Misunderstanding that Bitcoin can only be used as a store of value and not as a currency

People's doubts will surely diminish as the storage scale of Bitcoin's future grows and the performance bottlenecks in payment scenarios are overcome.

People's doubts will surely diminish as the storage scale of Bitcoin's future grows and the performance bottlenecks in payment scenarios are overcome.This article is sourced from 8btc, authored by Li Wangjian.

Introduction

From the perspective of Satoshi Nakamoto and the punk community, Bitcoin carries the mission of currency, and the functional positioning of currency includes value storage, payment, and accounting. The reality reflects this as well; since the first block of Bitcoin was mined, it has gone through a phase of gradual maturity.

Compared to fiat currency, using Bitcoin for payments is not complex from the user experience perspective, and it can even be simpler than using fiat: open the wallet (mobile app) ------ scan the payment QR code ------ enter key payment parameters such as amount and fees ------ confirm and send. In just four steps, a transaction can be completed. Currently, more than a dozen countries/regions accept Bitcoin payments, including influential Western countries such as Germany, Japan, Russia, and the United States.

Payment targets include water bills, electricity bills, gas bills, tuition fees, etc. In some countries/regions that have evolved more quickly, Bitcoin has already been adopted by B2B and B2C merchants for purchasing cars, food, etc. Some countries/regions have also started to support Bitcoin at ATMs, fully treating Bitcoin as one of the optional currencies at the retail end. A few countries have even begun to position Bitcoin as legal tender, fully replacing the functions of fiat currency.

Conversely, more countries/regions remain cautious or completely opposed to Bitcoin fulfilling the functions of currency, due to various reasons, including differences in understanding of currency itself and considerations from the technical dimension of the monetary system.

Some policymakers, think tank members, scholars, and numerous practitioners have raised doubts and denials regarding the stability of currency value and the capacity and concurrency performance of the Bitcoin system. They believe that Bitcoin can only serve as an asset for value storage and cannot be used for currency circulation.

This indicates that while the market's understanding of Bitcoin has made breakthroughs compared to a few years ago, there are still certain limitations and significant room for cognitive expansion. Of course, there are still a few who believe that Bitcoin is not even an asset; we will not elaborate further on this. The author wishes to reflect on the former perspective, explaining why Bitcoin is not limited to asset storage but is also suitable as a universal currency.

From the perspective of its inventor's intentions and the meaning of currency itself, Bitcoin is genuine currency and transcends the existing modern fiat currency system. In the abstract section of the Bitcoin white paper, Satoshi Nakamoto states the nature of Bitcoin in the first sentence:

"This paper proposes a system for electronic transactions without relying on trust, which allows online payments to be sent directly from one party to another without going through a financial institution."

This sentence clearly defines Bitcoin as a peer-to-peer electronic cash system. Unlike fiat currency, this currency is underpinned by a system that does not require the involvement of any financial institutions.

This system is simpler and more powerful than the clearing and settlement centers underlying fiat currency, powerful enough to replace central banks and simple enough to be open-source without compromising security. Therefore, Bitcoin inherently carries the gene of currency, not merely as a store of value or a speculative commodity.

Looking at the history of currency development, if a commodity possesses marketability in terms of time, space, and value dimensions, along with extremely high supply extraction difficulty and very low inflation rate, it already meets the necessary conditions to become currency. Historical currency systems have, to varying degrees, possessed these necessary conditions.

Currency itself has three major functional characteristics: value storage, medium of exchange, and unit of account. These three are not independent but exist in a strong progressive and causal relationship. Widespread value storage will make its value more stable; the stability of value will promote its application as a medium of exchange, significantly increasing its audience and application scope. Once the application scope of the medium of exchange reaches a certain level, it will increasingly become suitable for pricing goods, achieving grassroots consensus recognition, and the promotion of pricing will ultimately enable it to serve as a unit of account for society as a whole.

This rule has been followed throughout history, whether in the form of commodity money, gold and silver currency, or even modern paper money and checks.

Therefore, according to this evolutionary rule, Bitcoin is currently still in a stage where it is widely used as a store of value, with its application as a medium of exchange also developing rapidly.

People's doubts will gradually fade as Bitcoin's future storage scale grows and performance bottlenecks in payment scenarios are broken through. The greater the use of Bitcoin as a store of value, the more its market value will eventually reach a relatively stable state. Layer 2 scalability is rapidly developing, and Bitcoin will undoubtedly become the next generation of currency and an indisputable solution. The author intends to explore these two aspects to respond to doubts and analyze its inherent currency attributes while exploring its development direction.

Bitcoin's Market Value Will Tend to Stabilize

There are many factors influencing Bitcoin's price and market value. Currently, price volatility is a significant driver of its market value instability. This is especially evident during transitions between "bull" and "bear" markets, where daily fluctuations can reach as high as 30%. This indicates that the use of Bitcoin as a store of value is still not broad enough, and the participation of institutional investors is far from sufficient.

