How does the liquidity management protocol Tokemak simultaneously address the issues of liquidity and impermanent loss?

Primitive is an extensible and efficient on-chain derivative tool solution without oracles.

Primitive is an extensible and efficient on-chain derivative tool solution without oracles.Author: Jasur, Chain Teahouse

1. Project Overview

Tokemak is an innovative DeFi liquidity management protocol designed to generate deep and sustainable liquidity for DeFi and future tokenized applications by allowing control over the flow of liquidity.

It can be seen as a decentralized market-making platform and a liquidity router that disaggregates traditional liquidity supply and market-making in DeFi.

Tokemak sits "above" decentralized exchanges, allowing control over the flow of liquidity and providing a simpler and cheaper way to provide and procure liquidity—enabling liquidity managers to vote on the liquidity pools for the tokens they desire.

The current state of DeFi consists of fragmented, unpredictable, and costly liquidity. Builders of new projects incur significant costs, and dual-token pools face the risk of liquidity depletion, while providing 1:1 paired liquidity can be expensive for individuals, with impermanent loss being a major risk.

Traditional market-making solutions are opaque, highly centralized, and costly for native DeFi builders.

Insufficient liquidity can lead to poor pricing and volatility, negatively impacting projects/DAOs seeking deep liquidity for their tokens due to slippage caused by trading prices.

Additionally, protocols interacting with other project tokens require reliable liquidity.

The emergence of Tokemak aims to address the aforementioned issues of costly liquidity, insufficient liquidity, and the risks of impermanent loss.

2. Core Features

Tokemak enables users to provide liquidity and control its direction.

It offers unique composability investment opportunities for new and existing token projects as well as DAOs, allowing for more strategic liquidity deployment, ownership, and control.

It provides exchanges with opportunities to enhance their liquidity and create deep liquidity for specific projects using PCA (Protocol Controlled Assets).

Specifically:

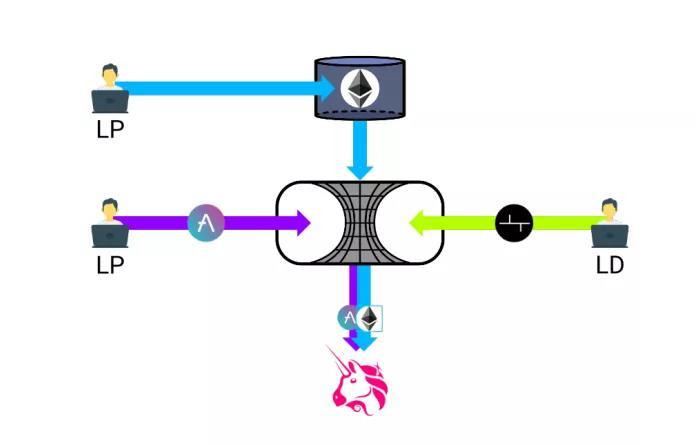

Liquidity Providers (LP):

Liquidity providers (LP) deposit single-sided assets into a single token reactor or genesis pool (including ETH, USDC) and earn returns in the form of TOKE (Tokemak's native protocol token).

Liquidity Directors (LD):

Liquidity Directors (LD) invest TOKE into various token reactors and vote on how liquidity is paired from the genesis pool and which exchanges it is directed to. They also earn returns in the form of TOKE.

TOKE Token:

TOKE can be seen as generalized or tokenized liquidity. By controlling and guiding Tokemak's TVL, TOKE holders can generate liquidity for any token they desire on any exchange they choose.

Tokemak Risk Control:

Tokemak has several different mechanisms and guardrails to reduce IL risk, ensuring that liquidity providers can always request their underlying assets at a 1:1 ratio. These mechanisms do pose some risks to TOKE stakeholders, but only as a last resort.

Tokemak Revenue Model:

The Tokemak protocol charges fees for providing liquidity across DeFi. Over time, this will allow Tokemak to build a strong reserve of various assets in Tokemak's PCA. Ultimately, the PCA is governed by TOKE holders through DAO governance.

3. Protocol Highlights

3.1. Addressing Impermanent Loss Faced by LPs

Tokemak allows liquidity providers (LP) to earn returns while avoiding the troubles of impermanent loss.

