Cryptocurrency VC Involution Record: A Never-Ending Hunger Game

A common development path in the crypto world is: printing money (issuing coins) — becoming a celebrity (gaining influence) — making investments.

A common development path in the crypto world is: printing money (issuing coins) — becoming a celebrity (gaining influence) — making investments.Written by: 0xmin

Crypto VCs Are Everywhere

Previously participating in blockchain week activities in Shanghai, my biggest impression is that crypto VCs are everywhere; it seems almost embarrassing to mingle in the circle without an investment title.

This is understandable; under the current policy environment, whether it's mining, exchanges, or project parties, they all fall under "politically incorrect" categories and must act low-key. Only crypto VCs can take the stage and showcase themselves. Additionally, this bull market has lasted long enough that some people have accumulated sufficient capital, and under the FOMO sentiment, fundraising has become easier. Moreover, the threshold for crypto VCs is incredibly low; both billions and millions of dollars can share the title of "Crypto Fund."

Exchanges, project parties, KOLs, communities, media… everyone is a VC.

1. Exchange-Related.

Each exchange either invests under its own name or establishes a separate capital brand. Some also act as LPs for other VCs; in short, they are not short on money.

For example, a certain exchange has Ventures, Labs, and Grants, all of which can make investments, and the internal competition starts from within.

There is also a new type of VC where exchange employees go out on their own to set up a fund while maintaining intricate ties with the exchange.

However, overall, the influence of exchange-related capital, except for top players like Binance Labs, is declining. Some top projects do not want to have too much contact with certain exchanges at the investment level from the start.

2. Project-Related.

A common development path in the crypto world is: printing money (issuing tokens) ------ becoming a celebrity (gaining influence) ------ making investments.

They earn their first bucket of gold from the project, then capitalize it, while also becoming a celebrity to enhance personal influence and gain more voice, either by setting up a fund independently or investing directly under the project's name.

Some project parties even raise a large sum of money and directly use it to establish a VC for investments, coincidentally hitting a good timing, making a fortune during the bull market, and then also profiting when the project goes live on exchanges, achieving dual benefits.

Additionally, various large projects (mainly public chains) are launching their own ecological funds, with amounts becoming increasingly exaggerated.

3. Outside the Circle.

In a bear market, crypto is a scam; in a bull market, crypto is a revolution. Under the attraction of the bull market, many traditional VCs and OLD MONEY are returning to the market, joining the internal competition with FOMO sentiment.

For instance, when Sequoia Capital leads the internal competition, other dollar funds have to follow suit, investing money and people, constantly exploring.

In comparison, Sequoia has already adjusted its fund structure, removing institutional barriers for direct investment in crypto, while most VCs still operate under traditional structures, only able to invest in large equity projects, with limited choices. More importantly, how to effectively use LP's money to invest in this highly volatile industry still lacks methodology and severely lacks talent.

Outside the stage, the participation level of outside big shots in the industry is far deeper than most people imagine. Funds with LP backgrounds from outside are springing up like mushrooms after rain, including large internet companies, listed companies, traditional gaming companies, financial firms, and even media groups… no one is against making money.

Of course, no one openly says they are investing in crypto; it’s not "elegant." Remember, the correct posture is, "We are investing in WEB3/metaverse/next-generation internet."

In fact, many elite-style traditional VCs secretly look down on crypto people, thinking they are just a bunch of scammers who got lucky (imagine Wang Xiaochuan's look at Sun Ge). This situation exists in every industry, but often the overlooked corners emerge with disruptive innovation, which is also the narrative of WEB3.0, a bottom-up transformation, where weakness and ignorance are not barriers to survival; arrogance is.

Crypto industry people also feel that traditional VCs are opportunists, running faster than anyone when the bear market comes, with Shen Nanpeng being just another Xu Xiaoping. (Poor Xu, who became a meme in the crypto industry for saying "the blockchain revolution has arrived" years ago.)

In short, everyone prefers Crypto Native rather than so-called elites and authorities.

When Sequoia Capital (Global) changed its profile (adding a DAO label) and tweeted "GM," everyone just felt a bit awkward, "like middle-aged people trying to fit into the younger crowd by using some internet slang." On December 9, Sequoia Capital (Global) changed its Twitter profile back to the original, a day known as "One Day Reform."

VC Dilemma: Rich but No Brand

When VCs are everywhere, internal competition is inevitable. Since everyone has plenty of money, the core issue is: Besides money, what else do you have?

The commodification of VCs is unavoidable, with everyone showcasing their unique skills to provide services. Some help introduce projects to exchanges; some invest tens of millions of dollars to help project parties increase TVL; some assist in writing articles, publishing, and building communities… effectively turning themselves into media and PR companies.