For institutional investors, the risk capital of an asset is proportional to its volatility; the higher the volatility, the more risk capital is consumed. However, Bitcoin's volatility is gradually stabilizing due to factors such as its price and market value rising rapidly, which will greatly promote the application of Bitcoin as a currency tool. This expansion of application will, in turn, promote the overall stability of its market value.

Price Increases Will Slow Down Volatility and Promote Market Value Growth to a Stable State

As the demand for Bitcoin as a store of value gradually increases and its annual output rate gradually decreases (the inflation rate will approach 0 around 2140), Bitcoin's market value will significantly rise in the future, especially with the millennial generation's growing recognition of Bitcoin's advantages over gold as an asset. Bitcoin's market value will have immeasurable upward potential, potentially surpassing gold in the near future.

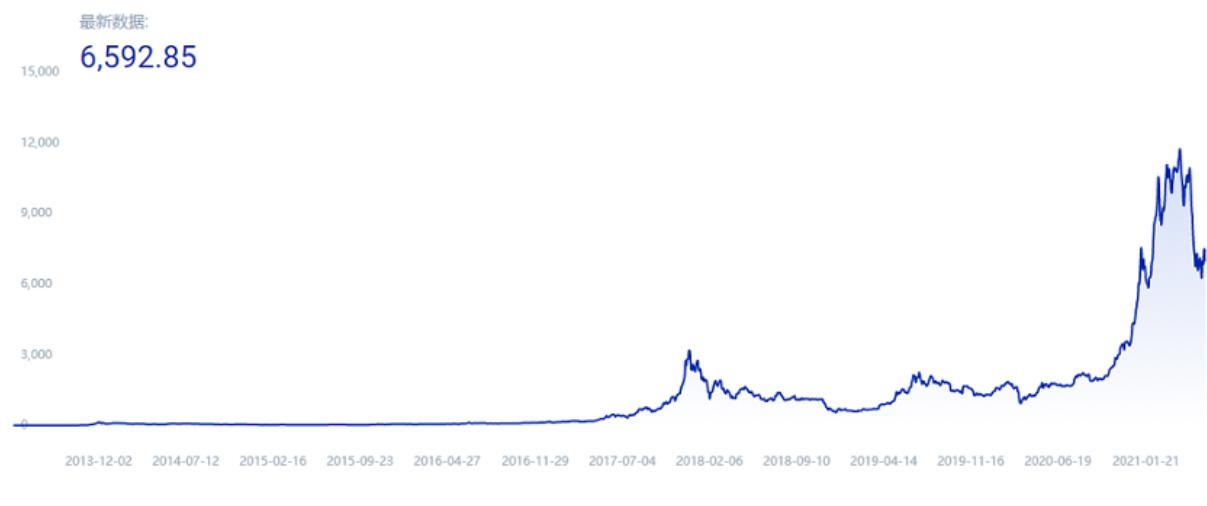

The strong growth of market value will lead to a decrease in volatility. Although Bitcoin is still in a relatively high volatility phase compared to fiat currency, its market value has increased by more than 100% compared to the same period last year, but there is still unlimited room for growth. The following is a market value trend chart of Bitcoin from its inception to the present, with the latest data showing Bitcoin's market value stabilizing around $660 billion.

Figure 1: Overall Market Value Trend Chart of Bitcoin Lifecycle

Data Source: tokenview.com

The market generally recognizes Bitcoin as digital gold. In fact, the value of gold also took time to reach a relatively stable state. Bitcoin has only developed for 11 years, and its market value still differs by an order of magnitude from gold. When Bitcoin's market value surpasses that of gold, its volatility will significantly decrease.

Let's take a look at the current comparison of Bitcoin's market value with typical global assets to glimpse its potential for growth. The following chart shows a simple comparison of the market values of Bitcoin, U.S. Treasury bonds, and gold.

Figure 2: Comparison of Market Values of U.S. Treasury Bonds, Gold, and Bitcoin

Data Source: Wind, Open Source Securities Research Institute

From the above data, it can be simply analyzed that Bitcoin has an upward potential of 10-20 times relative to gold (recently, Bitcoin's market value has seen a significant drop) and at least 10-30 times relative to U.S. Treasury bonds.

Bitcoin's market value is generally proportional to its price, as shown in the following price trend chart of Bitcoin over the past 90 days:

Figure 3: Price Trend Chart of Bitcoin in the Last 90 Days

Data Source: TokenInsight

The reason for examining the short-term curve is that we are currently in a "disadvantageous" policy environment, with a thorough crackdown on the mining industry in China. The trend has not been as extreme as in previous situations but has remained stable.

The greater the price volatility of a commodity, the more unstable the market sentiment, leading to larger trading volumes. The trading volume of Bitcoin over the past 90 days is shown in the following chart:

Figure 4: Trading Volume Trend Chart of Bitcoin in the Last 90 Days

Data Source: TokenInsight

The trading volume shows a brief peak, followed by a decline. Many Bitcoin holders do not care about price drops; they stop trading when the market declines, choosing to store their assets. At the same time, even during downturns, there are still a large number of "newcomers" entering the market, incorporating Bitcoin as a new component of asset allocation.

