The DeFi structured options market is experiencing an explosion, and Messari helps you understand the current market situation and key players

Compared to the broader DeFi ecosystem, the adoption of options-based protocols has begun to change rapidly as the options protocol in the fourth quarter attracted a higher TVL growth rate.

Compared to the broader DeFi ecosystem, the adoption of options-based protocols has begun to change rapidly as the options protocol in the fourth quarter attracted a higher TVL growth rate.Author: Dustin Teander

Original Title: 《Overview of Options Vaults》

Compiled by: Gu Yu

2022 was a hot start. In the first week of this year, the total market cap of cryptocurrencies fell by -11%. The top 100 DeFi tokens dropped even more, at -12%. However, there is one sub-industry within DeFi that performed exceptionally well in 2022—options. Options protocols not only did not decline but significantly outperformed the broader market, with a total market cap increase of 66% at the beginning of the year.

What a way to welcome the new year.

So far this year, part of the reason options protocols have been able to significantly outperform the crypto market is related to their starting point. Compared to other DeFi protocols, options protocols are relatively low in price. For example, Ribbon Finance had a circulating market cap of less than $100 million at the end of this quarter, with a price-to-sales ratio of 2x. In contrast, the circulating market cap to sales ratio for Uniswap, Yearn, and other companies is about 4x. The price disparity compared to other DeFi sectors is largely due to the relatively slow adoption of on-chain options.

However, the initial slow adoption has given way to strong growth. By the fourth quarter, the TVL growth rate of options protocols significantly outpaced that of the broader DeFi.

In December, the TVL of options protocols grew by 86%, while the overall DeFi TVL actually contracted by -1.5%. Throughout the quarter, options protocols expanded their TVL by 412%, while DeFi TVL grew by 278%.

The relatively strong growth of options protocols still falls far short of adoption levels compared to traditional finance. It is an understatement to say that options represent a huge market in traditional finance. Options play a crucial role in modern finance, used by market makers, hedge funds, and even retail traders. Amplifying the retail options trading market, Robinhood reported that 45% of its revenue in the third quarter came from options trading on its platform.

It turns out that options are both popular and profitable for Robinhood, whose user base is most similar to that of typical crypto users. Robinhood's approximately 19 million active users generate $656 million in annual revenue for the platform.

With such enormous profit potential and product consistency with retail traders, which protocols and ecosystems are leading the charge in capturing this market?

Let’s first break down the different types of protocols in the options space.

Overview of the Options Ecosystem

On-chain options protocols are primarily composed of two types of protocols: options markets and structured products. Markets are protocols that create actual options contracts and facilitate the buying and selling of options. The liquidity underwriting for each option traditionally comes from individual users writing options with deposited funds or from passive liquidity pools. Protocols like Opyn, PsyOptions, and Zeta Markets operate under a traditional order book style, while most other options market protocols, such as Dopex, Lyra, Premia, and Hegic, use a liquidity pool approach.

Structured product protocols sit above the options markets and provide users with vaults for depositing funds. Each vault executes defined option-based yield strategies, abstracting complex pricing and risk management away from users. This is similar to how Yearn executes yield farming strategies for money markets and exchanges under its vaults.

Selling covered call options or cash-secured put options are the most prominent structured product vaults in the industry. Covered call options generate yield for tokens by selling call options with a strike price above the current token price (out-of-the-money call options). Option buyers pay a premium for the options contract, which is directed back to the vault, increasing the yield for depositors. Cash-secured put options are similar but in the opposite direction. Stablecoins are deposited into the vault to underwrite put options for tokens with a strike price below the current value.

So far, structured product vaults have driven most of the on-chain options adoption. The original buying and selling of options at various strike prices have not attracted crypto users. Structured products eliminate all the complexities of underwriting options, pricing options, and strike prices, replacing them with simple deposits and earning from the vault.

Not only retail users are utilizing these structured options vaults. Many protocols are collaborating with structured options protocols for fund management and to create vaults for their token holders. Utilizing options vaults instead of typical collateral vaults for yield eliminates the need for token releases, effectively reducing the overall inflation and sell pressure of protocol tokens.

