Before understanding encryption, you need to understand the modern economy built on trust

Trust is the biggest cost.

Trust is the biggest cost.This article comes from Moneyness and is compiled by Rhythm BlockBeats.

Many people believe that crypto assets are worthless because they lack collateral and redeemability; everything is built on air. However, what many do not realize is that the fiat currency we use every day also lacks redeemability, and there are no assets backing it. The economies we see are built on trust.

So, what is different about crypto assets built on blockchain? Crypto assets are trustless; on-chain assets establish a trustless value system through the consumption of natural resources (electricity) combined with cryptography, economics, and more. This is why the crypto community adheres to a theory: Don't Trust, Verify!

This article originates from Moneyness, where the author classifies and analyzes the credit system and credit tools of the traditional economy. The author believes that the crypto industry is driven by meme culture, a view I do not fully agree with. Narratives and memes are indeed an indispensable part of the crypto industry, but for an early-stage industry, using narratives and memes for a cold start is the most efficient form. However, there is more behind crypto than just memes.

"Money is not valuable just because the government says it is; it's a meme culture," Brendan Greeley said in the Financial Times.

I completely agree with his point.

Crypto enthusiasts often say, "The dollar is a meme." This idea makes sense coming from the cryptocurrency community, as the price fluctuations of cryptocurrencies are purely driven by memes. There is no better example than Dogecoin (Doge), which started as a humorous cryptocurrency supported by a Shiba Inu gif. In fact, Dogecoin's big brother, Bitcoin, is the same. As shown in the image above, the harder you meme, the higher the coin price will go.

Therefore, for cryptocurrency analysts, to gain a deep understanding of a coin's value, it is essential to study its underlying meme culture and its meme artists closely.

But if the analysis of cryptocurrencies ultimately boils down to meme analysis, what kind of analysis applies to the dollar?

Greeley has reminded us that the dollars issued by banks are backed by the banks' loan portfolios, so they are suitable for credit analysis rather than meme analysis. Analysts evaluate the quality of the bank's investments to determine the quality of the dollar bonds issued by that bank.

Greeley also mentioned that central banks like the Federal Reserve are just a special type of bank, so the dollars they issue are also suitable for credit analysis. I pointed out in this blog that the currency issued by central banks (i.e., fiat currency) also requires credit analysis, just like any other bond. Although the dollars from the Federal Reserve or the yen from the Bank of Japan have some peculiar characteristics, they are ultimately just another form of credit.

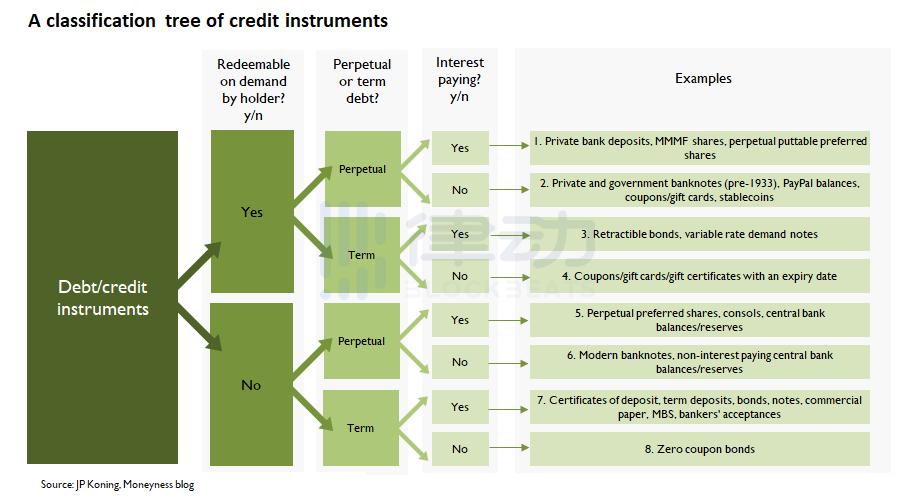

So what kind of credit is fiat currency? There are many types of credit instruments, from bonds to deposits to bank notes, each with its unique characteristics. To understand the applicability of central bank currency, I created a chart illustrating the differences in credit instruments under three different criteria.

The first criterion for comparing credit notes is whether the note holder can redeem it on demand. In other words, if I own a specific credit instrument or IOU, I can choose to return it to the issuer or debtor at a certain time and redeem something.

The second category involves the maturity of the instrument: does it have no maturity date (e.g., perpetual annuities)? Or is it long-term debt? If the credit instrument has a term, it means it will mature at a predetermined time, and the debtor must repay the original borrowed amount.

The last category is whether the note pays interest.

By analyzing these different characteristics, we arrive at eight different types of credit instruments, with examples listed on the right side of the chart.

As you can see, the dollars from the Federal Reserve, euros from the European Central Bank, and yen from the Bank of Japan belong to the 5th and 6th categories of credit instruments. Central banks issue two types of currency: physical banknotes and electronic balances (sometimes referred to as reserves). Central bank electronic reserves pay interest, while bank notes do not.

In addition, bank notes and electronic balances are very similar instruments. Both of these credit instruments cannot be redeemed on demand. In other words, you cannot take a banknote back to the issuing institution at 5:30 PM on a Friday and exchange it for something else. (Bonds and certificates of deposit also lack redeemability at any time.) Because they are both perpetual, like perpetual preferred stock or never-expiring coupons/gift cards.

Although these credit instruments lack redeemability, this does not prevent them from being credit instruments. It simply turns them into a different type of credit instrument. Yes, it may be of lower quality, but it is still a credit instrument.

For example, even if a redeemable bond (Category 3) suddenly loses its redeemability feature (and can no longer be redeemed at the owner's request), it is still a credit instrument; it has simply become an ordinary bond (Category 7). Similarly, if a perpetual redeemable preferred stock (Category 1) loses its redeemability, it is still an IOU. It has merely transformed into a new credit instrument, an ordinary perpetual preferred stock (Category 5).

The same principle applies to currency as a credit instrument. Decades ago, the dollars from the Federal Reserve could be redeemed for gold on demand, so they were considered Category 1 or Category 2 credit instruments. When the Federal Reserve abolished the redemption system in 1934, the dollar did not become merely a meme. Instead, it transformed into a different type of credit instrument, one belonging to Category 5 or Category 6.

When credit analysts figure out what type of credit instrument they are dealing with, their work is only half done. Next, they must go back and study the issuer of the instrument: Is the issuer reliable? Does it have enough assets to back the credit instruments it issues? Can it generate enough income to pay interest? Will related subsidiaries or parent companies, or other third parties enhance or diminish the issuer's credit?

As you can see, none of this is meme analysis; it is all credit analysis.

To recap, the dollars issued by the Federal Reserve are perpetual credit instruments that lack redeemability on demand. To determine the reliability of the Federal Reserve's perpetual non-redeemable credit instruments, you may need to analyze the Federal Reserve's financial condition. This should also include investigating the financial health of the Federal Reserve's parent company, the U.S. government: does the financial condition of the Federal Reserve's parent company enhance or diminish the Federal Reserve's credit?

So the value of the dollar is not simply because the government says it is valuable. Just as Tesla's financial condition determines the value of Tesla bonds, the financial condition of the central bank (and its parent) is also key to determining the value of central bank currency.

But if you want to conduct meme analysis, then look primarily at Dogecoin and Bitcoin.

Original link: http://jpkoning.blogspot.com/2021/07/the-dollar-isnt-meme.html