Now, many VCs like to tell a story (boast), saying, "I have deep incubation capabilities," which translates to, I can help projects do a few things (not limited to forming a group to introduce individuals, publishing an article…), in short, the standards for incubation are getting lower.

But in my view, for VCs, brand is the biggest and ultimate chip.

Having money but no brand is the dilemma many small and medium-sized crypto VCs currently face.

There is a consensus in the industry, which can also be seen as a bias, that truly high-quality projects are purely overseas projects. Therefore, at present, VC brand building overseas is particularly important.

Many capital sources will discriminate against "domestic projects," and some "domestic projects" will also discriminate against domestic capital.

For example, some domestic projects first secured large investments from overseas capital, immediately increasing their valuation by N times, then letting domestic capital take over; there are also domestic projects that first received domestic capital investments, then secured overseas capital investments, only to later want to fully refund or return half of the domestic capital's amount, "who told you your brand (prestige) level isn't enough?"

Thus, for VCs, a huge challenge lies in how to define and cultivate their core competitiveness beyond money? And how to build their global brand?

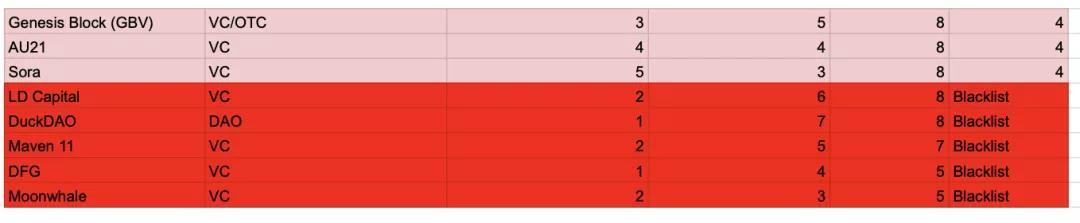

A case worth studying here is LD Capital.

Due to certain historical reasons, veterans in the circle generally hold a negative impression of LD, often associating it with "harvesting leeks." Previously, there was a viral VC ranking chart in the circle, said to be from the well-known community LobsterDAO, which listed LD Capital on the blacklist.

In this matter, LD is actually quite wronged.

The sequence of events is that the list has existed for a long time, with no one knowing its origin until someone posted it in the LobsterDAO Telegram community; defiprime shared it on Twitter, marking it as coming from LobsterDAO, and domestic media saw it and shared it back domestically, defining it as "the crypto VC ranking summarized by LobsterDAO," but later the community managers stated that the list had no connection to LobsterDAO.

As for whether to recognize this list, it is a very subjective matter.

I know many people in the industry look down on LD, thinking they are just following a spray-and-pray strategy, and even if they make money, it’s just luck… but putting aside biases and observing some of their layouts, there is still something to see, especially in the blockchain gaming sector, where they made a fortune this year, which can be considered a success.

Looking closely at their portfolio, some projects have quite exaggerated multiples, such as Illuvium, which cost $3 and peaked at $2000; Star Atlas, which cost $0.00045 and peaked at $0.26; Alien Worlds, which cost $0.003 and peaked at $7… multiple single projects have reported profits exceeding $100 million.

So the question arises: Why can LD, which doesn't have a great reputation, still invest in these star projects?

I once asked someone from LD Capital, and they gave me a particularly vague answer: "Boss Yi has a big vision, the partners are impressive, and the team collaborates well."

To explain, founder Yi Lihua fully delegates authority, giving his team enough autonomy and space to perform; several partners are very capable, with most quality projects coming from their personal efforts; LD places great emphasis on post-investment, with the team working together to serve the projects.

Very official, but also correct, the core relies on super individuals like partners to drive.

In my view, this is also a bottleneck faced by many VCs like LD. Once a VC reaches a certain scale, it needs brand support; it cannot just expand manpower to find projects but needs projects to come to the VC. A good brand makes investments simple and easy. Otherwise, the larger the scale, the more exhausting the investments become, and the more internal competition there is.

Just as Tencent defined its company mission in 2005 as "the most respected internet company," the bosses who made money in crypto should also have a big vision; they need to make money while cherishing their reputation and stepping onto the world stage.

A friend in the industry once said, "If you make a lot of money but have no status in the community, people will only see you as a coal boss in the crypto circle," which I deeply agree with.

Dimensionality Reduction Attack: Big Capital and Their Circles

The reality of internal competition in crypto is a two-tier differentiation, with capital clustering.

On one hand, some small and medium VCs are fighting tooth and nail for a few tens of thousands of dollars in quotas, while on the other hand, top VCs wield capital in one hand and brand in the other, launching dimensionality reduction attacks on other crypto VCs, and they love to band together.

a16z, the banner of Web3, has several partners tirelessly writing essays on Twitter to preach Web3 and occupy minds.