Liquidity providers deposit single-sided assets into a single token reactor and/or genesis pool (ETH, USDC) and earn returns in the form of TOKE (Tokemak's native protocol token).

Tokemak's method for achieving LP impermanent loss avoidance consists of two parts:

First, the Tokemak treasury covers the impermanent loss for LPs, effectively transferring the risk; second, it employs Guardrails to impose restrictions on the protocol.

· Covering with Treasury Reserves

When the net utilization of LPs is less than 100%, the system compensates for the missing portion of LPs by drawing from the treasury's asset reserves.

If the original treasury reserves are insufficient, the operational surplus and system revenue are pulled into the PCA by maintaining or increasing the asset projects listed in the treasury reserves:

If the treasury is sufficient, it directly uses treasury reserves to help LPs achieve full principal.

If method 1 is insufficient to cover the loss, the entire system's asset surplus and system revenue are counted into the PCA (treasury reserve assets) to further replenish the treasury asset reserves to cover the missing portion for LPs.

If both method 1 and method 2 are insufficient, the TOKE rewards allocated to the deficit reactor are included in the treasury reserve assets; if these rewards are insufficient, the staked TOKE will also be included.

As a final step, if the above steps are insufficient to make the user whole, the system will resort to using ETH and/or stablecoins from the reserves to complete the LP.

If there are not enough ETH or stablecoins available, high liquidity reserve assets will be sold externally for ETH or stablecoins.

· Setting Protocol Guardrails

Deploying guardrails imposes restrictions on the protocol, limiting the maximum amount of assets deployed per token reactor (asset pair) and deployment cycle.

This means that guardrail parameters need to be conservatively set so that reserves can cover up to 100% of relative exchange rate changes.

3.2. User Control Over Liquidity

Tokemak allows users to control the direction of liquidity through votes from liquidity managers (LD).

Users who lock TOKE (the platform token) will be eligible to vote.

Voting is tracked and calculated in contracts on Polygon. Users have two ways to submit votes:

3.3. Tokemak Provides Liquidity Solutions for Startups in Need of Liquidity

4. Target Customers

Users with liquidity seeking risk-adjusted returns (becoming LPs)

New protocols, tokens, or DAO organizations with liquidity needs (becoming LDs)

Exchanges looking to deepen market liquidity (becoming LDs)

5. Token Economics

5.1 Token Name:

TOKE

5.2 Total Supply:

100,000,000 TOKE

5.3 Use Cases:

Voting rights for liquidity governance, payment for LP and LD token rewards, DAO governance.

5.4 Distribution:

5,000,000 TOKE (5%):

Initial collateral for Cycle Zero, CoRE reactor collateral, first issuance of TOKE

9,000,000 TOKE (9%):

DAO reserves

16,500,000 TOKE (16.5%):

Contributors (12 months concentrated unlock + 12 months linear unlock)

14,000,000 TOKE (14%):

Team (12 months concentrated unlock + 12 months linear unlock)

17,000,000 TOKE (17%):

Investors (12 months concentrated unlock + 12 months linear unlock)

8,500,000 TOKE (8.5%):

DAOs & Market Makers (12 months concentrated unlock + 12 months linear unlock)

6. Team Introduction

● Carson Cook:

PhD in Physics, Master's in Electrical Engineering, previously worked in fintech at McKinsey, with experience in forex market trading. Carson began trading in the cryptocurrency market in 2017.

In early 2018, he founded Fractal, a DeFi market maker specializing in providing liquidity services for decentralized exchanges, which has been operating for over three years. The origins of Tokemak stem from Fractal's market-making experience.

● Bruno:

Previously worked at a Fortune 500 tech company, primarily responsible for designing Tokemak's token economic model.

● Craig:

Has years of experience leading business development and marketing for tech startups.

● Paul:

Responsible for design and community work.

7. Investors and Advisors

In April 2021, Tokemak completed a $4 million funding round led by Framework Ventures, with participation from Electric Capital, Coinbase Ventures, North Island Ventures, Delphi Ventures, and ConsenSys.

8. Conclusion

Tokemak is a very interesting protocol that uses users' money to earn money for others and then uses the profits to subsidize LP's impermanent losses.

On one hand, it addresses the liquidity needs of various project parties in the market, while on the other hand, it solves the impermanent loss problem for LPs.