The perpetual option creator Shield opens a new era of public participation in DeFi derivatives

The flourishing DeFi in 2020 brought vitality to the cryptocurrency market and rooted the concept of decentralization in people's hearts.

The flourishing DeFi in 2020 brought vitality to the cryptocurrency market and rooted the concept of decentralization in people's hearts.Introduction

Open Finance Begins to Shine

The flourishing DeFi in 2020 brought vitality to the crypto market and rooted the concept of decentralization in people's minds.

Looking at the current state of DeFi, projects are mostly concentrated in popular sectors like DEX and lending, with significant homogeneity. As investors' risk preferences and exposures change with the market, the importance of DeFi derivatives trading as a fundamental module of the DeFi market is gradually becoming apparent, giving rise to a number of representative projects that have attracted market attention; trading volumes continue to rise and set new highs, even rivaling centralized derivatives platforms.

Economic Incentives Rather Than Demand Become Major Drivers

However, the impressive trading data from these platforms is largely stimulated by "mining incentives," rather than reflecting genuine natural demand like Uniswap. In reality, current decentralized derivatives trading protocols face numerous issues, such as poor liquidity, opaque liquidation processes, low capital utilization, high fees, and significant risks.

Shield - A Product Born for Trading, Addressing User Pain Points

To address the persistent issues in the current DeFi derivatives sector and promote its development, the decentralized derivatives protocol Shield has proposed a series of innovative solutions, including dual liquidity pools (P2DP), a decentralized broker system, and a third-party liquidation mechanism.

Perpetual Options as a Lever

As the first product of the protocol, Shield has launched decentralized perpetual options. This product does not require manual rollovers and offers an operational experience similar to perpetual contracts, while also possessing the characteristics of options such as "high leverage," "no liquidation risk," and "unlimited profits with limited losses"; more importantly, the dual liquidity pool (P2DP) can provide unlimited liquidity and enable users to trade with zero slippage.

Decentralized derivatives are still a blue ocean, and Shield provides excellent ideas and innovative models that will lay the groundwork for the next phase of DeFi derivatives, lowering the participation threshold through protocol design and truly addressing user pain points.

I. Derivatives Will Lead DeFi into a New Stage of Mass Adoption

Cryptofinance has two key historical milestones: first, in 2008, the birth of Bitcoin marked the rise of cryptofinance, breaking the traditional institutions' monopoly on finance (TradFi), expanding the range of asset classes, and laying the foundation for the decentralized essence of cryptofinance; second, in 2020, the rise of decentralized finance (DeFi) extended the scope of cryptofinance, allowing crypto assets to become truly decentralized and genuinely empowering various functions, enabling deep community participation.

The Parallel Structure of CEX + DEX Has Become a Foregone Conclusion

Although DeFi has a relatively short development history, it has shown vigorous growth potential. Data shows that the value locked on-chain has surged from $1 billion two years ago to $256.95 billion today, with various DeFi projects emerging like mushrooms after rain. Moreover, DeFi has successfully "broken out," with even the traditionally cautious U.S. regulators expressing optimism about DeFi's prospects. "The entire concept of DeFi is revolutionary and may even reduce systemic risks to some extent, ultimately leading to large-scale disintermediation of the financial system and traditional participants," said Heath Tarbert, Chairman of the U.S. Commodity Futures Trading Commission (CFTC), giving high praise to DeFi.

On one hand, the rise of DeFi has indeed impacted CeFi, with DeFi lending directly transforming traditional financing channels; MakerDAO has even introduced traditional assets into the crypto market, challenging the core business of TraFi. On the other hand, with the rise of DEX platforms like Uniswap, some second- and third-tier centralized trading platforms have seen their trading volumes plummet. In the foreseeable future, the parallel structure of leading CEX + DEX will remain the mainstream model for a considerable time. After the explosive growth of DEX and lending sectors, the industry's most pressing question is, where is DeFi's next stop? The answer is DeFi derivatives. Furthermore, DeFi derivatives protocols represent the last piece of the pie in the DeFi market.

(1) DeFi Derivatives Erupt, but the Industry Landscape is Uncertain; Players Challenging the Top Positions Will Yield Excess Returns

Whether in traditional finance or cryptofinance, derivatives have always played a crucial role and are one of the key elements of all mature financial systems. Moreover, the trading volume of derivatives far exceeds that of spot trading, demonstrating their strong vitality.

