A Comprehensive Understanding of the Main Players and Operating Mechanisms in the DeFi Insurance Market

Only those who can bear high risks are welcome; otherwise, the development of DeFi will stagnate. Having insurance is key to attracting more users.

Only those who can bear high risks are welcome; otherwise, the development of DeFi will stagnate. Having insurance is key to attracting more users.This article is sourced from CoinGecko, authored by Lucius Fang, and compiled by Alyson.

In the DeFi ecosystem, insurance remains a niche market. However, as the insurance sector matures and institutional participants join, insurance could become one of the biggest pillars of DeFi. Recently, CoinGecko analyst Lucius Fang wrote about the DeFi insurance market, detailing the main players and their operational mechanisms, as well as future market prospects. Chain Catcher translated the original text and made adjustments that do not affect the intent.

With the continuous innovation of DeFi projects, we have seen an increasing number of hacking incidents, with losses becoming more significant. Since the second half of 2019, there have been 21 publicly reported DeFi security incidents, resulting in losses exceeding $165 million.

If this field only welcomes those who can bear high risks, the development of DeFi will stagnate; having insurance is key to attracting more users.

1. The Significance and Mechanism of Insurance

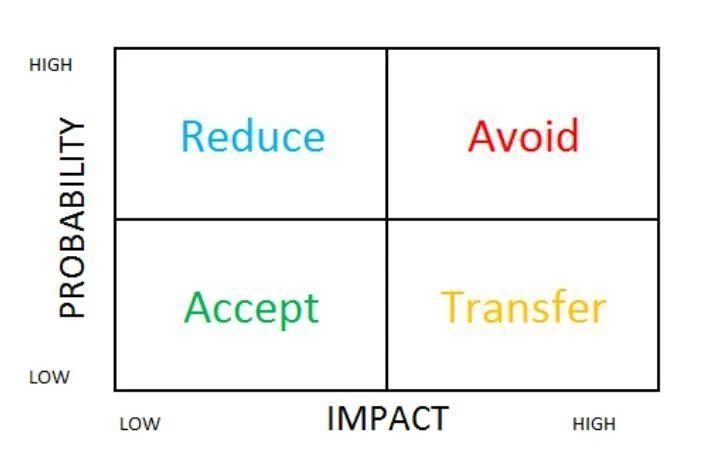

The insurance industry is a massive market, with global insured premiums totaling $6.3 trillion in 2019. The world is complex, and we always face the risk of some kind of incident. Below is a simple risk management framework that illustrates the measures we should take to address different types of risks.

Individuals should transfer out risks that have a high impact but low frequency (such as natural disasters and cancer) and manage these types of risks through insurance.

The operation of insurance is based on two main assumptions:

First, the Law of Large Numbers. The loss events covered by insurance must be of low frequency; if the frequency of events is high enough, the results will converge to the expected value.

Second, the Risk Pooling Mechanism. Loss events are characterized by low frequency and high impact; thus, the premiums paid by a large number of people subsidize the losses of a few large claims.

Essentially, insurance is a tool that pools capital and socializes large losses, preventing participants from going bankrupt due to a catastrophic event.

Insurance socializes the costs of experiencing catastrophic events, allowing individuals to bear risks. It is a risk management tool that encourages more users to participate, and for the DeFi industry, it is crucial to go beyond the existing segmented audience. The DeFi industry needs insurance products to persuade institutional participants with substantial capital to join.

2. Detailed Analysis of Three Major Insurance Projects

Currently, two major insurance projects dominate the DeFi insurance market—Nexus Mutual and Cover Protocol. We will examine how they operate in detail below. We will also delve into the Armor Protocol, as it plays a key role in the development of Nexus Mutual.

Nexus Mutual

Nexus Mutual is the largest insurance project in the crypto market. Its total locked value (TVL) is $288 million, founded by Hugh Karp, former CFO of Munich Re in the UK.

Nexus Mutual is registered in the UK as a mutual company. Unlike shareholder companies, mutual companies are managed by their members, and only members are allowed to transact with the company. Nexus Mutual is similar to a member-operated company that serves its members.

Currently, Nexus Mutual offers two types of insurance:

First, smart contract insurance, primarily aimed at DeFi protocols that hold user funds in custody, as these protocols may suffer hacks due to smart contract errors. The insurance covers major DeFi protocols such as Uniswap, MakerDAO, Aave, Synthetix, and Yearn Finance.

