Messari: What is leading the current DeFi innovation, aside from the concept of DeFi 2.0?

LaaS providers and second-layer protocols should not be defined as characteristics of "DeFi 2.0." In this rapidly evolving field, things should not be casually labeled with simplistic tags.

LaaS providers and second-layer protocols should not be defined as characteristics of "DeFi 2.0." In this rapidly evolving field, things should not be casually labeled with simplistic tags.Author: Chase Devens, Messari

Compiler: Pingfeng, The Path of the Metaverse

After a long period of stagnation, DeFi has re-emerged in the main narrative of the crypto space. The renewed interest in DeFi is largely due to the controversial term "DeFi 2.0" proposed by the anonymous developer Scoopy Trooples from Alchemix Finance. In a recent tweet, Scoopy emphasized some second-generation protocols built on the foundational innovations created by first-generation DeFi protocols (such as MakerDAO, Uniswap, Compound, and Yearn). This classification sparked controversy over the categorization of DeFi protocols and diverted attention from the actual changes happening behind the scenes. On Twitter, we see a chaotic scene where everyone is asking questions related to their favorite OlympusDAO fork projects.

Rather than debating the naming of this phenomenon (DeFi 1.0 or DeFi 2.0), let's take a step back and examine the macro themes driving the latest wave of DeFi innovation. A year ago, such reports would have covered trends like vampire attacks and issuance strategies. Today, in addition to discussing automation, enhancing or extending existing DeFi economic models, we will also explore the emergence of Liquidity-as-a-Service (LaaS) protocols.

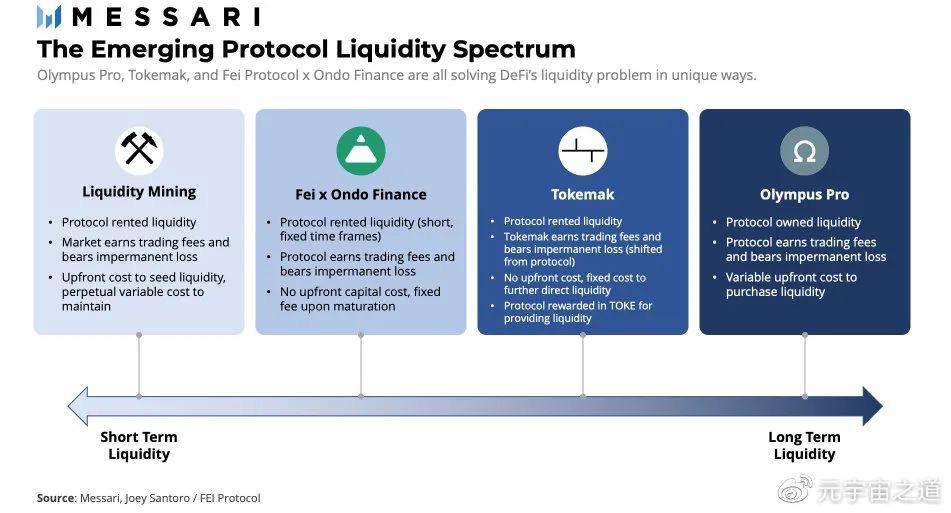

Liquidity-as-a-Service

Liquidity mining was the core and soul of the DeFi summer of 2020, but it has recently fallen out of favor as DeFi protocols struggle to cope with the consequences of capital providers extracting value from their systems. The liquidity mining model provided short-term incentives for liquidity providers and generated permanent costs on the protocol's balance sheet. As a result, projects realized they needed better systems to ensure sustainable liquidity while adjusting long-term incentives for investors. As this issue became more widely recognized, projects began focusing on LaaS. With LaaS providers, protocols can either purchase their liquidity directly from the market or rent liquidity from protocols designed to provide the best quality at the lowest cost.

