In-depth | A lengthy article deconstructing the design and future of the synthetic asset track

The synthetic asset track has immense imagination, potentially achieving true cross-chain capabilities, with strong product scalability. The oracle pricing trading model has limitless potential. Existing products are not mature enough, but they can evolve in multiple directions such as collateral, liquidation algorithms, synthetic models, trading models, trading risk control algorithms, and derivatives. Mature synthetic asset products can exponentially enhance the influence of DeFi.

The synthetic asset track has immense imagination, potentially achieving true cross-chain capabilities, with strong product scalability. The oracle pricing trading model has limitless potential. Existing products are not mature enough, but they can evolve in multiple directions such as collateral, liquidation algorithms, synthetic models, trading models, trading risk control algorithms, and derivatives. Mature synthetic asset products can exponentially enhance the influence of DeFi.Author: Prophet Lab

Preface:

The synthetic assets analyzed in this issue are known as the most complex and difficult-to-understand track in the DeFi field. Therefore, no part of the article should be missed. The author will try to use straightforward descriptions to reduce reading difficulty, avoiding overly obscure algorithmic formulas. However, understanding the synthetic asset track still requires some knowledge of infrastructure-type products and basic concepts.

The good news is that this article will explain various types of DeFi products during the analysis, helping readers with a weaker foundation to gain a comprehensive understanding at once.

This article is not positioned as an investment research report; it is more of a product design solution-oriented study, which may be relatively dry but useful.

What are synthetic assets?

Let’s briefly introduce what synthetic assets are and what problems they solve.

1. What is cross-chain? What problems does it solve?

First, let’s think about this question: What exactly is cross-chain doing? Why do we need cross-chain?

Many people would quickly answer—breaking the blockchain islands; the blockchain world needs to communicate with other worlds (making grand promises).

Yes, due to the isolation problem of blockchains, people are eagerly anticipating the emergence of a blockchain world that is decentralized, censorship-resistant, and capable of trading everything.

Thus, ecosystems like Polkadot and Cosmos have become increasingly prominent. Until now, although there hasn’t been much substantial progress, these projects have established sufficient value consensus in the secondary market.

However, as cross-chain technology has developed, whether it’s the notary mechanism, sidechain mechanism, or Polkadot’s relay chain + parachain + bridging chain model, there are many issues.

Either they are not decentralized enough, or they are too difficult.

2. Synthetic assets may be the most feasible cross-chain solution

Since the current cross-chain solutions do not make much sense, what can break the value isolation in the blockchain world?

The goal of synthetic assets is to trade any asset. Although the current synthetic solutions do not share attributes other than value fluctuations with actual assets, from the perspective of demand, most users’ need for "assets" often only involves enjoying the profits brought by price fluctuations.

Therefore, the author boldly believes that synthetic assets may be the most feasible and decentralized asset cross-chain solution at present (information cross-chain is not within the defined scope).

