Amara finance: A brief overview of the development of algorithmic stablecoins and infrastructure construction

The risk of negative premium for algorithmic stablecoins is far greater than that of positive premium. At the same time, if a negative premium occurs for algorithmic stablecoins, users who have deposited into LP can still arbitrage through market repurchase. Additionally, a negative premium does not increase the liquidation risk of positions; rather, it reduces the debt ratio.

The risk of negative premium for algorithmic stablecoins is far greater than that of positive premium. At the same time, if a negative premium occurs for algorithmic stablecoins, users who have deposited into LP can still arbitrage through market repurchase. Additionally, a negative premium does not increase the liquidation risk of positions; rather, it reduces the debt ratio.Source: Amara finance

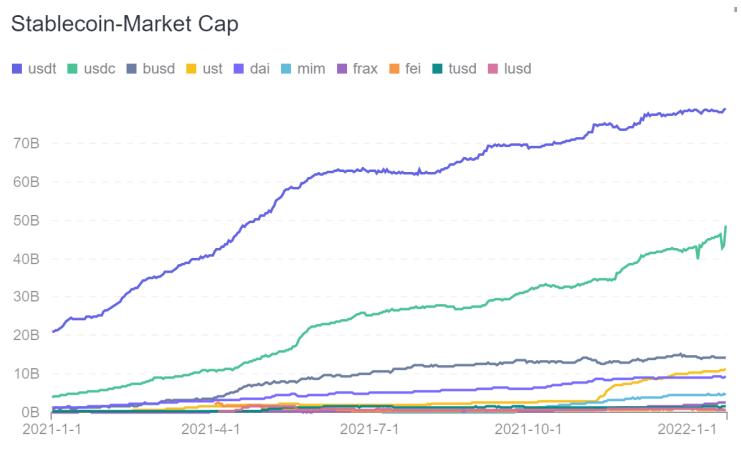

Stablecoins have seen significant growth as the infrastructure of the crypto world, driven by market development and the rise of on-chain applications. As of December 29, 2021, the circulating market capitalizations of major stablecoins were USDT $78.2 billion, USDC $42.1 billion, BUSD $14.6 billion, UST $10.1 billion, DAI $9.3 billion, FRAX $1.7 billion, TUSD $1.3 billion, and USDP $0.9 billion, totaling $158.2 billion, with an overall growth of 471% over the past year.

