Deconstructing the Bitcoin Transaction Ecosystem: What Institutions Are Involved and What Are They Doing?

This article helps you clarify the roles and functions of different institutions within the Bitcoin trading ecosystem, providing a deeper understanding of the institutional ecology in Bitcoin trading.

This article helps you clarify the roles and functions of different institutions within the Bitcoin trading ecosystem, providing a deeper understanding of the institutional ecology in Bitcoin trading.Source: Deep Chain Finance

Author: Hegel

When Bitcoin was first born, institutions were not very interested. However, since 2020, institutional interest has been growing stronger.

A major reason behind this is the pandemic, under which central banks, represented by the United States, have implemented overly loose monetary policies, causing severe market fluctuations.

In response to institutional interest, Arcane Research, a research institution under the Norwegian cryptocurrency investment company Arcane Crypto, specifically conducted a research report.

The results found that institutions generally agree that despite current issues such as regulation, they are still very confident about the future and believe that institutions will occupy a core position in the Bitcoin market.

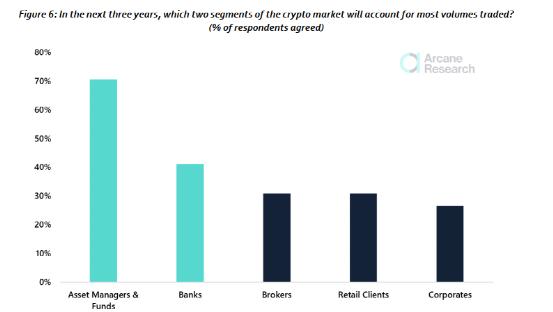

The survey question was: In the next three years, which two segments will dominate cryptocurrency trading volume? The feedback from institutions, ranked from high to low, is: asset management/funds, banks, brokers, retail investors, and non-financial companies. Source: Arcane Research Report

This research report titled "Bitcoin Ecological Trading System and Emerging Institutional Infrastructure" summarizes in detail the changes in the Bitcoin ecosystem after the entry of institutions.

What are the market makers and brokers? How are exchanges categorized? Why do banks need to provide custody?

Deep Chain Finance has translated and reorganized this research report, attempting to help readers clarify the roles and functions of different institutions within the Bitcoin trading ecosystem, providing a deeper understanding of the institutional ecological map in Bitcoin trading.

"Traders can be divided into four categories"

Before delving into the Bitcoin ecosystem, let’s take a look at the types of users directly participating in trading in the market. Most are individual investors, which can be divided into two categories:

1. Small fishes

Refers to small retail clients who usually exchange transactions using their local fiat currency and cryptocurrencies like Bitcoin. They mainly take on the role of "takers," and are not particularly concerned about the spread and fees involved in transactions. This is the "small fish."

2. Bigger fishes

Also retail investors, some are quite special, being very sensitive to prices and deliberately seeking trading platforms with low spreads and fees. They typically have accounts on different exchanges and are very active in daily trading. This is the "big fish." Exchanges compete fiercely around these "big fish," leading to high marketing costs.

Institutional investors, depending on whether they belong to the crypto finance or traditional finance sectors, can also be divided into two categories:

3. Crypto whales

The "whales" we often hear about are these institutional investors rooted in cryptocurrency. They seek the best liquidity and lowest latency, moving between different platforms, and are very willing to "lead" market direction, treating cryptocurrencies as their primary asset. They trade on their own and also commission brokers; they are active on exchanges and appear on OTC platforms; additionally, they use crypto-native derivatives trading platforms to execute more complex professional operations.

4. Whale in suits

Another type of institutional investor comes from the traditional finance sector and faces more restrictions. Besides cryptocurrencies, they invest in many different types of assets, so they tend to choose platforms they are familiar with to meet stringent regulatory requirements. Of course, they also have high demands for low latency and strong technology. They appear on fully compliant high liquidity platforms, such as LMAX Digital, the Chicago Mercantile Exchange (CME), and even Coinbase.

These two types of institutional players operate similarly when trading Bitcoin, with the biggest difference reflected in the strategies they choose when entering exchanges due to technical and compliance requirements.

