From the perspectives of macroeconomics, the Bitcoin blockchain, and derivatives, how will the market move next?

Will there be more adverse factors? Perhaps, especially if the stock market continues to decline and spreads impact the credit market.

Will there be more adverse factors? Perhaps, especially if the stock market continues to decline and spreads impact the credit market.Author: Dylan LeClair

*Compiled by: * Kyle, DeFi Dao

Bitcoin is at $35,000. How did we get here, and what happens next? This article introduces some analyses from macro, on-chain Bitcoin, and derivatives perspectives.

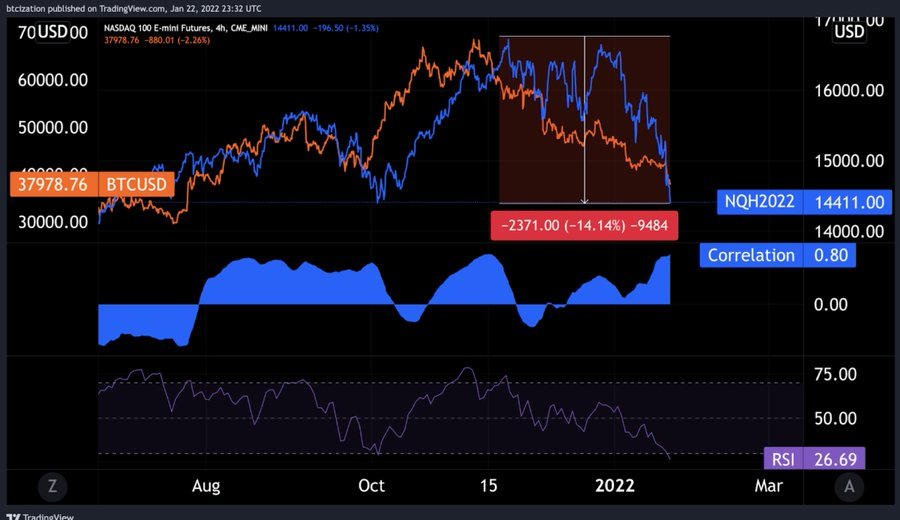

The community discussion topic has recently been the correlation between BTC and the Nasdaq (as well as other types of risk assets) over the recent period. Currently, the Nasdaq index has fallen 14% from its peak since March 2020 and its most oversold level. The drop is significant.

BTC - Nasdaq 30-day correlation is 0.80

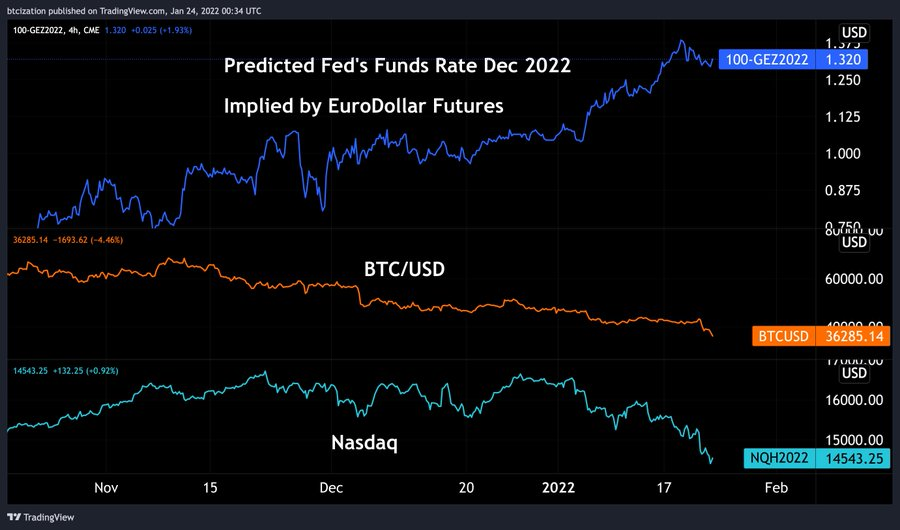

Eurodollar futures represent the expected federal funds rate market, which currently anticipates four rate hikes by December 2022.

