Understanding the ARCx DeFi Passport: The "Sesame Credit" of the DeFi World

It has the potential to become a core component of the reputation system and identity system in the DeFi ecosystem.

It has the potential to become a core component of the reputation system and identity system in the DeFi ecosystem.This article is from ChainNews, authored by Jiawei.

The synthetic asset protocol ARCx recently announced the completion of a $1.3 million funding round, led by Dragonfly Capital, Scalar Capital, and Ledger Prime, through the purchase of the protocol's governance token ARCX. ARCx stated that the investors in this round purchased the pre-split ARCX tokens at a price of $7,500 (equivalent to a post-split token price of $0.75), with a lock-up period of 6 months and monthly unlocks.

So far, this protocol initiated by DeFi Weekly founder Kerman Kohli has raised over $8 million in total, and the product has undergone several upgrades.

Along with announcing the completion of the new funding round, ARCx also officially revealed the details of its V3 product "ARCx Sapphire." The core product of ARCx Sapphire v3 is called "DeFi Passport," a product similar to "Sesame Credit" in the decentralized world, which has the potential to become a core component of the reputation system and identity framework in the DeFi ecosystem.

Blockchain itself is anonymous, and DeFi cannot assess the credit of participants; the protocol treats every user equally. In mainstream finance, for example in lending, when individuals or businesses apply for loans from banks, the banks assess their willingness and ability to repay. However, such assessments do not exist in DeFi lending. Credit risk management in DeFi heavily relies on over-collateralization, which also results in inefficient resource allocation in DeFi lending [1].

Suppose in DeFi lending, it is possible to define a "good borrower" through several indicators, such as never having been liquidated or actively repaying loans; it seems that the collateralization ratio for such borrowers could be relaxed to reduce collateral requirements and improve resource allocation efficiency.

The vision of ARCx Sapphire v3 is just that—establishing an on-chain credit assessment system that incentivizes the establishment of reputation in DeFi, allowing on-chain credit to generate its due value.

Understanding ARCx Sapphire v3

ARCx Sapphire v3 quantifies the credibility of each DeFi Passport holder's on-chain address by issuing "DeFi Passports" based on their credit scores. Credit scores will be determined by analyzing the historical activities of the holder's Ethereum address, with a range set from 0 to 999. This credit score determines the collateralization ratio the protocol offers to users.

For addresses with high credit scores, the DeFi Passport can provide competitive lending collateralization ratios (e.g., 105%, while the minimum collateralization ratio in MakerDAO is 150%. A lower collateralization ratio means less collateral is required to borrow the same amount of money).

In ARCx Sapphire v3, the application process for the DeFi Passport is as follows:

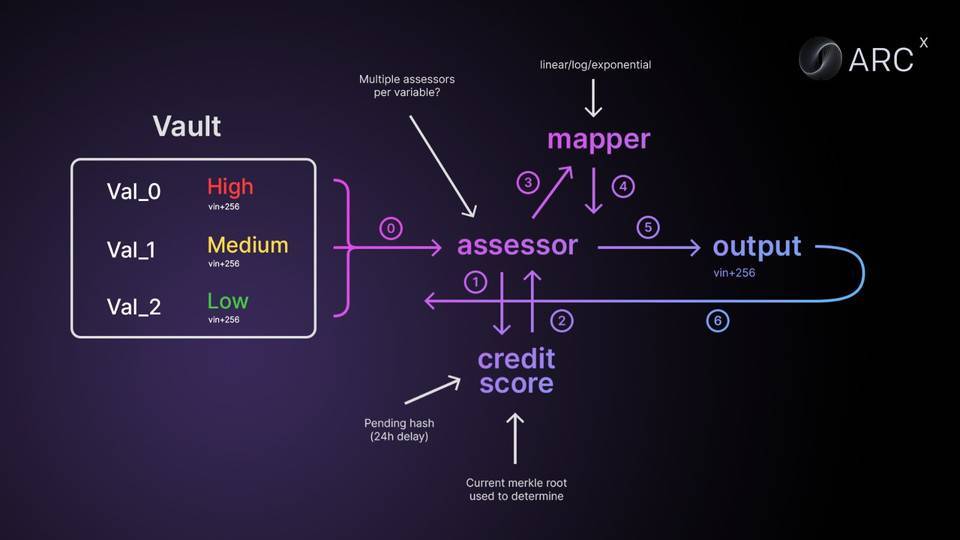

Consider a collateral account "Vault," where its collateralization ratio is dynamically determined by the credit score of the DeFi Passport. In this case, the Vault (containing collateral and its assets) will send a set of numbers to the smart contract Assessor. The Assessor will request the user's credit risk from the Credit Score, represented by a number from 0-999. Then, the Credit Score will be mapped to a continuous distribution via the Mapper function, and the mapped result will be returned to the Vault as the specific collateralization ratio for that user.