3. How do synthetic assets work?

(1) Over-collateralization model

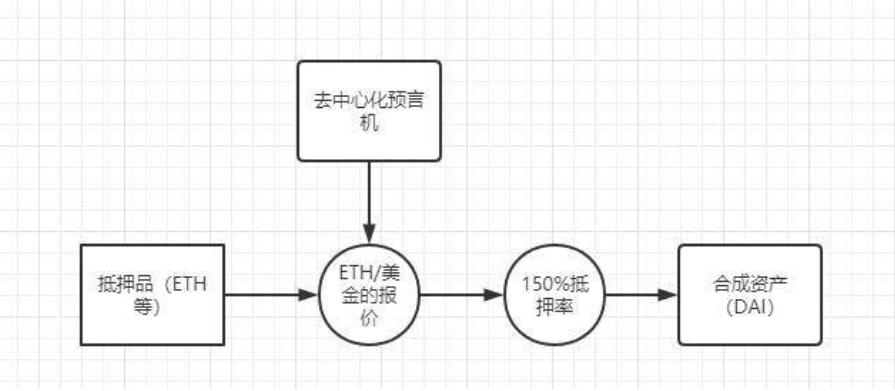

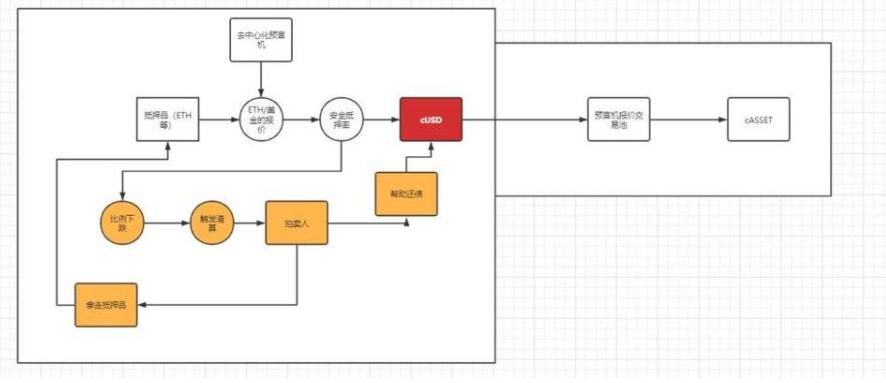

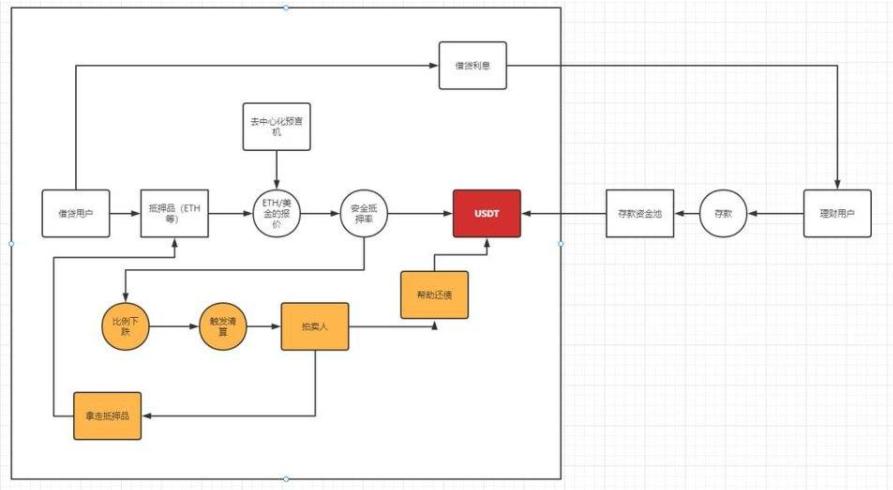

Strictly speaking, the pioneer in the field of synthetic assets is MakerDao, as DAI essentially represents a synthetic form of off-chain assets on-chain.

Users collateralize ETH and obtain the price of USD/ETH from decentralized oracles to create a USD stablecoin—DAI, using a 150% over-collateralization model.

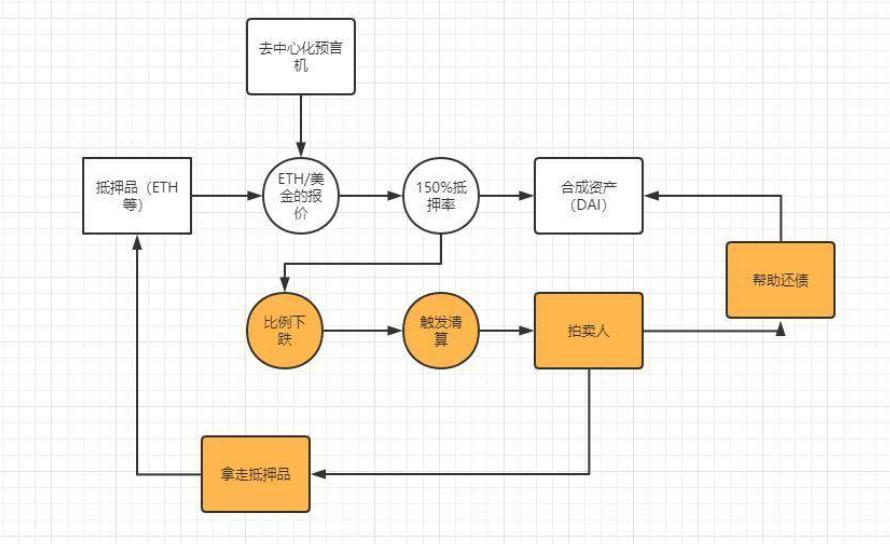

From the above image, we can clearly see that MakerDao has synthesized a USD stablecoin on-chain through an over-collateralization model. Since DAI's price does not fluctuate significantly, when the price of the collateral drops, the collateralization ratio decreases. At this point, when the collateralization ratio triggers the liquidation threshold, the collateral will be publicly auctioned in the market, and auction bots will help the collateralizer repay debts and take away the collateral.

The orange part represents the liquidation process:

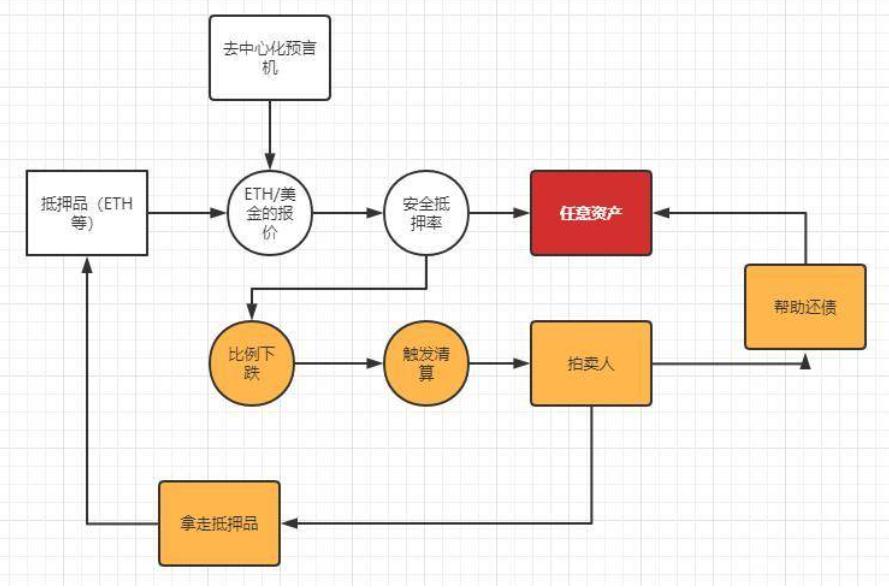

This is the complete process of collateralizing synthetic USD. Therefore, we can find that as long as external oracles can obtain stable asset quotes in a decentralized manner, theoretically, we can synthesize any asset.