When expectations of loose monetary policy tighten, the market reacts.

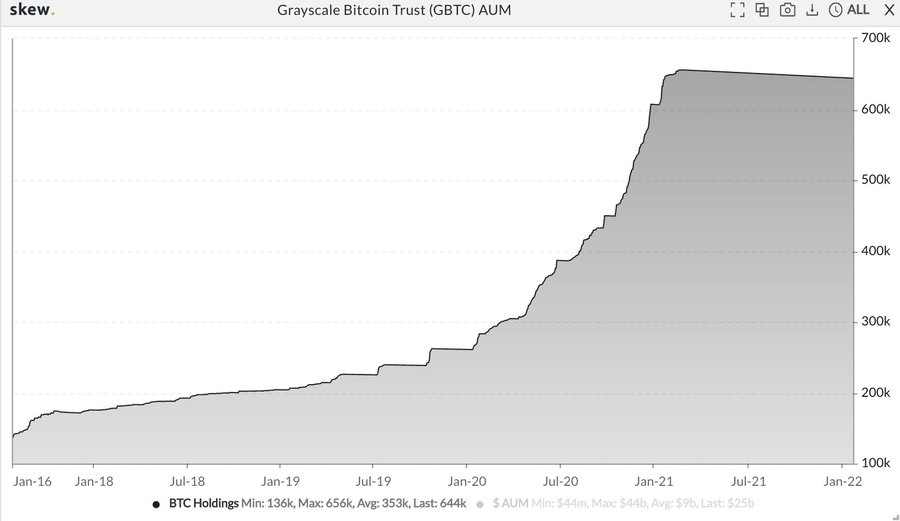

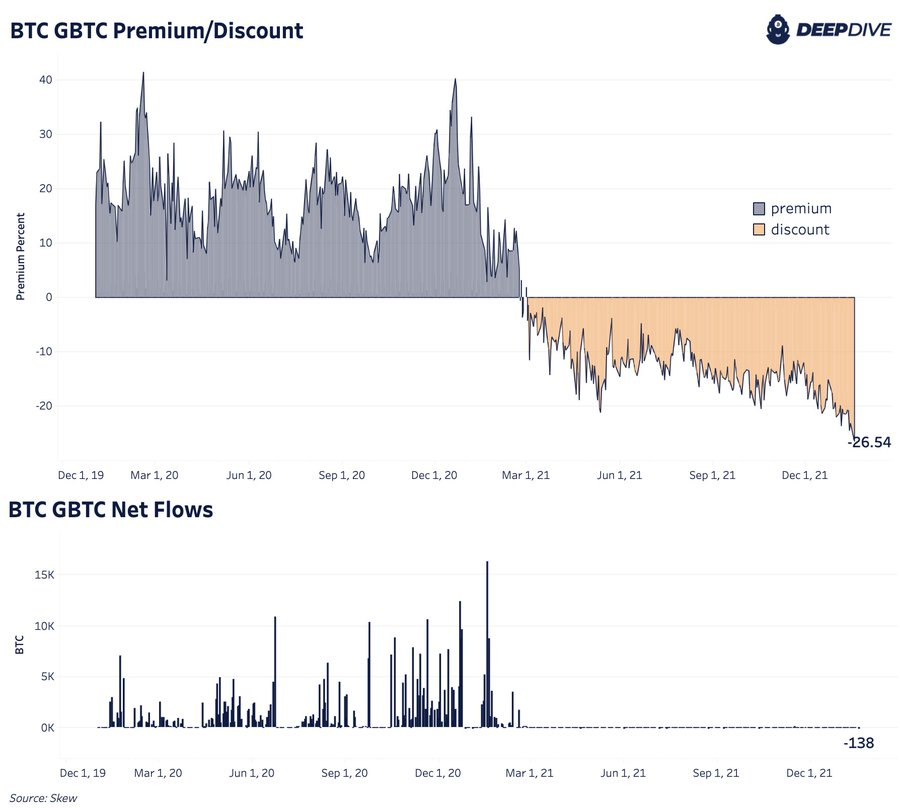

The increasing adoption of BTC by macro funds in 2020-21 has made BTC's behavior increasingly resemble that of a correlated risk asset. We can look at Grayscale's performance. Grayscale was a driving force in the early stages of the bull market, representing accredited investors and institutions exchanging 400,000 BTC for $GBTC shares.