The credit score of the DeFi Passport is dynamic and can be updated as needed.

Phase 1

In the first iteration of the product, on-chain addresses applying for the DeFi Passport need to complete an identity test to prove that the address is not a bot. After receiving the DeFi Passport, holders will gain exclusive access to high APY liquidity mining opportunities provided by ARCx and its partners.

Over time, DeFi Passport holders will continuously accumulate credit scores and enter Phase 2.

Phase 2

The second phase will take the initial collateralization ratio as a single variable, dynamically changing based on the borrower's credit score. In the early stages of the protocol, the system will adopt a small scale to reduce risk. This will be achieved in two ways:

- Enabling boundary risk parameters, such as providing 105% collateralization loans only for BTC and ETH.

- Offering more credit to good borrowers. A good borrower may meet the following conditions: having loans for several months on Compound, MakerDAO, or Aave; their collateral has never been liquidated; maintaining a large collateral position while keeping a high (time-weighted) collateralization ratio; and actively repaying loans during periods of high market volatility.

Additionally, ARCx has established a machine learning model to backtest the classification of "liquidated" or "non-liquidated" positions, reflecting the correlation between on-chain activity and credit risk.

How to Apply for DeFi Passport?

The early issuance of DeFi Passports will be conducted in batches.

The first batch will issue 100 addresses, representing 100 unique identities. The first batch of identities will receive the "First Edition" DeFi Passport, while the second batch will receive the "Second Edition," and so on.

Applicants must visit arcx.money, connect their wallets, and collateralize 1000 DAI to join the waiting list. To encourage long-term participation from users, applicants need to collateralize this DAI for a certain period. The collateralization period may change; for example, holders of the first edition DeFi Passport may need to collateralize DAI for one year, while subsequent versions of the DeFi Passport may require longer collateralization periods.

Early DeFi Passport holders will also enjoy exclusive yield farming opportunities, borrowing at low collateralization ratios, or receiving corresponding benefits based on the batch or version of their DeFi Passport.

Future Vision

In the future, ARCx plans to add more evaluation scores and pages for the DeFi Passport, including:

- Yield farming scores, which assess whether farming participants support the long-term development of the protocol rather than simply "mine-sell-withdraw."

- Airdrop scores, which evaluate whether on-chain addresses hold airdrops long-term or sell them immediately upon receipt, assessing whether the address supports the long-term development of the protocol.

- Governance scores, which assess the level of participation in on-chain governance. In addition to measuring governance participation, various decisions made by users on-chain and their governance nature within the protocol can also reflect their motivations and future behaviors.

- Trader scores, which distinguish between bots and real traders, allowing DeFi protocols to choose different ways to interact with counterparties. For example, DEX protocols may offer lower trading fees to real traders compared to bots.

Conclusion

The widespread adoption of over-collateralization in DeFi locks up liquidity—any asset used as collateral means forgoing other higher-yielding uses. For instance, collateralized assets mean giving up the right to sell at a price peak. The greater the asset price volatility or the longer the collateralization period, the higher the liquidity cost.

ARCx Sapphire v3 calculates the credit score of addresses by assessing their historical activity records, incentivizing the establishment of an on-chain credit system that can lower collateralization ratios and improve the utilization efficiency of DeFi resources, the practical significance of which is self-evident.

Overall, the adoption rate of the DeFi Passport will be key to its future development. If the product is widely accepted and can attract more DeFi protocols to offer benefits to high credit score addresses, the measurement of user credit will become more accurate, and the product use cases will expand accordingly; if the adoption rate is low, the credit score may become an empty promise, lacking credibility. The performance of ARCx Sapphire v3 is worth looking forward to.