"What roles do institutions play"

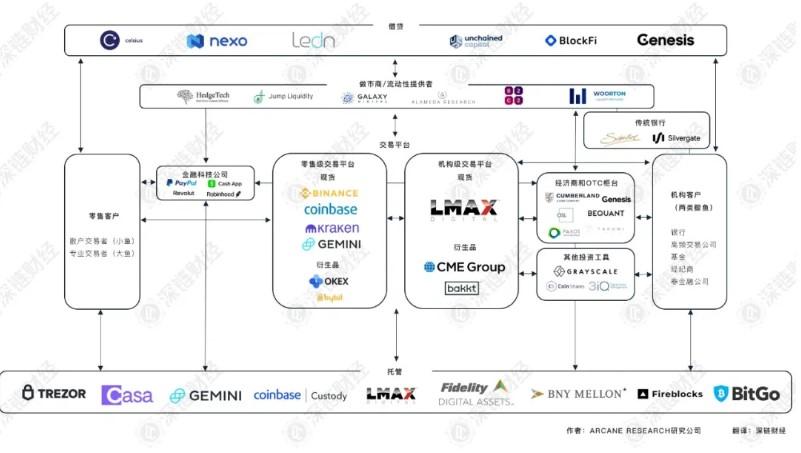

The biggest highlight of the Arcane report is the Bitcoin ecological map, which elaborates on the roles and functions of custodians, lenders, banks, exchanges, and investors within this ecosystem.

Arcane's designed Bitcoin trading ecological map

Participants in this ecosystem are interconnected, and a single company may take on several different roles; for example, Coinbase acts as both an exchange and a custodian. Retail-focused exchanges also seek liquidity from institutions, and some traditional payment tools obtain liquidity from brokers to support cryptocurrency trading functions. Banks sometimes also provide custody services.

Below are the roles of eight types of participants.

1. Market makers/liquidity providers

The soul of financial markets is liquidity, which gives market makers/liquidity providers a special mission.

Without market makers, the cryptocurrency market would experience collapses similar to the stock market. The crash in 2017 caused Coinbase to experience a flash crash, resulting in millions of dollars in compensation to investors.

Since the transaction prices are formed separately at each exchange, the arbitrage opportunities in cryptocurrencies are larger, making chaos more likely. The purpose of market makers is to create order out of chaos by filling the order book with artificial buy and sell orders, thereby stabilizing market sentiment.

In the early days of the industry, there were very few orders in the order book, which led to significant price fluctuations with each transaction.

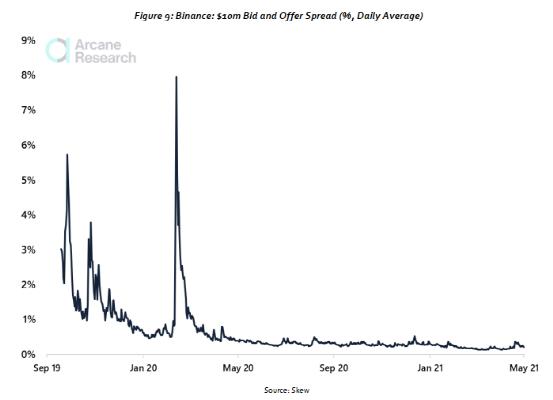

After 2016, this issue improved significantly, mainly reflected in the trend of narrowing bid-ask spreads.

Taking Binance as an example, two years ago, a $10 million transaction would cause a price fluctuation of 5% to 8%. Now, this spread has dropped to below 1%, indicating safer trading.

In the above chart, the 8% peak in March 2020 was due to the global outbreak of COVID-19, which led many investors to rush to withdraw funds for relief, resulting in insufficient liquidity. In contrast, this year's "big drop" was not as frightening, as liquidity was actually still normal.

Currently, the most important market makers include: Jump, HedgeTech, Alameda Research, Galaxy Digital, B2C2, and Woorton.

2. Brokers and OTC desks

The most efficient market makers generally collaborate with OTC (over-the-counter) desks to minimize slippage in the order book when completing large transactions.

Slippage refers to the phenomenon where, after submitting an order to the order book at an exchange, due to differences in order sizes between buyers and sellers, the final execution may consume multiple orders at once, resulting in a significant deviation between the final execution price and the initial order price.

To avoid incurring extra trading costs, market makers typically lock in prices through OTC transactions to complete target orders more quickly.

