A Casual Talk on Investment and Speculation: How to Become a Qualified Investor?

"In the short term, sentiment drives prices more than actual fundamentals."

"In the short term, sentiment drives prices more than actual fundamentals."This article is from Deribit, authored by Avi Felman, Head of Trading at BlockTower Capital, and compiled by ChainCatcher.

"When I was a young nobody, I started to succeed, and I was called a gambler. My scope and volume of business increased. Then I was called a speculator. My range of activities kept expanding, and now I am called a banker. In fact, I have been doing the same thing all along."

--Sir Edward Cassell

Everyone is a trader to some extent. Every decision made in life presents an opportunity for the opposite, and whether acknowledged or not, everyone makes thousands of trades every day. Deciding to study engineering instead of finance, or going to the movies with friends instead of to a bar, is a trade.

At a high level, people can strive to categorize every decision as a "trade" and begin to evaluate all choices from the perspective of expected value, assessing life choices in a manner similar to reviewing investments or deciding to buy options. This is a simple view of how actions can be categorized, but it serves as a useful heuristic for understanding the beginnings of different types of decisions.

With this in mind, every participant can be classified as a "trader" at the highest level before engaging in any financial market. Of course, this is not the universally accepted use of the term trader—indeed, many market participants would be outraged by the term and shout, "No, I am an investor!" The historical distinction between traders (speculators) and investors has long existed in the markets, and they are generally considered different concepts.

Joseph Penso de la Vega was the first writer to articulate this distinction in his 1688 work "Confusion de Confusiones," the oldest known work on the business of stock exchanges. In this book, he outlines three types of people: financial lords (wealthy investors), merchants (occasional speculators), and gamblers (persistent speculators).

Philip Carret, author of "The Art of Speculation" (1930), wrote: "The man who bought U.S. Steel at $60 in 1915, expecting to sell it for a profit, is a speculator… On the other hand, the gentleman who bought AT&T at $95 in 1921 and enjoyed over 8% dividend returns is an investor." In other words, Carret places more emphasis on motivation than on action. Here, the speculator focuses on price, while the investor focuses on business.

The approach of the famous economist John Maynard Keynes is more succinct, defining speculation as "the term for predicting market psychology" and investment as "the activity of predicting the expected returns over the entire life cycle of an asset." His approach is similar to Carret's but differs in one key aspect—the bet on a company's economic success is philosophically different from a pure bet on asset prices.

Creating a Framework

Is there a robust set of actions that defines whether something is a trade or an investment? Is it the intangible motivations of market participants that determine whether something is a trade or an investment? Is it time preference?