Second, custody insurance, mainly targeting the risk of funds being stolen by hackers or withdrawal being suspended. Nexus Mutual provides coverage for centralized exchanges (such as Binance, Coinbase, Kraken, Gemini) as well as lending companies (such as BlockFi, Nexo, and Celsius).

Users can purchase a total of 72 different insurances covering smart contract protocols, centralized exchanges, lending services, and custody services.

How to Purchase Insurance:

To purchase insurance from Nexus, users must register as members through the KYC process and pay a one-time fee of 0.002 ETH, after which they can use ETH or DAI to buy insurance.

Nexus Mutual converts the payment into NXM tokens, representing rights to mutual capital. 90% of the NXM is burned as coverage costs. 10% of the NXM will remain in the user's wallet. When a claim is submitted, it will serve as a deposit, which will be refunded if there is no claim.

Claim Assessment Mechanism:

Users can submit claims at any time within the guarantee period or up to 35 days after the guarantee period ends. When users submit a claim, they must lock 5% of the premium. Each policy allows users to submit claims up to two times.

Unlike traditional insurance companies, the outcome of claims is decided by member voting. Members have complete discretion over whether a claim is valid. Members can participate as claim assessors using NXM, but must adhere to a 7-day lock-up period.

When member votes align with the overall voting result, 20% of the premium will be shared proportionally with those members. However, if the votes do not match the result, members will not receive any rewards, and the lock-up period will be extended by another 7 days.

To qualify for a claim, users must prove they have lost funds, with smart contract insurance requiring a loss of at least 20% of funds, and custody insurance requiring a loss of at least 10% of funds.

Risk Assessment Mechanism:

The pricing of insurance depends on the amount of capital staked on specific protocols. Users can stake NXM on these protocols to become risk assessors. The pricing formula is as follows:

Risk Cost = 1 - (Amount of Staked NXM / Low Risk Cost Limit)^(1/7)

Underwriting Price = Risk Cost x (1 + Surplus Profit Margin) x Underwriting Period / 365.25 x Underwriting Amount

The low risk cost limit is the minimum staking requirement needed to achieve a minimum pricing of 2%, set at 50,000 NXM. The surplus profit is used to cover costs and create surplus for the mutual fund, with a surplus profit margin set at 30%. Therefore, the minimum insurance cost is 2.6%.

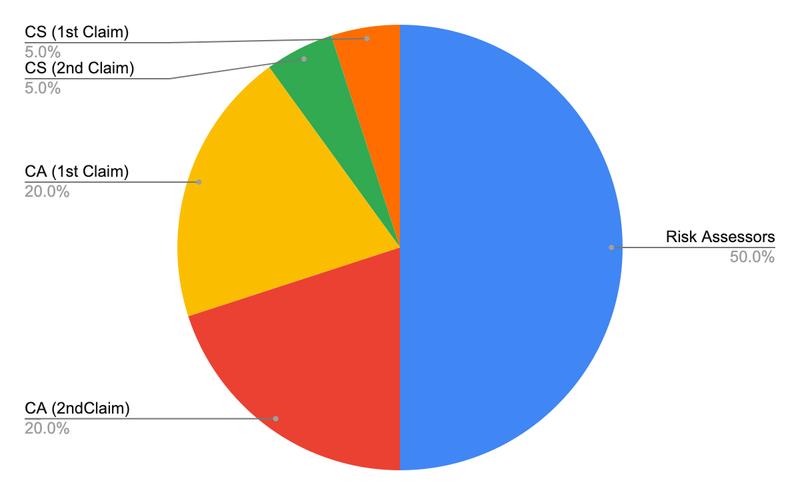

When a claim occurs, the risk assessors bear the loss. To bear this risk, 50% of the insurance premium is shared by the risk assessors.

The following pie chart shows where the premiums flow:

CS: The fee paid by users to submit a claim

CA: The fee received by assessors if a claim is submitted

If users do not submit a claim by the expiration of the policy, 10% of the premium will be refunded to the policyholder, while 40% of the premium will go into the capital pool.

Risk assessors can leverage their capital by 10 times to maximize capital efficiency. For example, if a risk assessor has 100 NXM, they can stake 1000 NXM across multiple protocols, where the maximum stake limit for any single protocol is 100 NXM.

The assumption here is that simultaneous attacks on multiple protocols are rare, and this practice aligns with how the insurance industry operates based on the law of large numbers and risk sharing.