A survey by Citibank indicated that 90% of cryptocurrency OTC trades are completed via electronic APIs, a much higher percentage than in traditional financial markets. The improvement of infrastructure has reduced the slippage for OTC trades worth tens of millions of dollars from 50 to 200 basis points (0.5%-2%) in 2017 to between 5 and 10 basis points (0.05%-0.1%).

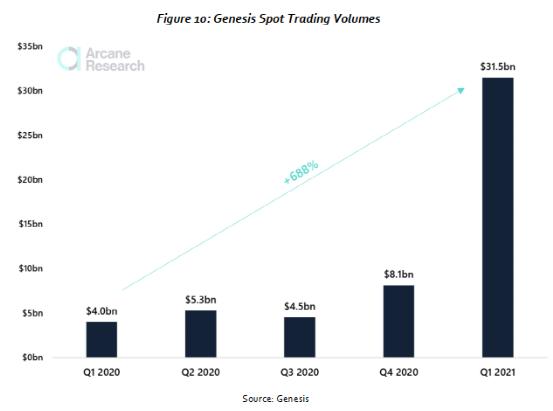

The main clients of OTC are hedge funds and index funds. Currently, the main institutions providing OTC services are mostly from quantitative investment backgrounds, such as Jump, B2C2, Alameda Research, and Genesis.

However, with non-financial companies like Tesla and MicroStrategy entering the Bitcoin space this year, the main customer structure of OTC platforms has also changed.

In Q4 of last year, non-financial companies accounted for only 0.5% of Genesis's client base, but this ratio skyrocketed to 25% in Q1 of this year.

Institutions not only hope to complete large transactions quickly with the lowest slippage but also want to make the process more convenient, thus giving rise to the role of brokers.

Brokers act as intermediaries, executing a series of complex investment processes for clients, including trading, custody, and clearing. The Block has pointed out that this business originates from the traditional financial prime brokerage (PB) services, specifically targeting institutional clients, and is highly innovative and complex; currently, the understanding of this in the mainland Chinese securities market is still limited.

Brokerage services in the cryptocurrency space are still new, facing the biggest challenge of clearing and settlement and deep capital market support, lagging far behind traditional financial markets in these aspects.

Another major issue is that existing brokerage services are too fragmented. The future winners will undoubtedly be super players who can achieve a "one-stop" solution for spot derivatives market trading acceleration, leverage extension, asset custody, capital introduction, and trading strategy formulation.

3. Traditional banks

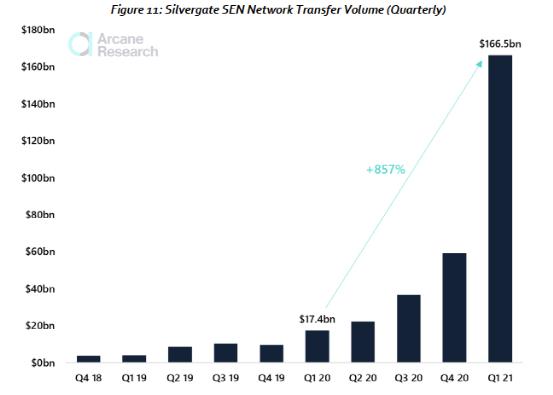

Crypto-friendly banks are often an overlooked category, but they provide large institutions with fiat currency deposit and withdrawal channels. The most famous is Silvergate.

Founded in 1988, this bank entered the cryptocurrency field in 2013 and quickly transformed into a special bank primarily serving crypto enterprises. Today, it has over 900 institutional clients, and by the end of last year, corporate deposits exceeded $3.7 billion, with more than half coming from 77 different cryptocurrency exchanges.

Silvergate prides itself on its self-built payment network, SEN (Silvergate Exchange Network). Through SEN, institutional users can complete fiat currency transfers and transactions year-round without interruption. In Q1 of this year, SEN processed fiat transactions totaling $166.5 billion, a year-on-year increase of 857%.

Of course, Silvergate's business is not limited to banking. Its CEO, Alan Lane, stated that the SEN network will further monetize in the future, mainly by promoting digital asset lending and custody services.

Another well-known bank is Signature Bank, which also primarily serves cryptocurrency businesses. This is the first bank supported by the U.S. Federal Deposit Insurance Corporation (FDIC) and has obtained a financial license from New York State, providing a sense of security and compliance. In the past two years, Signet has integrated with Fireblocks and the stablecoin TUSD protocol.