In traditional financial markets, the trading volume of derivatives is 20 to 40 times that of spot trading. In contrast, in the crypto financial market, the trading volume of derivatives on centralized exchanges also multiplied several times in 2020, with volumes continuously refreshing; particularly since the third quarter of last year, the daily trading volume of derivatives has first surpassed that of spot trading, highlighting the development potential of crypto derivatives.

Centralized Derivatives Platforms Face Numerous Challenges

Currently, crypto derivatives are still dominated by centralized exchanges, which, while developing rapidly, also face intense competition. Additionally, centralized exchanges have repeatedly experienced trust crises, raising concerns. Furthermore, with global regulatory policies tightening, various centralized platforms have announced stricter audits and trading restrictions, with some centralized platforms shutting down derivatives trading and retaining only spot products, making it increasingly difficult for users to access derivatives trading services.

With the rise of DeFi, DeFi derivatives, which possess advantages such as censorship resistance, on-chain settlement, and user-friendliness, have become an optimal solution, leading many industry insiders to have high hopes for them, believing they will become the next blue ocean and replace centralized derivatives.

Decentralized Derivatives Are Still in Their Early Stages

Although the current volume of DeFi derivatives is still not comparable to centralized derivatives, their development momentum is strong. Especially in the second half of this year, under tightening policies, the trading volume of DeFi derivatives has surged, ushering in a wave of rapid development. Today's DeFi derivatives can be likened to the early days of Uniswap; although still in their infancy, they possess boundless vitality and potential, offering the possibility of generating excess returns from an investment perspective. In this blue ocean, one or two DeFi derivatives platforms will eventually emerge that surpass leading CEXs like Binance.

More critically, although there are many players in the DeFi derivatives space, no true leading projects have emerged, and no paradigm products have appeared, meaning the industry landscape has yet to solidify, and emerging projects still have considerable room for development.

Many may argue that dYdX has already become the leader in derivatives, but the reality is not so. In fact, dYdX's trading volume only exploded after the issuance of governance tokens, not due to natural demand. It employs a "trading mining" mechanism, where users can earn tokens as incentives for trading, which led to the surge in trading volume. Other derivatives platforms like Deri and Prep are in similar situations; once trading mining is canceled, their trading volumes drop significantly. Some derivatives platforms have recently seen volume increases due to airdrop incentives.

Ultimately, these DeFi derivatives protocols have not truly addressed users' rigid demands. The reason why DEXs like Uniswap stand out is that they capture the long-tail traffic in the trading domain. A good DeFi derivative must solve the developmental dilemmas of DeFi derivatives to become a market leader.

(2) The Development of DeFi Derivatives is Influenced by Three Major Factors

The development of DeFi derivatives faces many obstacles, which can be roughly categorized into three areas:

Product Variety Limitations. The most common types of derivatives are futures and options; which should DeFi derivatives choose?

Currently, the vast majority of platforms focus on the futures market due to its low entry barriers and broad user base. Particularly, the perpetual contract market, which does not require frequent management and position establishment, has trading volumes far exceeding those of spot and margin trading, making it highly favored. However, futures have low capital utilization rates and are prone to liquidation, exposing users to significant risks.

Options, on the other hand, have many advantages such as no liquidation risk and high leverage, and the market size of traditional financial options is comparable to that of futures, making them seem like a good choice. However, the reality is that options have higher entry barriers, greater user education costs, and the trading volume of crypto options is far less than that of futures.

Therefore, the best choice is to combine the dual advantages of options and futures to launch a product that meets users' needs for "controllable risk and unlimited returns," such as Shield's perpetual options (explained in detail later).

Poor Product Experience. Currently, the vast majority of DeFi derivatives protocols still face issues of insufficient trading depth/liquidity, with users sometimes unable to execute trades when opening or closing positions. In terms of liquidation, some DeFi protocols, to avoid losses, not only require higher margins but may even forcibly liquidate user positions in advance; during extreme market conditions like price spikes, trading pages may become inaccessible, preventing users from trading.

Insufficient Infrastructure. Some DeFi derivatives protocols choose to build on Ethereum, but due to network congestion, they often face issues such as trading delays and high gas fees.

These various problems have led to the slow development of DeFi derivatives, with no leading projects emerging and difficulty attracting professional derivatives users.

II. Shield Has the Strength to Become the Leader in the Perpetual Options Sector

Addressing Pain Points from the Perspective of Complete Openness, Decentralization, and User-Centric Needs

To tackle the persistent issues in the current decentralized derivatives sector and promote its development, the DeFi derivatives trading protocol Shield has proposed a series of innovative solutions. On November 5, Shield's mainnet 1.0 was officially launched. As the first product of the protocol, Shield has also introduced decentralized perpetual options (which launched a test version last year).