Mirror does this; on the synthetic asset project Mirror, users can collateralize UST (a semi-algorithmic stablecoin from the Terra ecosystem) to generate various synthetic assets. Users can trade various synthetic assets, including stocks and gold, on Mirror's built-in AMM.

(2) Global debt model

The largest project in the synthetic asset track, Synthetix, has a slightly different solution from MakerDao and Mirror. In addition to synthesizing certain assets through over-collateralization, Synthetix has established a new global debt mechanism based on a quote trading model. This allows Synthetix users to first synthesize the USD stablecoin sUSD and then use sUSD to trade any supported synthetic assets like stocks and foreign exchange with zero slippage and infinite liquidity.

This global debt model is also the most complex part of synthetic assets. Let’s understand the global debt model with this mindset.

If we are product managers, and the requirement is to create a trading market for synthetic assets that does not consider liquidity and relies on external quotes, how should we proceed?

First, we need to understand that if the price comes entirely from external quotes, it means that this trading market has no pricing power. No pricing power means that the trading demand within the platform needs to be as similar as possible to the trading demand in the external market. This ensures that there is no premium loss in the internal market.

Synthetix does this: it borrows the quote-driven model from traditional trading, where a large market maker provides quotes to the market, and the counterparties for buying and selling users are the market maker rather than each other. Synthetix does not play the role of this large centralized market maker. Therefore, its solution is global debt:

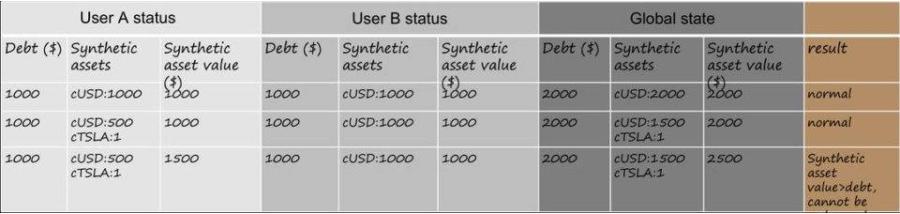

Example:

Assume that user A and user B each collateralize to generate 1000 USD of cUSD, and the current global debt is 1000 USD + 1000 USD = 2000 USD. User A creates a position in Tesla stock worth 500 USD. A day later, Tesla stock rises by 100%. The global debt then becomes 1500 USD + 1000 USD. At this point, when A and B want to redeem their assets, they need to share the additional 500 USD of debt, so user A profits 500 - 500/2 = 250 USD, while user B loses 500 - 500/2 = 250 USD.

This is the common debt warehouse model used by traditional synthetic asset projects.

4. Problems in the synthetic asset track

However, whether it is the over-collateralization model of MakerDao or the over-collateralization + global debt model of Synthetix, there are actually many problems. In our discussion, we will subjectively divide synthetic asset products into the two types mentioned above.

(1) Problems with the staking lending model

The model of collateralizing ETH to borrow DAI is an over-collateralization model, and the demand may have multiple forms:

- A. Users do not want to sell ETH but are currently short on cash. Therefore, they execute this operation. Essentially, they are bullish on ETH and bearish on synthetic assets. Because if users are just short on cash and not bullish on ETH, they could simply sell ETH immediately. If the synthetic asset is a volatile asset like TSLA or XAU, the synthetic asset users should essentially be bullish on the collateral and bearish on the synthetic asset. The likelihood of this demand occurring is low; the best approach is to set the collateral as a stable asset like Mirror does. This way, the price fluctuation risk faced by synthetic asset users will be greatly reduced.

- B. Shorting a certain asset can be done using other capital-efficient methods; the over-collateralization form is simply not flexible enough. Therefore, the actual demand of most synthetic asset issuers should be arbitrage.

There are two types of arbitrage here: the first is to mine by staking to obtain platform tokens, and the second is to synthesize assets based on oracle prices and then capture the external market premium.

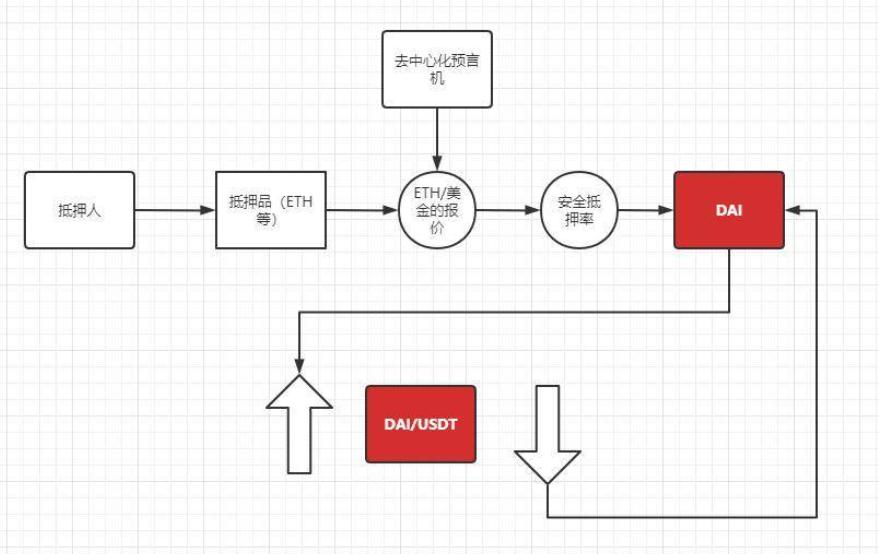

Specifically, as shown in the figure:

Taking DAI as an example, when the demand for DAI in the blockchain world rises, the DAI/USDT trading pair will generate a premium, for example, 1 DAI = 1.1 USDT. At this time, using ETH to collateralize and synthesize DAI, and then exchanging it for 1.1 times USDT in the secondary market. When the supply of DAI increases, the price will revert, and then the 1.1 times USDT can be exchanged back for DAI to repay the debt, capturing the profit.