If you want to understand Web3.0, visit a16z's official website to read Future (a16z's media platform); if you want to learn about the ace projects of Web3.0, check a16z's portfolio… this is the effect they hope to achieve, continuously seizing the discourse power of the Web3 era.

Paradigm, which recently raised $2.5 billion for its latest fund, money is important, but what’s most frightening about Paradigm is its first-class research, innovation, and practical capabilities, allowing them to monopolize innovation from the source.

On November 25, Paradigm announced the appointment of Georgios as CTO, at the top of the blockchain food chain, combining technology and capital. I believe this is the future norm for T1 crypto VCs: understanding technology and possessing it.

Paradigm has cutting-edge theoretical innovations; it has the hardest technology; it has even more capital… to the extent that Paradigm can turn decay into magic. If you don’t believe it, look at how Uniswap was gradually nurtured by Paradigm.

Meanwhile, in the traditional VC field, Lightspeed and Sequoia are expanding into the crypto world at rocket speed, forming their own circles.

This is another major trend in the crypto VC world: capital clustering, becoming increasingly closed.

For example, every public chain ecosystem has its own VC circle, and you will often find that the investors in quality projects within the ecosystem are those few firms, as is the case with Polkadot, Solana, etc. Even the star projects within the Ethereum ecosystem are divided among the core circles.

The most closed-off is the Terra ecosystem, which is basically monopolized by Do Kwon and his friends. For instance, Delphi Digital personally incubates projects and designs economic models, while other VCs cannot squeeze in at all.

It makes sense; if there’s a 99% chance of making money from a project, why not take it for yourself or share it with friends who work together, instead of giving it to outsiders?

Self-strengthening leads to universal strength.

The Future of Crypto VCs

Back to the point, how to invest in good projects?

The core boils down to two points: one is discovering good projects, and the other is being able to invest in them. Most VCs get stuck on the second point.

In the long run, crypto VCs need to build a unique core competitiveness to strengthen their brand.

I personally think some good ideas are to establish influence in vertical fields.

You cannot seize every opportunity; rather than casting a wide net, it’s better to focus vertically on a specific area, as crowded places are always very competitive.

For example, one of this year's biggest winners, Animoca, and its backing Everest Ventures Group (EVG), have been deeply involved in the gaming sector for many years, with strong blockchain games like SANDBOX rising to fame overnight.

In the early hours of December 9, Animoca Brands founder Yat Siu announced this year's achievements on Twitter:

Investment and digital asset revenue for the first nine months of 2021 grew to approximately $529.6 million, holding over $600 million in liquid digital assets (including BTC, ETH, USDC, and AXS, FLOW, etc.).

The digital asset reserves belonging to Animoca Brands' product and platform ecosystem (including proprietary tokens like REVV, SAND, TOWER, and GMEE) have risen from approximately $2.9 billion at the end of September 2021 to about $15.9 billion at the end of November 2021.

Multicoin Capital's achievements mainly come from Layer 1, with Solana and THORChain (which I define as 'cross-chain L1') being particularly outstanding.

Secondly, embrace change; your enemy is never your competitor; it may be the times.

In Jin Yong's novels, the Golden Wheel Dharma King was defeated by Yang Guo with one move after practicing martial arts for 16 years because he completely disregarded the rules. What defeated Kodak and other camera brands was not their peers but smartphones; the future enemies of crypto VCs may not come from current VC peers.

This is an era where everyone is a media outlet, and everyone is a VC.

Let me mention a few VC organizations and forms that I believe may rise.

DoraFactory, I noticed this organization because a friend from a large crypto VC once said, "DoraFactory's ability to invest in good projects is much stronger than ours."

The reason is simple; DoraFactory is backed by DoraHacks, which has hosted hundreds of blockchain hackathons globally, with star projects like Matic originating from its hackathons.

To put it metaphorically, DoraHacks is the first midwife nurturing great projects, helping early projects grow, naturally gaining better investment opportunities ahead of others.

Entering the new era of public chains and the Warring States period, hackathons have also become a platform for excellent projects. Gitcoin belongs to the Ethereum camp, while the non-aligned DoraFactory occupies a very important ecological position.

Next is DAO VC, or venture capital DAO, which I summarize as the union of super individuals, a deconstruction and disruption of the traditional VC model.

Although it has not yet impacted the traditional crypto VC market, the wind has begun to blow, stirring up waves.

For example, Metacartel, whose DAO members include founders of Aave, Nexus Mutual, Ocean Protocol, and Axie Infinity, and has incubated Raible, Gelato Network, and DAOHaus.

Venture capital has always been concentrated around Silicon Valley, with both capital and talent gathered in specific areas. However, DAO-based VC funds can invest more effectively on a global scale and attract talent. In the DAO model, carry and fees can be embedded in smart contracts.

Although the road ahead is long, change is happening.

Risk warning

Risk warning Risk warning

Risk warning