How do traditional venture capitalists participate in cryptocurrency project investments? What should LPs pay attention to?

In the highly uncertain emerging market of Crypto, how should VCs get involved?

In the highly uncertain emerging market of Crypto, how should VCs get involved?This article is from Suyuan Yuxin.

Crypto, as a new asset class, generally follows the same investment principles as traditional markets. However, in practice, GPs need to reassess and sometimes adjust their investment methods based on the characteristics of crypto when building crypto venture capital funds. Even if the principles and philosophies remain unchanged, GPs cannot simply replicate previous practices and strategies when investing in crypto, and LPs will not expect GPs to remain static.

Most new GPs will follow a standard venture capital portfolio model, reserving about half of the 30 portfolio company slots for those companies that are not initially in the pool. However, investing in crypto is different; this model cannot be applied without further consideration.

When constructing a crypto venture fund portfolio, LPs' perspectives and findings are:

Excellent GPs are generally not swayed by the price fluctuations of Bitcoin and other cryptocurrencies; they often analyze the industry from a more macro perspective, providing excess returns for themselves and LPs.

In the next five to ten years, venture capital will also face opportunities for a change of guard. Crypto networks will become the backbone of global public infrastructure and are likely to lead a new generation of internet-based services. If venture capital can ride this wave, new opportunities may emerge.

To ensure investments are not impaired, GPs need to learn to timely recover funds from failed crypto assets and increase bets on successful ones, striving to excel in the crypto investment market.

The reasoning is clear to everyone; let's discuss the specifics.

1. First, sketch out a portfolio

The concept and method of portfolio construction by GPs is the first crucial hurdle, and its impact on returns may be greater than any subsequent investment decision. Like many things in investing, clarifying the concept is simple, but executing it well is challenging.

Therefore, GPs must first clarify which startups they can access, then understand the level of risk and return that they and LPs can digest, and finally adjust the portfolio accordingly based on these parameters.

Of course, details determine success or failure. In the public market, constructing a portfolio involves determining position sizes and then diversifying those positions across various sectors and other aspects. Achieving this step is already quite difficult, and in venture capital, faced with various variables at different investment stages, GPs may sometimes make decisions that adhere to convention, leading to path dependence due to weak investment realization capabilities.

As a result, early mistakes made in the fund's lifecycle become more entrenched as time goes on, making it harder to correct through selling off some assets or rebalancing, and they can affect opportunities later in the fund's lifecycle, even leaving negative impacts after the cycle ends.

For example, the initial investment size of GPs can affect their ability to set terms and how much they can invest in follow-on rounds. However, GPs typically need to develop deeply within a given sector, which is akin to betting on a very small probability. If the investment scope is too broad, it is easy to encounter direct competitors, which is generally not favored.

GPs investing in crypto should recognize that they need to independently propose an ideal strategy for constructing a crypto investment portfolio, which is no easy task. Moreover, for GPs, finding a strong answer and understanding where the value of the next generation digital economy will come from is just a key stepping stone. Absorbing these insights and then designing a complete portfolio that can yield substantial returns is another matter that requires thorough research.

2. Identify the sector and choose the right tools

LPs hope GPs will understand which vertical business lines may grow and how to accumulate and capture value. Over the past decade, the thesis around "Bitcoin is money" has been discussed at many levels of the stack: Bitcoin itself, exchanges, apps (wallets, hardware security modules HSM, payment channels), or adding another layer to Bitcoin's blockchain with the Lightning Network (making Bitcoin transactions faster and cheaper). Successful GPs can choose the correct vertical direction and the appropriate investment level, and LPs are eager for GPs to balance both.

In traditional venture capital, equity is the main source of value for GPs. In crypto investments, the primary forms of investment are digital assets (network tokens), convertible assets like SAFT (Simple Agreement for Future Tokens), or equity in startups, including claims to future token issuances. However, the ultimate value still rests on the tokens rather than the equity.

In addition to crypto networks, GPs may also consider equity investments in traditional "picks and shovels" businesses (an investment strategy referring to the fact that most gold miners failed during the gold rush, while those selling picks and shovels profited), and constructing a portfolio that includes both types of investments is more challenging.