This is just the simplest example; there are many more variations of arbitrage, which will not be elaborated here.

From this example, we can see that under the staking lending model, the price of synthetic assets on external exchanges can easily generate premiums, and this premium may be the main driving force for most collateralizers.

MakerDao is relatively better, as it only needs to maintain the liquidity of DAI. However, every time Mirror launches a new synthetic asset, it must maintain the liquidity of another asset; otherwise, the scarcity of liquidity in the external market will create huge arbitrage opportunities.

Therefore, we can see that the trading pairs incentivized by Mirror's liquidity mining are numerous. This will significantly increase the operational pressure on the operating team. In simpler terms, this form is more suitable for teams that are "wealthier." During my interactions with several investors, many believe that the synthetic asset track needs more financing.

This is indeed a problem, but it is not entirely accurate, as this issue mainly affects synthetic asset projects based on the staking lending model.

- C. The over-collateralized synthetic model poses a global liquidation risk in extreme market conditions. Taking the events of March 12, 2020, and May 19, 2021, as examples, when the collateral experiences a significant drop in a short period, the speed of collateral liquidation will exceed the speed at which users can add collateral or repay debts. The act of liquidation itself will also exacerbate the price drop of the collateral; when a large amount of collateral is liquidated in a short time, the assets with poorer liquidity are affected more severely.

Moreover, this global liquidation risk is particularly severe when both the collateral and synthetic assets are volatile assets. Therefore, most products set their minimum collateralization ratios relatively high, and in the liquidation mechanism, to cope with the occurrence of death spiral events, they often adopt delayed quoting or partial liquidation methods.

(2) Problems faced by the global debt + staking lending model

This form essentially turns all collateralizers into the "market makers" described in the quote-driven model. Collateralizers become the counterparties to traders, and while collateralizing, they are also betting against the traders' profitability. When traders' profits are negative, the collateralizers, or users issuing cUSD, benefit from debt relief. When traders' profits are positive, the collateralizers, or users issuing cUSD, face increased debt.

- Most collateralizers overlap with traders; users who make correct judgments earn little, while users who do not operate may incur losses.

- The difficulty of adding new trading targets will greatly increase, affecting the scalability of trading targets.

- The problem of front-running trades caused by complete reliance on oracle quotes is severe.

Is this reasonable? We can't help but ask this question.

The original intention of users trading synthetic assets is to hope to trade various valuable assets on-chain without censorship, without regulation, and in a decentralized manner. The purpose of synthetic asset protocols is to bring more valuable asset targets to the blockchain world.

However, if users need to bear this "debt risk," why would they go to these platforms to synthesize?

This is also the dilemma faced by these synthetic asset protocols at present. When market sentiment is strong, and the platform token price and liquidity incentives are rich enough, debt risk is not a primary concern for users. However, when the price of the platform token itself suffers, the liquidation risk faced will be catastrophic, with collateral prices dropping while synthetic asset prices rising. Other users who have synthesized stablecoins also cannot escape the punishment of global debt.

We have observed that some globally debt-type synthetic asset projects with initially poor liquidity encountered similar problems during their early stages. Moreover, the largest global debt synthetic asset project—Synthetix—has been trying various methods to solve this issue.

Additionally, the Synthetix community once proposed creating a debt mirror index asset, which would create an index composed of five parts (wBTC, wETH, DAI, DPI, and LINK) to simulate the composition of the debt pool* (with a 10% reduction in USD). In short, the purpose of this mirror index is to hedge against the volatility brought by global debt, and some even proposed replacing sUSD with sDEBT. This shows how significant the impact of debt volatility issues is.

(3) Overall problems faced by the track:

In addition to the specific problems faced by the two types of synthetic asset projects mentioned above, the overall track also faces some other issues.

- A. The product logic of synthetic asset projects is overly complex, with high costs of contract interaction and user experience.

Taking the largest synthetic asset project, Synthetix, as an example, when you open the PC version of the Synthetix website, it is difficult to directly find a place to trade synthetic assets. This is because Synthetix has separated its synthetic asset trading into another ecological project, Kwenta. Splitting asset issuance and trading leads to a poor user experience for new users. Moreover, the logic of synthetic assets is quite complex, and the costs of contract interaction are high. However, this issue has improved significantly since Synthetix has migrated entirely to Layer 2.

- B. Asset scale is limited

Mainstream synthetic asset projects are all issued by collateralizing platform tokens; even the UST used by Mirror is also issued by single-token collateralization of LUNA. This leads to the issuance scale of synthetic assets being greatly restricted by the market value of the platform token. Moreover, the cost of iteration is very high, and scalability is extremely poor.

Imagine if a synthetic asset project's mission is to introduce off-chain assets to the blockchain world, but the scale that can be introduced is always less than one-fifth or even one-eighth of the market value of the platform token; this is unacceptable.

- C. The overall openness of the product is poor, and the impact of debt risk is significant.