Not only these traditional "banks" are engaged in banking services, but some cryptocurrency-native institutions are as well. Kraken, an established cryptocurrency exchange, successfully obtained a banking license in Wyoming last year—specifically, a Special Purpose Depository Institution (SPDI) license.

This means that Kraken's inflow and outflow of funds are more convenient, allowing it to operate exchange business and provide deposit and withdrawal banking services, all in full compliance.

4. Financial technology companies

Compared to B-end payment tools, C-end payment tools are more familiar to the public. The financial technology companies in the Bitcoin ecosystem are four-legged—Cash App, PayPal, Robinhood, Revolut, all of which started as payment tools and later gradually developed trading functions.

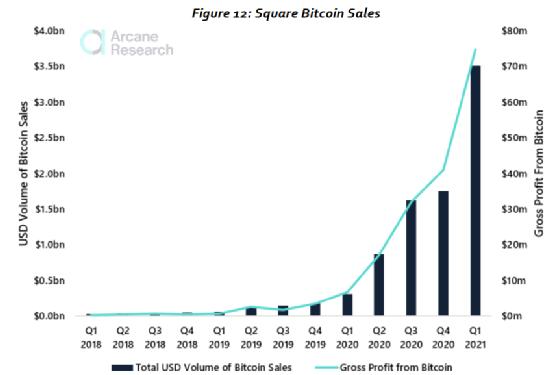

The earliest to enter the market was Cash App, founded in 2015 as Square Cash. The parent company, Square, was founded by Twitter CEO Jack Dorsey. Cash App is one of the most popular financial applications in the U.S., with 36 million active users as of March this year. Even MicroStrategy's CEO Michael Saylor admitted that he has bought Bitcoin on Cash App.

On Cash App, users can not only use Bitcoin for payments and transfers but also trade Bitcoin as an asset. In Q1 of this year, Bitcoin sales on Cash App exceeded $5.5 billion.

PayPal obtained a Bitcoin license from New York State, so every Bitcoin sold to customers must be backed by actual Bitcoin reserves, with liquidity provided by Paxos.

In the past two years, PayPal has been very active. In October last year, PayPal launched cryptocurrency trading features. In April this year, it allowed its payment company Venmo to open cryptocurrency trading, and in early July, it raised the limit for U.S. compliant users to purchase cryptocurrencies from $20,000 to $100,000.

On July 29, during the Q2 investor conference call, PayPal's CEO revealed that the development of a super app wallet has been basically completed, featuring high-yield storage and fast deposit functions.

Robinhood is also a very popular trading platform this year, having been criticized multiple times by U.S. securities regulators for its heavy gamification tendencies. In fact, Robinhood is not an exchange itself. After clients place trade orders, the platform buys and sells cryptocurrency assets on different exchanges on their behalf.

Robinhood has been reported multiple times to have "some issues in cryptocurrency trading" at critical moments, especially when trading would pause during spikes in Dogecoin prices, causing market dissatisfaction.

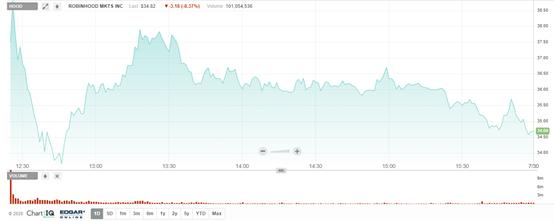

On July 29, Robinhood went public on NASDAQ under the ticker symbol HOOD. Its IPO was not smooth, with its valuation being pressured down by hesitant investors, and it found itself embroiled in compliance disputes with regulators. On its first day of trading, the stock price failed to exceed the issue price and ultimately fell 8.4% after fluctuations.

Robinhood's stock price movement on its first day of trading, source: NASDAQ official website

The biggest difference between Cash App and other tech company products is that it allows free deposits and withdrawals of cryptocurrencies. On Cash App, users can withdraw Bitcoin to other wallets at any time. PayPal and Robinhood do not have this feature, while Revolut, which emphasizes low fees and low counterparty risk, is only testing this feature for high-end users.