We believe this space is in its infancy and is advancing rapidly each year, not to mention how quickly things can change between the initial delivery and the end of investments. Therefore, GPs can consider that the future of crypto is unpredictable and allow their imaginations to run wild, but they must also think deeply. With strong support from LPs, GPs have the freedom to choose investment tools to maximize value for LPs.

In some vertical markets, investing in tokens may be the most reasonable approach, typically in decentralized market networks; in others, equity investments may be more feasible, such as exchanges; and in yet others, the situation is still unclear, like Layer 2 (building a network on top of Layer 1 public chains to enhance Layer 1 network performance, with related concept tokens like LRC, ZKS, MATIC, and OMG). LPs are looking for GPs who have deep thoughts and insights, are mature enough to navigate the trade-offs between various investment tools, and are disciplined and resolute in their actions.

3. Fund size and investment stage

The size of the fund is the biggest factor affecting GPs' portfolio strategies, as it constrains portfolio construction and must align with the investment sector and the fund's risk parameters. If the fund size is too small, GPs may not be able to execute their investment strategy; if the fund size is too large, the risk-return profile may differ from what GPs initially promised LPs.

The significant investment opportunities in any specific sector are very limited and will generally be fewer than the amount the fund needs to deploy. Given that most eye-catching risk opportunities in crypto are still in seed and early rounds, with typical seed rounds around $2-4 million, it makes little sense for GPs to set an excessively large crypto venture fund size at this stage.

Thus, GPs need to convince LPs that their strategy and portfolio construction align with the fund size.

Generally speaking, the earlier the stage of investment in a venture fund, the higher the potential return on initial investments, and the more valuable the pro-rata investment rights in later rounds, but the risks are also greater. The greater the difference between pre-seed and seed rounds, the larger the return disparity between the top and bottom quartiles. Although it may be less efficient, choosing a significantly different arena allows new GPs to showcase their advantages in the market.

Traditional venture capital has fixed rounds like Series A and seed rounds, but crypto networks also have similar investment rounds because GPs can invest in liquid tokens through secondary markets and participate in projects at earlier stages. These early rounds include locked token phases, pre-network launch phases, pre-testnet phases, pre-technology phases, pre-whitepaper phases, and even pre-team phases. Just like non-crypto startups, mature crypto investors will summarize the thesis of the maximum risks at each stage to mitigate risks.

The maturity time for crypto network investments is not short, but their realization time (more precisely, "tradeability") is certainly shorter, with fewer rounds experienced before realization. Most crypto networks do not take 6-9 years to launch their networks and respective tokens, nor do they raise more than five rounds of funding; they typically go through a few rounds of private financing.

Despite incomplete information, obtaining these opportunities early and underwriting risks is primarily what smaller new funds are doing. Unlike traditional venture capital, the realization of crypto investments does not signify maturity, and this will be discussed further. Understanding this is key to grasping the risks in the crypto sector.