Most synthetic asset projects, although they have trading functions like Uniswap and other DEXs and provide a relatively better trading experience, have poor openness in asset types. Unlike the completely free form of Uniswap, the trading targets of synthetic assets have high requirements. This is mainly because the trading model adopted by synthetic assets is the global debt model. In this model, any new trading target will affect the existing debt pool, making it difficult to achieve sufficient openness, often requiring community governance to add new trading targets.

- D. The trading model is overly complex, and the product usage threshold is high.

Users participating in issuance bear higher risks compared to other lending, stablecoin, and over-collateralization models. This is because the factors affecting collateral liquidation include not only the price of the collateral/synthetic asset but also the global debt. This raises the participation threshold for users. In mature issuance and trading models, users should not have to consider risks other than price fluctuations of trading pairs.

Although synthetic asset projects currently face several significant problems as mentioned above, if these issues can be properly resolved, the advantages of synthetic asset projects will be particularly great.

5. Scalability of synthetic assets

Due to the complexity of synthetic assets themselves and their unique trading models, synthetic asset projects often have the ability to form their own ecosystems.

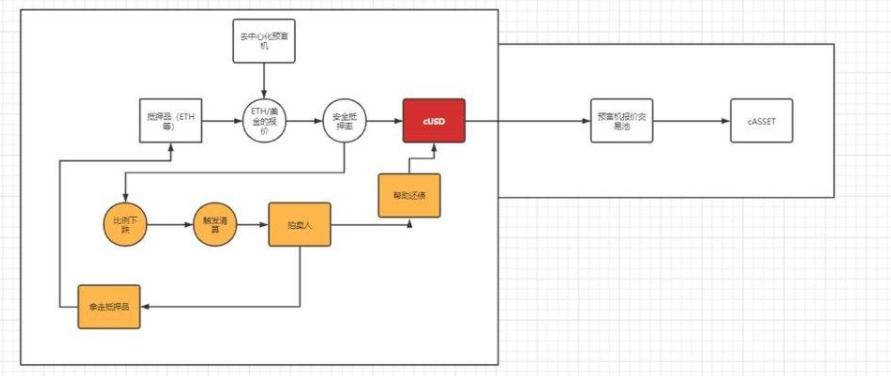

- A. The issuance of synthetic assets can actually include a complete over-collateralized stablecoin issuance module.

As shown in the figure below:

- B. The collateral issuance module of synthetic assets also has similar situations to over-collateralized lending models.

Based on the same flowchart: it only requires adding a deposit pool and replacing the debt of the issued synthetic asset with the funds from the actual deposit pool. Additionally, it can charge extra lending interest.

- C. The trading of synthetic assets is actually a better DEX experience than other products like Uniswap, as it does not require additional liquidity to be added, and market makers do not need to participate in market making, resulting in zero slippage. For example, with an average slippage of 1%, the latest 24-hour trading data shows that under the same trading volume, the trading model of synthetic assets can reduce slippage losses for users by nearly 30 million USD.

- D. Due to the existence of the quote trading model and the global debt sharing model of collateral issuance, synthetic asset projects can easily derive leveraged and contract trading products. Even various secondary options and insurance products can emerge from this system.

Taking Synthetix as an example, its strong scalability helps its ecosystem extend beyond just the issuance of synthetic assets, including the aforementioned Kwenta exchange, Dhedge asset management protocol, etc.

However, this scalability cannot be fully realized on Synthetix. The main reason is that the sunk costs of the product itself are too high. The initial design limits the development of Synthetix and is difficult to change. In the next chapter, we will carefully analyze the problems that exist here and our solutions.

In summary, self-ecosystem synthetic assets cannot be simply understood as a single DeFi project. High scalability is sufficient to help synthetic asset projects have greater potential than other types of projects.

6. Composability of synthetic assets

A significant advantage of DeFi products over traditional financial products is composability. Various DeFi projects can achieve more complex functions through contract calls, maximizing capital efficiency.

Therefore, when assessing the potential of a track, the composability of that track must be considered.

Compared to other tracks, synthetic asset products have become more composable due to their unique product functions.

For example:

- A. The zero-slippage quote trading model is very suitable for helping internal assets like BTC and ETH in the AMM system reduce slippage in trading. For instance, Curve reduces the large trading slippage of DAI/BTC through the form of DAI (stablecoin)/sUSD (1:1 exchange)/sBTC (zero slippage)/BTC (1:1 exchange).

- B. Assets with stronger value consensus issued through synthetic asset platforms can become collateral for other lending-type and over-collateralized stablecoin-type products.

- C. The process of asset synthesis is essentially consistent with the process of collateral lending; therefore, in some other use cases, synthetic asset projects can also play the same role as lending products.

If the synthetic asset track can solve the existing difficulties, there is reason to believe that synthetic asset products will have enormous potential to ignite the market.