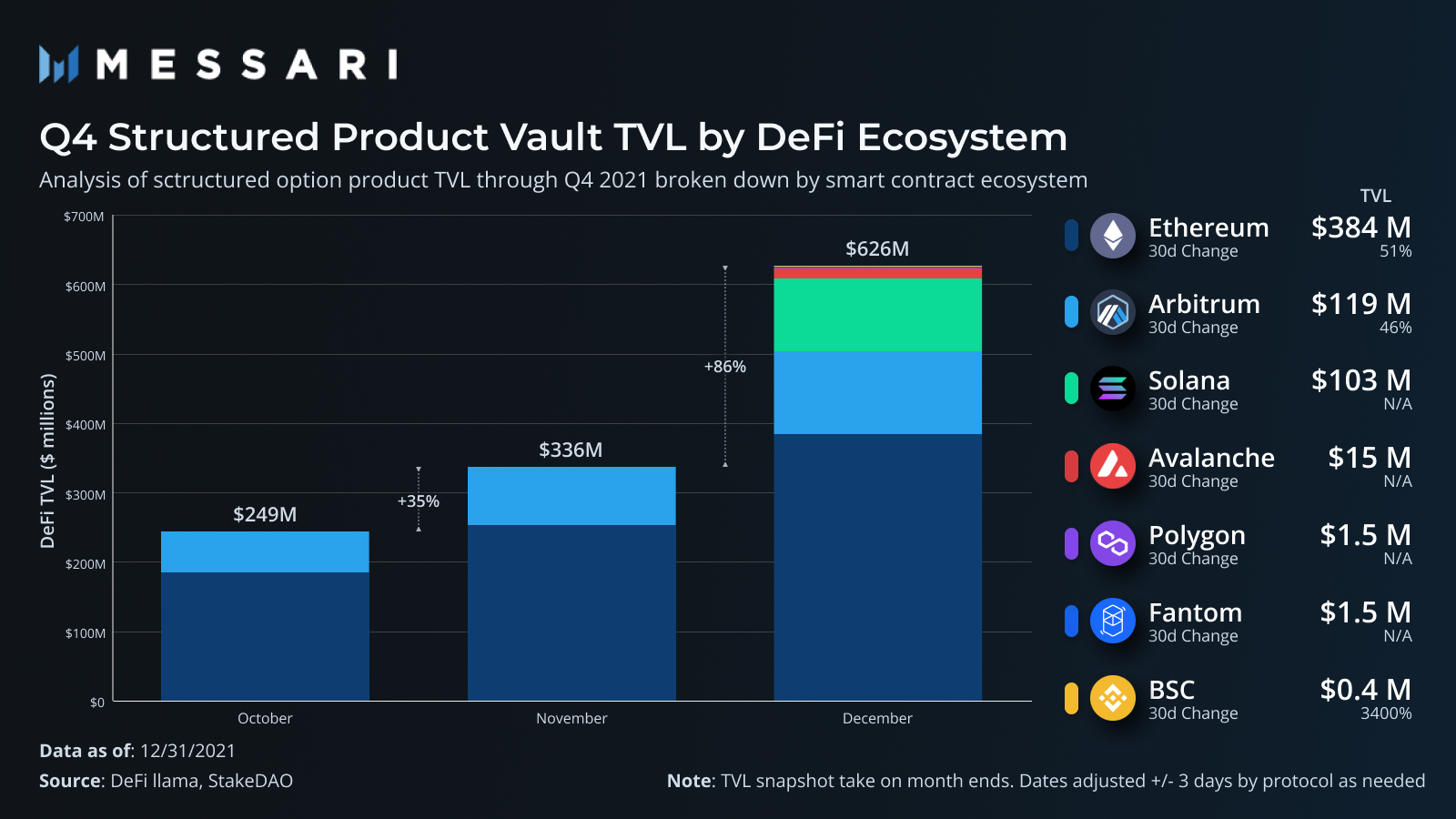

As structured product vaults drive most of the on-chain options adoption, let’s zoom in on these protocols to understand which smart contract ecosystems users are utilizing and which specific protocols are attracting the most usage.