Traders hoped to buy GBTC shares from Grayscale at NAV through "risk-free" trades (with a lock-up period of 6 months) and arbitrage the "risk-free" trades marked at a premium. They began to realize that the arbitrage was broken when the shares started trading below NAV in February.

However, it is important to remember that 650,000 BTC still exists and is traded in the over-the-counter market in the form of $GBTC shares. As the premium turns into a discount, inflows stop, and incentives for investors to allocate to $GBTC instead of $BTC itself emerge.

With market risks receding, there has been a relentless sell-off of $GBTC recently, with the discount to NAV widening to a historic low, which makes sense considering the situation of many trust holders: they are the same group of macro investors allocated to BTC in 2020-2021.

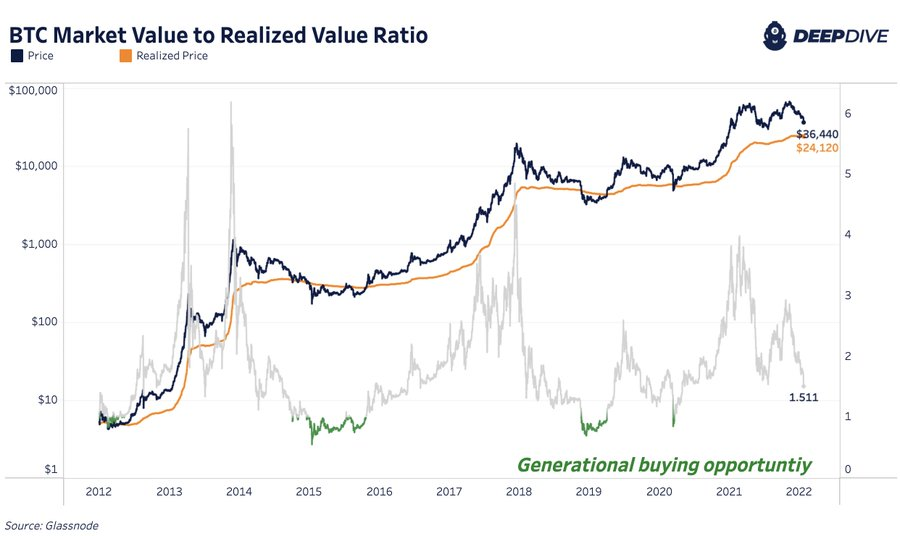

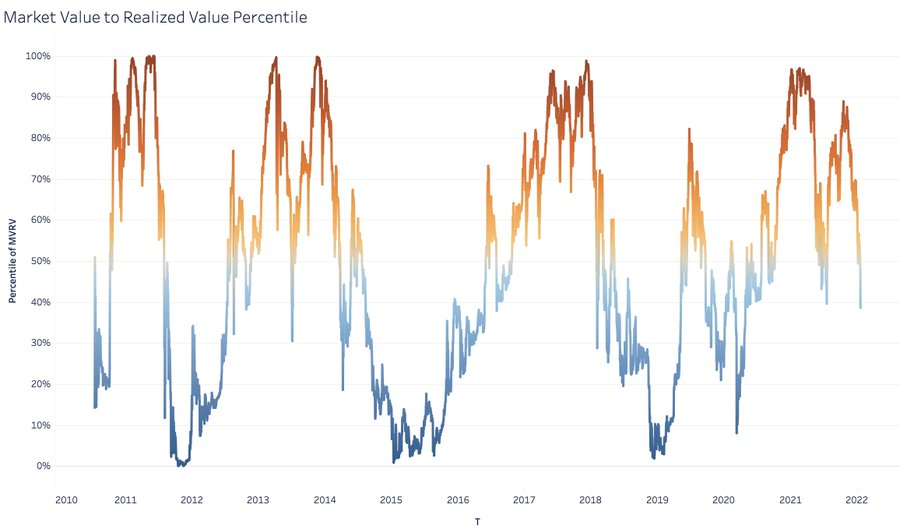

Now let's look at where $BTC trades relative to historical valuations. The current on-chain cost basis of the network is $24,000. The ratio of cost basis to price; that is, the MVRV ratio, shows Bitcoin's historical boom/bust cycles. The current MVRV is about 1.5.