According to the latest version of the cryptocurrency service terms on its official website (June 30, 2021), cryptocurrencies on PayPal are more like investment tools—currently, the deposit and withdrawal functions for cryptocurrencies are not open, users are not allowed to send cryptocurrencies to friends' accounts or their own third-party wallets, and they cannot directly use cryptocurrencies to buy goods. Moreover, this service is only available to U.S. users.

Of course, at this year's Consensus conference hosted by Coindesk, PayPal representatives also stated that they are currently developing deposit and withdrawal functions.

In addition to having deposit and withdrawal advantages, Cash App itself holds 8,027 Bitcoins, which Arcane estimated to be worth about $500 million at the time of the report's release, with a holding cost of about $220 million.

In fact, Cash App's first-mover advantage is closely related to founder Jack Dorsey's emotional connection to Bitcoin. Recently, at The ₿ Word conference, Jack praised the Bitcoin protocol as beautiful and expressed a desire to use Bitcoin to promote peace among humanity.

In summary, Square's leading position in the Bitcoin ecosystem will continue for some time.

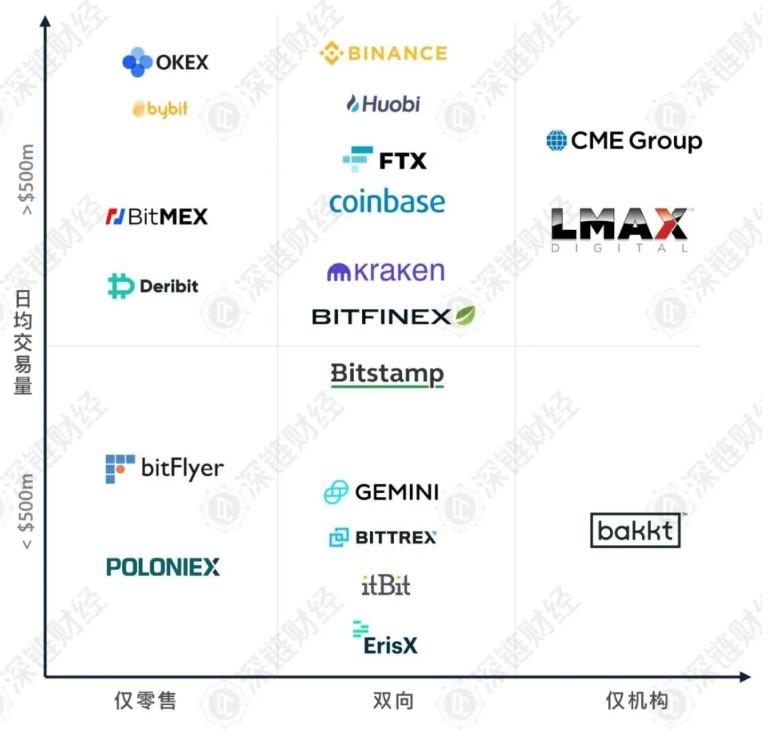

5. Exchanges

There are many ways to categorize exchanges, with the most important standard being customer targeting. Some exchanges cater only to retail users, such as Bybit and BitMEX; some cater only to institutional users, like LMAX and the CME; most are dual-purpose, like Binance, Huobi, FTX, Coinbase, and Gemini.

5.1 Retail exchanges

C-end exchanges must find ways to attract and retain new customers. Due to the abundance of exchanges and low customer loyalty, these exchanges must strengthen research and development and frequently hold activities like new coin listings.

Since most customers are retail investors, they are not very sensitive to the fees for placing orders, so the fees that retail exchanges can charge are actually higher than those of institutional exchanges.

The core competitiveness (USP) of retail exchanges is ease of operation, a very user-friendly UI interface, and a variety of marketing activities. Correspondingly, marketing costs are also very high; if there are too few new coin activities, customers will not be retained.

For retail investors, the biggest worry for C-end exchanges is that the user volume is too large, so when the market fluctuates violently, they are very likely to encounter server downtime issues.

5.2 Institutional exchanges

Conversely, for institutions, downtime is absolutely intolerable. Institutional users entering exchanges have many common prerequisites: a professional operating interface, massive throughput capacity, no downtime, credit limits, and compliance operations.

Therefore, the technical requirements for institutional exchanges are extremely high. Even in extreme volatile markets, they must ensure 100% real-time trading, and liquidity depth is indispensable. The dual requirements of compliance and technology make the platform development difficulty for institutional exchanges far exceed that of retail exchanges.