As Bitcoin's market value increases, changes in demand will also lead to a decrease in Bitcoin's price volatility. This is akin to a molecular formula x/y, where as y (market value) increases, the impact of changes in x on the value of x/y diminishes.

As market value rises, liquidity will grow exponentially, and the amount of capital required for the same level of volatility will also increase exponentially, thus the volatility caused by speculative capital in the market will converge.

Supply and Demand Relationship Stabilizing is Beneficial for Overall Market Stability

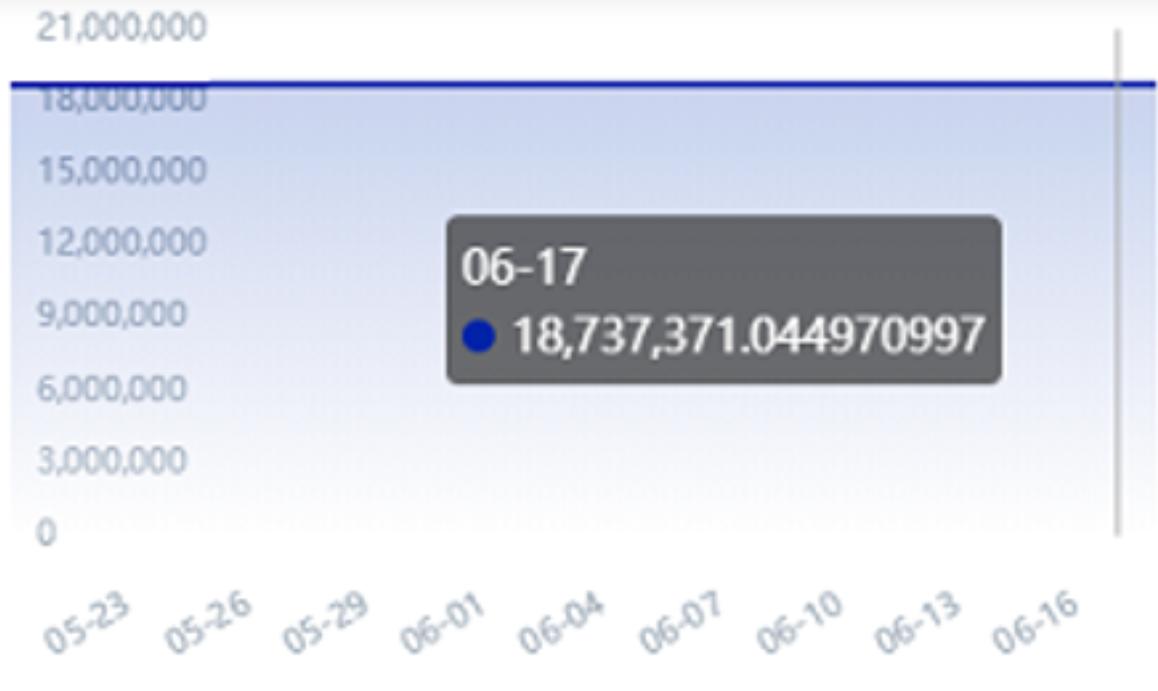

Bitcoin's supply is algorithmically fixed, with a fixed amount produced every 10 minutes. Therefore, according to traditional financial logic, there is no supply elasticity to changes on the demand side, leading to greater price volatility compared to goods with sufficient supply elasticity. Even gold has newly discovered mining volumes, while Bitcoin's total supply is definitively capped at 21 million.

Figure 5: Number of "Issued" Bitcoins

Data Source: tokenview.com

Currently, over 18.7 million Bitcoins have been mined, exceeding 89% of the total supply. Insufficient supply alone does not cause volatility; rather, the fixed nature of supply combined with fluctuations in investor demand leads to market volatility. In fact, when prices rise to a certain extent, the flexibility of the mining mechanism is amplified, and a small amount of output at high prices can effectively contribute to the market.

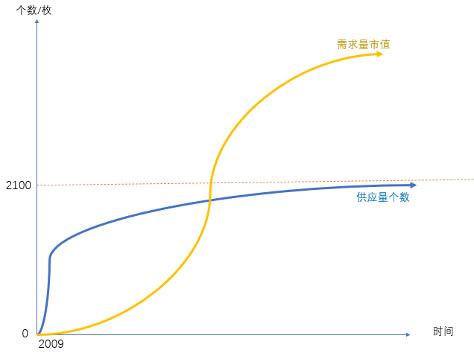

By analyzing the trends of Bitcoin supply (quantity) and market circulation demand (market value), we can observe some patterns:

Firstly, the current increase in demand is at the steepest part of the curve, while the increase in the number of Bitcoins is having an increasingly smaller impact on the total supply chain. The market circulation demand is rising, which will inevitably lead to an increase in Bitcoin's price to satisfy the supply-demand relationship.

Secondly, once demand reaches a relatively saturated stage, Bitcoin's overall market value will have grown to a certain extent, and the trends of market value and price will gradually flatten, reaching a state of supply-demand balance.

This is determined by Bitcoin's supply model, where the total number of Bitcoins will increasingly stabilize. On the other hand, the demand for Bitcoin's functions (storage, circulation) is also experiencing an upward phase. Once Bitcoin is widely accepted and applied in the mainstream market, the total demand curve will also gradually flatten. When both of these factors stabilize, we will find that their trend curves will be relatively parallel (as shown by the yellow and blue lines in the following chart).

In other words, the increase in Bitcoin's market value (the number of mined Bitcoins and price fluctuations) will basically meet the market circulation demand, while the impact of new circulation demand and the amount of Bitcoin issuance on the overall market will significantly decrease. However, at this point, the combined effect of Bitcoin's mining output and price will cover the overall growth demand for market circulation, fully fulfilling the functions of a universal currency.

Figure 6: Bitcoin Supply and Demand Diagram

Supply-Demand Curve Diagram

Although at this stage, like traditional products traded on stock exchanges, Bitcoin's price volatility is largely driven by investor demand. It can also be said that Bitcoin is significantly influenced by investor sentiment, as a considerable proportion of its participants are individual investors.

After all, Bitcoin and its technology are quite revolutionary for the world. To have unwavering confidence in Bitcoin's long-term future requires considerable psychological resilience, which brings uncertainty to the overall market. This fundamental uncertainty is the driving force behind Bitcoin's volatility.

In fact, recent events have demonstrated a direct link between public perception and Bitcoin's value. Elon Musk, who previously expressed support for Bitcoin's value creation, tweeted that due to the significant energy consumption required for Bitcoin mining, which is not environmentally friendly, Tesla would stop accepting Bitcoin as a payment method. Such a statement led to a drop in Bitcoin's price; conversely, measures or proposals by countries or governments to accept Bitcoin as legal tender typically lead to an increase in Bitcoin's dollar price.

This indicates two issues: firstly, a significant proportion of current market participants still use Bitcoin as a store of value, as only value storage users are most sensitive to market sentiment. If Bitcoin were used as a medium of exchange, this group of users would respond much more slowly, similar to how over 85% of ordinary people do not care about the exchange rate of the renminbi.

Secondly, there is still a considerable distance to achieving a stable supply-demand curve, whether for storage or circulation, as Bitcoin's demand is still in a high growth phase. Because in this model, once the two curves reach a parallel state, the overall impact of market demand (positive or negative) on the market will be significantly reduced.

Let’s take a look at the demand and habits of Bitcoin's top holders. The following is a summary of the wealth distribution of the top 200 Bitcoin addresses:

Figure 7: Bitcoin Wealth Rankings

Data Source: tokenview.com

TokenView shows that the top 10 "wealthy" addresses hold 6.2% of Bitcoin's total market value, which is an increase of about 0.7% compared to January 2019 (5.51%). Similarly, the share of addresses ranked 11-50 has also increased from 7.09% to 8.06%, showing an increase of nearly 1%, indicating an overall trend of wealth concentration.

Aside from a few major exchange addresses, comparing the transaction records and transfer details of these wallets reveals that these large Bitcoin holders have not engaged in unilateral dumping or price manipulation. Instead, they have continuously accumulated assets during Bitcoin bear markets, indicating that large holders still use Bitcoin as a store of value.

Including exchanges, using Bitcoin as a store of value remains one of the direct means of wealth increase, which also indirectly contributes positively to Bitcoin's price stability.

For market participants, whether for liquidity or for storage and investment needs, the greater the risk and volatility of Bitcoin, the higher the probability of profit and loss. Therefore, from a subjective market perspective, the overall trend is likely to be more stable.

Expanding Application Scope Will Mitigate Volatility Impact, Converging Overall Market Value Volatility

As Bitcoin adoption increases, the demand-side change curve will flatten, leading to a decrease in price volatility.

Currently, the digital asset sector has gradually moved away from a single spot trading model, with options, contracts, and various financial derivatives integrating with traditional finance, and Bitcoin as the anchor asset occupies a significant portion of this landscape, providing a solid foundation for the normalization of Bitcoin's use.

The recent market surge over the past year has further facilitated the in-depth development of Bitcoin's application. Bitcoin has gained widespread social consensus, particularly with the successful IPO of Coinbase, which has significantly expanded the consensus base for digital assets.

In terms of value storage, an increasing number of institutions and enterprises are supporting Bitcoin through "on-balance" or "off-balance" means. According to publicly available data, there are currently 31 listed companies or publicly traded products holding Bitcoin, totaling over 1 million Bitcoins, accounting for about 6% of Bitcoin's circulating supply.

Many institutions are actually hidden "off-balance." A considerable number of fund companies, especially private equity funds, indirectly hold Bitcoin assets. Therefore, the amount of Bitcoin assets held by "public" institutions is far more than 6%, and the application scale of Bitcoin as a value store has far exceeded the general public's understanding.

In the payment sector, an increasing number of young people are willing to accept Bitcoin and digital assets. This provides a foundation for expanding the application scope of Bitcoin, as more merchants and payment service providers accept Bitcoin, creating market demand for Bitcoin's exchange application value.

Using Bitcoin for payments has become an undeniable trend, akin to the widespread adoption of mobile payments in the past, being embraced by more and more merchants and individuals. This also expands the application scope of Bitcoin, thereby enhancing its value empowerment.

From the speed of Bitcoin's payment application expansion, Bitcoin has become a financial product accepted and used across all fields, with the value attributes of virtual currency becoming increasingly dominant. Some countries are attempting to directly use Bitcoin as legal tender, which amplifies Bitcoin's currency value and fully realizes its monetary application value, significantly boosting Bitcoin's "practical" value.

This widening application scope will, in turn, drive the manifestation of its value storage characteristics, maintaining constant value demand.

On the other hand, when fiat currencies worldwide are excessively issued, Bitcoin's asset hedging characteristics become apparent. Citizens in countries with severe inflation prefer to hold Bitcoin rather than their local fiat currency, providing a long-term development foundation for Bitcoin. As more goods and services adopt Bitcoin pricing, it won't be long before society partially enters the Bitcoin "Satoshi Standard" era, at which point the price volatility of Bitcoin relative to fiat currency will cease to exist.

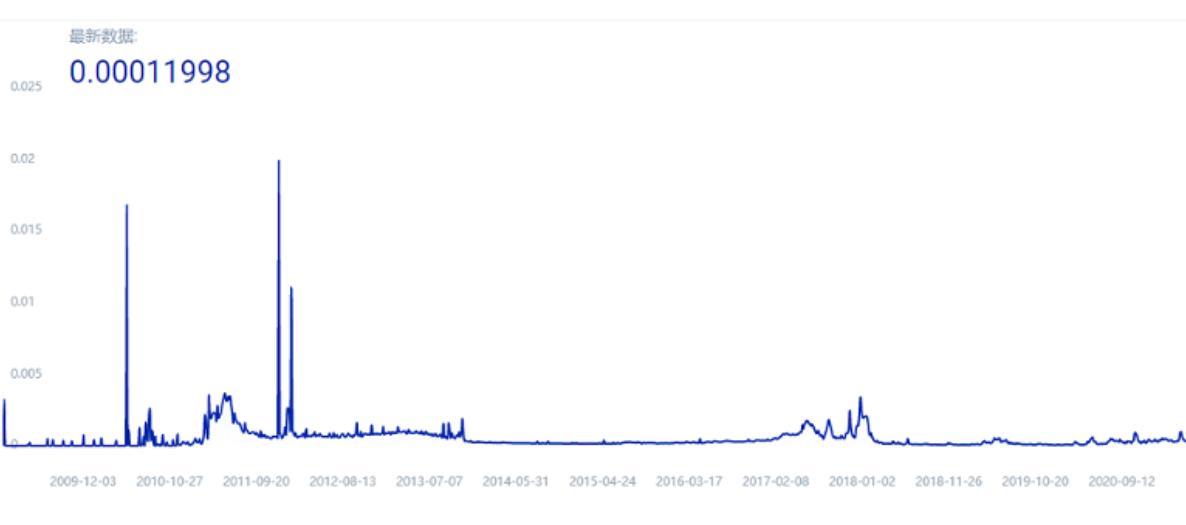

From a technical perspective, Bitcoin's settlement costs have also remained within an acceptable range. The following chart provides a brief analysis of the payment costs of Bitcoin as a payment method.

Figure 8: Cost of a Single Bitcoin Payment (btc)

Data Source: tokenview.com

Relatively speaking, the payment costs are within a reasonable range. During periods of rapid price increases, transaction costs may rise, which is an inevitable process when transitioning from a rare asset to a universal currency. As price stability increases in the future, transaction/payment costs will become increasingly controllable and widely accepted.

Overall, in terms of transaction costs, Bitcoin is one of the most stable performers in the mainstream digital currency market, and it is at a lower level compared to fiat currency. Therefore, in terms of transaction costs, Bitcoin has advantages over fiat currency, especially in special scenarios such as cross-border transactions.

In summary, whether from the maturity of Bitcoin, its market trend analysis, or the development trend of market recognition capabilities, there is no reason for its volatility not to gradually stabilize, and the speed of this stabilization is quite rapid; all we need is time.

This stable trend is fundamentally driven by people's recognition of its currency attributes, which follows the basic laws of currency development: commodity trading → store of value → medium of exchange → unit of account. We are currently nearing the midpoint of the third stage.

Performance Bottlenecks in Payment Scenarios Are Continuously Being Overcome

The performance bottleneck of Bitcoin's mainnet is a consensus, which relates to Satoshi Nakamoto's original design intention.

Satoshi did not envision that future ecological applications would directly apply to the mainnet. In other words, his original intention was to establish the core network of the currency system itself, that is, the primary network of currency, which is a small but beautiful product, rather than a large and comprehensive system. The primary network of currency primarily demands decentralization and security, rather than performance and other functional characteristics that application scenarios focus on.

As the largest network computer in terms of computing power globally, Bitcoin's payment performance may not even match that of a regular computer serving as a centralized payment system. Its core principle lies in using large-scale distributed computing power to solve the decentralization and security issues of the currency network, which aligns with the modern idea of "machines replacing humans."

This is the core value of the primary network, as it bridges the trust gap between the supply and demand sides of payments.

Figure 9: Core Value of Bitcoin's Primary Network

Data Source: Public Information

From a design principle perspective, this is consistent with traditional currency systems. In traditional currency systems, central banks primarily address the issue of endorsement mechanisms, not concurrency or performance issues.

Therefore, the development of Bitcoin's application ecosystem will inevitably follow this developmental path to some extent. TPS will no longer be a bottleneck, just as people do not expect every transaction to occur within the central bank system.

Conversely, there are numerous cases of people blindly attempting to modify the performance of Bitcoin's mainnet based on erroneous perceptions. Attempts to expand the Bitcoin mainnet through forks like BCH and BSV have not gained traction and cannot replace the BTC mainnet. Any performance enhancement that sacrifices decentralization and security will be counterproductive and end in failure.

Expansion Through Layer 2

Bitcoin is a new technological system and infrastructure, much like the previous generation of the internet. When the internet was first born, people thought of it as another communication channel parallel to telephones, radios, and televisions. In reality, the internet was a completely new foundational technology platform at the time, where people cultivated a different form of radio, video, and social media. The social, community, and media forms based on the internet are experiences that traditional methods had never encountered, especially in terms of transmission speed and communication efficiency.

Thus, the internet is not something that exists in parallel with traditional applications at the application level; it is a new generation of restructured underlying architecture.

Blockchain and Bitcoin also represent underlying architecture, which can be understood as a major version upgrade of the internet through decentralized thinking. In the digital asset world based on Bitcoin, there will be digital forms of currency, assets, securities, bonds, and other entities, representing a new platform and a generational leap in infrastructure based on trust relationships.

On this new platform, there will be elements that traditional fields lack, as well as those that continue traditional evolution. The vitality of the new platform is much stronger than imagined, and its impact exceeds people's expectations.

Currently, Bitcoin is still in the early development application stage of Layer 1, and its value has not yet been fully explored. Firstly, the entire digital currency industry is still not large enough, lacking explosive applications for the general public. Secondly, the industry's understanding of Bitcoin itself still needs improvement, especially regarding its functional scope.

Therefore, the author proposes that the industry needs to define the development of Bitcoin applications in layers, similar to Ethereum but with distinctions. We should define the Bitcoin mainnet as Layer 1, with its function being Bitcoin itself, akin to the role of a central bank in traditional finance; while Layer 2 should be defined as various applications developed around Bitcoin. Layer 2 can be centralized or decentralized, and it can involve blockchain technology or non-blockchain technology, with the goal of building traffic and shaping application value.

All regulatory matching should occur in Layer 2, which will facilitate the expansion of the application market while meeting the institutional and policy requirements of different countries/regions, avoiding the misleading dichotomy of "centralization vs. decentralization" that positions Bitcoin in opposition to traditional financial and technological systems.

From a technical perspective, Layer 1 has a TPS ceiling, while Layer 2 does not. Under this Layer 1---Layer 2 architecture, the future Bitcoin L1 mainnet will only serve as the final settlement layer for processing settlements between large centralized and decentralized L2 applications.

According to Bitcoin's current acceptance performance (in the most ideal state, the average transaction size is 225 bytes, under a 1M block limit, approximately 4,400 transactions can be packed every 10 minutes, which is about 7.3 transactions per second, or roughly 7 transactions per second), it can handle about 7 transactions per second, equating to 600,000 transactions per day. If we treat the mainnet as a central bank and L2 applications as commercial banks (or third-party payment companies), the number of settlement demands on the mainnet central bank is (N*(N-1))/2, where N is the number of commercial banks.

This means that it can accommodate up to 1,095 L2 applications. This is based on the current situation without expansion and the extreme topology of commercial bank operations. In reality, a single L2 cannot possibly conduct business with all other L2 applications, and expansion can also exponentially increase business capacity. Therefore, overall, supporting around 10,950 L2 commercial banks (approximately 10,000) is entirely feasible.

Centralized L2 applications themselves have no performance limitations, thus meeting the performance requirements of Bitcoin versions of VISA, UnionPay, and Alipay, with demands for 100,000 concurrent users or even larger not posing any bottlenecks. This completely resolves the TPS performance bottleneck of the entire system structure. Ignoring political policies, from a purely technical perspective, the Bitcoin system fully meets the technical requirements of a universal currency.

Let’s revisit the currency attributes of gold and Bitcoin. Gold has fatal shortcomings as a currency, while Bitcoin fills this gap. Gold lacks marketability in terms of space and value on Layer 1, thus relying on L2 (gold standard banks) to achieve payment characteristics across space and value scales.

This ultimately leads to gold being physically concentrated in central bank vaults, resulting in centralized institutions forcibly abolishing the gold standard (the collapse of the Bretton Woods system). In contrast, Bitcoin has no L2 institution that can enforce the central control of Bitcoin after forcibly aggregating it. Even in the future, mainstream Bitcoin L2 applications will be entirely decentralized, allowing L1 owners to retrieve their assets anytime and anywhere without censorship. It can be seen that L1 and L2 are not completely decoupled; they need to coexist complementarily to perfectly ensure the integrity and fairness of the currency system. L1 addresses security and credit issues, while L2 primarily addresses performance and application issues.

In the expansion of L2, we will briefly examine specific typical application scenarios from both decentralized and centralized perspectives.

Decentralized Layer 2 Expansion

In the expansion of L2, decentralization is one path, and there are already many applications, including the Lightning Network and cross-chain projects.

The off-chain protocol to enhance network scalability has sparked a wave of interest within the cryptocurrency community. These solutions allow the vast majority of transaction processing tasks to be shifted from Layer 1 blockchains to off-chain systems, thereby bypassing all costs, performance, and latency issues associated with Layer 1 blockchains. The common feature of these projects is to build a routing system that maps assets on Layer 1 to another (external) service for circulation, specifying asset custodians and conditions for unlocking assets.

- The deposit process essentially involves depositing user funds into the routing protocol, which then maps this asset to an equivalent amount in another system.

- When updating user balances, the routing system receives notifications of balance updates.

- The withdrawal process corresponds to the deposit process, where users withdraw funds to the Layer 1 blockchain through the routing system, while their corresponding balance in the other system decreases.

The primary function of this routing system is to guide users to custodial services, such as decentralized exchanges. Another increasingly popular application scenario for routing is to achieve interconnectivity between different chains or different blockchain project systems, which is also the origin of sidechains.

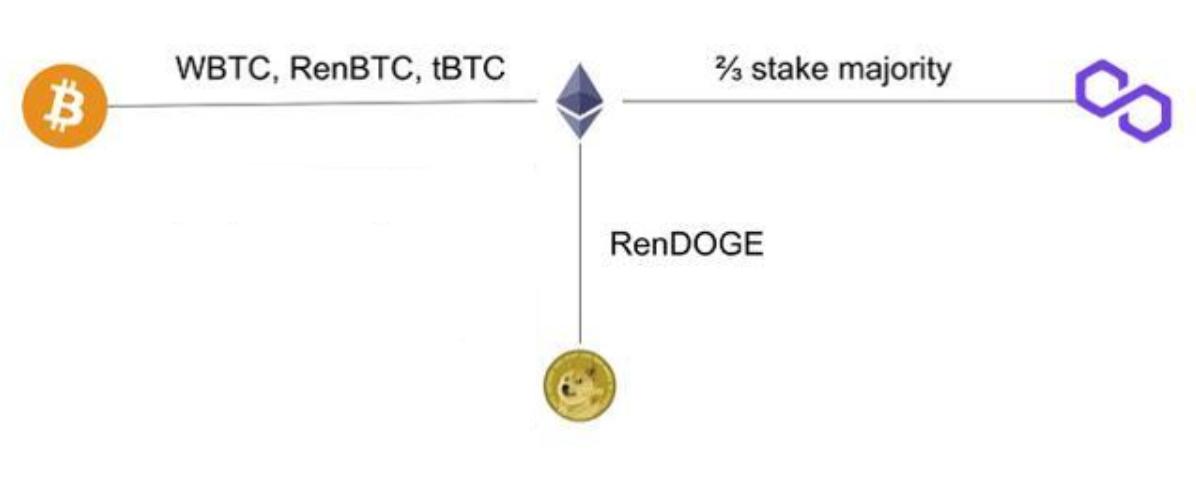

WBTC is a classic application of this routing design: transferring Bitcoin to Ethereum for circulation and application.

Figure 10: WBTC Principle Diagram

Data Source: Public Information Compilation

The most crucial aspect of this decentralized routing expansion is its security model, as it is completely independent of the L1 network. In the WBTC project, BitGo Trust is responsible for holding the locked BTC and issuing an equivalent amount of WBTC on Ethereum; smart contracts on Ethereum track all accounts involved in WBTC transfers.

In this case, Ethereum's security model is independent of Bitcoin, and the WBTC routing security model is independent of both Ethereum and Bitcoin. This effectively treats Ethereum as a sidechain for Bitcoin, enabling cross-chain transactions from Bitcoin to Ethereum. Thus, it is not difficult to see that the entire system's greatest security reliance comes from the routing itself, and users need to trust that BitGo will respect the account balances recorded in the smart contracts.

Cross-chain technology is key to realizing the value internet; it is the remedy that rescues blockchains from isolated islands and serves as a bridge for blockchain expansion and connectivity.

Industry giants like Binance have promoted the launch of the Binance Smart Chain, aiming at cross-chain financial infrastructure and unlocking value interconnectivity. Notably, its cross-chain financial infrastructure is not limited to establishing DeFi (decentralized finance) solutions for interconnecting blockchains but also includes bridges to CeFi (centralized finance).