The current MVRV ratio is at the 38th percentile of historical records. In the past, when $BTC dropped below its actual price (MVRV below 1.0), it has become a generational buying opportunity. Everyone can speculate that if we drop to $24,000, it would certainly be very attractive for buying.

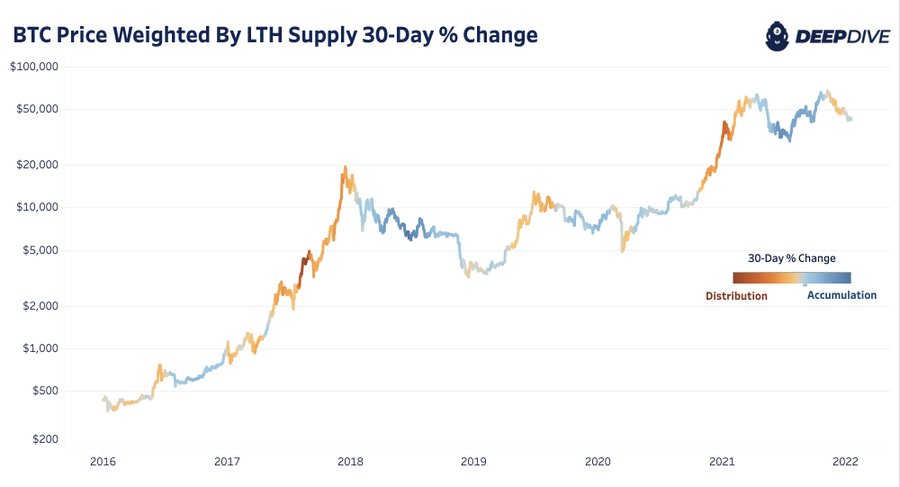

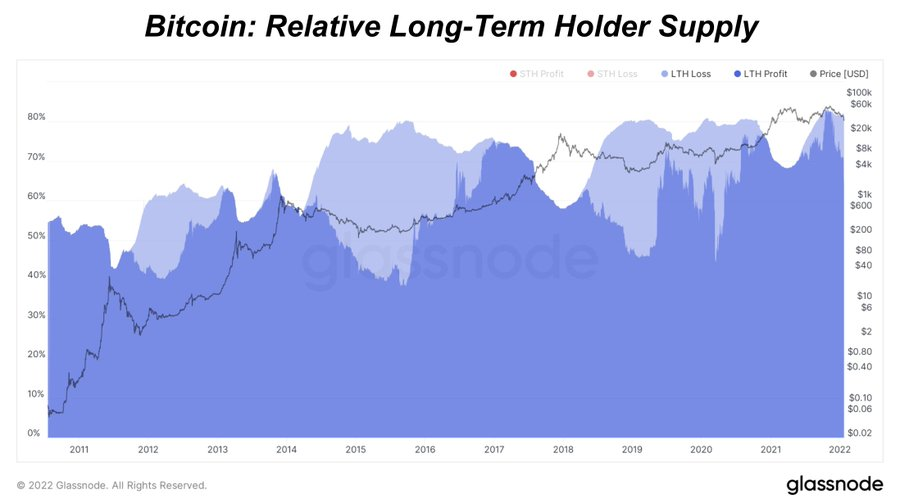

We also see long-term holders distributing during the downturn over the past few months, which is a peculiar phenomenon historically.

LTHs typically accumulate during bear markets and consolidation periods and distribute during uptrends; macro concerns have played a role.

Accumulation has now begun again.