If the claim amount exceeds the funds held by the risk assessors, the capital pool of the mutual fund will cover the remaining amount.

To ensure there is always enough capital to pay claims, the mutual demand from both sides must keep the capital above the Minimum Capital Requirement (MCR). Typically, the MCR is calculated based on the risks of the insurance sold. However, due to a lack of claims data, both sides follow manually determined parameters set by the team.

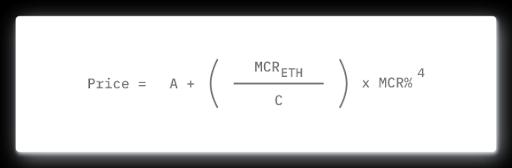

Token Economics:

The NXM token economics is a crucial factor in attracting and retaining capital. It uses a joint curve model to determine the price of NXM. The calculation formula is as follows:

A = 0.01028

C = 5,800,000

MCR (ETH) = Required Minimum Capital

MCR% = Available Capital / MCR (ETH)

MCR% is a key factor in determining the price of NXM, as it appears to the fourth power in the pricing formula. When people purchase NXM based on the joint curve model, the available capital increases, leading to an increase in MCR%, which in turn causes the price of NXM to grow exponentially.

It is important to note that when MCR% is below 100%, the exit of the joint curve model will be halted to ensure there are sufficient funds to pay claims.

wNXM:

Nexus Mutual has released wrapped NXM (wNXM), allowing investors to access NXM without undergoing KYC. Users can wrap NXM into wNXM and then sell it on secondary markets like Uniswap and Binance.

wNXM has many drawbacks; it cannot be used for risk assessment, claim assessment, or governance voting. The launch of the Armor protocol helps address this issue by converting wNXM into arNXM.

Shield Mining:

To encourage more risk assessors to stake their NXM, Nexus Mutual launched the Shield Mining program, which plans to reward staked users with native tokens. Shield Mining has helped increase the amount of staked NXM and the available insurance.

Protocol Revenue:

The NXM token differs from other governance tokens in that its price is controlled by a formula. Therefore, mutual benefit will help increase available capital and raise the price of NXM. There are two sources of profit:

1) Collected premiums - Paid claims - Expenses.

2) The spread when users sell NXM from the bonding curve is 2.5%.

Armor Protocol

To overcome the limitations of KYC, Yearn Finance created yInsure, allowing users to purchase Nexus Mutual insurance without KYC. yInsure was originally managed by Safe Protocol, but the project was canceled due to some internal conflicts between founder Alan and community member Azeem. Alan went on to launch the Cover protocol, while Azeem took over the yInsure product and launched the Armor protocol.

The Armor protocol has four main products: arNXM, arNFT, arCORE, and arSHIELD.

arNXM:

Nexus Mutual created Wrapped NXM (wNXM), allowing investors to invest in NXM without KYC. However, as more wNXM is created, the number of NXM available for internal interaction functions (such as staking, claim assessment, and governance voting) decreases.

Armor created arNXM to solve this issue, allowing investors to participate in the operations of Nexus Mutual without KYC.

To obtain arNXM, users can stake wNXM in Armor. Armor unwraps wNXM and stakes the NXM tokens in Nexus Mutual. By staking in Nexus Mutual, stakers signal that the smart contract is secure, opening up more channels for insurance sales.

Armor will retain a reserve of 10,000 wNXM to ensure there is sufficient liquidity for trading between arNXM and wNXM. Armor replenishes the reserve every ten days.

arNXM can be considered a wNXM liquidity pool, where users can deposit wNXM into the pool, expecting to receive more wNXM in the future.

arNFT:

arNFT is a tokenized form of insurance purchased on Nexus Mutual. arNFT allows users to buy insurance without KYC. Since these insurance targets are tokenized, users can now transfer them to other users or sell them on secondary markets. These tokenized insurances will further explore DeFi composability.

All Nexus Mutual insurances can utilize arNFT.

arCORE:

arCORE is a pay-as-you-go insurance product. Armor tracks the exact amount of user funds through a liquidity payment system, as they can dynamically span different protocols.

The technical foundation of arCORE integrates with arNFT, which are sold at a premium after being decomposed. arCORE allows for more innovative product designs and showcases the composability of the DeFi ecosystem.

arCORE products charge higher insurance premiums to compensate for the risk that arNFT stakers bear for insurance that cannot be fully sold. Currently, the premium multiplier for arCORE is 161.8%, meaning the price will be 61.8% higher than if purchased directly from Nexus Mutual.