Retail exchanges seek novelty, while institutional exchanges seek stability.

Additionally, exchanges can also be categorized into spot exchanges and derivatives exchanges based on the different trading products.

5.3 Spot exchanges

With the rise of compliant exchanges, more and more users choose to complete exchanges directly between fiat currencies and cryptocurrencies. However, to date, the vast majority of trades are still conducted using stablecoins as intermediaries.

Even Binance, the largest exchange by global trading volume, only started laying out fiat trading in 2019. For a long time before that, Binance only supported crypto-to-crypto trading.

Among mainstream exchanges, the highest fiat trading volume is Coinbase, followed by LMAX Digital, Bitfinex, Bitstamp, and Kraken.

In summary, as the compliance construction of cryptocurrencies continues to advance and regulation improves, the shift from crypto-to-crypto trading to fiat trading is an inevitable long-term trend.

5.4 Derivatives exchanges

The trading volume of Bitcoin derivatives has already surpassed that of spot trading. The derivatives market plays a more critical role in the price discovery process of Bitcoin.

Comparison of monthly spot and derivatives trading volumes for Bitcoin since July 2019. Green represents spot, black represents derivatives. Source: CryptoCompare

Derivatives exchanges can be divided into two categories:

The first category is offshore, unregulated derivatives exchanges. The KYC (Know Your Customer) requirements for these exchanges are usually not very strict, allowing anyone, regardless of wealth, whether a novice or a wealthy whale, to experience margin trading. The minimum margin ratio is only 1%.

The second category is compliant derivatives exchanges that accept strict regulation. Clients are all certified investors, and each contract requires a minimum investment of at least 5 Bitcoins, with margin ratios as high as 40%.

The advantage of offshore exchanges is that registration is easy, and there are few restrictions on deposits, allowing even very small amounts of capital to participate, thus attracting many retail investors globally, resulting in massive trading volumes. Major representatives include Binance and Bybit, with Binance alone accounting for 35% of derivatives trading volume.

Of course, the disadvantages of offshore exchanges are also obvious: due to fewer restrictions, retail investors often succumb to temptation and engage in high leverage, significantly amplifying risks. Liquidation has become a common occurrence, akin to opening Pandora's box.

Regulatory authorities have clearly been keeping an eye on these offshore exchanges, not wanting them to become "lawless territories."

In October 2020, the U.S. Commodity Futures Trading Commission (CFTC) and the Department of Justice (DOJ) charged BitMEX with illegally operating a derivatives platform and providing trading services to U.S. citizens; exchanges like Binance and FTX also stated in July this year that they would reduce the maximum leverage ratio from 100x to 20x, emphasizing that leveraged trading is not the mainstream of the cryptocurrency ecosystem.

Compliant exchanges have solved the problems of offshore exchanges but have also brought the disadvantage of a narrow coverage. Ordinary people find it difficult to access their Bitcoin futures products.

The largest compliant derivatives exchange is the Chicago Mercantile Exchange (CME), which offers cash-settled futures and has trading time restrictions, only open for trading from Sunday at 5 PM to Friday at 4 PM, with a uniform market closure for one hour after 4 PM each day. In contrast, Bitcoin spot trading is available 24/7, with liquidity clearly stronger than that of CME's Bitcoin futures.

In December 2017, the Chicago Board Options Exchange (CBOE) also announced the launch of Bitcoin futures but completely withdrew after June 2019. Currently, the largest exchange in the second category is the CME.

The main liquidity providers for the CME include Akuna Capital, B2C2, BlockFi, Cumberland, Galaxy Digital, Genesis, NYDIG, and others.

Overall, the largest contributors in the derivatives market are still offshore exchanges. The role of offshore derivatives exchanges is the most significant in the price discovery process of Bitcoin.

After all, the belief in the cryptocurrency industry is that: everyone has the right to trade freely, and as long as they are willing to bear the risks, they should not be obstructed. Freedom comes with responsibility: participating in leveraged trading with 1% margin is the user's freedom, but they must also be prepared to pay the corresponding price.

6. Other investment tools

Grayscale and its competing ETFs are also important members of the ecosystem. Investing in these funds can enjoy tax benefits.