Stablecoin Market Capitalization Source: Footprint Analytics

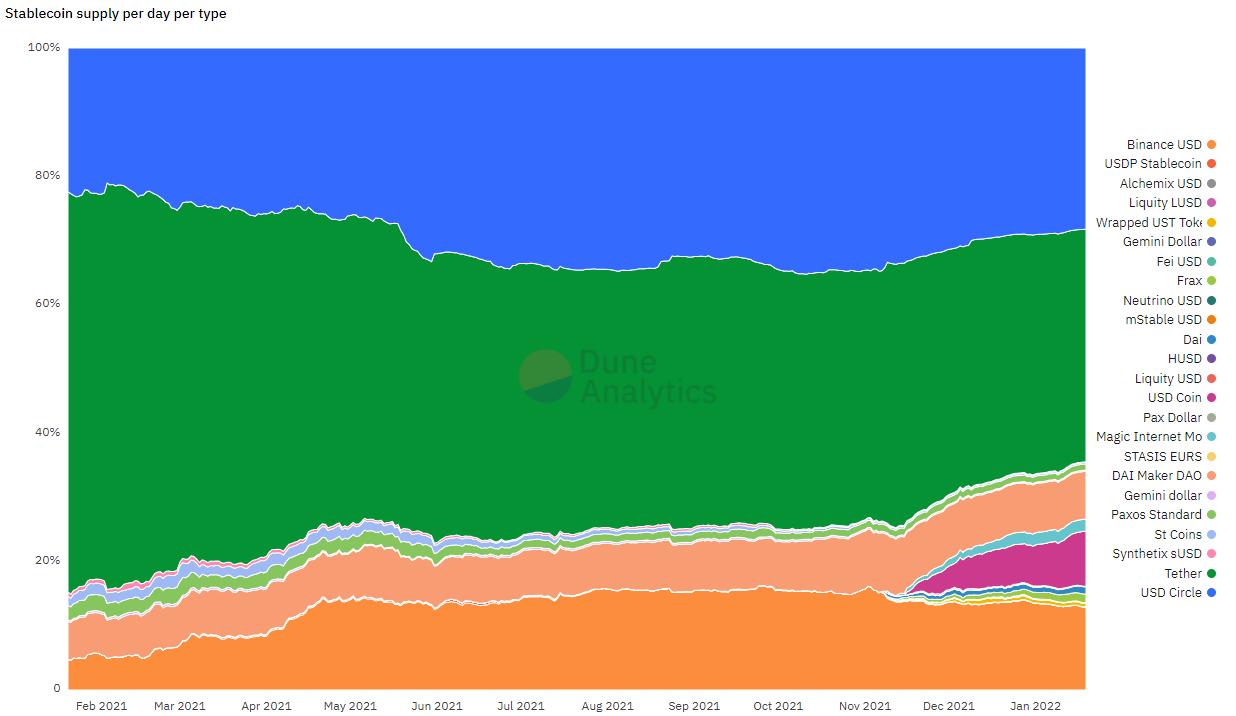

Among them, centralized stablecoins still dominate the composition, accounting for over 85% of the market capitalization. However, as issues related to compliance and asset transparency have been disclosed, the risks of centralized stablecoins have gradually emerged. Therefore, the crypto world has begun to explore decentralized stablecoin solutions.

The emergence of over-collateralized stablecoins, represented by MakerDao, has opened a viable path for decentralized stablecoins, but over-collateralization not only leads to low capital efficiency but also restricts growth based on the market value of collateral. As a result, new algorithmic stablecoin solutions have gradually emerged, with algorithmic stablecoins like UST, Frax, and Fei coming to the forefront.