This aligns closely with the author's layered theory of the Bitcoin ecosystem, as decentralization does not mean completely abandoning centralized applications; the two are compatible.

Additionally, the currently hot NFT (non-fungible token) ecosystem is emerging, with its advantage being the mapping of offline assets onto the blockchain, forming interactions between off-chain and on-chain. Theoretically, NFTs can expand across multiple chains, such as Ethereum or Polkadot, but they can all serve as L2 applications on the Bitcoin network. This understanding will gradually be accepted by the industry.

Centralized Layer 2 Expansion

On the L2 level of Bitcoin, the more important aspect is the expansion of centralized applications, which may differ from Ethereum's positioning. Bitcoin can integrate more extensively with traditional financial institutions, merchants, business circles, and specific business scenarios.

Traditional leading clearing organizations like VISA have already begun to conduct USDC settlements on Ethereum, and similarly, they can connect to the Bitcoin mainnet through the routing architecture described earlier, conducting daily or monthly settlements. By constructing a clearing center using traditional technology, they can support Bitcoin's clearing and settlement, connecting with global merchants and facilitating circulation worldwide. On the acquiring side, there are leading payment institutions like PayPal joining the traditional financial sector, as well as long-term efforts from payment institutions like BitPay that focus on acquiring Bitcoin and other mainstream digital currencies. On the issuing side, digital currency wallets like Crypto and UQWallet are integrating with VISA and other mainstream international card organizations' issuing and clearing networks, expanding the payment capabilities of digital currency users into traditional financial payment networks.

Figure 11: Crypto

Data Source: crypto.com

Figure 12: UQPAY

Data Source: UQPAY

Conclusion

It is evident from the technical analysis across several dimensions that Bitcoin fully possesses currency attributes and functions, making it suitable for a broader range of payments, including B2B and B2C retail scenarios.

Even though Bitcoin's volatility is significant at this stage, it does not hinder its use as a daily payment tool and means. Merchants can use third-party Bitcoin acquiring systems to convert Bitcoin and fiat order amounts in real-time to mitigate the risks of Bitcoin's price volatility, thus achieving a hedge against the volatility of Bitcoin in daily payments. People will gradually diminish the barriers between centralization and decentralization, with the important aspect being the ability to provide a better user experience and enhance the security of user assets and data.

The revolutionary aspect of Bitcoin lies in its status as the greatest reserve asset in history and a superior currency network. Holding Bitcoin has become an effective way to protect developing economies from the potential impacts of fiat currency inflation.

In the face of technological innovation trends, countries/regions worldwide are showing an increasingly inclusive trend, including policy formulation, environmental shaping, and economic support. Recently, in the wave of digital asset and blockchain technology innovation, various countries/regions have exhibited some policy differences for various reasons, but the overall trend is clear: Bitcoin is bound to move towards the payment end, gradually fulfilling its currency functions, and this influence will grow larger until the arrival of the Bitcoin Satoshi Standard era.

At the Bitcoin 2021 conference in Miami, the President of El Salvador, Nayib Bukele, planned to introduce legislation to make it the world's first sovereign nation to adopt Bitcoin as legal tender.

Figure 15: Nayib Bukele Social Media Screenshot

Bukele stated that the country is collaborating with digital wallet company Strike to leverage Bitcoin technology to establish modern financial infrastructure. Subsequently, the country voted and officially passed a bill to make Bitcoin legal tender. This bill will take effect 90 days after being published in its Official Gazette.

This provides a good example of Bitcoin's "legalization" to replace traditional financial infrastructure, although replicating this on a larger scale in other countries is challenging. Once the country achieves positive results, other countries are likely to follow suit with similar policies. The "Bitcoin Law" in El Salvador explicitly states that Bitcoin is legal and fulfills currency functions, including payment circulation and exchange. It is reported that several countries, including Paraguay, will formulate similar laws to follow suit.

At the same time, in our previous discussion on the globalization of computing power, it actually affects the production/distribution side of Bitcoin. National policies are also generally moving towards inclusivity. For instance, Miami, Florida, has begun to attract Bitcoin miners, offering support through cheap nuclear power.

Francis Suarez, the Mayor of Miami, stated that Miami is open to Bitcoin miners worldwide, hoping to support miners willing to come to the area by enhancing the city's virtually unrestricted supply of cheap nuclear energy. This also validates the author's earlier prediction that Bitcoin possesses global currency attributes, with a stronger resistance to external interference than any fiat currency.

Marx said, "Gold and silver are not naturally currency, but currency is naturally gold and silver." Bitcoin, on the other hand, inherently carries the DNA of currency. After traversing the stages of value storage, universal recognition, and circulation application, Bitcoin is the largest and safest universal currency for value storage.

By around 2050, when Bitcoin reaches $1 million per coin, we may witness the "Satoshi Standard" era, where Bitcoin payments are applied globally, and people will no longer be fixated on Bitcoin's asset or currency attributes, nor will they discuss its legality. What we need to do now is accelerate the world's transition to the crypto world and strive together!

Risk warning

Risk warning Risk warning

Risk warning

Popular articles