Feasible solutions and ideas

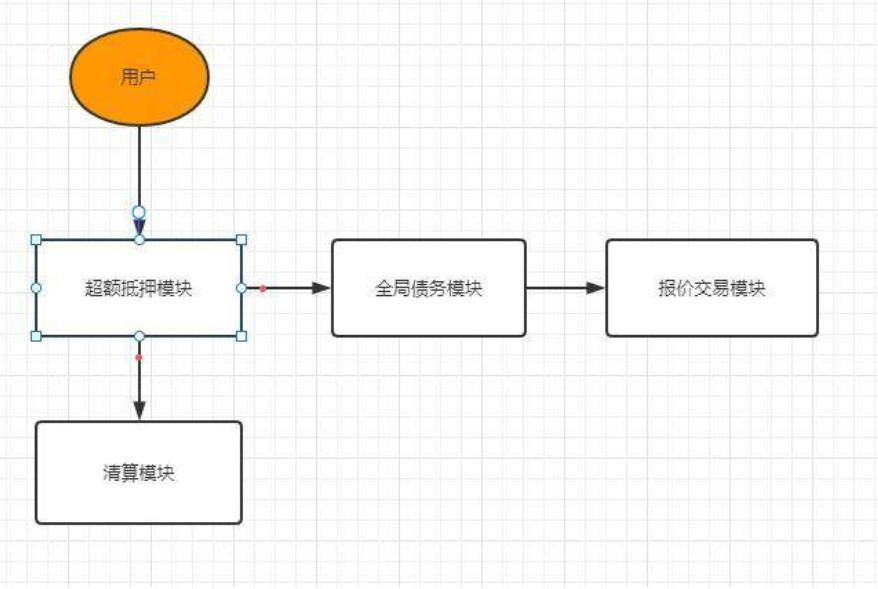

1. Modularize the key components of synthetic assets

Taking the most complex global debt model of Synthetix as an example, we can break down the following diagram into four components:

With this modular thinking, we can more clearly understand the ideas and impacts of the solutions.

2. Trace back the problems and propose solutions

(1) The product logic of synthetic asset projects is overly complex, with high costs of contract interaction and user experience.

This problem is not severe at present. Although reviewing Synthetix's SIP history reveals that Synthetix has proposed many ideas to reduce contract interaction costs, the fundamental issue is that Layer 1 efficiency is too low and costs are too high.

When the main functions migrate to Layer 2 or other more efficient underlying layers, the problem will not be significant.

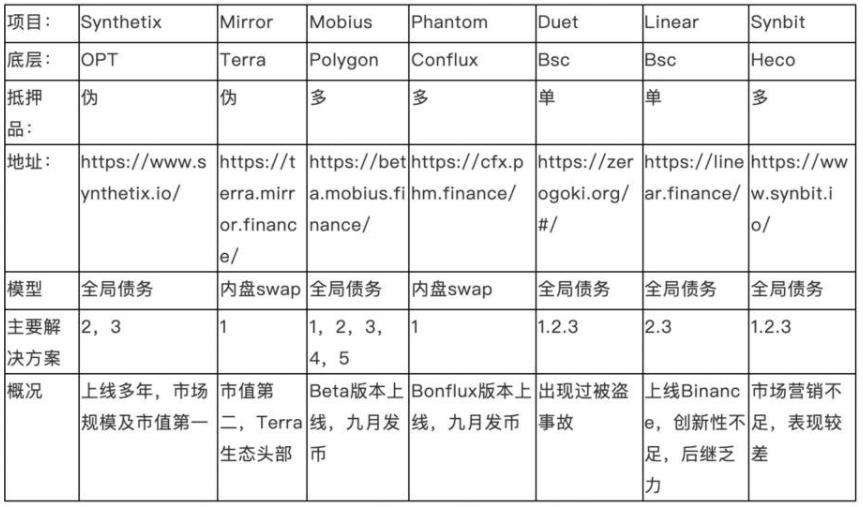

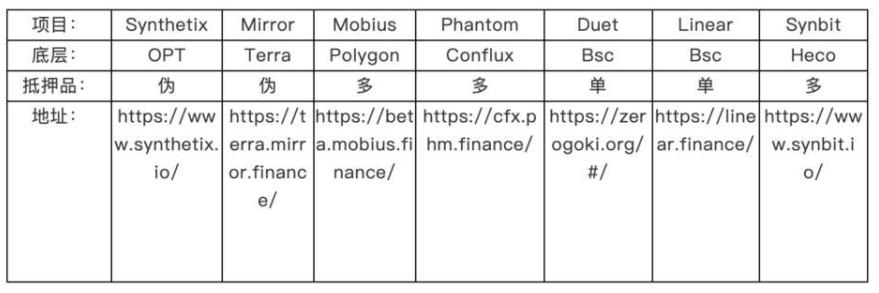

Moreover, this point is particularly evident in emerging synthetic asset projects. The following summarizes the situations of some synthetic asset projects that Prophet has researched:

(2) Asset scale is limited

The solution to this problem is actually quite simple: choose quality assets to support multiple collateral types. However, it should be particularly noted that in the global debt pool model, any new collateral must have the same positioning as the platform token and share the same debt pool.

Only in this way can it be ensured that the synthetic assets issued by the new collateral are expanding the overall asset scale rather than betting against the original debt pool.

The new collateral types for Synthetix face the problem I mentioned; the collateral issued by ETH and BTC is essentially a collateral lending behavior, where the global debt pool of SNX lends sUSD to the debt pools of ETH and BTC.

Thus, even if new collateral is added, the asset scale of the new collateral must still be less than the market value of SNX's minimum collateralization ratio.

The reason Synthetix does not add actual multiple collateral types, according to our research, is that the SNX token contract is highly coupled with the main contract, resulting in "technical debt" that cannot be executed technically.

Furthermore, other collateral types should all be relatively stable external assets rather than internal synthetic assets, as external assets are beneficial for asset scale.