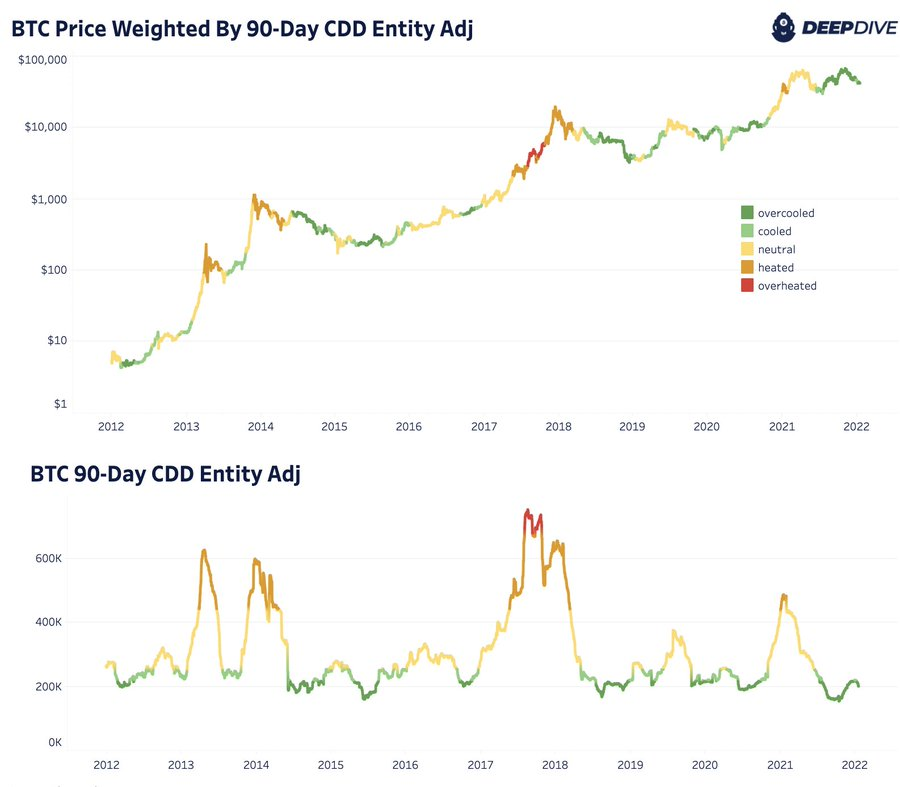

The number of coin days destroyed (CDD) is calculated by multiplying the number of coins in a transaction by the number of days since those coins were last used.

The 90-day rolling accumulation of CDD shows relative accumulation/distribution. Currently, accumulation is strong.

How is $BTC performing in derivatives?

There are a few points to note:

Perpetual futures

Quarterly contracts

Types of collateral used to enter derivative contracts

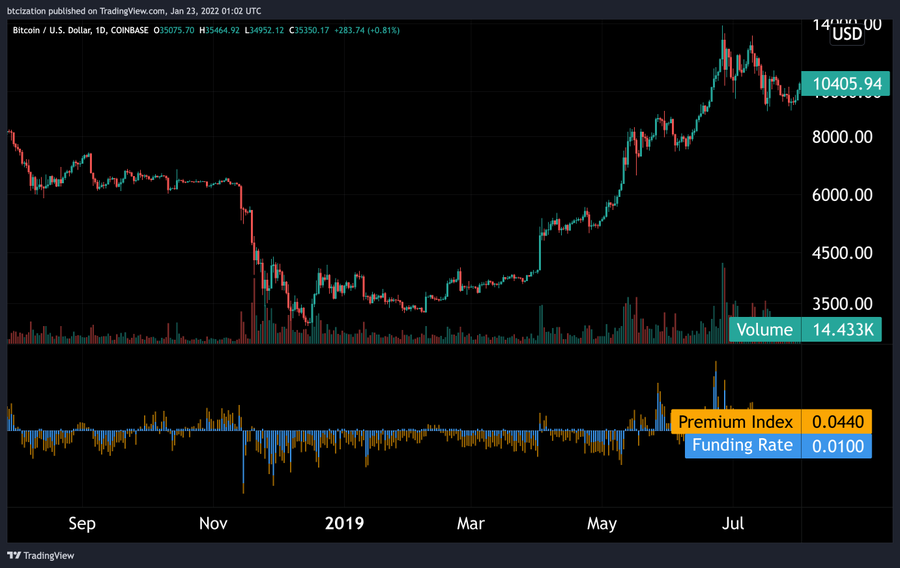

Perpetual futures funding shows whether derivatives are leading/lagging the spot $BTC price. Speculative longs are no longer dominant, but shorts are not overly aggressive either. A bottom is typically characterized by a sustained negative funding rate; derivatives shorts become overly greedy.

For example, this was the bottom of the 2018-19 market when shorts found themselves aggressively shorting the $3,000 bottom after an 85% drawdown.

This data comes from the major derivatives exchange BitMEX at the time, similar stories emerged after the COVID crash and last summer.

From a quarterly perspective, the correlation between price and futures basis has been close to 1:1 since last summer.

The conclusion is that existing derivatives traders have been driving the market.

0% or negative basis should signal market capitulation.

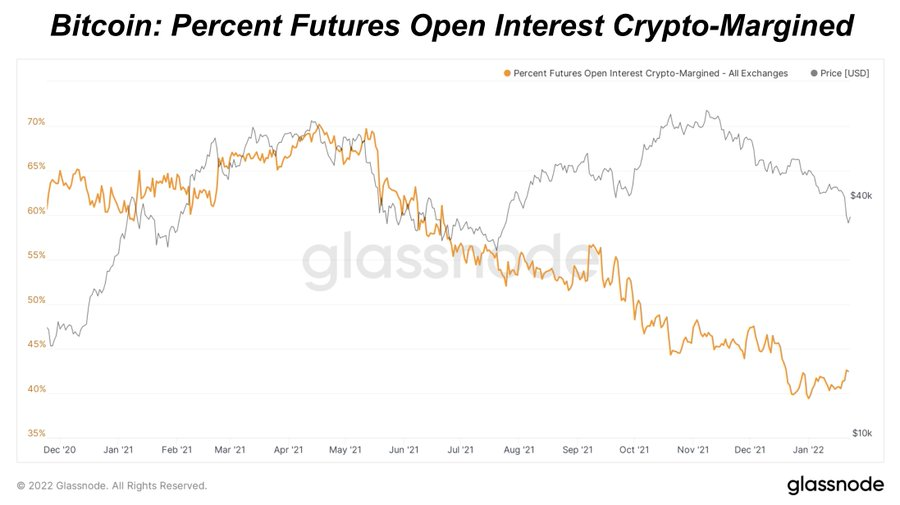

The use of crypto collateral for dollar-denominated BTC futures continues to decline long-term, which is a positive development, as stablecoins do not have the convex relationship that BTC margin futures have during market downturns.

Since the beginning of 2021, the dollar DXY, which measures the value of the dollar against other fiat currencies, has been on an upward trend.

As the Federal Reserve attempts to tighten, focusing on the strengthening dollar will be key.

A rapidly strengthening dollar will disrupt all assets (see March 2020).

As for when the bull market will return, conditions are relatively mature, with about 81% of the supply held by long-term holders, but supply is only one side of this equation.

A bull market recovery requires strong spot demand (not derivative speculation).

The question is, when will the marginal selling by macro funds turn into marginal buying? The reality is that there are trillions of dollars in bonds with negative real yields------when the Federal Reserve changes its tightening policy, expect $BTC to take off.

In the long-term debt cycle, the endgame of the economy is binary.

In a true deflationary scenario, there is infinite counterparty risk as the fiat debt unwinds throughout the economic system.

Will there be more headwinds? Maybe, especially if the stock market continues to decline and spreads impact the credit market.

