Can UXD, led by Multicoin, break the existing stablecoin pattern?

Raising 57 million dollars in a day, is UXD a game changer or just another pitfall in the stablecoin sector?

Raising 57 million dollars in a day, is UXD a game changer or just another pitfall in the stablecoin sector?Written by: 0x76@Rhythm Research Institute

Among the many sub-sectors in the Crypto industry, stablecoins, especially algorithmic stablecoins, may be the area that has caused the most pain for investors. However, entrepreneurs in the industry have not stopped their exploration. Just last weekend, a new stablecoin project called UXD Protocol, developed on Solana and backed by renowned funds like Multicoin, successfully conducted its IDO and raised $57 million.

So, does UXD Protocol have any key breakthroughs compared to previous stablecoin projects, and is it possible that it might repeat the mistakes of other algorithmic stablecoin projects?

Basic Mechanism of UXD

The UXD Protocol includes two native tokens: one is the stablecoin UXD (equivalent to DAI in MakerDAO), and the other is the governance token UXP (equivalent to MKR in MakerDAO).

Strictly speaking, UXD Protocol is not an algorithmic stablecoin project. Its fundamental mechanism for maintaining price stability is still based on full collateralization of assets. Similar to MakerDAO, users must provide sufficient collateral assets to the protocol before minting the stablecoin UXD.

Taking SOL as collateral as an example, suppose the current market price of SOL is $200. If a user collateralizes 1 unit of SOL, they can generate 200 units of the stablecoin UXD from the UXD Protocol. At the same time, the UXD Protocol will short SOL in the perpetual contract market at a 1:1 ratio to the amount received in spot. At this point, the protocol holds a long position of 1 unit of SOL in the spot market while holding a short position of 1 unit of SOL in the futures market, thus constructing a risk-neutral combined position.

So, what are the benefits of doing this?

The biggest advantage of maintaining the collateral's risk neutrality is that it allows the total market value of the collateral to remain unchanged at $200 indefinitely. If the price of SOL rises by 10%, the spot will gain $20 while the futures will lose $20; if the price drops by 10%, the spot will lose $20 while the futures will gain $20.

Thus, the $200 UXD stablecoin issued by the UXD Protocol is always backed by sufficient redeemable collateral equivalent to $200, which will not be affected by price drops that trigger liquidation mechanisms.

When a user needs to redeem UXD, the UXD Protocol will close the corresponding perpetual contract. If at this time the price of SOL rises from $200 to $400, the short position in the perpetual contract will incur a loss of $200, offsetting the $200 profit from the spot position. Ultimately, the value returned to the investor will still be $200 worth of SOL. At the settlement price, the user will finally receive 0.5 units of SOL.

Note this example: the user initially collateralized 1 SOL to mint the UXD stablecoin, but when the user redeems, due to the doubling of SOL's price, the user can only get back 0.5 SOL. In other words, as the price of the collateral rises, the quantity of the collateral also decreases. Similarly, if the price of SOL drops by half, the assets redeemed by the user will increase to 2 SOL.

This is completely different from the lending protocols we usually use. In MakerDAO, users who deposit ETH to obtain the stablecoin DAI can capture the appreciation of ETH's price while using the stablecoin. The mechanism of UXD Protocol is more akin to directly selling assets for stablecoins, and when redeeming the collateral, using the same amount of stablecoins to buy back the assets at the current market price.

So the question is, since this is equivalent to directly selling assets, why would users still want to obtain stablecoins through UXD Protocol instead of using a simpler and more direct method of selling assets?

Value Capture Mechanism of UXD

Based on the analysis above, UXD Protocol must make users more willing to choose to mint stablecoins through UXD Protocol instead of directly selling assets. Therefore, UXD Protocol must be able to provide users with additional value while obtaining stablecoins. In UXD Protocol, the main source of this additional value comes from the short positions in perpetual contracts it holds.

We know that perpetual contracts are a derivative tool that anchors the marked price to the spot price through a funding fee mechanism. If the contract price is higher than the spot price it tracks, then the long position in the perpetual contract must periodically pay funding fees to the short position holders. Conversely, if the contract price is lower than the spot price, the short position pays the long position.

The source of value capture for UXD Protocol lies here.

