Learn about the multilateral central bank digital currency bridge mBridge in one article. Will it interact with the rich ecosystem of Ethereum in the future?

mBridge is an important breakthrough point for the People's Bank of China in the global cross-border payment revolution and a key entry point for reshaping the global payment system.

mBridge is an important breakthrough point for the People's Bank of China in the global cross-border payment revolution and a key entry point for reshaping the global payment system.Original Title: “【News Weekly Review】Multilateral Central Bank Digital Currency Bridge: The Beginning of Disrupting the International Payment System”

Source: Mobile Payment Network

Author: Mu Chu's Article

The multilateral central bank digital currency bridge project has recently gained significant attention.

On November 3, coinciding with Hong Kong FinTech Week, the People's Bank of China Digital Currency Research Institute, the Hong Kong Monetary Authority, the Bank of Thailand, and the Central Bank of the United Arab Emirates jointly released the use case manual for the multilateral central bank digital currency bridge project, which briefly introduces the project’s application scenarios and testing progress.

Since the People's Bank of China joined in February 2021, this project has received high levels of attention. Today, let's briefly discuss what the multilateral central bank digital currency bridge project is all about.

Development History

The multilateral central bank digital currency bridge project originally started as a bilateral pilot project between the Bank of Thailand and the Hong Kong Monetary Authority.

In 2017, the Hong Kong Monetary Authority began researching central bank digital currency projects, naming it LionRock. LionRock is a famous peak in Hong Kong that resembles a lion, and the "LionRock Spirit" is a well-known motivational concept in Hong Kong.

In August 2018, the Bank of Thailand launched its central bank digital currency (CBDC) project named Inthanon, which involved eight commercial banks in the country. According to my research, Inthanon seems to represent Doi Inthanon, a mountain in Chiang Mai, Thailand, which is the highest mountain in Thailand.

In May 2019, the two CBDCs from Hong Kong and Thailand conducted a "mountain-to-mountain" collaboration, launching the Inthanon-LionRock project aimed at exploring the application of CBDCs in cross-border payments.

In September 2019, the first phase of the Inthanon-LionRock project was initiated and completed in December of the same year. This phase primarily focused on technical openness, with both parties successfully developing a proof-of-concept prototype based on Distributed Ledger Technology (DLT) with the participation of ten banks from both regions.

In November 2020, the second phase of the Inthanon-LionRock project was launched. During this phase, both parties explored commercial use cases in cross-border trade settlement and capital market transactions.

In February 2021, the Inthanon-LionRock project entered its third phase of development, with the People's Bank of China and the Central Bank of the UAE joining, expanding the project from two parties to four. Meanwhile, the Hong Kong center under the International Bank for Settlements Innovation Hub also supported the project. The project was officially renamed the "Multiple Central Bank Digital Currency Cross-Border Network" (m-CBDC Bridge), which is what we refer to as the multilateral central bank digital currency bridge.

In September 2021, the four parties released the first phase report of the multilateral central bank digital currency bridge project, at which point the convenience and efficiency the project could bring to cross-border payments began to emerge.

In November 2021, the four central banks published the use case manual for the multilateral central bank digital currency bridge project, introducing 15 potential application scenarios and testing progress, covering international trade settlement, cross-border e-commerce, supply chain finance, and more.

For convenience, we will refer to the multilateral central bank digital currency bridge project as mBridge from here on.

What is the Principle?

In September 2021, the International Bank for Settlements Hong Kong Innovation Center released a summary report titled "Inthanon-LionRock to mBridge: Building a multi CBDC platform for international payments" (hereinafter referred to as "the report").

The report indicates that mBridge evolved from the Inthanon-LionRock phase, inheriting its technical principles and some concepts. mBridge will adhere to three main principles: non-harm, compliance, and interoperability, with the overall goal of "designing and iterating a new generation of efficient cross-border payment infrastructure to address pain points such as high costs, low speed, and complex operations."