"The core of the Shield protocol is to build an open, secure, and highly accessible derivatives infrastructure, making it one of the largest DeFi Lego blocks. In its current state, we encourage everyone to experience our first innovative on-chain product, perpetual options," stated the Shield team.

Shield's perpetual options are an innovative derivatives tool that combines the dual advantages of perpetual contracts and options, and it is currently the first true DeFi perpetual option on the market.

Significantly Lowering Participation Barriers - Making Settlement Procedures No Longer a Problem

From an operational experience perspective, the entry barrier for this product is very low. Users simply connect their wallet address, transfer funds, and choose to go long or short to complete the trade, providing an experience similar to perpetual contracts, greatly simplifying the entry threshold for options. Users do not need to understand complex concepts such as "strike price" or "settlement price," which also greatly expands the audience.

(Shield Perpetual Options)

"Traditional European and American options are complex and difficult to understand, making them hard to popularize. To meet broader trading needs, we considered whether we could simplify options by eliminating fixed expiration dates. Thus, the design concept of perpetual options was born," explained the Shield team.

Three Ingenious Designs Make Perpetual Derivatives Stand Out

Shield's perpetual options draw from perpetual contracts, having no expiration date and requiring no manual rollovers, but their underlying core remains options. This means they inherit the multiple advantages of options.

1. No Margin Liquidation Risk

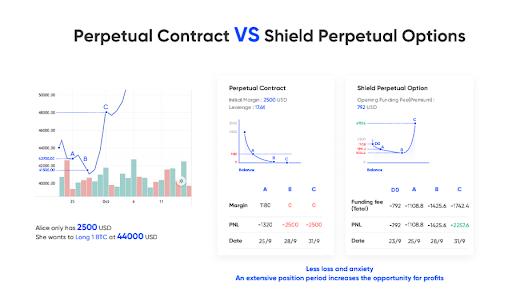

Assuming user Alice holds $2,500 in capital and opens a perpetual contract with 17x leverage when Bitcoin is priced at $44,000, if Bitcoin drops more than 6%, Alice faces liquidation risk; even if the price later rises to $60,000, Alice's profit would be $0. However, if she chooses Shield's perpetual options, Alice only needs to pay the "daily funding fee" to maintain her position; even if Bitcoin's price drops, it won't lead to liquidation; once the price rebounds to a specific target for closing, she can still achieve high returns.

Based on real market conditions, if Alice had opened a perpetual contract in the last week of September, she would have lost her entire $2,500; however, if she had opened Shield's perpetual options, her final profit would be $2,257, with a return rate close to 100%. As shown below:

2. Controlled Losses, Unlimited Profits, and Safe Leverage

Shield's perpetual options will deduct funding fees at a fixed rate every 24 hours to maintain positions, with daily losses kept below 0.4%, which is also the maximum loss users might incur; however, once market volatility increases, theoretically, users' profits have no upper limit.

Moreover, Shield's perpetual options support leverage ratios from 25x to 500x, far exceeding the leverage multiples of perpetual contracts in the market, maximizing capital utilization. Low risk with high returns is also the greatest feature of options.

3. No Position Anxiety, Peace of Mind Holding Positions

In extreme market conditions, users holding perpetual contracts may experience significant anxiety, constantly flipping between closing and holding positions. Sometimes, just after closing a position, the market suddenly reverses, increasing anxiety and creating a vicious cycle of consecutive operational errors. Once users hold Shield's perpetual options, they need not worry about price spikes causing forced liquidations, alleviating position anxiety and allowing them to hold positions for as long as necessary until they realize profits.

According to information on the official website, Shield's version 1.0 currently supports trading pairs BTC/USDT and ETH/USDT, with plans to add support for other cryptocurrencies in the future.

Although the decoupling degree and protocol attributes of Shield 1.0 are not yet sufficient, we prefer to view Shield's perpetual options as the first attempt of the Shield derivatives protocol. We will continue to iterate and upgrade until the world has a secure, robust, and developer-friendly decentralized derivatives trading protocol," stated the founder of Shield in a letter.

Overall, Shield's perpetual options present virtually no learning or migration costs for traders in the mainstream perpetual contract market. The emergence of Shield's perpetual options will deliver a dimensional blow to the current perpetual contract market and inevitably impact existing DeFi derivatives products, reshaping the market landscape.