Market Capitalization Share of Different Stablecoins Source: Dune Analytics

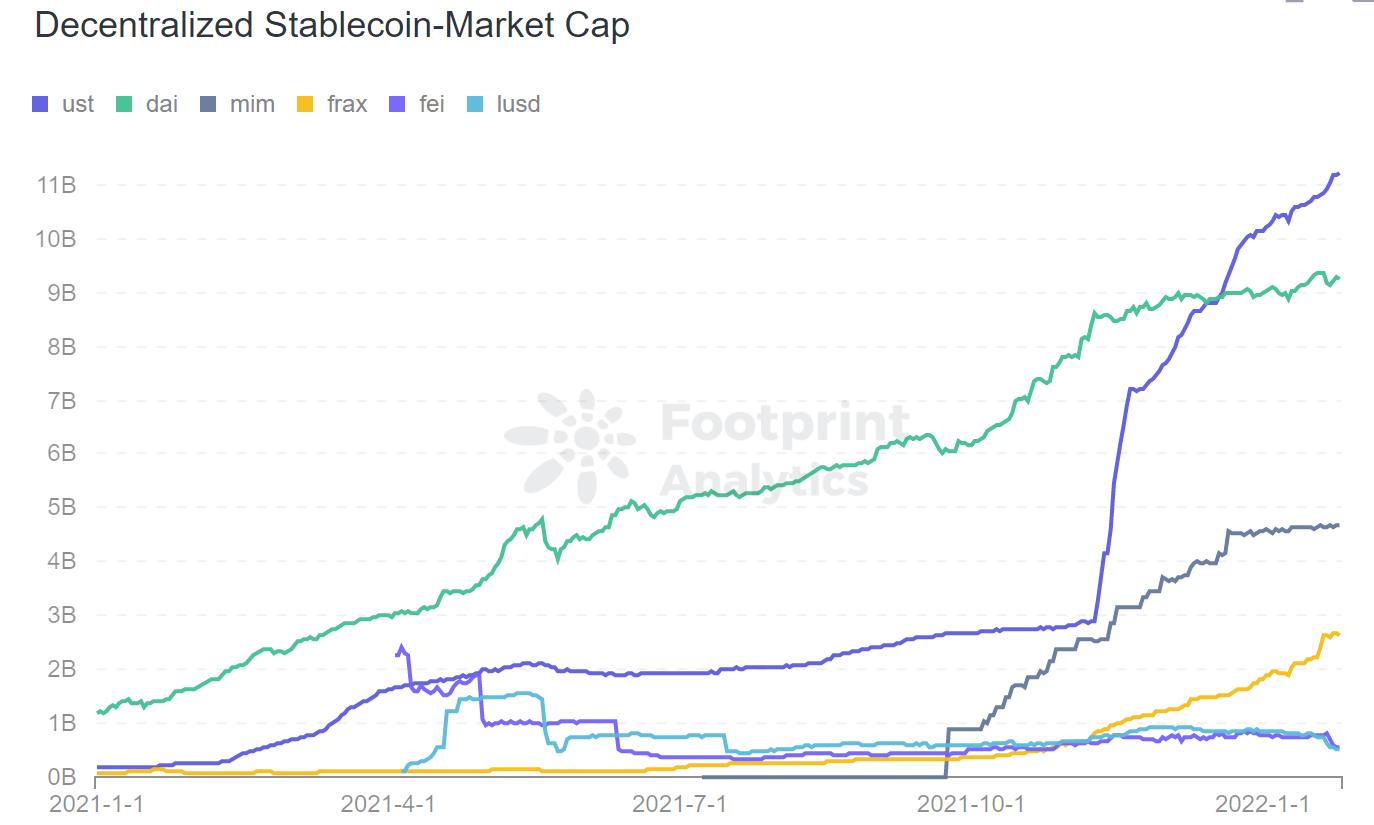

Currently, UST's circulating market capitalization has reached $11.22B, surpassing DAI's issuance, and has grown over 300% in just two months since November. Undoubtedly, algorithmic stablecoins have entered a rapid development phase and are gradually demonstrating their high capital utilization and growth characteristics.

Decentralized Stablecoin Market Capitalization Source: Footprint Analytics

However, the lack of infrastructure for algorithmic stablecoins is constraining market development. Almost every project needs to create its own application scenarios to empower stablecoins and provide substantial subsidies in project tokens to increase stablecoin usage, which undoubtedly places a heavy burden on project developers. An analysis of UST and MIM serves as an example:

The Luna ecosystem continuously cultivates ecological projects to empower UST, such as the Luna lending platform Anchor, which incentivizes UST lending with high token subsidies, encouraging users to hold UST and lend on the Anchor platform, thereby maintaining UST's usage rate.

