Bringing interest rate swaps into DeFi: Understanding the mechanisms and application scenarios of the fixed income platform Strips Finance

Strips Finance converts floating interest rates to fixed rates through hedging and other methods to lock in returns. Its first DeFi product is the "Interest Rate Swap Trading System" on Ethereum.

Strips Finance converts floating interest rates to fixed rates through hedging and other methods to lock in returns. Its first DeFi product is the "Interest Rate Swap Trading System" on Ethereum.Author: Li Ke

In June of this year, the interest rate derivatives trading platform Strips Finance completed a $2.5 million seed round financing led by Crypto.com Capital, Finlink Capital, and Mechanism Capital, with participation from DeFiance Capital, Pnyx Ventures, DeFi Alliance, Magic Ventures, and Darren Lau.

In traditional finance, interest rate swap transactions (such as converting floating rates to fixed rates) account for 80% of the over-the-counter derivatives trading volume, but such interest rate derivatives trading platforms have only just begun to emerge in the current DeFi landscape.

Strips aims to become the largest stable income trading platform, where "stable" refers to locking in returns by converting floating rates to fixed rates through hedging and other methods. The first DeFi product launched by Strips is the "Interest Rate Swaps" (IRS) system built on Ethereum.

Strips not only introduces the concept of interest rate swaps from traditional finance to blockchain but also creates a "perpetual interest rate swap" system with leverage ranging from 1 to 10 times. Users can hedge interest rate returns, leverage liquidity mining returns, and engage in interest rate arbitrage through this system.

The interest rate swap market is enormous, with the U.S. interest rate swap market trading volume being 24 times that of stock trading volume. The Strips team hopes to leverage its extensive experience in financial markets to make it an important part of decentralized finance by positioning itself in the interest rate trading market.

A bit abstract? What is an Interest Rate Swap (IRS)

An Interest Rate Swap (IRS) is essentially a contract and a type of derivative. To simplify understanding, one can think of the fixed rate as the opening price and the floating rate as the closing price.

If one expects future interest rates to rise, they can go long by buying at a fixed rate (Pay Fixed) when opening a position and selling at a floating rate (Receive Floating) when closing the position to gain profit.

If one expects future interest rates to decline, they can go short by selling at a fixed rate (Receive Fixed) when opening a position and buying at a floating rate (Pay Floating) when closing the position to gain profit.

Strips allows users to open positions with leverage of 1 to 10 times, enabling users to leverage a relatively small margin to amplify their returns, which also increases risk.

In the market, borrowers and lenders have a demand for swapping fixed and floating rates in different directions based on the need for risk hedging, value preservation, and arbitrage, thus creating interest rate swaps.

In summary, interest rate swaps are popular and highly liquid financial derivative instruments where counterparties exchange fixed and floating rates based on a specified notional amount. Converting fixed rates to floating rates can achieve hedging, speculation, and risk management purposes. Interest rate swaps can reduce or increase exposure to interest rate volatility risk or obtain lower or higher rates than without the swap.

The Role of the Strips Interest Rate Swap Platform

For users, using Strips' interest rate swap platform can achieve specific objectives:

For liquidity mining providers, locking in high APY%

When investors expect mining yield rates to decline unilaterally and wish to obtain stable returns, they can short in the IRS, selling at a fixed rate when opening a position (i.e., receiving a fixed rate), keeping the notional amount of the position consistent with their actual mining staking amount and setting leverage, and then buying at a floating rate to close the position (paying the floating rate), thus "converting" actual returns from floating rates to fixed rates.

For DeFi lending users, hedging risks to lock in interest

When borrowers believe that market interest rates will rise unilaterally over a certain period, they can go long by buying at a fixed rate (paying the fixed rate) when opening a position in the IRS and selling at a floating rate (receiving the floating rate) when closing the position. The profits gained from going long in the IRS can hedge against losses incurred from rising rates in actual borrowing, achieving the effect of paying interest at a fixed rate.

For arbitrageurs, engaging in high-leverage interest rate trading

For pure arbitrageurs who are neither borrowers nor lenders, if they expect floating rates to decline over a certain period, they can short floating rates on Strips using leverage (i.e., receiving fixed, paying floating); if they expect floating rates to rise, they can perform the opposite operation to go long on floating rates (i.e., paying fixed, receiving floating). Strips amplifies the returns and risks for arbitrageurs through 1-10 leverage.