III. Innovative Protocol Design and Scientific Pricing Establish a Moat

Although the market prospects for DeFi perpetual options are broad, the entry barriers are high, especially since Shield has built its own moat, thus not needing to worry about being surpassed by latecomers. Specifically, Shield has made significant innovations compared to other competitors in the following areas: dual liquidity pools, precise on-chain pricing of perpetual options, and a decentralized network designed based on Nash equilibrium.

(1) P2DP - Solving the Initial Liquidity Shortage of Derivatives

For derivatives, liquidity and depth are crucial. Regarding liquidity solutions, current DeFi derivatives mainly fall into the following categories.

First, there is the order book model represented by dYdX and Injective, advocating off-chain matching and synchronizing assets with orders to high-performance public chains. This model is favored by some users due to its adherence to centralized platform trading habits, but it is essentially a semi-centralized model. Particularly in the early stages of projects, some orders are primarily matched through their off-chain servers, failing to execute entirely on-chain, and it remains a semi-centralized approach. Recently, dYdX faced significant interruptions due to AWS outages, exacerbating concerns about its over-reliance on AWS.

Second, there is the AMM model variant represented by the Perpetual protocol (vAMM, sAMM), which essentially uses the same x*y=k constant product formula as Uniswap. The advantage of this model is that it supports leveraged trading, but the downsides are also evident, particularly high slippage.

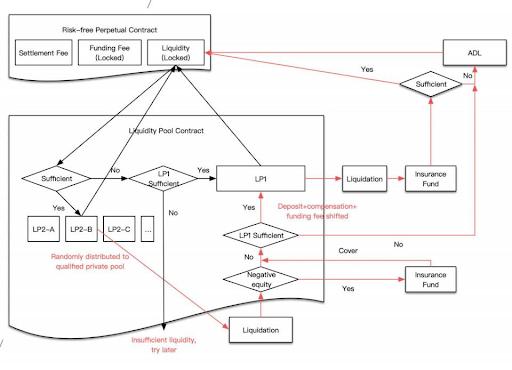

Shield creatively proposed a new liquidity solution - the dual liquidity pool P2DP (Peer to Dual Pools), fundamentally solving the LP counterparty risk by introducing a private pool that can hedge risks, ensuring on-chain liquidity.

In simple terms, the dual liquidity pool consists of a public pool and a private pool. The public pool is a unified reserve liquidity pool where anyone can provide liquidity as a supplement, while the private pool is reserved for professional market makers, requiring higher capital strength, quoting ability, and position management. When users open positions, the system first allocates orders to the private pool (primarily provided by professional institutional market makers); private pool market makers can hedge external risks after accepting orders with a 20% margin; when the private pool lacks liquidity or insufficient order margin leads to liquidation, orders will be transferred to the public pool.

(Dual Liquidity Pool Structure Diagram)

In summary, during the entire trading process, professional market makers will bear the main counterparty risk in the private pool, while ordinary users participating in the public pool primarily serve as the final "insurance" for the private pool, thus reducing risk.

Thanks to the establishment of the dual liquidity pool, Shield's perpetual options can achieve zero slippage and instant execution.

(2) Precise On-Chain Pricing of Perpetual Options - Application Driven by Scientific Principles

The importance of pricing in options trading is self-evident. Currently, on some centralized platforms, option pricing is primarily led by market makers, who set prices independently, resulting in a lack of transparency in the pricing mechanism and significant discrepancies in the reasonable value of options. Due to the absence of a pricing formula applicable to perpetual options, the Shield team had to invest considerable effort in developing a pricing model. By applying mathematical knowledge such as stochastic processes, volatility, and partial differential equations with initial boundary values, Shield found the precise solution for the Shield perpetual options holding fee (option fee). Achieving this precise solution in the EVM is nearly impossible. To complete on-chain pricing, the Shield team applied cutting non-linear processes, replacing the precise solution of the non-linear pricing model with an approximate solution of linear computation, successfully realizing on-chain pricing.

"This derivation process of the precise solution for the pricing model is itself an excellent academic paper in a core journal." The Shield perpetual options are the first academic-grade product based on the Shield protocol. (Note: Pricing model paper download link https://docsend.com/view/7k98hrtjtscc5w7j)

(3) Decentralized Network Designed Based on Nash Equilibrium - Providing Strong Participation and Economic Incentives for Various Roles

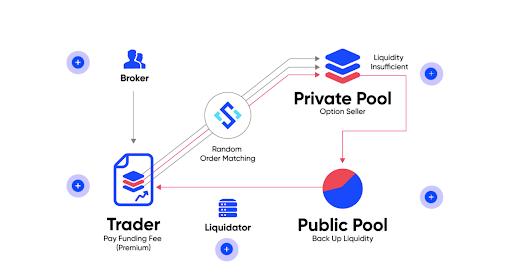

To build a secure, stable, and open decentralized derivatives trading protocol, Shield designed a trading network based on non-cooperative game theory (game theory). This decentralized network includes five roles: traders, brokers, private pool LPs, public pool LPs, and liquidators, using the SLD token for value scheduling and governance within the network.