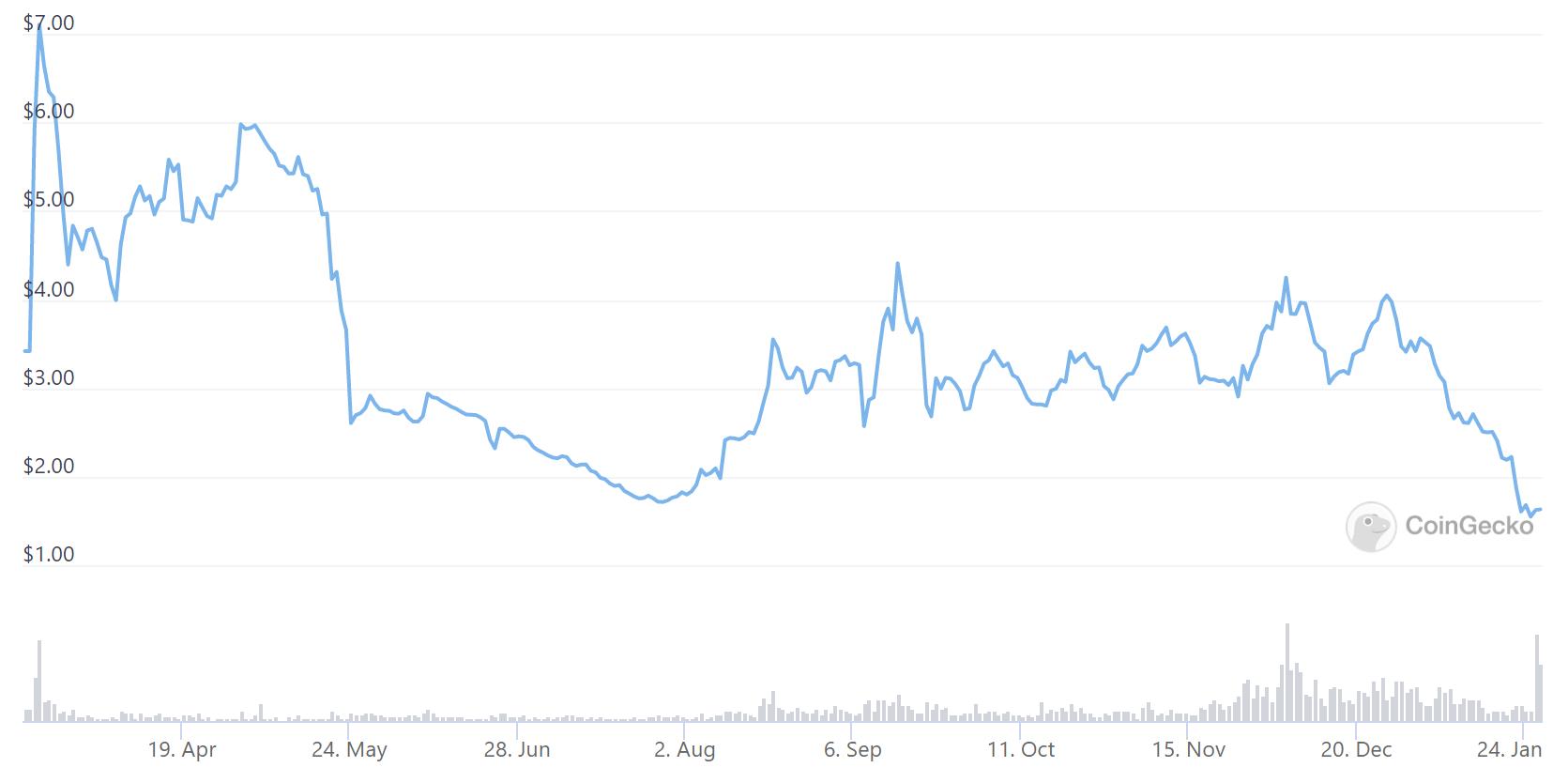

Every project in the Luna ecosystem is sacrificing its own interests to subsidize UST, which ultimately hinders the development of ecological projects. Since its launch, Anchor's token price has consistently declined, dropping 80.2% from its peak.

Anchor Token Price has dropped 80.2% since its launch Source: CoinGecko

MIM's innovative yield-bearing token collateral minting mechanism significantly improves capital efficiency, but a milestone affecting MIM's ecosystem development was seizing the liquidity incentive war of Curve. By acquiring a large amount of CRV voting rights early on, MIM's pool was able to provide substantial CRV token rewards as subsidies, increasing MIM's usage due to the high incentives.

From the analysis of these two cases, successfully developing a stablecoin ecosystem requires two conditions: high subsidies + application scenarios. For project developers, without other ecological projects sacrificing their own development or seizing liquidity incentive opportunities like CRV, it is challenging to achieve a cold start. If the project solely relies on token liquidity incentive subsidies, it will face significant selling pressure in the future, easily triggering a death spiral in token prices.