Usage Scenarios of the Strips Interest Rate Trading System

Scenario 1: Easily going long or short on interest rates with up to 10 times leverage

With just a few simple steps, users can engage in interest rate trading with high leverage.

Connect to Metamask wallet

Select market (Nerve > 3pool)

Input position size

Choose leverage multiple (1--10x)

Choose to open a long/short position

Confirm the transaction on Metamask

If a trader currently holds a long position, they will benefit from rising market interest rates. Market interest rates are entirely determined by the supply and demand of market participants. Conversely, if a trader currently holds a short position, they will benefit from falling market rates.

Scenario 2: Hedging to lock in high APY%, avoiding a decline in APY% over time from liquidity mining strategies.

For example, depositing USDC on Compound:

Only liquidity mining: If one chooses to stake $10 million in Compound from February 15 to May 23, they can earn an interest rate of 1.47% as shown by the blue line.

If hedging liquidity mining: In addition to existing mining yields, one can lock in future returns by shorting and swapping rates (IRS) on Strips. Overall, the hedging liquidity mining strategy will increase returns from 1.47% to 2.5% during the same period.

Scenario 3: Predicting the direction of interest rate changes (or liquidity mining rate APY%) and betting on arbitrage.

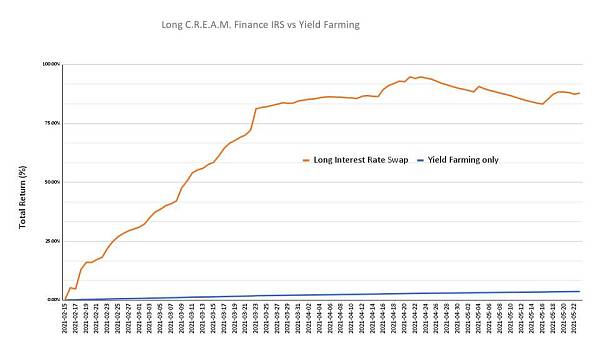

Directional bets on interest rate changes can be made through trading on Strips. Taking cream.finance as an example:

Only liquidity mining: By depositing USDC into cream.finance from February 15 to May 23, one can earn 3.7% interest, as shown in blue in the chart.

If leveraging to go long on rates: Going long on cream.finance rate trading (paying fixed, receiving floating); paying fixed APY% and receiving floating APY% during the same period will yield a net return of 88%.

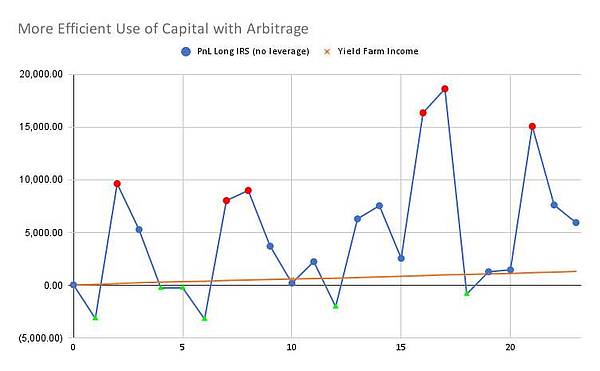

Scenario 4: Releasing "locked" capital from liquidity mining and obtaining higher returns from arbitrage.

Existing "liquidity mining" protocols require staking the underlying assets to earn returns. Using Strips, there is no need to hold the underlying assets; only 10% of the position needs to be used as collateral to achieve interest rate trading arbitrage, and it also enables interest rate trading arbitrage across different DeFi protocols.

For example:

AAVE's USDC rate is 3.5%

Compound's USDC rate is 6%

The trader can: go long on AAVE USDC through interest rate swaps

The trader can: go short on Compound USDC through interest rate swaps

Scenario 5: Arbitrage "basis" trading

Through Strips, one can trade perpetual contracts' funding rates with 10 times leverage. For basis traders, this means they can "lock in" profits by hedging position funding fees on Strips.

For example: A trader currently holds a short basis position

The trader is currently shorting BTC-0924 and going long on the BTC-PERP perpetual contract on Binance

The trader is currently paying the funding fee for the BTC-PERP perpetual contract every 8 hours (read more about funding fees)

The trader can go long on the BTC-PERP funding rate through IRS on Strips and pay a fixed rate while receiving the floating rate of the BTC-PERP perpetual contract every 8 hours, thus converting the floating rate into a fixed rate.

Arbitrage can also be done on funding rates between derivative exchanges.