For the additional premium, 90% will be returned to arNFT supporters, while 10% will be charged by Armor as a management fee. With a premium multiplier of 1.618 and a 90% revenue share, the utilization rate must exceed 69% for arNFT investors to profit.

If the amount of insurance sold is less than 69% of the staked amount in the pool, those stakers will have to bear the insurance costs themselves.

arSHIELD:

arSHIELD is an insurance repository for liquidity provider (LP) tokens, where the insurance premium is automatically deducted from the LP fees earned. arSHIELD essentially creates LP tokens with insurance, allowing users to avoid upfront payments.

arSHIELD only covers the protocol risks of liquidity pools. For example, insured Uniswap LP tokens only cover the risk of damage to Uniswap's smart contracts, not the risks of the underlying assets (such as the underlying asset protocol being hacked).

arSHIELD is merely a repackaged version of arCORE, with two different risk levels.

The Shield + Vault is the safest version, guaranteeing payouts. It is fully collateralized but has limited underwriting capacity. It has a high multiplier of 200%, making its price twice that of the Shield Vault.

The Shield Vault is the riskier version, where claim payouts may not be fully reimbursed, as it depends on the available funds in the pool during the hack.

To compensate for the additional risk, it has only a 100% premium multiplier, meaning its price is the same as if purchased directly from Nexus Mutual itself. The insurance capacity is designed to be unlimited, making it difficult for users to be satisfied with the collateralization rate, as it may not be fully collateralized.

Claim Mechanism:

After users submit a claim, an audit process will be triggered and submitted to Nexus Mutual for review. Armor token holders will also participate in the claim approval and payment process of Nexus Mutual. If payment is confirmed, the amount will be sent to Armor's payment treasury and then allocated to the affected users.

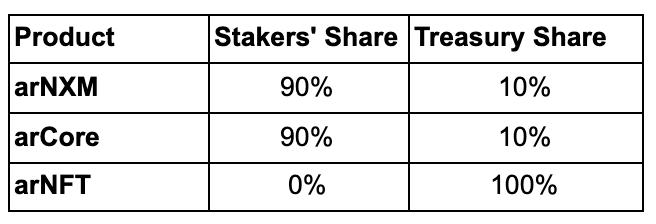

Protocol Revenue:

The following is the profit-sharing fee schedule for the project as of February 2021.

It is important to note that for each insurance purchased from Nexus Mutual, the project retains 10% of the premium for claims, while the claim fee is 5% of the premium. Each user can apply for two claims for the same reason, and if no claims are submitted by the end of the policy term, 10% of the premium will be refunded. This is the source of arNFT's profits.

Cover Protocol

As mentioned earlier, the Cover Protocol was incubated by Yearn Finance, originally providing yInsure through the Safe protocol. In November 2020, Yearn Finance announced a merger with the Cover Protocol to insure its yvaults, but Yearn Finance chose to terminate the partnership on March 5, 2021.

Coverage Categories:

The Cover Protocol only provides smart contract insurance. Let's look at an example of how insurance is sold:

Market makers can deposit 1 DAI, and they will be able to generate 1 NOCLAIM token and 1 CLAIM token. These two tokens only represent the risk of a single protocol. The tokens are only valid for a fixed time frame (e.g., six months). After six months, two scenarios may occur:

If no valid claim event occurs, NOCLAIM token holders can claim 1 DAI, while the CLAIM token's value is zero.

If a valid claim event occurs, CLAIM token holders can claim 1 DAI, while the NOCLAIM token's value is zero.

This is similar to a prediction market, where users bet on whether the protocol will be hacked within a time frame.

The Cover Protocol introduces a partial claim mechanism, so when a valid claim event occurs, the expenditure of CLAIM token holders will be determined by the Claim Validity Committee (CVC).

How to Purchase Insurance:

First, Balancer Swap (old), where users need to trade in Balancer and purchase CLAIM tokens from the Balancer pool.

Second, Flash Swap (new), where users can purchase insurance from the Cover Protocol's webpage with just one Ethereum transaction.

Claim Assessment Mechanism:

First, regular claims, which cost 10 DAI. COVER token holders will first vote on the validity of the claim. It will then move to the Claim Validity Committee (CVC) for a final decision.

Second, forced claims, which cost 500 DAI, and will be sent directly to the CVC for a decision.