4. Position size and diversification

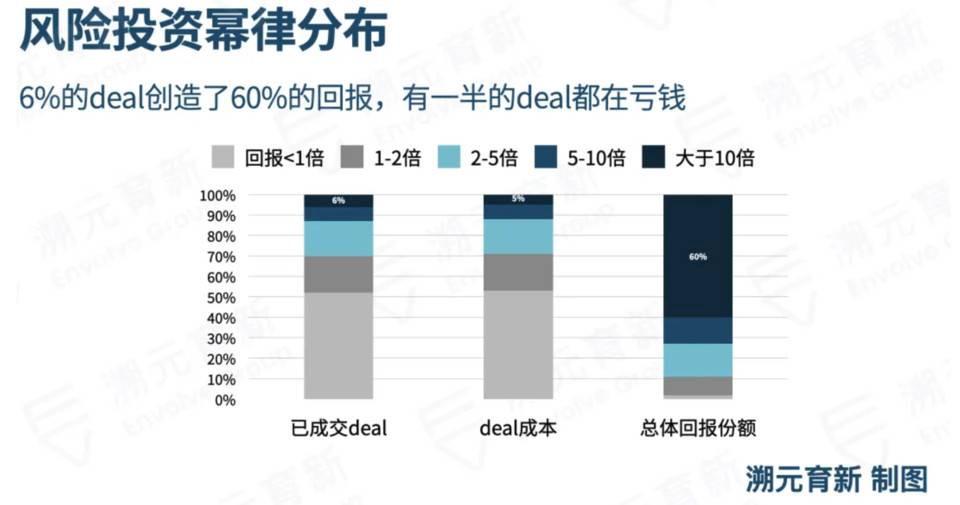

In the venture capital asset class, maximizing exposure to successful companies while diversifying risk and maintaining a balance is as challenging as walking a tightrope on a cliff. As we mentioned in our last weekly report, traditional venture capital returns exhibit a power-law distribution, where a small number of standout companies generate the majority of returns. Former a16z partner Benedict Evans found that 12% of investments (equivalent to 10% of invested capital) accounted for 74% of total returns in U.S. venture capital.

Venture capital portfolios are driven by outliers. If you tend to use mathematical models to extrapolate results, Jerry Neumann (founder of Neu Venture Capital, who invested $7 million in mobile analytics service Flurry, which was sold to Yahoo for $240 million in 2014) has done an excellent job simulating how power laws affect venture capital portfolio returns. He concluded that while broader portfolios have better chances of yielding attractive returns, one must also acknowledge certain practical limitations, such as constraints in managing operational portfolios.

Analysis of historical investment return data for crypto VC indicates that the power-law distribution in crypto may be stronger than in traditional startup investments. This poses a challenge for GPs investing in crypto; if they miss out on unicorn shares, the fund will perform poorly, and the investment sector is narrow, with only 10-15 special transactions globally each year.

GPs may find it difficult to control the win/loss ratio, so their advantage may depend on maximizing returns from the star companies they invest in. Understanding this, GPs generally choose more concentrated portfolios, although doing so also brings concentrated risks.

A concentrated portfolio refers to allocating funds to 10-15 core positions, with the maximum position size reaching 15%. This does not necessarily exclude starting with a larger portfolio before refocusing on successful companies. Concentration allows VCs more room for choice and abundant resources to add value to the invested companies. Ultimately, portfolio diversification should not come at the expense of quality and portfolio support.

5. Average investment size and target ownership

Target ownership is the percentage of the invested company that the fund hopes to hold. For example, if a fund invests $2 million in a company with a pre-tax valuation of $18 million, the fund will hold 10% of that company.

For many traditional venture capital firms, target ownership is important because there are too few breakout companies in each venture portfolio, meaning that their high-risk exposure is necessary for fund returns. Additionally, a larger ownership stake allows GPs to exert greater influence, set terms, and/or participate more in fund governance as board members.

However, funds should focus on risk exposure and valuation, allowing ownership to derive from that rather than explicitly setting it as a target. This is even more true in token investments, where the governance role GPs may play is either diminished or not closely tied to their own investments. Especially in DPoS (Delegated Proof of Stake) networks, other investors may delegate their votes.

Risk exposure is also crucial because venture capital firms want every dollar invested to be well spent, which is to ensure a more reasonable opportunity cost in due diligence, portfolio management, and value-added activities. Of course, it is also about valuation. In competitive investments, limited capacity is a hurdle that GPs must balance with maximizing upside (and downside protection).

Since only a portion of crypto VC investors invest through equity, further confusion arises. Investing in native network tokens allows users to experience the value of the network but may not grant them control over the company sponsoring the project or the sale of tokens.

Moreover, these projects generally have a clear intention to create decentralized networks with decentralized ownership, which directly conflicts with any venture capital fund's desire to retain some investment control. The entire issue of crypto network governance is a topic that requires time to discuss and is often related to space venture capital.

Thus, LPs are looking for GPs who can secure allocations in competitive rounds while remaining sensitive to valuations. GPs can leverage personal relationships, participate softly in governance, provide reasonable advice, and become significant and influential investors.