Suppose:

The funding rate for the BTC-PERP perpetual contract on Binance is currently 12%

The funding rate for the BTC-PERP perpetual contract on FTX is currently 6%

The trader: can go long on FTX BTC-PERP funding rate through interest rate swaps

The trader: can go short on Binance BTC-PERP funding rate through interest rate swaps

Strips' Automated Market Maker (AMM) and Its Returns

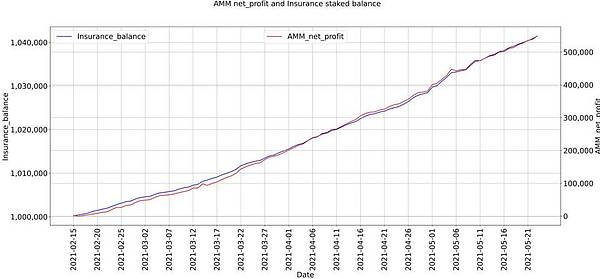

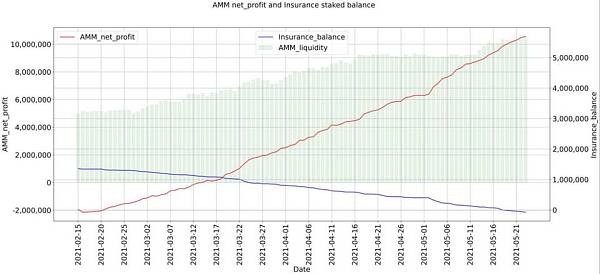

Strips' interest rate trading system is entirely based on an Automated Market Maker (AMM), where market prices are determined solely by supply and demand. Liquidity providers can provide liquidity in the AMM to earn 75% of the market's trading fees and act as market makers. Strips states that by running simulations of over 800 historical market volatilities and 10 times market volatility, its AMM has achieved:

An annualized investment return rate of 22% APY

A Sharpe ratio of 5.64 (a performance metric evaluating investment returns and risks)

A Sortino ratio of 55 (same as above)

Based on historical data from Compound, AAVE, and other companies from February 15, 2021, to May 23, 2021, across 5 markets.

The Strips team indicates that to test the robustness of its AMM, it has placed the AMM under various stress market conditions. Using a standard deviation 6 times higher than historical levels, it found that the AMM could achieve a +200% return within 100 days.

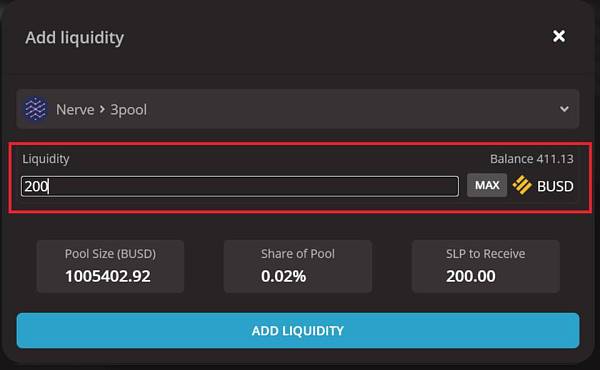

Adding Liquidity in Strips AMM

Select Liquidity on the left, then click ADD LIQUIDITY to increase liquidity.

Select the market to add liquidity.

Input the amount of liquidity to provide (currently only BUSD is supported), and confirm from the Metamask wallet.

Insurance Pool

To ensure that all traders receive full compensation, Strips has set up an insurance fund pool to act as the last line of defense during periods of high market volatility. This is the last liquidity source and keeps the market solvent.

If a trader's margin ratio falls below 3.5%, their position will be liquidated, and the insurance pool will take over the position and automatically close it.

When a trader's position is automatically liquidated, a small fee must be paid to the insurance. Additionally, 5% of the market's trading fees and AMM earnings will also be allocated to the insurance pool.

However, not all markets are included in the insurance pool. To ensure market insurance coverage, community governance must obtain 66% of the votes to pass.

Project Progress and Development Direction

Currently, Strips has completed the development of basic modules such as interest rate swap trading, liquidity addition, and insurance pool, and has released its 0.3 test version, allowing users to experience and provide feedback on the test version.

Users can currently choose to trade with 1-10 times leverage, and in the future, the leverage multiples may be increased through community governance voting.

In the future, Strips plans to introduce other interest rate derivative trading, such as interest rate options, volatility markets, perpetual bonds, and perpetual futures contracts.