In the past year and a half, they have developed rapidly, accumulating 800,000 Bitcoins.

Grayscale and ETFs take different routes. Both are funds, but Grayscale is a closed-end fund traded on the OTCQX in the U.S., and only qualified investors can participate. In the primary market, investments in Grayscale can be made with physical Bitcoin or fiat cash. Fund shares can be transferred in the secondary market, but due to the lack of a redemption mechanism, the price of Grayscale funds often trades at a discount or premium to the market price of Bitcoin.

ETFs are a special type of fund that falls between open-end and closed-end, allowing for trading on exchanges and free creation and redemption, making the process flexible and convenient, resulting in ETFs tracking prices closely to the market price of Bitcoin.

Due to the demand for redemptions, Bitcoin ETFs must leave reasonable liquidity channels and regularly ensure a balance in Bitcoin holdings. Therefore, Bitcoin funds maintain close ties with brokers and OTC desks to facilitate smooth exchanges between cash and Bitcoin.

Canada is relatively open regarding Bitcoin and Ethereum ETFs, while U.S. institutions have not been so fortunate. Many institutions have submitted applications to the SEC, including Fidelity, NYDIG, Galaxy Digital, SkyBridge Capital, VanEck, Valkyrie, Wisdom Trust, etc., but the SEC has yet to approve any ETF, with recent responses mostly being "delayed responses."

7. Custody

Trezor and Ledger were the first to provide hardware wallet services, allowing users to store their cryptocurrencies using small USB devices. Later, Casa emerged, offering high-end membership services such as multi-signature recovery of Bitcoin access and multiple hardware backups in different locations to avoid disasters caused by losing a single private key.

Exchanges are also providing custody services for important clients; for example, Coinbase has established a separate entity, Coinbase Custody, where assets are isolated from the exchange and specifically accept user entrustments for the custody of cryptocurrencies. Gemini followed suit and invested $200 million to insure the cryptocurrencies under custody, claiming to be "the custodian with the broadest insurance coverage in the world."

As one of the most prestigious institutions globally, Fidelity began researching blockchain technology as early as 2014 and established a digital asset subsidiary, Fidelity Digital Assets, in 2018, launching a custody solution a year later. Specific performance has never been disclosed, but the CEO confidently stated that this business has achieved "incredible success."

Traditional trust service providers also want to get a piece of the pie. BNY Mellon, which has over $41 trillion in assets under custody, announced in February this year that it plans to launch custody services in the second half of the year, intending to offer different services for different clients, such as physically isolated cold storage, storing wallets in abandoned military bunkers in the Swiss Alps; secure multi-party computation (MPC) mathematical models; and hardware security modules (HSM) that add expansion cards in computers to handle encryption and decryption operations.

An abandoned military bunker in Switzerland has been transformed into a Bitcoin cold storage facility. In addition to BNY Mellon, Standard Chartered, Northern Trust, JPMorgan, Goldman Sachs, and Citibank are also deploying digital asset custody services.

The largest clients for custody services are cryptocurrency exchanges, such as Binance, Coinbase Pro, Gemini, FTX, B2C2, Galaxy Digital, Genesis. Additionally, OTC desks, market makers, lending companies, and payment processing companies also have demand.

8. Lending

Credmark data indicates that by Q1 2021, the cryptocurrency lending market had reached a scale of $29 billion.

Lending can activate the liquidity of the Bitcoin trading ecosystem. For leveraged trading, institutions prefer to seek lending companies rather than exchanges because exchanges' automatic liquidations are too frequent.

The main clients of the Bitcoin lending market are market makers. The main providers include Genesis and BlockFi, with Genesis serving only institutional clients, while BlockFi also serves individual clients. Additionally, traditional institutions are also developing different lending services. Silvergate, as a traditional bank, collaborates with Fidelity to provide USD loans to institutions through the SEN payment network. In this process, the Bitcoin pledged by clients is separately held by Fidelity.