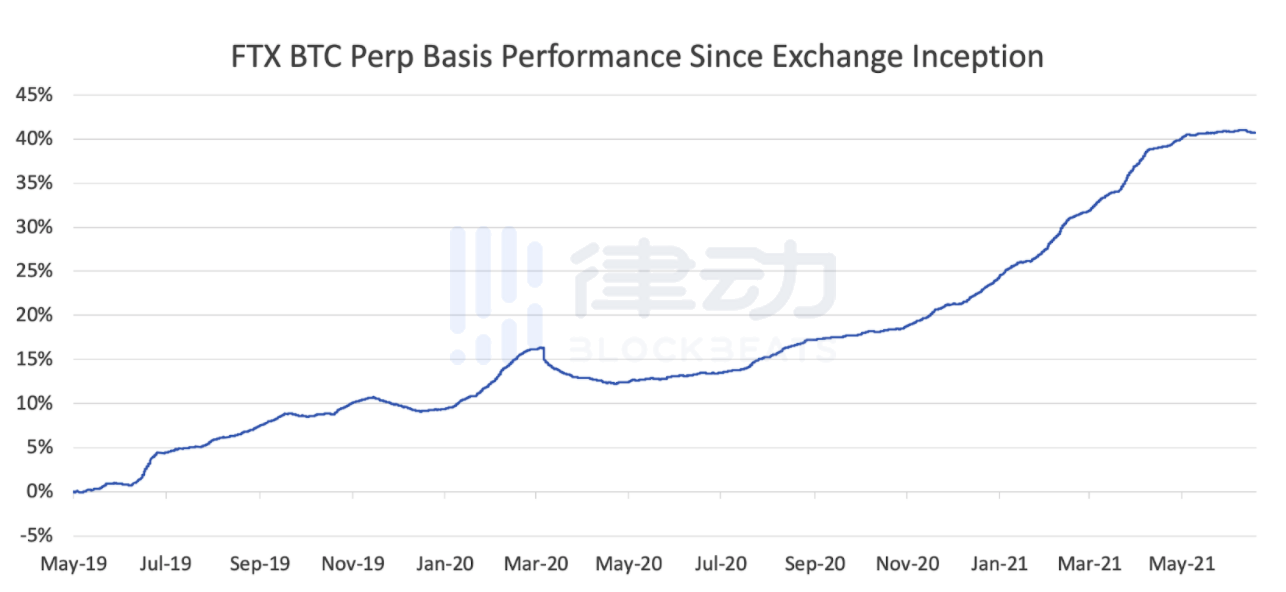

According to historical data backtesting (see the chart below), in the crypto market, the price of perpetual contracts is higher than the spot price for the vast majority of the time. In other words, in most cases, long position holders of perpetual contracts need to periodically pay certain funding fees to short position holders. According to the design rules of the UXD Protocol, for every stablecoin that needs to be minted, the UXD Protocol must also hold an equivalent amount of collateral short positions in the market.

Therefore, if UXD Protocol can be widely adopted in the future, it may become the largest holder of short positions in the crypto perpetual contract market at that time, thereby obtaining a large amount of funding fees paid by longs as the main source of income for the protocol. According to the official documentation of UXD Protocol, this income will be partially allocated as risk reserves, while the remaining portion will be distributed to UXD holders.

In other words, if a user directly sells 1 unit of SOL, they will only receive $200 in income once. However, if they mint $200 UXD through UXD Protocol, they will not only gain $200 in purchasing power but will also continuously receive an additional reward. This incentive system can encourage more people to choose to use the UXD Protocol to obtain stablecoins instead of directly selling assets.

Logical Flaws of UXD

The above reasoning seems to be an extremely ideal design, but this trading structure always gives a sense of profit created out of thin air. So where does the income obtained by UXD Protocol from the short positions in perpetual contracts actually come from?

It is important to note that one of the prerequisite assumptions for UXD Protocol to operate normally is that the perpetual contract market can maintain this imbalance in the long term. In other words, it is necessary to maintain the status quo of perpetual contract prices being higher than spot prices for most of the time, so that UXD Protocol can continuously arbitrage from this imbalance to maintain the healthy operation of the protocol.

However, if UXD Protocol can indeed achieve large-scale adoption in the market, as the scale of assets managed by the protocol gradually expands, the short positions in perpetual contracts it holds will also inevitably grow. This will cause the perpetual contract market to return to equilibrium, eliminating the prerequisite assumption for the protocol's establishment and suppressing the main source of income for UXD Protocol. In other words, the mechanism design of UXD Protocol inherently carries a certain self-limiting nature, inhibiting the unlimited expansion of its protocol scale.

Therefore, although the mechanism design of UXD Protocol is eye-catching, it may still be difficult to become the ultimate solution for stablecoins.

Will UXD Be the Endgame for Stablecoins?

Although stablecoins have undergone years of exploration, the current state of development in the industry is still unsatisfactory. Among them, algorithmic stablecoin projects are particularly notorious for their pitfalls, leaving countless investors with significant psychological scars from various de-pegging incidents.

In this context, UXD Protocol has still managed to attract a large amount of market funding subscriptions due to its unique innovations. The fundamental reason lies in the fact that this project can alleviate the shortcomings of existing stablecoin solutions to a certain extent.

Compared to MakerDAO, UXD Protocol greatly improves the capital utilization rate of the protocol. Even when users use highly volatile asset classes, the capital utilization rate for minting stablecoins remains as high as 100%, while also providing income sharing to stablecoin holders instead of paying interest like DAI. Additionally, compared to centralized stablecoin solutions like USDC, UXD Protocol is more decentralized, and the collateral assets are entirely sourced from crypto-native assets.

However, considering that UXD Protocol inherently carries a certain self-limiting nature in its basic mechanism, and still requires consuming an equivalent amount of original capital while giving up the subsequent appreciation of the collateral, ordinary investors need to exercise caution in their judgments before entering, especially when the current IDO has already greatly overdrawn future price increases.