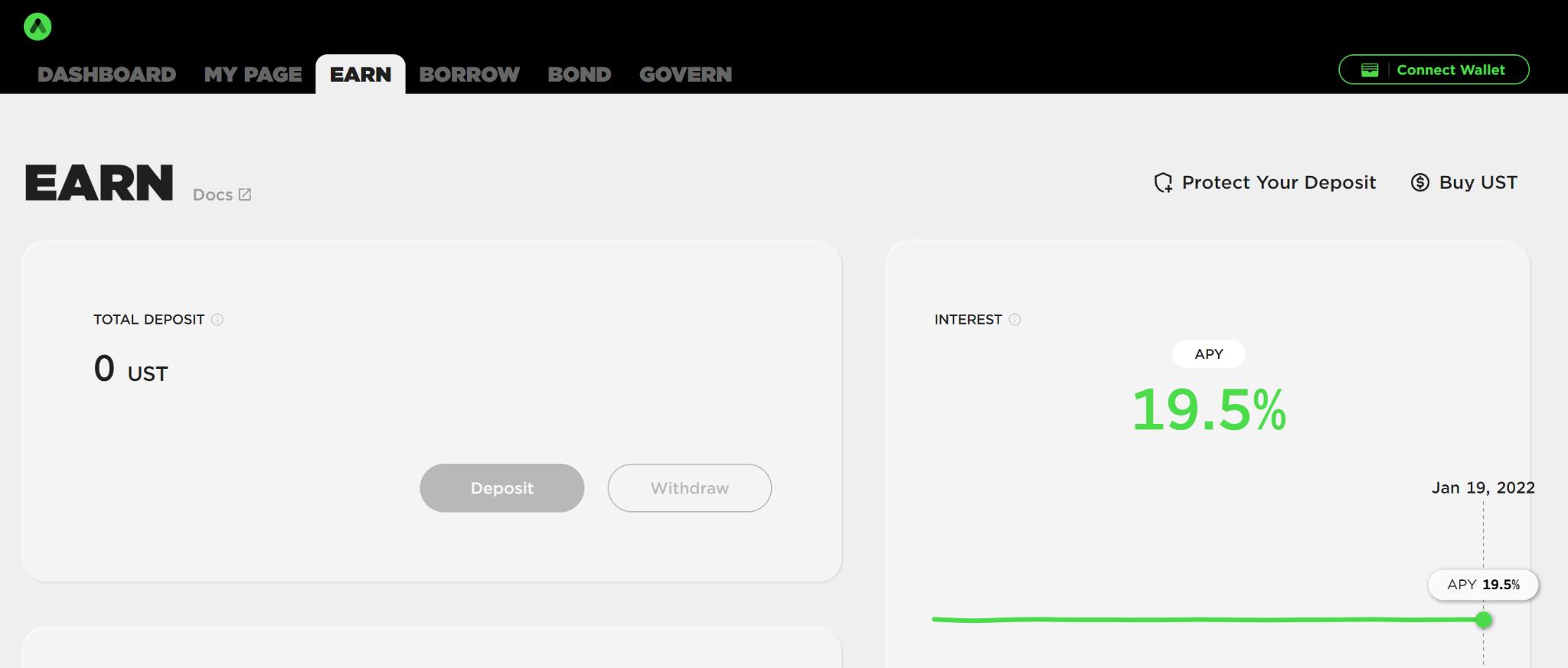

At the same time, the market volatility of algorithmic stablecoins is higher than that of mainstream stablecoins, resulting in higher interest rates for holders. Taking UST as an example, the subsidized interest rate on Anchor remains at 19.5%. If the project does not provide token subsidies, it is difficult to promote the application of stablecoins.

In Anchor, the subsidized UST lending yield is maintained at 19.5%

Amara Finance------Building Long-Tail Asset Lending & Algorithmic Stablecoin Infrastructure

To address the current pain point of a lack of application scenarios for algorithmic stablecoins, Amara will build a brand new long-tail lending market. Long-tail LP assets will be used as collateral to lend algorithmic stablecoins. Currently, long-tail LP assets can only participate in liquidity mining, with no other applicable scenarios, resulting in very low capital utilization. In Amara, users can deposit their long-tail LPs, which are engaged in liquidity mining, into the Amara platform, allowing them to lend algorithmic stablecoins supported in the Amara market without affecting their liquidity mining returns.

In mainstream lending protocols, long-tail assets are often difficult to use as collateral due to higher risks. However, half of the value of the long-tail LPs supported by Amara consists of mainstream cryptocurrencies, significantly reducing the volatility of the assets and largely addressing the price fluctuation risk.

At the same time, the borrowable assets are algorithmic stablecoins, with risks and depths that nearly match, thus avoiding certain malicious risks. In terms of interest rates, long-tail LPs in the liquidity mining market often yield annual returns exceeding 100%, so slightly higher interest rates will not affect the utilization rate of stablecoin lending.