6. Reserves and follow-on investments

Reserves are the portion of the fund set aside for follow-on investments, and how much to reserve is often a hot topic of debate between GPs and LPs. If reserves are ample, the fund is more likely to invest in later rounds (with lower variance); conversely, it means GPs cannot support founders in subsequent rounds of financing or maintain their ownership percentage through financing.

GPs who actively participate in portfolio companies (for example, holding board seats) benefit from a strong information advantage when deciding whether to participate in follow-on rounds. However, this advantage is often overused, to the point where GPs not participating in follow-on investments may be interpreted as a strong negative signal, potentially jeopardizing the founders' chances of raising the next round of financing, which may incentivize GPs to continue investing in projects they would not have chosen otherwise.

Unfortunately, the best investment projects also attract a swarm of competitors, making the right to invest pro-rata very difficult to obtain or secure. Reserves allow GPs to double down on these high-performing companies, but they must manage the risk of adverse selection: allocating incremental follow-on investment funds to the bottom of the portfolio is easier than to the top quartile.

In addition to maintaining investment proportions, reserves are also an important leverage factor for other considerations. In venture capital, if GPs cannot allocate additional funds in subsequent rounds to fulfill pro-rata rights, dilution protection rights, and liquidation preferences, then the negotiated protective measures may lose their value. One fundamental reason for retaining reserves is to ensure that preferred shares do not dilute into common shares.

However, in the crypto space, the story unfolds differently: 1) there are fewer follow-on private investment rounds needed, 2) traditional investor protections in early investment rounds are weaker, and 3) the amount of cumulative funds deployable before high-performing companies realize is low. Therefore, the demand for reserves decreases.

So, should more reserves be retained for follow-on investments in public token markets?

After all, inflation-based crypto networks exhibit dilution dynamics similar to traditional venture capital follow-on financing rounds. While non-crypto venture capital is not expected to experience much additional dilution after realization, the inflation schedule or consensus mechanism of crypto networks typically gradually dilutes early supporters until the network is fully spread out.

Therefore, for future public market purchases, crypto VCs may wish to retain reserves or engage in generalized mining to avoid dilution of shares or earn incremental allocations while fundamentally supporting the entire network.

Traditional venture capital firms may find it difficult to accept this perspective, preferring to retain reserves to double down on investments in crypto networks through public markets.

In theory, public markets offer more turbulent entry opportunities, with fewer information asymmetries, leading to more accurate pricing and liquidity premiums (the time and cost required to realize an investment asset). On the surface, crypto VCs should focus their capital allocation on private markets where they have stronger advantages. In practice, it remains unclear whether this is the case in this emerging industry.

We find little evidence that most GPs in the crypto public markets have conducted thoughtful, rigorous, and disciplined valuation work. In fact, considering the extreme conditions in the public crypto market, these valuations may be even more wildly inaccurate than those in professionally investor-led private market pricing.

A publicly traded token can tell us very little about a specific crypto network's stage, maturity, or risk level unless it has reached or surpassed a mature stage like beta. This investment is likely just an early bet on technology with asymmetric return potential, and it should be viewed as such before it matures, regardless of its realization capability.

Unlike traditional venture capital, follow-on investments in the crypto public market are entirely possible, allowing GPs to set aside their doubts.

Overall, one question LPs will continue to consider is the "correct" reserve level for early crypto venture funds. However, in our discussion, realization capability is hardly a relevant parameter. Instead, due to reduced path dependence on follow-on investments (fund governance, share classes, etc.), current crypto venture funds should require less reserve than traditional venture capital. Additionally, since a relatively large portion of the capital is concentrated in the first investment, seizing the best opportunities early and making higher allocations will be a key driver of portfolio returns.

7. Exit strategy and secondary market

If GPs do not know when or under what conditions to withdraw their investments, and do not understand what kind of returns to expect, then investing is not a wise decision, unless you are Warren Buffett.

For traditional VCs, exit routes through IPOs or acquisitions are generally smooth, but this is not the case in the crypto world: once network tokens can be traded, investors can exit their positions, but there has not been enough experience throughout the crypto market cycle to understand whether this situation will persist, diminish, or be completely replaced by something else.