The collateral situations of other products are as follows (models with multiple collateral types that do not fundamentally help asset scale are marked as pseudo):

(3) The trading model is overly complex, and the product usage threshold is high

This problem is the most frustrating one I encountered during usage. The UI quality of most synthetic asset projects is relatively poor. I believe the reason for this is that all projects' UIs lack reasonable prioritization and clear division of usage areas.

In my view, synthetic asset projects should clearly divide product functions into three distinct areas. These three areas are based on the user profiles that synthetic asset projects face.

Essentially, synthetic asset projects should have three types of users:

- The first type of user is the asset issuer and also the collateralizer, who captures the arbitrage space brought by the rising demand for cUSD by bearing the debt volatility risk of collateral issuance.

- The second type of user is the trader, whose demand is to purchase synthetic assets on the synthetic asset platform.

- The third type is the miner, whose goal is to obtain rewards through collateral or trading actions.

In some cases, the attributes of these three types of users may overlap, but organizing the relevant UI design logic based on such profiles should be more reasonable.

I have attached the specific situations of the above projects, and you can research them yourself.

(4) The internal premium issue caused by lack of pricing power

In the fourth section of the first part of this article, we discussed the internal premium issue caused by the over-collateralization model for synthetic assets. There are two approaches to solving this problem:

A. Increase the liquidity of internal trading pairs. When liquidity is greater, the premium impact caused by the same volume of internal demand will be smaller. This solution is consistent with the idea of expanding the overall asset scale. Increasing the value base can reduce the impact of individual operations.

B. Create a larger arbitrage space to encourage arbitrageurs to eliminate the premium.

This solution is similar to the market maker incentive plans of centralized exchanges and liquidity mining incentive plans. It can reduce the arbitrage costs for arbitrageurs through tiered fee structures, which essentially lowers the market-making costs for "market makers."

Alternatively, token incentives can be used to encourage arbitrageurs' arbitrage activities.

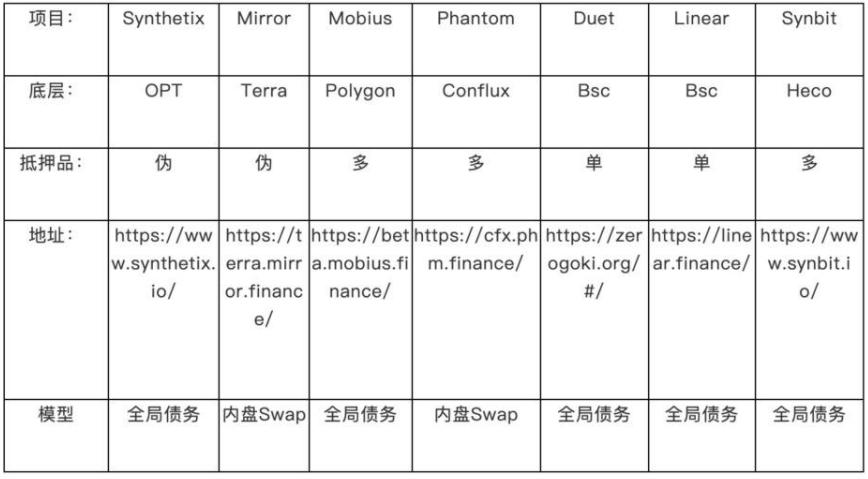

(5) The debt volatility issue caused by lack of pricing power

The above image shows the trading models adopted by these projects: it can be seen that most projects use a global debt model similar to Synthetix. The benefits of this trading model are obvious. However, we have repeatedly mentioned the problems:

The solutions can be summarized in the following five ways:

1: Expand the overall asset scale.

For example, if the position of cUSD within the platform accounts for a larger proportion of the total positions, it means that the impact of other synthetic asset positions on the overall debt will be smaller. Therefore, expanding the overall asset scale essentially reduces the impact of individual debt changes on global debt.

As shown in the figure, when the holding of cUSD is large, even if cTSLA rises by 200%, its impact on global debt remains minimal.

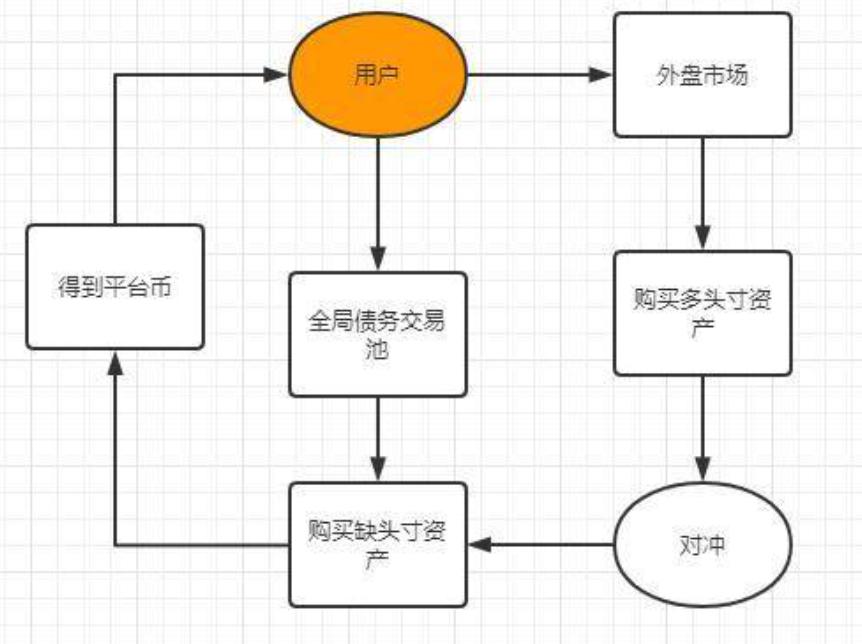

2: Provide reverse assets or shorting functions to adjust the platform's net position.