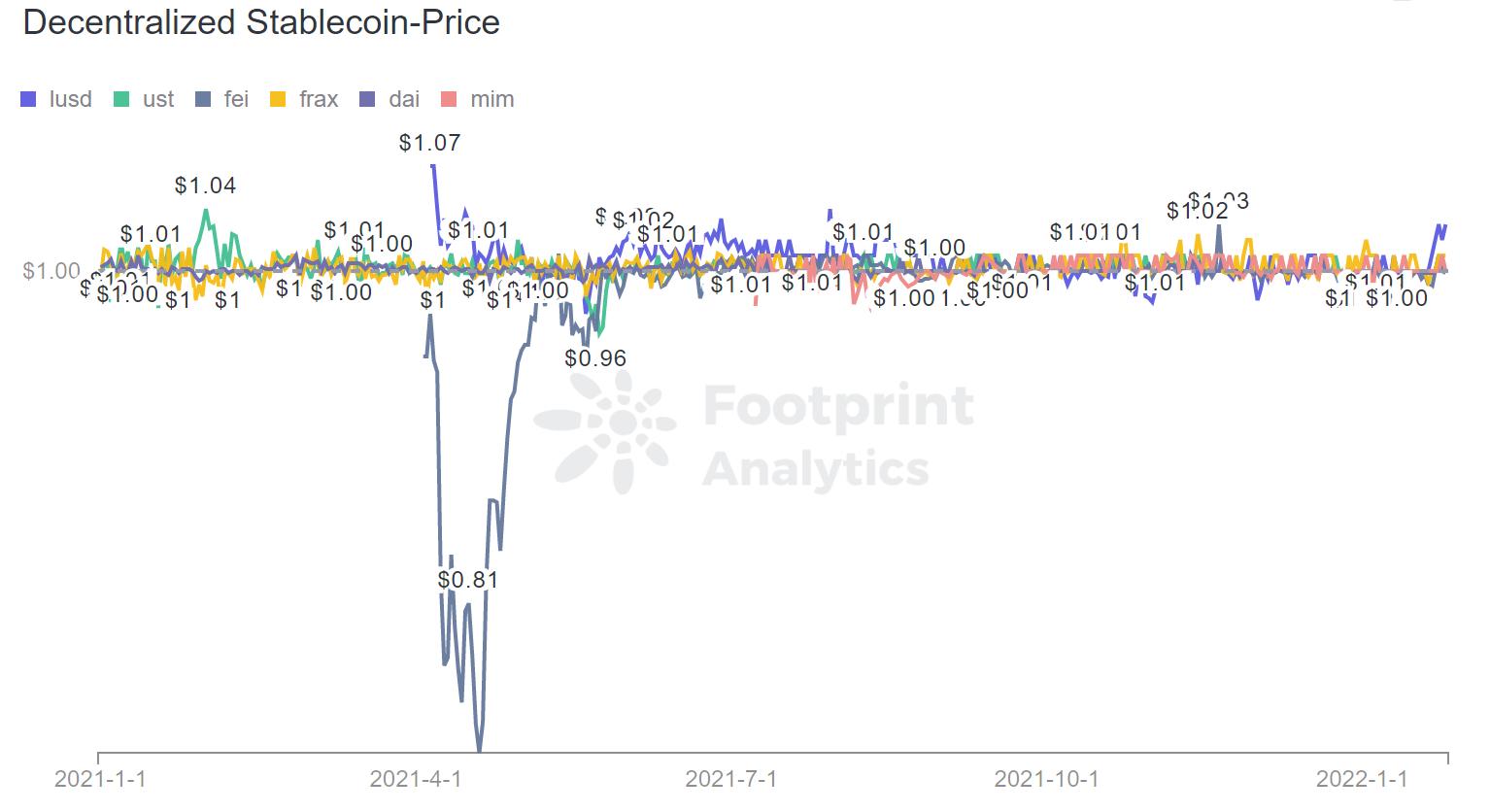

The biggest problem facing decentralized stablecoins is that before a strong community consensus is formed, if a bear market occurs, the assets controlled by the protocol may significantly shrink, and the price of the stablecoin can easily fall into a negative premium due to panic, with very few instances of sustained positive premiums. LUSD once reached $1.07 but quickly returned to within a ±3% range, while Fei faced insufficient use cases at its inception.

The imbalance of supply and demand leads to price decoupling, causing the protocol-controlled assets to plummet from an initial $2.4 billion to $500 million in an instant. Therefore, for decentralized stablecoins, the risk of sustained negative premiums far outweighs that of sustained positive premiums.

Price Fluctuation of Decentralized Stablecoins Source: Footprint Analytics

This is a very tricky issue for any stablecoin project. Therefore, the existence of Amara's long-tail lending market will provide substantial demand for stablecoin issuers. For users borrowing stablecoins on the Amara platform, they can mitigate risks by exchanging for mainstream stablecoins like USDT in real-time.

As mentioned earlier, the risk of negative premiums for algorithmic stablecoins is far greater than that of positive premiums. Additionally, if a negative premium occurs for algorithmic stablecoins, users who have deposited LPs can also arbitrage through market repurchases, and negative premiums will not increase the risk of liquidation; instead, they will reduce the debt ratio.

For example, suppose Steve holds $100 MARA-USDT LP, which originally could only yield 100% APY through liquidity mining. Now, he can deposit the LP into the Amara platform to earn a compounded annual return of 120% while borrowing $50 of algorithmic stablecoins.

Taking UST as an example, after borrowing, Steve can exchange UST for other tokens for investment or swap it for USDT to avoid risks. If UST's price drops to $0.94, he can repurchase UST for $47 and repay all debts, thus making a profit of 6%.

Amara targets the long-tail liquidity and algorithmic stablecoin market, aiming to improve the utilization of long-tail assets while providing application scenarios for stablecoins. In the future, it will collaborate with more algorithmic stablecoin projects to jointly promote the development of the stablecoin market.