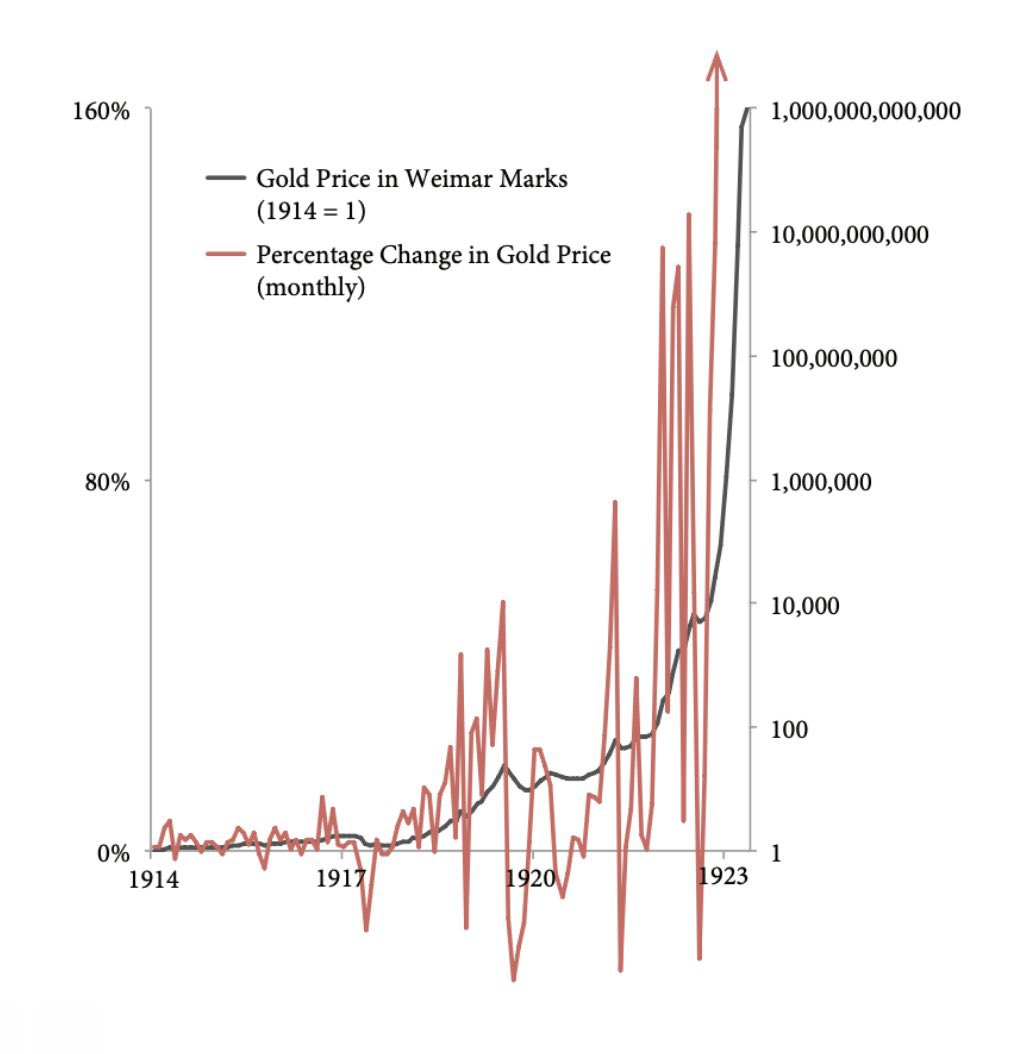

If you are a leveraged gold holder in Weimar, you will be wiped out multiple times.

Is America Weimar gold? No, but there is a lesson here.

"You often see the chart of gold priced in paper currency in Weimar Germany parabolically rising. What the chart does not show is the sharp declines and volatility that occurred during hyperinflation. Speculative activities using leverage were repeatedly punished."

As a capital allocator, your goal is to maintain and increase your purchasing power over time. The mechanics of $BTC almost guarantee that marginal production costs will continue to rise indefinitely.

Ultimately, for over 95% of people, the best strategy is to passively allocate to $BTC and then lay flat. Volatility is indeed your opportunity, and fortunately, volatility does not seem to be disappearing anytime soon.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles