In-depth study: Will UST collapse?

Will Terra be the trigger for the next financial crisis in blockchain? Can the financial building's dampers withstand the impending tidal wave of liquidation? Whether the building will collapse or not, we shall see.

Will Terra be the trigger for the next financial crisis in blockchain? Can the financial building's dampers withstand the impending tidal wave of liquidation? Whether the building will collapse or not, we shall see.Author: CYC Labs

We talk about the Terra collapse every day because we remain skeptical about its "left foot stepping on the right foot" economic model. However, if we focus on the relationship between its two core components, namely the relationship between LUNA and UST and the breadth of utility, how likely is this collapse? Or even if a collapse occurs, will there be mechanisms to correct it? Therefore, today we will look at whether Terra is heading towards extinction from this perspective.

The Foundation of the Terra Empire: Anchor

First, let's take a look at the situation of Terra itself. If we consider Terra as the Federal Reserve, then UST is the dollar, and LUNA serves part of the role of reserve gold (of course, LUNA is different from gold. Here, we are just saying that its role as a store of value is similar. But don't forget, the value of LUNA itself is also supported by the utility of UST). So, we should first look at the current supply of both. According to the information provided by the Terra dashboard, the latest data is as follows:

If you remember what was said about the Terra chain before, you should recall that the official total issuance of UST is 10 billion. If calculated at the price of USD, this total supply should indeed be around 10 billion. The reason for the over-issuance is unknown for now, but we can temporarily assume that the current demand for UST has exceeded the previous setting. Previously, we also discussed the PVC mechanism between UST and LUNA, which means that the over-issuance of UST will drive up the price of LUNA, thus entering a virtuous upward spiral. Everything seems to be going well, but let's take a look at what the real utility of UST is like now.

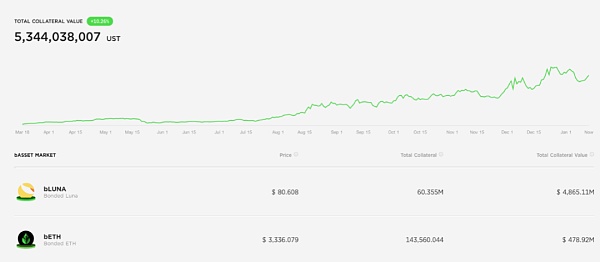

At this point, we need to look at the application that is the lifeblood of Terra—Anchor. Why look at it? Because currently, the total amount of UST is 10.54 billion, and the TVL on Anchor, when priced in UST, is:

Among them, the UST staked for borrowing is 5,572,388,550. This means that over 50% of the UST in circulation is directly in Anchor. If all the assets on the platform are backed by UST, then over 98% of UST is in Anchor. Alright, let's remember this proportion for now. Next, let's look at other applications. At this point, we should turn our attention to the recently popular Abracadabra.

The Wizard of Terra: Abracadabra

First, let's take a look at the current UST locking situation on Abracadabra:

Of course, if you have a bit of understanding of this project, you would know that UST is thriving on Abracadabra and is related to the recent Degenbox (released on November 3, 2021). Initially, I only wanted to talk about Degenbox, but if I only discuss that, it might be hard for everyone to understand. So, let's quickly go over the project itself.

The Wizard's Magical Wand: Leveraged Yield

First, we understand that Abracadabra is very similar to Alchemix. Nominally a lending protocol, it essentially issues its own MIM token by releasing token liquidity. We can skip the other details, but there is an interesting feature called "Leveraged Yield Position." The entire process can be illustrated in the following diagram:

The official process is as follows:

To explain this more clearly, let's take a user who wants to utilize their yvUSDT position as an example:

Step 1 and 2: The user selects the desired leverage, obtains yvUSDT, and deposits it as collateral.

Step 3: Based on the selected leverage, the protocol borrows the corresponding amount of MIM.

Step 4: These MIM will be exchanged for USDT (the current price peg and slippage play an important role here).

Step 5: These USDT will be deposited into the Yearn Vault to obtain yvUSDT.

Step 6: These yvUSDT tokens will be deposited back into Abracadabra to serve as collateral for the user's position.

It may seem like there are many steps, but to summarize it in one sentence: You provide the collateral they require, and they won't give you MIM directly, but rather provide you with farming yields based on the leverage you set (up to 10x), such as the corresponding Yearn yield.

Now, let's get to the main topic, Degenbox.

Degenbox

There are only a few steps here. In summary, users can stake UST to obtain MIM. However, Abracadabra's profits come from Anchor. To be more specific, the protocol will cross-chain 85% of the user's staked amount to Terra to stake in Anchor (through EthAnchor), and then cross-chain the staking proof aUST back to Degenbox for staking, increasing the value of the user's collateral assets.

Additionally, leveraged yield positions also apply to Degenbox. This point is very important. It should also be noted that this leveraged yield position does not mean that if you have 100 dollars, you can obtain 1000 dollars worth of collateral yield, but rather that you need to deduct slippage, borrowing fees, and other loss costs, as follows:

So, in summary, if the slippage setting is 1%, choosing 90% of the TVL with 10x leverage can yield 6.7 times your original cost.

This means that this feature allows me to profit from nested strategies in Yearn. Stake 100 ETH to obtain 100 yvWETH, then stake yvWETH in Abracadabra to open 90% TVL with 10x leverage to obtain 6.7 times the Yearn ETH yield. Using the latest Yearn ETH rate (1.18%) and Abracadabra's yvWETH borrowing rate (0), let's calculate what the yield would be:

Total yield = Ryearn ETH x 0.9 x 1.18% x 6.7 - 0 = 7.1154, while the yield without leverage would be: 1.062, which is a significant difference.

However, high yield comes with high risk. Leveraged yield positions do not directly give you MIM, and once liquidation occurs, you will not own any tokens.

The mechanism of Abracadabra has been discussed, and we can now look at how it integrates with UST. Since both UST and MIM are stablecoins, the liquidity scenario should undoubtedly look at the MIM-UST pool on Curve:

Currently stabilized at 1 billion dollars. Assuming that the average data shows that the total collateral + borrowing amount on Anchor accounts for 90% of the entire UST supply, then the remaining 10% is basically all in the Abracadabra pool. This also indicates that these two protocols are crucial for the stability of Terra. Especially Anchor, where the vast majority of UST resides, and its promised fixed annual interest rate of 20%—if an accident occurs and UST decouples from USD, will a storm arise? This will be the key part I want to introduce today.

Warning of an Approaching Storm

Considering extreme situations, if Anchor has problems (after all, it is a P2P, and having such a high stablecoin APY could lead to a collapse), how will it affect UST and LUNA? This needs to start from the TVL structure of Anchor.

First, as mentioned above, users can stake UST with Anchor and receive an APY of around 20% (which will fluctuate, but on average is 20%), this part of the money is what was mentioned earlier, approximately 5 billion; the remaining 5 billion is the collateral of borrowers, mostly composed of LUNA, with the remaining part being ETH. The distribution is as follows:

At this point, we need to see how Anchor can pay back the 20% APY to its users. Generally, we can think of the simplest way for P2P to profit, which is to have borrowers pay an APY higher than 20%. However, if the interest rate is really that high, I don't think many people would be willing to borrow money from Anchor. This can be seen from its loan rates:

As we can see, the latest loan rate is only 2.3% (the actual loan rate is Distribution APR - Borrow APR. D APR is the loan's ANC reward rate). Even if we consider a Borrow APR of 15.76, it still cannot cover the required 20% annual interest rate. So, there must be other solutions to improve repayment capability. At this point, we can turn our attention to the collateral of the loan users—LUNA and ETH.

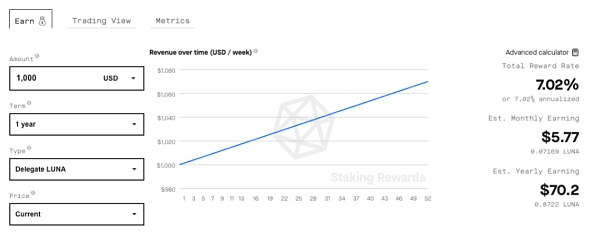

According to official statements, the collateral LUNA will be staked on the Terra mainnet to earn an annual interest rate, while ETH will be staked on Lido to earn a rate. The current rates for these two are as follows:

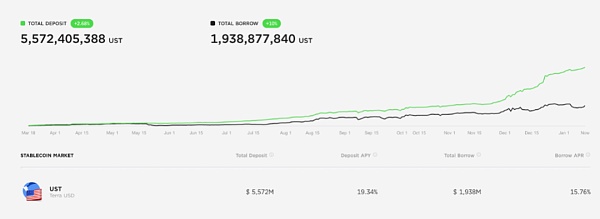

Assuming we compare the expected APY repayment amount from the current Anchor staking amount with these profit outputs, we can easily find that the current profit output cannot cover the interest. Of course, before that, we need to look at the comparison of the borrowing amount on Anchor:

As we can see, the amount lent to the protocol far exceeds the amount borrowed, and even if calculated at a borrow rate of 15%, it is still far from enough to cover deposit interest. Let's calculate directly.

Using the latest staking UST rate of 19.34%, the amount Anchor needs to repay annually is:

5572m x 19.34% ≈ 1077.62m

And according to the current rates, the annual profit output is:

Luna: 4865.11m x 7.02% ≈ 341.53m

ETH: 478.92m x 4.7% ≈ 22.51m

Borrow: 1938.87m x 15.76% ≈ 305.56m

Total income: LUNA + ETH + BORROW = 669.6m

Well, it turns out that Anchor seems to be operating at a loss. This can be seen from the daily income changes of the protocol:

However, if I closely observe the deposits above, I will find that borrowers far outnumber lenders, which has occurred recently. What happened is not the main point. Now, let's think about a question: Anchor is not foolish; how should it respond to this situation?

The simplest idea is: reduce the fixed APY of 20%.

However, this raises another question: over half of the circulating UST is in Anchor, and what attracted users is its 20% stablecoin APY. If this APY is reduced, will it have a significant impact on the stability of UST? Coupled with the fact that UST-MIM is now a large pool, will it further affect the stability of MIM or even other stablecoin pools on Curve? In summary, this is an upgrade to the question we posed at the beginning: If Anchor's interest rate is significantly reduced, what will happen to UST?

Will the building collapse, or will it remain intact?

Once the Anchor interest rate is significantly reduced, we can make some assumptions. Typically, these assumptions can be divided into optimistic, normal, and pessimistic scenarios. Let's look at them one by one.

First, let's look at the optimistic scenario: Suppose this situation occurs, but the market still considers UST to be a low-risk asset. Even if the interest rate decreases, people are still willing to believe in the stability of UST. Therefore, in this case, there will be no substantial impact on UST.

Next, let's consider the normal scenario: The market is relatively stable, but market participants are profit-driven. This means that everyone has a threshold in mind. Once the Anchor interest rate falls below this threshold, it will stimulate the market to take some action. Let's assume this threshold is 10%. Once the deposit APY falls below 10%, people will withdraw their staked UST, leading to a decrease in the amount of UST staked in the pool, which will further cause borrow interest to rise rapidly, in turn stimulating deposit APY to climb, attracting people to stake UST again, creating a cycle. This is a phenomenon we often see and is the most likely scenario to occur under normal market conditions.

Finally, let's look at the situation we are most curious about, which is the pessimistic scenario: The premise of this situation is that the market considers UST to be a high-risk asset: Once Anchor's interest rate falls below their psychological threshold, it will cause panic, and a large amount of staked UST will be withdrawn, and this withdrawn UST will be the most unstable factor.

Where will these unstable UST go? Well, liquidation arbitrage bots will go crazy. Let's look at a few scenarios:

Hold UST: **You believe? I just think UST is risky, how could I hold it.

Sell UST for other stablecoins: This will undoubtedly lead to UST decoupling (regardless of the duration):

It will affect Curve and Abracadabra's Degenbox. But how much impact it will have will be detailed later.

It will put selling pressure on LUNA. With too much UST in the market, the protocol needs to use LUNA to buy back UST, affecting the price of LUNA.

- I manually redeem LUNA with UST for arbitrage: Those who understand the Terra mechanism are likely to take this action. Redeem LUNA with UST, then sell LUNA on the open market. This will again split into two situations:

The depth of LUNA in the open market is good, and centralized exchanges can absorb this volatility (it won't trigger protocol mechanisms).

It can't hold. As more LUNA enters the open market, the protocol will use UST to buy back LUNA, creating a cycle that leads to a death spiral (UST severely decouples). According to 0xHamZ's modeling calculations (based on 519), it is as follows:

Now, let's look at the impact on Curve and MIM.

Where will the domino effect stop?

We know that vampire attacks are very famous, but there is another type of attack that has recently gained popularity, known as the Viking Attack. This refers to Degenbox's siphoning of Anchor. In our assumed pessimistic scenario, if Anchor's interest rate decreases, leading to UST decoupling from the dollar, it also means decoupling from MIM, and it will affect the 3CRV pool. However, due to the existence of Curve, once decoupling occurs, a large number of arbitrage bots will go crazy to arbitrage, gradually bringing this peg back. This can be seen from the historical records of the MIM-UST or UST-3CRV pools on Curve.

However, we need to delve deeper into the specifics:

Once a large amount of UST floods into the market, it means that UST will become cheaper, and a large amount of UST will be converted into MIM or 3CRV. At the same time, Degenbox will initiate liquidations, turning a large amount of UST into MIM, which will again lead to selling pressure on LUNA… What will the final situation be? Borrowing the analysis of another big player, Naga King:

"Currently, the MIM-UST pool has a volume of 1 billion, of which 950 million MIM is backed by UST. If this 95% UST is withdrawn and traded for MIM in this pool, it will lead to over 90% UST in the composition of this pool, predicted to be 93%."

Of course, Degenbox has also considered this, so it proposed a fault tolerance measure: If a large-scale withdrawal of UST from Degenbox occurs, once the total amount withdrawn exceeds 10% of the total amount in the Degenbox pool, withdrawals will be restricted. Until UST is withdrawn from Anchor back to the mainnet. This may take several hours. Usually, during this process, market arbitrageurs will play a role in bringing the price back to normal levels. Of course, this is all under the condition that consensus is not completely lost; otherwise, arbitrageurs would not arbitrage something of no value.

Why not mention the 3CRV pool? The most important reason is that the UST-3CRV pool can still absorb the volume, relatively speaking, Curve can handle this volatility, so the impact on Curve is not significant.

Conclusion

Through UST, we can see that the stability of the stablecoin relies more on the arbitrage mechanisms designed within it. However, once consensus is broken or extreme market conditions arise, it could all be gone in one wave, especially when it becomes so extreme that arbitrageurs no longer want to arbitrage; it becomes meaningless to discuss anything. This also proves once again that things like Terra, which involve infinite nesting, can profit effectively in any era. Ultimately, will Terra be the trigger for the next financial crisis in blockchain? Will the financial building's dampers withstand the impending storm of liquidations? Whether the building will collapse or remain intact, we will wait and see.