According to the report, the prototype blockchain network layer of Inthanon-LionRock was built on Hyperledger Besu by ConsenSys, a company founded by Ethereum co-founder Joseph Lubin. This raises a potential question about whether mBridge will have strong compatibility with the Ethereum mainnet and whether it will interact with Ethereum's rich ecosystem in the future.

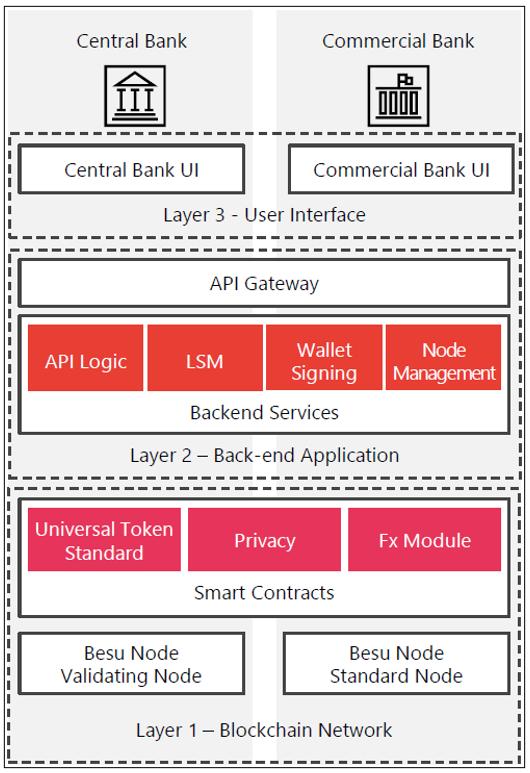

The system architecture of mBridge consists of three layers:

Core Layer: This layer includes the blockchain distributed ledger technology and its related data, as well as the implementation layer for smart contract logic programming.

Backend Application Layer: This layer provides identity verification, access permissions, routing functions, wallet signing, key management, foreign exchange mechanisms, and more for the core layer.

Frontend Layer: This layer provides interfaces for accessing the core system and offers the necessary functions to end users.

In terms of technical principles, mBridge still follows the foundation of the Inthanon-LionRock project. It employs a "corridor network," where all participating banks operate their own nodes in both domestic networks and the corridor network, with only central banks having the core management rights over the nodes. The use of blockchain and distributed ledger technology ensures that the entire link can maintain sufficient security.

On the corridor network, through tokenized assets, parties can transact in a peer-to-peer manner without the need for intermediary accounts. This allows the platform to seamlessly provide tokenized PvP (Payment vs Payment) transfers across different currencies and jurisdictions.

In cross-border payments, the amount of digital currency exchanged by both parties will be reflected in the corridor network, with the mapped product also known as "Depository Receipts." From the perspective of the core layer, the central bank can gain detailed insights into the operation of digital currencies on the corridor network.

In simple terms, if Bank A in Country A needs digital currency from Country B and exchanges 100 million, then 100 million in depository receipts will appear on the corridor network. Depository receipts in the corridor network are universal, allowing for more efficient exchanges between currencies participating in mBridge. If Bank C needs 50 million digital currency from Country B, Bank A can complete the transaction through depository receipts on the corridor network. It is worth mentioning that depository receipts are merely certificates and cannot circulate directly; currency circulation in each country still requires the exchange of corresponding digital currencies. This scenario is more suitable for wholesale digital currency applications.

What effect does mBridge ultimately aim to achieve?

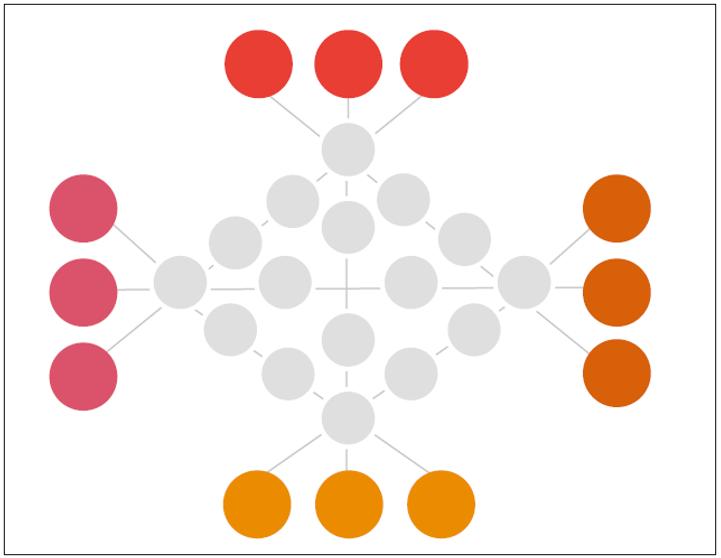

The report presents two diagrams to illustrate the efficiency improvements mBridge brings to cross-border payments. The traditional correspondent bank cross-border payment model:

This model requires passing through multiple nodes in multilateral transactions, with different countries and hidden policy restrictions. This is also the currently popular SWIFT model. Although SWIFT has introduced products like SWIFT GPI and SWIFT Go in recent years to enhance the settlement efficiency of the entire network from several days to minutes, the underlying logic remains unchanged, and transaction efficiency and regulatory risks are still lacking.

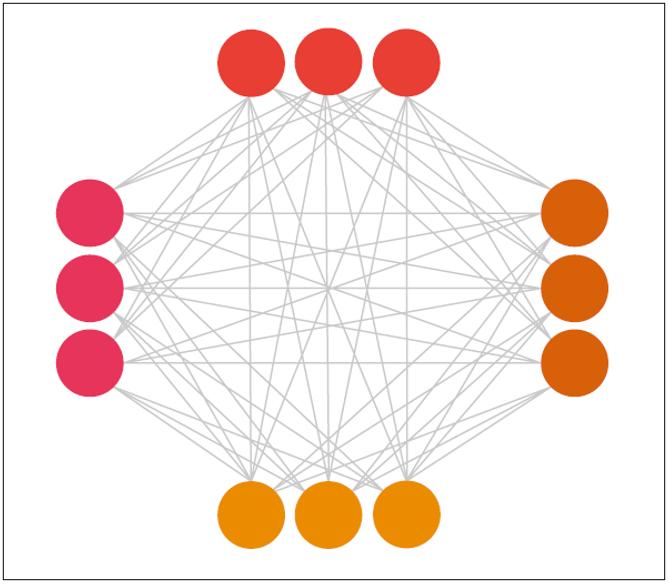

The mBridge transaction model is illustrated in the following diagram:

The multilateral model allows for direct peer-to-peer transactions on the corridor network, eliminating intermediaries, with transaction speeds reaching seconds. By removing many intermediary steps, costs can be significantly reduced, foreign exchange operation risks eliminated, transparency increased, and regulatory work minimized.

I believe that under the SWIFT model, intermediaries merely transmit information, while actual transaction execution requires bilateral banks to operate according to a unified messaging system. However, mBridge cannot be simply termed a digital currency version of SWIFT; it inherently possesses certain exchange characteristics, with central banks relying on the corridor network to facilitate the exchange of depository receipts and digital currencies. Through smart contracts, countries can establish corresponding trading rules and regulatory policies.

According to the latest summary from the mBridge application manual, mBridge can provide a cross-border payment experience that is low-cost, easy to operate, free of exchange rate risks, highly transparent, and with low reporting burdens.

Possible Impacts

For the People's Bank of China, mBridge represents a significant breakthrough point in the global cross-border payment revolution and an important entry point for reshaping the global payment system.