The CVC is composed of external smart contract auditors. If the claim is approved, the Cover Protocol will refund the claim application fee.

Risk Assessment Mechanism:

Balancer Swap (old): As mentioned above, the Cover Protocol heavily relies on market makers to expand coverage. After minting NOCLAIM and CLAIM tokens, they will have to provide liquidity for DAI in the Balancer pool. Here are the details:

NOCLAIM / DAI pool ratio is 98% / 2%, with an overdue fee of 3%.

CLAIM / DAI pool ratio is 80% / 20%, with an overdue fee of 5%.

Flash Swap (new): It relies on a single pool, without needing two different pools to guide NOCLAIM and CLAIM tokens.

- NOCLAIM / DAI pool ratio is 50% / 50%, with an overdue fee of 0.2%.

Market makers' income primarily comes from overdue fees generated by the Balancer pool.

The new Flash Swap system has some advantages:

First, insurance costs are expected to decrease because there is only one Balancer pool for yield farming. Under incentives, market makers will purchase more NOCLAIM tokens in exchange for yield farming rewards or trading fees, driving up the price of NOCLAIM tokens. Thus, the price of CLAIM tokens will decrease to CLAIM = 1 - NOCLAIM.

Second, market makers are expected to earn more fees because each time insurance is purchased, the NOCLAIM token must be sold into the Balancer pool. Unlike the old system, market makers only need to provide liquidity for one pool.

Since each purchase involves CLAIM / NOCLAIM tokens, a fee of 0.1% is charged during the redemption process, so the Cover Protocol is expected to generate higher platform revenue.

The price of insurance is determined by the supply and demand of the Balancer pool.

Yield Farming:

The Cover Protocol simultaneously yield farms for both the NOCLAIM / DAI pool and the CLAIM / DAI pool in the old BalancerSwap system. In the new Flash Swap system, only the NOCLAIM / DAI pool is incentivized.

Protocol Revenue:

Exchanging CLAIM and NOCLAIM tokens will incur a fee of 0.1%. COVER token holders have the right to vote on how to use the treasury. There are ongoing discussions about using COVER tokens to generate revenue, but the details have not yet been finalized.

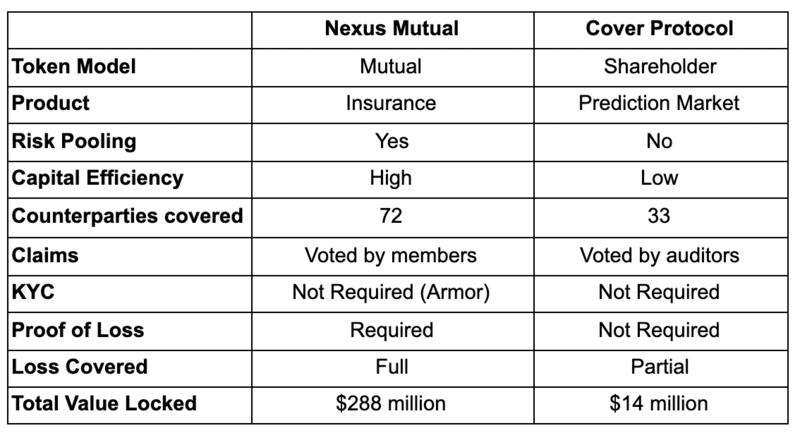

3. Comparison of the Two Major Insurance Projects

Investment Efficiency

Nexus Mutual allows capital providers to leverage their funds by 10 times, resulting in higher premium income for stakeholders. Investors do have to bear more risks, but this approach is more consistent with how traditional insurance diversifies risk across different products.

At the same time, since each pool is isolated, investors in the Cover Protocol cannot leverage their capital. While there are plans to bundle different risks for insurance in the V2 version, very few details have been disclosed so far.

Due to lower capital efficiency, Cover insurance is more expensive than Nexus. For example, purchasing insurance for OriginDollar in the Cover Protocol costs 12.91% annually, while in Nexus Mutual, it is only 2.6%.

We can quantitatively calculate investment efficiency by dividing the effective insurance amount in the capital pool. The capital efficiency of Nexus Mutual can be as high as 200%. In contrast, for the Cover Protocol, it is inherently less than 100%.

Insurance Coverage

The Cover Protocol only covers 22 protocols, while Nexus Mutual covers 74 trading pairs. Nexus Mutual offers greater flexibility in coverage terms, allowing users to decide when to start coverage on any given day, with coverage lasting up to a year.