Olympus Pro

Olympus DAO is the first project to utilize a novel bonding mechanism to create an alternative to the "liquidity mining" model. By issuing its native token OHM at a discount, Olympus is able to purchase LP positions from the market, creating "protocol-owned liquidity" (POL). The recent launch of Olympus Pro (which introduces Olympus's bonding model to the broader DeFi ecosystem) marks the birth of the first LaaS product in DeFi. Olympus Pro provides projects with customized implementations of the Olympus bonding mechanism while also introducing new demand channels for their native tokens. Projects purchasing their liquidity will earn revenue from trading fees but will also bear the impermanent loss (IL) associated with price fluctuations. This approach may be best suited for large projects with less price volatility to minimize IL.

Tokemak

Unlike Olympus, Tokemak is a protocol specifically designed for liquidity provision. Broadly speaking, Tokemak acts as a decentralized market maker. The native token TOKE represents tokenized liquidity, which is used to influence the liquidity direction across DeFi. Protocols earn TOKE rewards by "seeding" liquidity into the Tokemak ecosystem and can influence liquidity direction by staking their TOKE. Since liquidity is ultimately controlled by Tokemak, it retains the trading fees associated with the controlled assets but also bears the impermanent loss. From the protocol's perspective, this approach is similar to liquidity mining; the protocol is still "renting" liquidity but does not earn trading revenue and is not affected by IL. However, protocols earn native TOKE rewards for participating in liquidity rather than incurring permanent costs to maintain liquidity.

Fei Protocol x Ondo Finance Partnership

In addition to revamping its core stablecoin protocol, Fei Protocol recently announced plans to collaborate with Ondo Finance to provide affordable, short-term LaaS options for DeFi. The protocol will be able to deposit their native tokens into Ondo's liquidity vault for a specific period, pairing them with newly minted FEI, which will then be sent to an AMM for liquidity provision. The Fei x Ondo design is attractive for projects looking to generate on-demand liquidity without upfront costs to acquire liquidity on the other side. Fei will charge a small fixed fee for providing the other half of the liquidity position upon the vault's maturity. As the project itself acts as a liquidity provider, it is entitled to collect trading fees but also faces potential impermanent loss. At the end of the term, Ondo will return the provided token liquidity minus trading fees (positive) and IL (negative). This strategy offers protocols a new way to provide liquidity at a very low cost over a short period.

Overall, LaaS providers are introducing methods to create sustainable liquidity for protocols at a lower cost. While each option has its pros and cons, it is becoming increasingly clear that the current system needs to move away from reliance on liquidity mining, and LaaS is in the early stages of this process.

Second Order Protocols

The second category of projects reshaping DeFi is known as "second-order" protocols. Leveraging the composability of DeFi, these projects build on existing DeFi infrastructure to automate, enhance, or extend existing DeFi economic models and processes. Since they sit on top of existing "money Legos," their utility comes at the cost of multiple risks.

Automaters

The "yield-as-a-service" platform created by Yearn provides projects with an automation strategy to adapt to other specialized functions in DeFi: identifying a time or gas-inefficient process and packaging it with minimal fees, thereby making the ecosystem more convenient and efficient. Several projects are currently being built to automate specific micro-processes within DeFi. Popsicle Finance uses assets as LP positions and manages liquidity across multiple exchanges and Layer 1s. Convex Finance recycles $CRV and Curve LP tokens to enhance rewards, trading fees, and governance functions. Although it is a somewhat older project (in crypto terms), Pickle Finance provides automatic compounding services for yield aggregators that lack the native feature of auto-compounding. Projects offering automation services have emerged, demonstrating that if specific problems are not fully addressed by a dominant protocol, new participants will step in to complete the work.

Enhancers

The first iteration of DeFi protocols created several 0-to-1 innovations, which now serve as the cornerstones of programmable financial systems. Some of the most prominent examples include Maker (Collateralized Debt Position or CDP), Compound and AAVE (decentralized interest markets), Uniswap (automated market maker), and Yearn (yield aggregator). Unlike these first-generation DeFi protocols, "model enhancers" do not actually introduce any new operational models to DeFi. Instead, they recycle the outputs of existing protocols to provide end-users with a more optimized model.