Ecosystem TVL

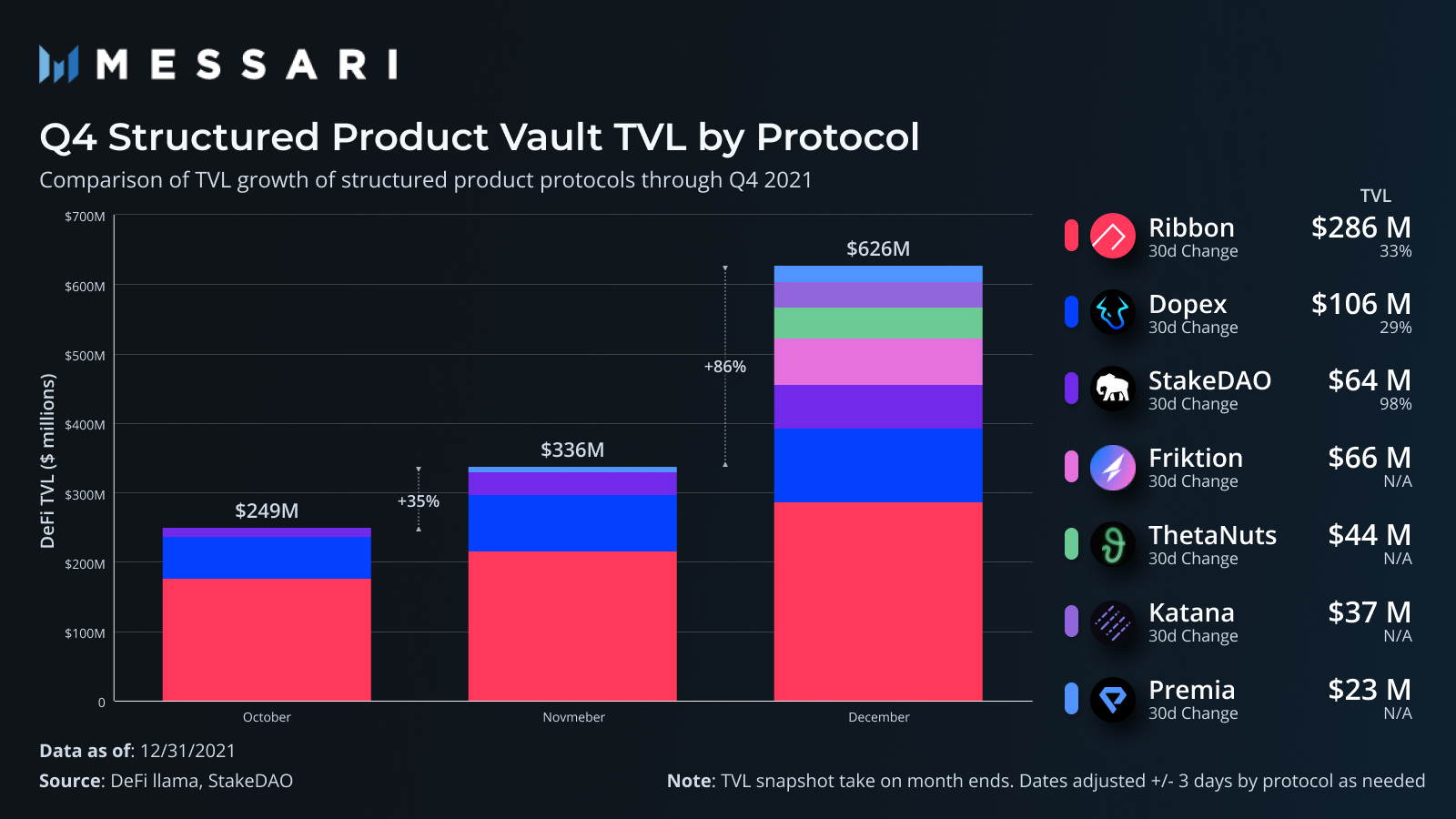

Of course, Ethereum has the largest TVL in structured products. It is home to Ribbon Finance, the first widely used structured product protocol. Ribbon popularized structured products in the crypto space and subsequently dominated the field until other protocols began launching in the fourth quarter.

Led by the rapidly rising Dopex, Arbitrum is the second-largest structured product ecosystem. Compared to L1 ($5 billion - $14.3 billion), Arbitrum's overall TVL ($1.7 billion) is significantly reduced, so having the second-highest TVL options indicates strong relative user consistency within the ecosystem. Dopex is currently the largest options protocol on the platform and is responsible for most of the growth. The price increase of its token has also driven the outstanding performance of the options industry this year (with a market cap increase of 85% from January 1 to January 9).

Solana launched two new protocols in December, both attracting significant funds within weeks of their launch. Friktion and Katana offer similar structured product vaults and support a wide range of assets. Compared to the 7 offered by Ribbon, 4 by Dopex, and 3 by StakeDAO, these two protocols provide a total of 14 different vaults.

Ribbon continues to dominate structured options with over half of the TVL. After starting the quarter with nearly all of the industry's TVL, its market dominance is declining. This is not a reflection of Ribbon's growth status, which is impressive in itself, but rather highlights the rapid rise of other protocols in the industry during this quarter. Let’s delve into each and compare their nuances.