The Cover Protocol only provides pre-determined term insurance. For a specific series, the insurance period is valid until the end of May, regardless of when the user purchases the insurance; the coverage will end in May. Therefore, over time, the value of CLAIM tokens will trend towards $0, while the value of NOCLAIM tokens will trend towards $1.

Nexus Mutual covers most major DeFi protocols, allowing users to find more comprehensive services. It offers a broader coverage range than the Cover Protocol, which is limited by its total locked value (TVL). Even so, due to a lack of stakers, many Cover insurances have been sold out.

The launch of the Armor protocol has indeed alleviated this issue by attracting more wNXM into arNXM, thereby threatening NXM.

The Cover Protocol can be seen as a competitor for long-tail insurance, as projects can be launched more quickly without cumbersome risk assessments. This is because each risk is isolated and contained within a single pool, unlike in NXM, where claims from any single protocol could erode the capital pool.

However, opening insurance for lesser-known projects is not an easy task. In addition to being limited by capacity, insurance costs are often prohibitively expensive. For example, a newly listed project, Reflexer Finance, has a payment cost of 32.46% annually.

Claim Ratio

Yearn Finance suffered a $11 million hack in February 2021. Although the company ultimately decided to cover the losses through its own fund, insurance has now decided to pay compensation to prove that their products indeed function as expected.

Nexus Mutual has accepted 14 claims, with a total claim amount of $2,410,499 (1351 ETH + 129,660 DAI). This resulted in a 9.57% loss for users who staked NXM with Yearn Finance.

If claimants can prove they have indeed lost at least 20% of their funds, they can be fully compensated for their losses.

Meanwhile, the Cover Protocol decided to set the payout ratio at only 36%, as the losses accounted for just 36% of the affected vaults. If users hold 1000 CLAIM tokens, they can only receive $360.

Yearn Finance holds CLAIM tokens worth $409,000. In reality, market makers only lost $147,000. Insurance buyers should be aware that purchasing insurance from the Cover Protocol does not guarantee full compensation, as its method of determining claim amounts is more akin to a prediction market.

Summary

Nexus Mutual currently leads the insurance market by a wide margin, seemingly without competitors. However, its penetration in DeFi is very low, accounting for only 2% of the total DeFi TVL.

Competitors have ample room to catch up. In a field where innovations emerge daily, the throne of the insurance king is always within reach.

The Cover Protocol has been rapidly innovating, even during the entire security protocol debacle. Although the product has not yet gained widespread attention, achieving 0 to 1 innovation has never been easy. We must remember that the Cover Protocol has been launched for less than a year. It is still too early to determine which is superior.

4. Other Upcoming Insurance Protocols

Unslashed Finance

Currently in testing mode. Unslashed Finance offers investors a bucket-style risk-sharing model. The first product is called Spartan Bucket, covering 24 different risks, including custodians, wallets, exchanges, smart contracts, and oracles.

Lido Finance purchased $200 million worth of insurance from Unslashed Finance for its stETH (ETH 2.0 stake) to mitigate the risk of receiving severe penalties. Penalties refer to the punishments imposed on proof-of-stake (PoS) network validators when they fail to maintain the network continuously.

Nsure

Nsure completed a $1.4 million seed round of financing back in September 2020, with funding from Mechanism Capital, Caballeros Capital, 3Commas, AU21, SignalVentures, and Genblock. Currently, Nsure has been deployed on the Kovan testnet of Ethereum.

Nsure is a risk trading market. It relies on the NSURE token's stake to represent the protocol's risk and uses it for pricing. They are running an underwriting program in the testnet to test how pricing will work in the mainnet, with participants receiving NSURE tokens as rewards.

They have also proposed a risk rating scale that rates each project based on multiple criteria, including team and history, exposure, code quality, developer community, etc. Besides the staking portion, the risk rating will affect the final policy price.

InsurAce

InsurAce recently raised $3 million, with investors including Alameda Research, DeFiance Capital, ParaFi Capital, Maple Leaf Capital, etc., but has not yet announced its launch date.

InsurAce aims to become the first portfolio-based insurance protocol, offering investment and insurance products to enhance capital efficiency. Unlike current insurance products, where users must purchase multiple insurances when interacting with different protocols during yield farming, InsurAce provides a portfolio-based insurance that covers all protocols involved in the aforementioned investment strategies.