"What factors do institutions value most"

Through communication with banks, funds, asset management companies, high-frequency trading systems, and proprietary trading companies in the ecosystem, Arcane summarized the characteristics of institutional investors' attitudes towards Bitcoin, mainly reflected in three aspects:

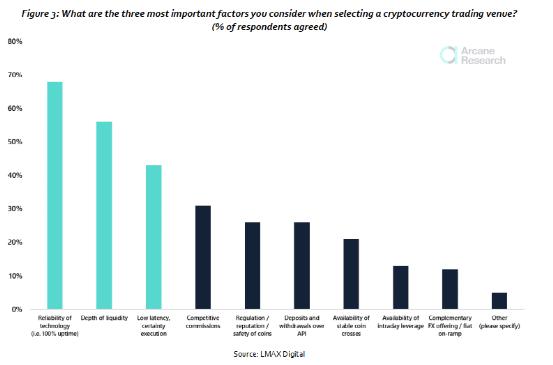

1. Choosing a trading platform: Reliability is paramount

The three most important factors are: first, reliable technology that must operate 100% normally without downtime; second, liquidity depth; third, low latency, with clear trading situations. Additionally, they will consider the following factors: favorable fees; compliance with regulations, good reputation, and security of assets; the ability to perform deposit and withdrawal operations via API; allowing the use of stablecoins; providing intraday leveraged financing trading; and offering fiat currency channels.

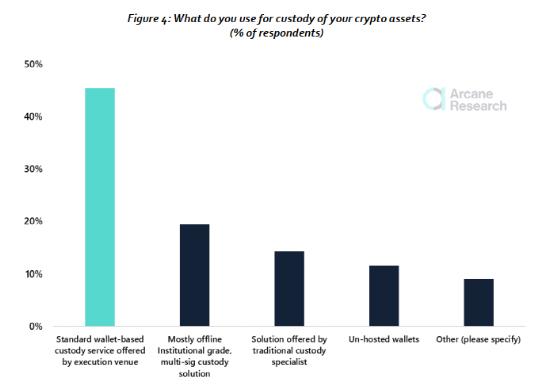

2. Choosing a custodian: Security first

Research found that nearly half of institutions directly choose trading platforms for custody. The three most common custody solutions are: offline, institutional-grade, multi-signature custody; traditional custody professional institutions; and non-custodial wallets.

As for the considerations when choosing, the top priority is undoubtedly security, followed by tangibility, convenience, and the ability to relate to exchanges.

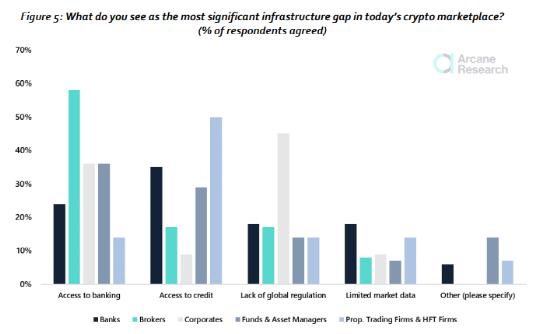

3. Choosing infrastructure: Connecting to traditional finance

The improvement of infrastructure is a prerequisite for institutions to hold investments in Bitcoin. Most interviewed institutions believe that the infrastructure that needs to be strengthened the most currently lies in the connection with banks and credit systems. Specifically, banks, funds, and asset management institutions are most eager to enhance banking and credit infrastructure, brokers are most eager to enhance banking infrastructure, ordinary companies hope to strengthen banking and compliance services, while proprietary trading firms and high-frequency trading firms most wish to enhance credit system construction.

"The 'new era' of Bitcoin"

Recently, there has been a sense of optimism, with many feeling that financial market behavior has entered a new era driven by retail investors, influencers, and traffic.

Indeed, the influence of retail investors and online messages is continuously expanding. During the "GameStop" movement, retail investors stirred social media sentiment through Reddit, forcing Wall Street institutions that were shorting GameStop stock to yield.

This has also excited retail investors in the crypto space, who want to replicate the success of GameStop. The Dogecoin army is particularly prominent, claiming to make a move on April 20 this year to push Dogecoin to $1.

However, in the end, their grand ambitions ended in failure, as Dogecoin fell back from the $0.4 level to around $0.3 on that day.

Ultimately, massive capital and professional investment techniques determine that institutions will still dominate any financial market, and their role cannot be ignored. A healthy trading ecosystem must enable mutual benefits for both individual and institutional investors. The absence of either party's participation is insufficient to constitute an "ecosystem."

The new era of Bitcoin is characterized by both institutionalization and retail participation.