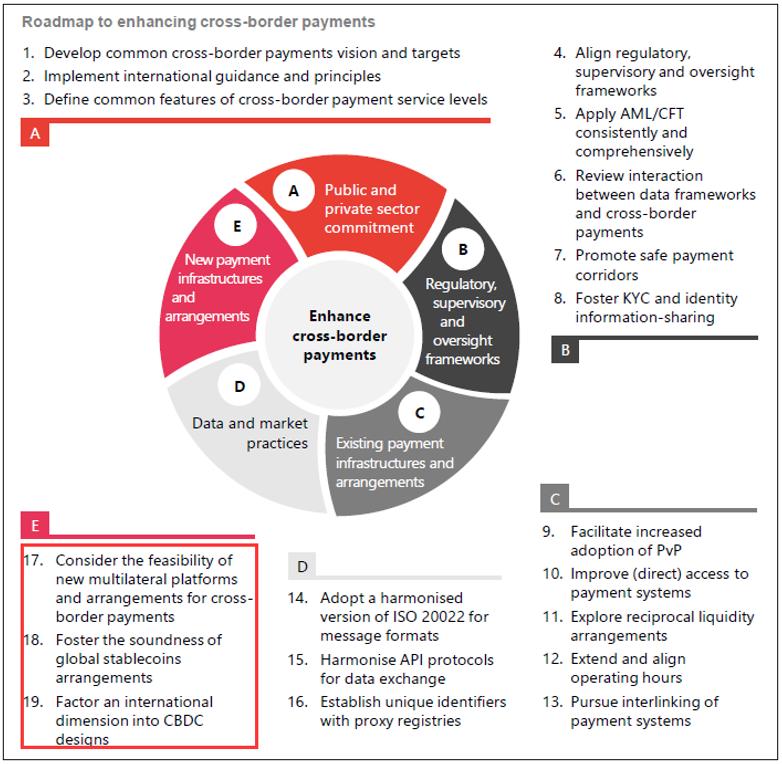

At the G20 meeting held in 2020, the 20 countries reached a consensus to prioritize strengthening cross-border payments as an issue that should be addressed. In the report titled "Enhancing cross-border payments: building blocks of a global roadmap Stage 2 report to the G20," released by the International Bank for Settlements in July 2020, it clearly pointed out the current issues in cross-border payments and proposed 19 directions for solutions.

Among these, exploring new payment technologies, systems, and arrangements includes three directions: considering new multilateral cross-border payment platforms and deployments, observing the development of global stablecoins, and exploring CBDCs.

Among these three paths, the first implies recreating a SWIFT-like system, such as Europe’s INSTEX; the second involves observing the development of stablecoins like Meta's (Facebook) Diem and USDT; the third is projects like mBridge.

In addition to banning stablecoins, the Chinese government has launched CIPS, which makes it quite difficult to break through under the existing SWIFT system. mBridge, on the other hand, starts from scratch as the world’s first cross-border settlement platform built around digital currencies. Regardless of its success, the People's Bank of China is positioning itself strategically.

In contrast, the United States benefits from the strong position of the dollar, making SWIFT favorable to it, so there is no need to recreate a multilateral cross-border payment platform. The U.S. attitude towards CBDCs is extremely cautious, and to some extent, it does not wish to launch a CBDC. At the end of 2019, the U.S. Treasury Secretary stated that the Federal Reserve would not issue digital currency within five years. Earlier this year, the Federal Reserve indicated that it would release a U.S. version CBDC research report in the summer, but it has yet to be published.

Regarding stablecoins, both U.S. officials and tech giants are exceptionally supportive, with most major stablecoins pegged to the relatively stable dollar, such as Diem and USDT. In the payment ecosystem, companies like Square, PayPal, Visa, and Mastercard all support the development of cryptocurrencies to varying degrees.

However, achieving success for mBridge is not an easy task. A report from KPMG indicates that it will take at least ten years for mBridge to be widely adopted. In addition to facing challenges from stablecoins worldwide, the development of mBridge is directly related to the level of enthusiasm from various countries regarding CBDCs. If countries launch CBDCs and recognize and join mBridge, that would be half the battle; the remaining challenge lies in the negotiations and adjustments among countries.

Of course, leveraging the open, fair, and transparent environment of mBridge may accelerate the internationalization of the renminbi, but currency competition is ultimately a reflection of comprehensive national strength and global influence, and mBridge will mirror the strength of a nation.