The project claims to use an actuarial-based pricing model rather than relying on collateral or the market to price insurance. Given the lack of claims history in the DeFi ecosystem, whether they can propose a reliable model is questionable.

Other insurance protocols include InsureDAO and Insured Finance.

Some derivative protocols also offer interesting insurance products, such as:

Hakka Finance's 3F Mutual --- covers the fixed exchange rate risk of DAI.

Opium Finance - covers the fixed exchange rate risk of USDT.

So far, the adoption of these insurance products provided by derivative protocols has been lackluster.

Unlike other types of projects like DEXs and lending, insurance projects receive less attention. Besides being a more capital-intensive business, the awareness of purchasing insurance in the crypto space is still not as prevalent. As more insurance protocols are launched this year, we may see more users utilizing insurance.

5. Conclusion

First, insurance only covers about 2% of the total locked value (TVL) in DeFi and has not been widely adopted.

Derivatives such as credit default swaps (CDS) and options may reduce the demand for purchasing insurance. However, building these products typically requires more capital compared to the risk-sharing of insurance, leading to higher premiums. Additionally, derivatives are inherently more expensive due to their greater price risk.

High-risk users and retail users are likely to dominate the current DeFi market. They may not prioritize risk management and thus do not consider purchasing insurance. When the time is right, the insurance market will gain greater momentum and have more collaboration with institutional capital.

Second, despite rapid business growth, the price of NXM has stagnated. Nexus Mutual's core business is operating well, with the effective policy amount growing from $68 million at the beginning of the year to $730 million in February, showing steady growth. This tenfold increase is impressive, yet the price of NXM has remained stagnant.

As investors withdraw from Nexus Mutual, the MCR% has reached the 100% lower limit. Investors now have more options in the synthetic Ethereum stack. NXM is now competing with ETH 2.0 staking providers (Lido's stETH, Ankr's AETH), Alpha Homora's ibETH, and Curve's ETH pools.

Last year, hackers stole $8 million worth of NXM tokens from Nexus Mutual founder Hugh Karp and dumped NXM through the wNXM market, causing a significant drop in the price of wNXM.

Since the MCR% has reached the 100% lower limit, NXM holders cannot sell NXM through the joint curve model. The only way for holders to exit their positions is to sell through wNXM, creating a price gap between wNXM and NXM.

As long as the price gap exists, the best way to acquire NXM is to buy cheap wNXM. Therefore, capital will only flow into the mutual market before the price gap narrows. According to the formula, the price of NXM will remain suppressed until new funds flow in.

Nexus Mutual has proposed several plans to address this issue: creating a community fund to incentivize community members to participate more; exploring ways to invest idle capital pools, such as ETH 2.0 staking; and expanding the product range through the introduction of stacked risk insurance, stablecoin de-pegging insurance, and oracle insurance.

Third, the launch of the Armor protocol has brought significant advantages to Nexus Mutual, solidifying its leading position in the DeFi insurance market. As a wNXM liquidity pool, arNXM intends to replace wNXM. It has attracted so much wNXM that arNXM now contributes 47% of the total NXM, facilitating more insurance purchases.

The current total effective collateral of arNFT is approximately $491 million, while Nexus Mutual's effective collateral totals $700 million. arNFTs contribute about 70% of the effective coverage.

The Armor protocol was only launched two months ago and has already made significant contributions to the development of Nexus Mutual.

Fourth, the Cover Protocol's speed of innovation is rapid, but its business growth is not satisfactory. The Cover Protocol offers fewer product types and has limited flexibility in insurance terms. However, it allows projects to go to market faster and can be purchased with relatively less capital. Therefore, some projects can only use the Cover Protocol and not Nexus Mutual.

The premium costs of the Cover Protocol are much more expensive, but due to high yield farming returns, it is still worth purchasing. People can also bet on which protocol might be hacked, similar to a prediction market. This does not apply to Nexus Mutual, as they require proof of loss.

Recently, the Cover Protocol launched a credit default swap (CDS) product in conjunction with the Ruler Protocol. It is worth noting that the teams behind the Ruler Protocol and the Cover Protocol are the same, and releasing another token with the same developers may not be a good sign.

Yearn Finance has decided to terminate its partnership with the Cover Protocol. Without the intrinsic demand for yVaults, the Cover Protocol may find it challenging to surpass Nexus Mutual.

Note: The content of this article does not constitute any investment advice.