Because reverse assets are essentially the counterpart of positive assets, when the net position approaches zero, it means that regardless of how the prices of synthetic assets within the platform change, the debt will not increase. This is because all changes in long positions are hedged by changes in short positions.

As shown in the figure, if the synthetic asset debts within the platform include cUSD, TSLA, and iTSLA, then TSLA = iTSLA. Thus, even if TSLA rises by more than 100%, it will have no impact on global debt.

3: Use economic incentives to adjust net positions.

When user B's position in TSLA is much larger than user C's position in iTSLA, the balancing effect of iTSLA becomes negligible. Therefore, economic incentives are a very intuitive way to flexibly adjust based on actual conditions.

The significance of this approach is essentially to create arbitrage space.

Arbitrageurs can purchase shortfall assets on the synthetic asset platform and buy equivalent long assets in the external market to hedge. The platform token incentives minus the transaction fee losses equal the final risk-free profit.

4: Dynamic fees + position fees.

Through the previous solution, we can clearly see that the balancing mechanism of global debt is somewhat similar to the price-reverting mechanism of perpetual contracts to spot prices.

Both create arbitrage space to encourage the reduction of long positions and increase short positions. The core logic is to hope that the net position approaches zero or reduces the proportion of net positions in total positions. Because changes in net positions are the core factors affecting changes in global debt. The smaller the proportion of net positions, the smaller the impact on global debt.

Therefore, the dynamic fee mechanism is applicable to the global debt trading model, just like the position fee mechanism.

The only issue is that this increase in fees effectively increases "slippage," which is not conducive to the interaction between synthetic asset projects and other projects. For example, the large exchange of sBTC between Curve and Synthetix is not very feasible.

However, I believe that in the short term, the composability with some well-known projects is indeed very important. But the mission and demand that synthetic assets carry are incomparable to any other DeFi track projects. Moreover, this slippage will be smaller when the net position is smaller. As the asset scale increases, slippage will also decrease. The impact of composability will also be smaller.

Project parties should still think about the problem from a longer-term perspective. From my experience, the debt risks faced by most projects in the early stages are far greater than the impacts brought by composability.

5: Profitability betting insurance pool.

Earlier, when discussing the global debt issue, we mentioned that "collateralizers have become counterparties to traders, and collateralizers are betting against traders' profitability while collateralizing."

This statement indirectly reflects that global debt can even result in negative new debt situations, even in the case of only one-way assets.

This is because, when extending the time dimension, even if some users hold long positions and can profit, many other users may hold long positions at high levels and sell at low levels. Thus, global debt may decrease instead of increase.

In many mature trading markets, most actual users indeed lose money. If a betting pool could be provided based on previous phase data after the data of synthetic asset projects stabilizes.

Users participating in the betting pool can inject cUSD to bet on the changes in global debt in the next phase.

If global debt increases, the betting pool pays the new amount.

If global debt decreases, the debt rewards that should have been given to collateralizers are given to users participating in the betting pool.

The purpose of this approach is to create a global debt index product, allowing third-party users to bet on this risk.

The benefit is that it can allow collateralizers to bear less risk, similar to collateralizers in pure over-collateralization models like Mirror and MakerDao.

The difficulty lies in product cycle design, price tracking, pricing methods, and handling situations where full compensation cannot be made.

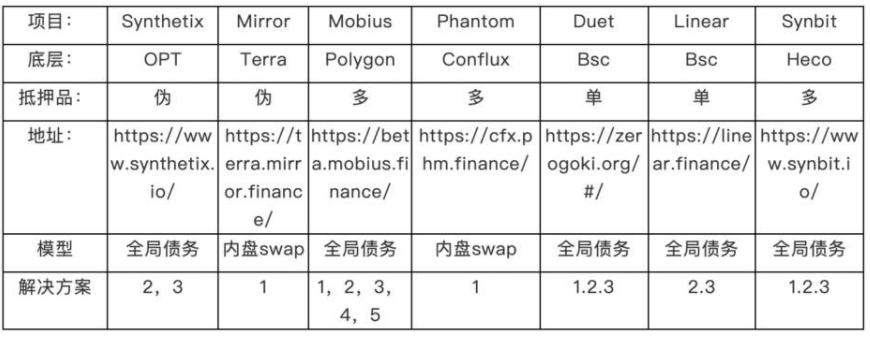

These are some of the solutions that Prophet has considered. We have reviewed the aforementioned projects and marked the adoption of similar solutions below.

In addition to the projects mentioned above, UMA can also be considered part of the synthetic asset track. Additionally, Duet adopts a similar algorithmic stable form in its synthetic asset issuance model. Prophet's research on this part is not in-depth, so it will not be elaborated here.

Summary

In summary, the synthetic asset track still faces many problems, but there are corresponding solutions.

However, due to the overall architecture being relatively complex, early projects often have many technical debts due to a lack of experience in the initial design. From the current performance, these technical debts have become significant constraints on the development of these projects.

Therefore, the scalability of architectural design and the scalability of product functions will be key focuses for Prophet in the future.