Ribbon

Ribbon Finance is a traditional structured product protocol that operates on top of Opyn's market. Each of Ribbon's 7 vaults utilizes deposited funds weekly to underwrite options on Opyn, then sells or auctions them, with the premiums collected returned as yield to the vault. In the fourth quarter, Ribbon generated over $11 million in underwriting fees for its vaults.

In September, the protocol released the V2 version of its vaults and has recently fully migrated all funds to V2. Like V1, V2 vaults execute options selling strategies weekly. The changes in V2 include decentralized vault exercise options, altering the fee structure, and enabling meta-vaults (fee-sharing for protocols building strategies on top of Ribbon vaults). The shift in fee structure from withdrawal fees to management and performance fees (2% and 20%) aligns the protocol's goals more closely with users and allows for more composable strategies on top of Ribbon.

Ribbon has been an innovative team in the space, being the first to launch yield products combined with Yearn's yvUSDC. Users' USDC collateral is not used to sell put options against regular USDC but is converted into yield-generating yvUSDC, enhancing the vault's excess yield status through earnings from borrowing demand in the ecosystem and option premium income. In addition to innovating on the types of products offered, Ribbon is also pushing an expansion strategy towards other public chains launched in December on Avalanche and has plans to implement on Solana.

Dopex

Dopex may have the most ambitious and creative roadmap among all the projects here, and while its current usage is not the highest, its valuation has soared to the highest circulating market cap among all options protocols. The way the protocol works is also quite unique. Dopex does not use deposits to underwrite options from another protocol but instead acquires liquidity and underwrites all options on the same protocol.

Its main product is SSOV (Single Staking Options Vaults), serving as a structured option. Each month, users can deposit funds into the vault and choose the strike prices at which they want to provide liquidity. After the deposit period ends, the funds are used to underwrite options at various strike prices, which other users can purchase during that period. This is a more refined covered call approach compared to the "one-and-done" vaults used by Ribbon, providing users with more control (at the cost of complexity). Currently, only four assets are supported for calls: DPX, rDPX, ETH, and gOHM.

Dopex's fees are not charged to vault depositors but to option buyers, marking a clear distinction from other protocols. A fee of 20 basis points is charged when purchasing options, with an additional 10 basis points for options that are in the money at the end of the epoch.

Dopex's creativity lies in its dual-token model (DPX and rDPX) and how it leverages its reward emissions. SSOV vaults earn DPX rewards as well as premiums, effectively combining a typical two-pool collateral vault with an options vault. On the roadmap, Dopex plans to implement the popular veDPX model, directing rewards to vaults based on the voting weight of locked DPX tokens. As the protocol continues to collaborate with Dopex to create SSOV vaults (OHM being the first), this model will become increasingly important as the protocol acquires DPX to incentivize liquidity for its pools. Theoretically, options vaults for rewards could become more popular as protocols seek to move away from yield formed by token reward releases (which lead to dilution and sell pressure) towards a more evergreen model focused on selling options on assets.

rDPX is Dopex's discount token, issued as compensation to option underwriters who lose capital at a rate of 30% during the period, offsetting the risk of providing capital. However, the planned utility of rDPX far exceeds that of a pure rebate token. Dopex plans to add synthetic assets to the platform and utilize rDPX as collateral to mint the stablecoin dpxUSD for use throughout the protocol. rDPX is undergoing an official restructuring, with token design details to be released later this month.

Beyond protocol design, Dopex has some interesting ideas on how to leverage options in DeFi. One point to note is the application of options to Curve gauge emissions. Instead of using options to speculate on the token price at expiration, options are used to understand changes in the Curve metric weights for CRV reward emissions. The so-called Curve wars revolve around the idea of controlling significant CRV to directly reward the AMM pools chosen by voters (which incentivizes liquidity in those pools). By offering options on the CRV reward rates provided by pools, users or protocols can indirectly benefit from CRV emissions without competing for veCRV votes.

StakeDAO

StakeDAO initially started as a yield aggregator similar to Yearn but has recently added structured product vaults to its product suite. While traditional yield aggregator vaults continue to account for a large portion of the protocol's TVL, its structured options vaults have seen strong growth in the fourth quarter, making it one of the largest protocols in the industry.

StakeDAO currently offers three vaults, all of which are similar in nature to Ribbon vaults. Both protocols utilize Opyn as the options market to collateralize their options. The main difference for StakeDAO lies in combining the yield from its yield aggregator vaults and options vaults. Assets deposited in the StakeDAO options vault are then automatically deposited into the corresponding passive yield vault on the platform to generate additional yield.