Source: Abracadabra.money

One of the fastest-growing projects last month, Abracadabra.money, is an excellent example of using model enhancer strategies to create CDPs from yield-bearing assets. The CDP model was originally introduced by MakerDAO as a way to create a trustless credit system. Users utilize various over-collateralized vaults to mint the protocol's native stablecoin Dai. A common criticism of Maker is the capital inefficiency of its CDPs, as their assets remain locked in vaults without earning any interest. To improve the efficiency of the CDP model, Abracadabra uses existing yield-bearing assets as collateral to mint its native stablecoin MIM. This not only puts users' idle assets to work but also provides deeper liquidation support for borrowers. As the collateral of Abracadabra continuously generates interest and increases in value, the probability of liquidation decreases over time but never reaches zero. Although model enhancers like Abracadabra do not introduce any new fundamental elements to DeFi, these projects find product-market fit by improving capital efficiency.

Extenders

Model extenders introduce innovations similar to the 0-to-1 innovations created by first-order protocols, generating new overall value for the entire system. Unlike their foundational counterparts, these primitives can only be realized through the use of DeFi protocols in the stack.

Alchemix Finance is an example of a model extender. At first glance, Alchemix's use of CDPs built on yield-bearing assets appears very similar to Abracadabra. However, the subtle difference allows Alchemix to create a capital-efficient, over-collateralized borrowing model that is unaffected by liquidation. In the Maker/Abracadabra model, liquidation is always a possibility because the value of their collateral is priced in a different underlying asset than the issued stablecoin. Unlike Maker and Abracadabra's multi-collateral stablecoins, Alchemix's loans are synthetic versions of the underlying collateral, allowing them to be priced in the same underlying asset. For example, ETH loans are issued in the form of alETH, a synthetic asset pegged to the price of ETH. This enables Alchemix to eliminate price risk from its model and ensure that there is no possibility of liquidation. Therefore, fully collateralized assets can be utilized throughout DeFi to provide a continuous source of loan repayment. While many consider "self-repaying loans" to be the primitive of Alchemix, the true extension is the ability to absorb opportunity costs (the opportunity costs caused by choices of consumption or saving).

Another group of model extenders adopts DeFi derivatives and deconstructs them into independent parts. Examples of such projects include Pendle and Tranche Finance. This optionality provides users with more customization and hedging strategies. Given their high level of innovation, the number of model extenders is relatively small compared to model automaters and enhancers. However, the unique attributes of these projects can serve as seeds for creating "killer applications" in DeFi that bring the masses into the space.

Compound Risks

The re-collateralization used by model automaters, enhancers, and extenders does not come without costs. The composability of these second-order protocols leads to multiple (compound) risks, which are no longer controlled solely within the protocol. If the protocol generating their inputs is attacked, the second-order protocol will also fail. This creates a house of cards structure, where the failure of any foundational pillar can cause the entire tower to collapse. Under otherwise identical conditions, the value added by second-order protocols is offset by the risks introduced by composability. While many projects adopt a worry-free marketing approach, it is important to understand that in second-order protocols, risks are more apparent than ever.

Other Cases and Conclusion

The above groupings do not comprehensively cover the innovations in the field. That is to say, a protocol may be a pioneering innovation but may not fit into the categories above. One example is Rari Capital's Fuse product. Fuse adopts the interest pool model of Compound and AAVE and applies it on a nuanced level, allowing users to create an interest pool from any asset combination using reliable price oracles. Although it does not operate as a LaaS provider and does not directly build on other protocols, it still provides meaningful innovation by introducing a permissionless interest pool structure.

LaaS providers and second-order protocols should not be defined as characteristics of "DeFi 2.0." In this rapidly evolving field, we should not casually label things with simplistic tags. We can leave this work to future historians. If we are lucky, we will endure a whole year before addressing the inevitable "DeFi 3.0."

Risk warning

Risk warning Risk warning

Risk warning

Popular articles