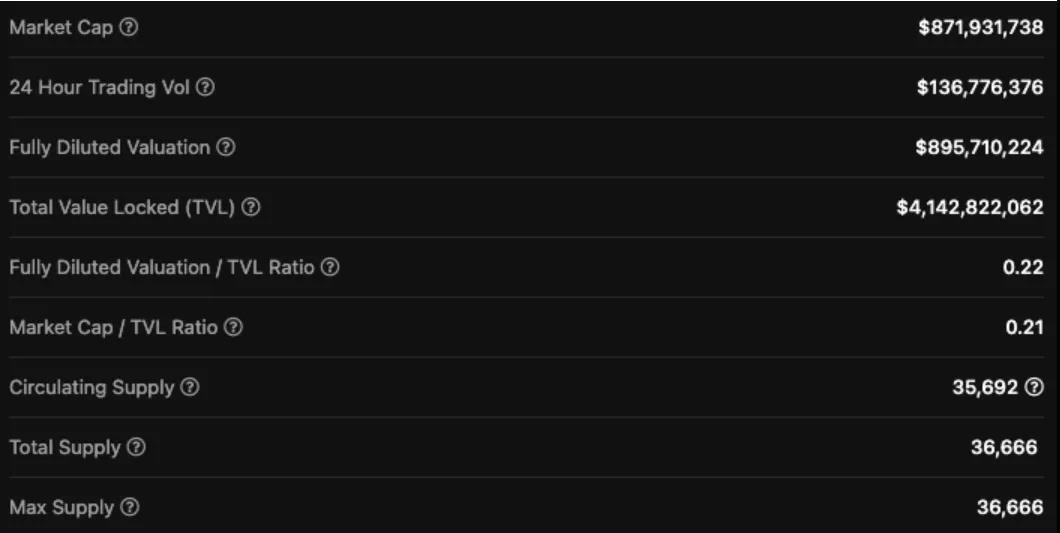

Here is a contrasting example where the circulating supply is close to the max supply. However, this does not mean that this project is reliable, but it does reduce the risk for investors.

Distribution

The distribution of Tokens is the next pillar of the Token economic system that investors should pay attention to, and it is a very straightforward pillar. Distribution refers to the distribution of the percentage of specific Tokens held by each wallet. Would you want one person to hold 70% of the token supply? If you do, then that project will be very centralized, and they can endlessly dump Tokens, making us retail investors poorer and jeopardizing the project's future.

A good distribution design aims to allocate Tokens to as many people as possible. This way, if someone wants to exit, their sell-off won't significantly impact the price. The best way to check Token distribution is to look at the Token allocation chart in their whitepaper and check the wallet distribution on a blockchain explorer.

Monetary Policy

Monetary policy determines whether the Token is an inflationary or deflationary model, and it also decides the degree of inflation/deflation and the overall consensus mechanism of the project. As mentioned earlier, high inflation can lead to asset prices declining over time.

A low inflation rate combined with POW (like Bitcoin) can be a good thing because it can create productivity within the ecosystem. Ethereum 2.0 and EIP 1559 allow ETH to be burned with each transaction, which theoretically should make Ethereum deflationary.

This leads to my next thought on how to analyze the four pillars of Token economics together and their interactions. Let's revisit the example of a highly diluted Token from the supply section of this article.

While it has a high FDV, suppose its monetary policy consumes 7% of the circulating supply annually and has a 5% Token release plan each year. So even if 7/8 of the supply is locked and there is inflationary pressure, this results in a year-on-year deflation rate of 2%. Under this monetary policy, the Token will not face any inflationary pressure from locked supply, but in reality, there is negative supply pressure due to the reduction in circulating supply.

Finding the interactions among various pillars of Token economics can help us clarify the advantages of Token economics. Looking at just one pillar can often be misleading. (Note that there is debate about whether burning is an effective use of funds, so this article uses Token burning as a simplified example to explain this concept.)

Value Capture

The final pillar is how much value the protocol captures and how that value should be distributed. In Web 2, all captured value goes back to companies like Facebook, Google, and Twitter. They earn billions from user data and social media interactions, while users receive zero dollars in return.

Users might get a blue checkmark at most. Web 3 disrupts this by allowing protocols to capture the value they provide and distribute it to Token holders. You can be a user of the protocol and simultaneously receive rewards.

Not all protocols can effectively capture value. I believe that before we have a Token architecture that can capture 100% of the value provided by the protocol, a lot of research and experimentation is still needed.

The simplest comparative example is the battle between Uniswap and Sushiswap in 2020. Uniswap launched their AMM (Automated Market Maker) but did not release a Token. Of course, they provided an innovative product with significant value, but they captured 0% of the value for network participants. Then Sushiswap forked Uniswap and created the SUSHI Token.

SUSHI holders can vote on governance issues and stake their SUSHI for xSUSHI to earn transaction fees generated by the protocol. While this model is far from perfect, it allows Token holders to share in the revenue much more than the value captured by Uniswap's model. If Uniswap had launched a Token that could capture value at the time of the AMM release, it would have been much harder for Sushiswap to gain new users.

VeToken Economic Model

That covers the basics, so what is Ve?

Ve stands for "voter escrowed," and it has rapidly become a popular Token economic model adopted by newer DeFi protocols since its introduction. Interestingly, the ve model was invented by Curve Finance, which is part of "DeFi 1.0."

It works by locking your CRV tokens and converting them into veCRV, which has governance capabilities within the protocol. The locking period is not fixed; Token holders can decide how long they want to lock their CRV, up to a maximum of 4 years.

Over time, the amount of veCRV held by the holder linearly decreases during the locking period. This incentivizes holders to regularly re-lock their CRV for maximizing governance and rewards. The main innovation is how to create weighted voting and weighted rewards. Additionally, once you convert CRV to veCRV, you are locked in for the specified time period and cannot unlock early like with other protocols.

Suppose Bill and Alice each have 100 CRV. Bill decides to lock his CRV for 2 years, while Alice locks hers for 4 years. Even though they initially have the same amount of CRV, Alice will end up with twice as much veCRV as Bill, meaning she will have twice the governance votes and rewards compared to him.

Effects of the VeToken Economic Model

One of the main problems that the veToken economic model addresses is the 1 token = 1 vote issue. In non-ve models, large whales can purchase massive amounts of tokens for short-term governance and reap rewards without bearing any risks beyond short-term prices. Thus, a competing protocol can buy millions of dollars worth of competitor protocol Tokens and vote in favor of bad proposals, then dump the Tokens.

In the ve model, this type of whale manipulation is much less effective because their votes are not as valuable as those of long-term holders. If a protocol or whale wants to have a significant impact on another protocol, they will have to lock their Tokens for a period of time. Once their Tokens are locked, it creates an incentive to act in a way that aligns with the best interests of the protocol. The CRV wars are the best example of this.

Moreover, supporters of the protocol who choose the longest locking period will have a greater say than those under the 1 token = 1 vote model. Compared to short-term speculators, these die-hard supporters gain more rewards and passive income. As long as the protocol continues to progress, stakers will understand that they will receive passive income in the foreseeable future rather than jumping from one protocol to another under uncertain conditions.

Finally, the ve model directly impacts 3 of the 4 pillars, with distribution being the only pillar that has a weaker relationship with the Ve model.

The Ve model affects supply through the long-term locking of Tokens. Holders are incentivized to lock their Tokens for the long term to maximize their influence and rewards.

When these Tokens are locked, they exit the market for a long time, reducing sell pressure. Because of the reduced supply, this should organically lead to price increases over time. This circulating supply performs exceptionally well compared to the 1 token = 1 vote model.

VeToken holders are the ones who determine the protocol's monetary policy, just like in the 1 token = 1 vote model. The difference is that the veToken model is an upgrade because it aligns the long-term incentives of the protocol with those of the stakers.

As mentioned earlier, this incentivizes holders with the most vested interests to vote in favor of favorable monetary policies for the protocol, rather than allowing potential malicious third parties or self-interested parties to support policies that harm the protocol.

The final pillar where the ve model has a significant impact is how the protocol distributes the captured value to its holders. The model allocates captured value based on how long you are locked. However, there is still a lot of room for innovation to maximize the value returned to users.

Innovation

Many protocols in the DeFi space are striving to implement the veToken economic model, which is great! Compared to traditional token economic models, this is a step forward, but veTokenomics will not be the pinnacle of token design.

This section will introduce some projects that are using the veToken economic model as a foundation for innovative designs. (Note that I am not suggesting you invest your entire net worth into the Tokens discussed below; I am merely discussing the innovations they are exploring within the veToken economic model, which remains an unknown experiment.)

Cartel is currently creating a ve version of their BTRFLY token, but with a twist. They plan to release blBTRFLY and dlBTRFLY instead of veBTRFLY, representing bribery locking and DAO locking of BTRFLY, respectively. blBTRFLY is a retail-focused Token that maximizes returns for holders, while dlBTRFLY focuses on DAOs and protocols that want to maximize their DeFi governance. Simplified understanding:

blBTRFLY = Higher Yield

dlBTRFLY = Greater DeFi Governance Power

This is an interesting design based on the veToken economic model, and I will be watching how it operates in practice.

The next innovative protocol is Trader Joe. They have released a new Token economic model that introduces three derivatives of Joe to replace xJOE, namely: rJoe, sJoe, veJoe.

Staking JOE for rJOE allows rJOE holders to participate in project launches within the JOE ecosystem. (Rocket Joe is more subtle than this, but that is beyond the scope of this article.)

Staking JOE for sJOE allows sJOE holders to share in the revenue paid by the platform. This revenue is paid in stablecoins, allowing users to earn passive income.

Staking JOE for veJOE allows veJOE holders to earn higher rewards in the Joe farm and gain governance rights.

The veToken economic model is currently in a developmental phase. We are seeing protocols begin to create multiple derivatives of their main Token, each with a specific use case. This allows users to maximize their investment strategies in the parts of the protocol they are most interested in.

Conclusion

In summary, Token economics is difficult, and protocols need to ensure the correct pairing of the four pillars with the economic system. Additionally, they need to innovate on top of these four pillars to remain competitive. The VeToken economic model represents a significant step forward and is a huge improvement over previous Token economic systems.

It reduces supply, rewards long-term investors, and aligns the incentives of the protocol with those of investors. In 2022, more protocols will continue to add the veToken economic model to their design architecture and innovate on top of the veToken economic model as middleware to create unique economic systems.