StakeDAO's uniqueness also lies in its use of Frax as a stablecoin to underwrite its short vaults. In addition to option premiums and yield generated from StakeDAO's passive Frax vault, users can also stake their LP tokens on Frax for additional yield.

StakeDAO's fee structure also differs from Ribbon. While Ribbon has shifted to a management and performance fee model, StakeDAO currently does not charge platform fees on assets or profits but instead charges a 50 basis point withdrawal fee from the vault.

Friktion

Friktion launched in mid-December and is the largest structured product protocol on Solana, with over $90 million in TVL. The TVL has increased nearly 50% since the beginning of the year, up from $66 million at the end of last year. This represents a growth profile of approximately $30 million in new TVL every 15 days. It operates under a traditional structured product architecture similar to Ribbon. Options are underwritten across various platforms and sold weekly or bi-weekly.

Driving its growth is its impressive ability to add new markets. Friktion has 14 live options vaults and supports a more diverse range of assets than typically EVM-based protocols focused on ETH and BTC products. Friktion has vaults for assets such as Luna, FTT, SOL derivatives, and various Solana DeFi ecosystem tokens. Its ability to expand the available options is driven by its ability to sell options to off-chain market makers through channels RFQ (not limited to the collateral types of supported on-chain options markets, such as psyOptions).

ThetaNuts

ThetaNuts may have the most aggressive cross-chain strategy among all structured options protocols. ThetaNuts has been deployed on Ethereum, BSC, Avalanche, Polygon, Fantom, Boba, Aurora, and more. While it does not dominate any market, its advantage lies in being the first to launch on chains that currently have no other options protocols. Its cross-chain strategy has helped it achieve over $44 million in year-end TVL, most of which comes from its Ethereum deployment.

ThetaNuts currently does not charge fees on its vaults. It appears to adopt a similar off-chain options auction model, allowing it to offer its options assets as it is not limited to the on-chain supported collateral of options market protocols.

Katana

After winning the Solana Ignition hackathon earlier in 2021, Katana launched in mid-December and has developed into the second-largest structured options protocol on Solana, with a year-end TVL exceeding $37 million. It offers a set of products very similar to Friktion, with a total of 14 different vault strategies supporting similar assets such as Luna, FTT, Solana derivatives, and Solana DeFi tokens.

Katana is also actively seeking financial management partnerships with various DAOs. Injective and Katana recently announced a funding management partnership, where Katana will provide options vaults for INJ and support fund generation through option premiums. In addition to Injective, Katana has also announced various other partnerships with Solana-based protocols to enhance its capital deployment capabilities.

Premia

In terms of TVL, Premia is relatively small but has achieved an interesting DeFi-native options approach. Similar to Dopex, liquidity underwriting options comes from liquidity pools on the protocol. Users can deposit funds into the liquidity pool and earn yield as these funds are used to purchase options. Therefore, the premiums do not rely on on-chain options markets or off-chain buyers but depend on the demand for options on its protocol.

It currently offers 3 markets for its users and is deployed on Ethereum, Arbitrum, and BSC. However, the deployments on Ethereum and Arbitrum account for the majority of the TVL, with nearly half coming from each ecosystem. While the TVL numbers are relatively small, the platform has effectively generated fee income from its capital. Additionally, due to the lack of attention on the protocol, the trading prices of options often tend to be 10%-20% lower than similar products on protocols like Dopex.

Conclusion

As DeFi matures and the high yields generated from leveraged lending decline, options protocols have every reason to ramp up providing supernormal premiums with minimal risk. Especially as protocols begin to seek yield sources for token holders outside of token issuance, this will dilute and drive ongoing sell pressure on project tokens.

Compared to the broader DeFi landscape, the valuations of options protocols are quite modest, with many top options protocols having market caps below $100 million. As the adoption of options-based protocols begins to change rapidly with the higher TVL growth rates attracted by options protocols in the fourth quarter compared to the broader DeFi ecosystem.

It is crucial to closely monitor the level of on-chain options purchases. Robinhood's success in stock options has been driven by retail traders buying and selling options on its platform, while much of DeFi's adoption has simply been depositing into options strategy pools. This means that DeFi protocols are forced to seek buyers off-chain (often market makers) to obtain premium income. Protocols like Dopex, Lyra, and Premia are built on the premise of users directly buying and selling options on the protocol, so a shift in user behavior is critical if these platforms are to scale to significant valuations.