While traditional VC firms often exit shortly after realization, this may not be the best option in crypto venture capital. Since liquid tokens are a prerequisite for the normal operation of crypto networks, the realization capability of tokens must have emerged early in the project's maturity.

For its true value, the realization capability of tokens appears too early, often surfacing when the underlying company has additional funding needs.

If the investment (for example, in a SAFT) begins to realize, GPs should not feel pressured to sell their positions. At the same time, the assets in the venture portfolio have a realization market, meaning GPs can decide daily whether to miss opportunities or earn additional commissions by choosing to exit or readjust positions.

As projects mature, using the secondary market as an exit route is a contentious topic for GPs and LPs. On one hand, it allows funds to return profits to investors more quickly, improving short-term IRR while reducing portfolio risk; on the other hand, if GPs sell too early, they may face criticism from LPs and founders, jeopardizing their status as long-term partners.

Overall, investing in crypto does require active management of the portfolio in the post-network launch phase, and without entering and exiting investments, GPs need to choose exit points, utilizing available realization sources, especially investments outside of crypto to realize their profits. If done well, crypto VCs can build a flatter J-curve portfolio than traditional venture funds.

8. Investment recovery

Investment recovery refers to the practice of reinvesting profits back into the fund, which can increase the fund's net multiple (TVPI, DPI), but delaying capital recovery may actually lower IRR in the short term. In traditional venture capital, some limited investment recovery is common to compensate for the total cost base, including management fees and fund expenses.

Because crypto investments can realize early, and the volatility after realization is high, if GPs want to regularly manage and rebalance their realized portfolios, they can advocate for higher investment recovery rates. GPs need to consider that the shorter holding periods and the gains and losses from rebalancing the portfolio may have tax implications for LPs and regulatory impacts on the appropriate fund structure.

9. Conclusion

Venture capital and new technologies always go hand in hand. But in the field of crypto, they are in a new position, utilizing the same new technology they invest in.

This introduces a whole new dimension of uncertainty, including the layering of value and changes in exit mechanisms. LPs cannot fully plan exit routes and exit valuations according to their desires, and GPs also need to closely collaborate with the companies they invest in, plan business development trajectories, flexibly respond to variables, and maintain a clear understanding of market and technological directions.

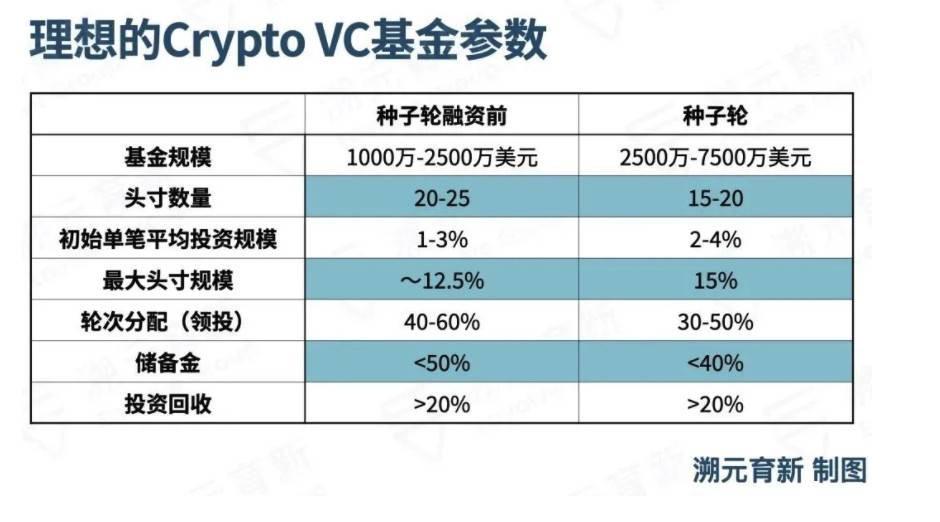

Many parameters of portfolio structure do not have absolute correct answers; LPs need to accept that GPs may deviate from standard industry parameter levels. If hard metrics must be set, our ideal venture capital fund parameters are as follows, but we believe these parameters will continue to evolve in the future.