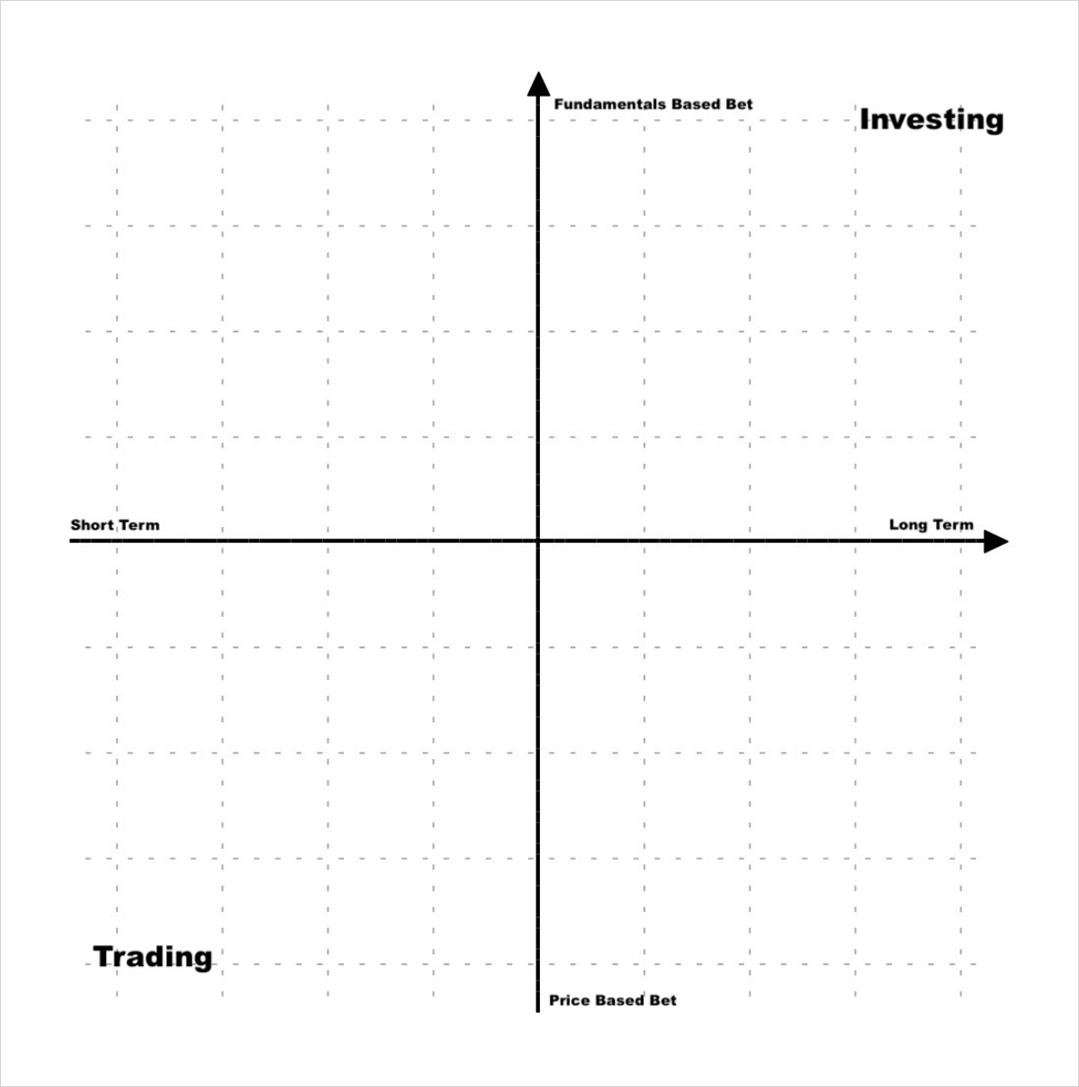

In reality, these terms exist on gradients across multiple axes, and different situations will trade and invest based on various criteria. We can parse this by exploring the standards that separate traders from investors and prompting readers to think about definitions through examples. The two focal points we are concerned with are motivation and duration.

The simplest version of this grid

Most of our historical references seem to agree that if someone's motivation for making a decision relates to the actual economic condition of the business (or agreement) and the corresponding growth viewed as an investment, then making a decision based solely on the expected future price of the asset is considered a trade. Using this approach, two people may take identical actions externally but can be classified in two different ways.

Consider the following two scenarios:

You are a self-proclaimed venture capital fund that made an early investment, but the project unexpectedly went public just two weeks after your investment. Your tokens are unlocked and hit the market at 100 times your initial investment. You feel they are overvalued now, so you sell them on the open market.

You are a hedge fund that made an early investment and entered the market as expected two weeks after your investment. Your tokens are unlocked and can be flipped for profit.

In scenarios 1 and 2, both entities experience exactly the same action, but you might view them as an investor and a trader, respectively. The internal decision-making of both is entirely different, yet the process and outcome are exactly the same. In this specific case, the venture capital fund is more focused on the actual economic condition of the business, while the hedge fund is merely speculating on whether individuals will value the perceived worth of the business.

Let’s look at a set of separate situations with subtler differences around this concept:

You buy an asset because you believe it will drive fundamental changes that will boost business growth. For example, you buy Apple stock after the launch of the iPhone because you believe smartphones will rapidly increase its social penetration. Once that trend is complete, you plan to sell it.

You buy an asset because you believe it will spark interest among people. For example, you buy Apple stock after the launch of the iPhone because you believe people will be excited about the prospects of the new blockbuster product and will pay a higher price per share. Once Apple reaches your target price, you plan to sell it.

The difference in the above examples lies in where the speculation occurs. Both investment and trading require speculation, but investment can be seen as speculation on whether the business will succeed economically.

Speculation on price is viewed differently because it is not at the core of most asset investments' actual "success" in the world. If you choose to bet on whether people will like the iPhone and bring cash flow to Apple, that is fundamentally different from betting on whether people will pay a higher price for Apple tomorrow due to excitement over the iPhone—regardless of whether that excitement is objectively proven by new technology.

Both are bets on human behavior, and humans are reflexive and memetic creatures who often replicate social and physical trends in the same way. With this in mind, there is no philosophical reason to distinguish between these two types of bets. However, to parse the purpose of investment versus trading, the key is to build "fundamentals" within a narrow scope of betting on assets.

Continuing the discussion on duration, we find ourselves looking at a simpler gradient. Long-term bets are primarily associated with investment, while short-term bets are primarily associated with trading. This aligns perfectly with the framework of betting on short-term trends versus betting on genuine long-term changes.

The level of conviction in investment is typically higher than that in trading, and the average duration of each is closely related to this. The stronger your conviction about a subject, the longer you are likely to let it play out. Thus, duration becomes a representation of conviction.

Crypto Applications

Turning our attention back to cryptocurrency, discussing this brings some complexities when you believe Bitcoin is not an asset that generates cash flow. By the way, Buffett or Keynes would say that investing in Bitcoin is a misnomer because there is no real economics in the traditional sense. Bitcoin is purely a bet on whether people will continually find value in Bitcoin. On the other hand, many Bitcoin buyers purchase it intending to hold it long-term. Therefore, while the motivation may resemble trading, many people's level of conviction reaches the level of investment. Given this framework, for many, Bitcoin seems akin to a highly conviction-based trade, as Bitcoin's success is largely measured by price.

The philosophical distinction is not purely for fun. Understanding the qualifications of both helps the average market participant for various reasons.

Once it is understood that trading is a short-term, price-based game, one can begin to parse general rules. First, posing questions about views on fundamentals is always more valuable than the actual fundamentals, because in the short term, views drive prices more than real fundamentals.

When looking at trading in the crypto space, one should focus on the criteria that directly impact price rather than those that indirectly affect price. For example, bullish trading in MATIC depends more on current sentiment, open interest, unlocking timelines, and trading patterns than on its total locked value, security model, or 6-month roadmap.

When investing, it is better to ignore short-term views of the market and focus on the larger outlook of how the road will actually unfold. Given that the duration may be longer, people should spend more time building confidence in their investments rather than trading. More time should be spent on value accumulation mechanisms, the potential of product scenarios, and the long-term perceptions of the market.

The best market participants are always able to combine high-level frameworks with direct, practical actions and methods. A deep understanding of philosophical differences can often help individuals develop and execute better, becoming more rigorous traders and/or investors (or both!).