- Brokers: Under the commission system incentive of the [Broker Campaign], brokers continuously bring traders to the Shield network through education and referrals.

- Traders: Buyers of the Shield protocol, paying transaction fees and holding costs to meet their trading needs.

- Private Pool: Sellers of the Shield protocol, providing liquidity for the protocol's private pool through professional market-making capabilities, earning liquidity rewards (SLD) for accepting orders.

- Public Pool: A reserve liquidity pool that anyone can participate in, earning LP rewards (SLD) through reserve liquidity mining.

- Liquidators: When the margin of traders and liquidity pools is insufficient to trigger liquidation contracts, they earn arbitrage income of 150% of gas fees.

The operational flow of the protocol is as follows: traders place orders based on demand, and orders are distributed to the private pool through a chain-based random matching engine; if the private pool runs out of liquidity, orders are allocated to the public pool until the trader completes the order; if the available balance of the trader, private pool, or public pool is insufficient to pay fees or incurs losses, the liquidator initiates liquidation. As shown below:

It is important to note that the "on-chain random order matching algorithm" is also a significant innovation of the Shield protocol. The specific principle is to generate random numbers using the block hash value of the order transaction and the block time, taking the remainder as the corresponding private pool number; if the private pool is in a closed order state or has insufficient available balance, it will poll sequentially until it encounters an available private pool.

(4) Tokennomics - An Efficient Protocol Value Capture Model

The Shield protocol provides token incentives such as liquidity mining, with the tokens used for incentives accounting for 60% of the total supply (1 billion tokens). Additionally, according to the white paper, the mining rewards will be halved once 20% of the remaining mining shares are mined, reducing the circulation of the SLD token from the source.

The SLD tokens earned from mining can be redeemed for value through a buyback and burn contract, with each token holder having the right to trigger the buyback contract. Shield ensures that each round adds 100,000 flash exchange shares, keeping the flash exchange shares equal to 100% of the value of the buyback pool (funded by 90% of transaction fees), thus generating a buyback price.

- When the secondary market price of SLD is above this price, the value of the buyback and burn pool will continue to grow as no one redeems it.

- When the secondary market price falls below this price, people will buy SLD in the secondary market to redeem the buyback contract for profit, thus ensuring the minimum price in the secondary market (this minimum price is similar to the price derived from PE valuation in stock valuation).

The transaction fees in the buyback and burn pool on the left will grow without an upper limit as business increases, while the circulating SLD pool on the right will continue to deflate due to burning and halving of mining rewards. In the long run, this model design ensures the long-term value redemption of SLD.

IV. Shield's Perpetual Derivatives Will Open a New Chapter in DeFi Applications

From the previous introduction, it can be seen that designing a decentralized derivatives protocol is not an easy task. The new pricing model and liquidity solutions, among others, pose high challenges to the team's financial engineering product design capabilities.

The Shield team's members come from top financial institutions and leading internet companies, combined with a profound application of blockchain technology, making the product's implementation possible. The following is Shield's development blueprint and several important milestones:

- In December 2021, launch the standard perpetual contract based on Shield protocol version 2.0 and L2 technology;

- In 2022, launch the highly composable Shield protocol version 3.0 for developers, including structured products and achieving complete decentralized governance of the Shield protocol.

The innovation and development potential of Shield in the DeFi derivatives market have also attracted capital attention. In May of this year, Shield raised $2 million in funding, led by A&T Capital and Hashkey Capital, with participation from SevenX Ventures, Incuba Alpha, Youbi Capital, OKEx Blockdream Ventures, Bonfire Union, Moonwhale Ventures, Zonff Partners, and Shima Capital. It is undeniable that DeFi derivatives are currently in their infancy, with potential risks and issues. However, with the entry of emerging players like Shield, the industry is experiencing significant disruption and innovation, and more projects are beginning to explore the development direction of DeFi derivatives, which is beneficial for the entire industry.

The DeFi derivatives sector is gradually becoming a market hotspot, and we look forward to more new features.