USV: Fat Protocol and Thin Application

The shared open-source data layer with a reward mechanism prevents a "winner-takes-all" market, changes the rules of the game at the application layer, and creates a series of companies that are completely different from the business models at the protocol layer.

The shared open-source data layer with a reward mechanism prevents a "winner-takes-all" market, changes the rules of the game at the application layer, and creates a series of companies that are completely different from the business models at the protocol layer.This article was published on Ethereum Enthusiasts, authored by USV, and compiled by Nina and Elisa.

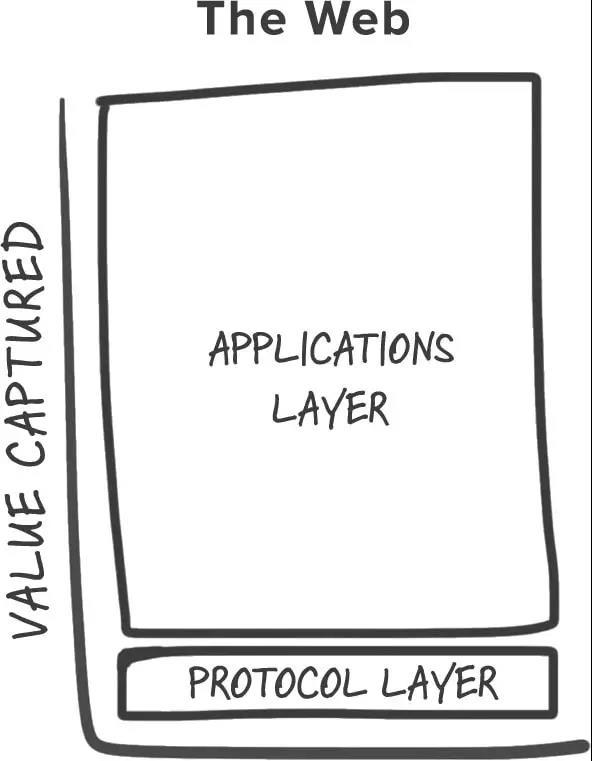

Here is a way to think about the differences between the internet and blockchain. The previous generation of shared protocols (TCP/IP, HTTP, SMTP, etc.) generated immeasurable value, but most of it was captured and re-aggregated at the application layer, in the form of data (think of Google, Facebook, etc.). In terms of value distribution, the internet technology stack consists of "thin" protocols and "fat" applications. As the market has developed, we have concluded that investing in applications yields higher returns, while direct investments in protocols and other technologies have low returns.

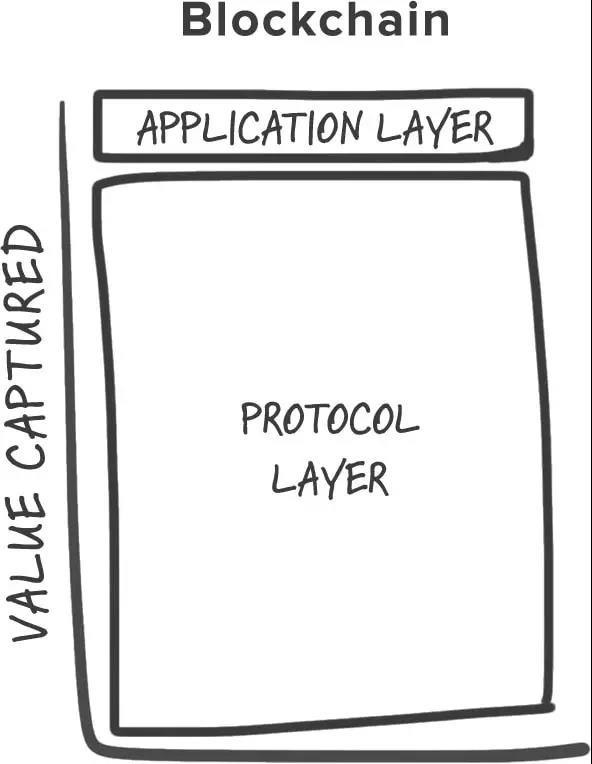

In the blockchain technology stack, the relationship between protocols and applications is reversed: value is concentrated at the shared protocol layer, with only a small portion of value distributed at the application layer. Thus, it is a technology stack of "fat" protocols and "thin" applications.

We see this in the two main blockchain networks, Bitcoin and Ethereum. The Bitcoin network has a market capitalization of about $10 billion (note: the market cap at the time of the article's publication, the same applies to Ethereum's valuation), while the top companies built on its network can reach only a few hundred million dollars, and most may be overvalued due to "business fundamentals" standards. Similarly, just one year after Ethereum's public release, before any truly groundbreaking applications emerged, its valuation reached $1 billion.

For most blockchain-based protocols, two factors lead to this outcome: the first is the shared data layer, and the second is the introduction of theoretically valuable cryptographic "access" tokens.

About a year ago, I wrote an article about the shared data layer. Although this article was shelved for a long time, its main point remains unchanged: by replicating and storing user data through open-source and decentralized networks, rather than having independent applications accessing different information silos, we lower the barriers to entry for new participants and create an ecosystem: the products and services above will be more vibrant and competitive. For example, think about how easy it is to switch from Poloniex to GDAX, or any of its dozens of cryptocurrency trades, and vice versa, because they have equal and free access to the underlying data and blockchain transactions. On the same open-source protocol, several competing, non-cooperative, but interoperable services can be built. This forces the market to find ways to reduce costs, create better products, or come up with better methods.

But merely having an open-source network and a shared data layer is not enough to motivate widespread adoption of blockchain. The second factor, the protocol tokens used to access network services (Bitcoin transactions, Ethereum's computing power, Sia and Storj's storage)【1】 addresses this issue.

At Union Square Ventures (USV), we have had many discussions about investments based on blockchain networks, after which Albert and Fred wrote the following article. Albert views protocol tokens from the perspective of incentivizing open-source protocol innovation: they can serve as research and development funds (through crowdfunding), create value for shareholders (by increasing token value), or both.

Albert's article will help you understand how tokens incentivize protocol development. Here, I will focus on the incentive schemes of tokens and how they affect value distribution (which I call the token feedback loop).

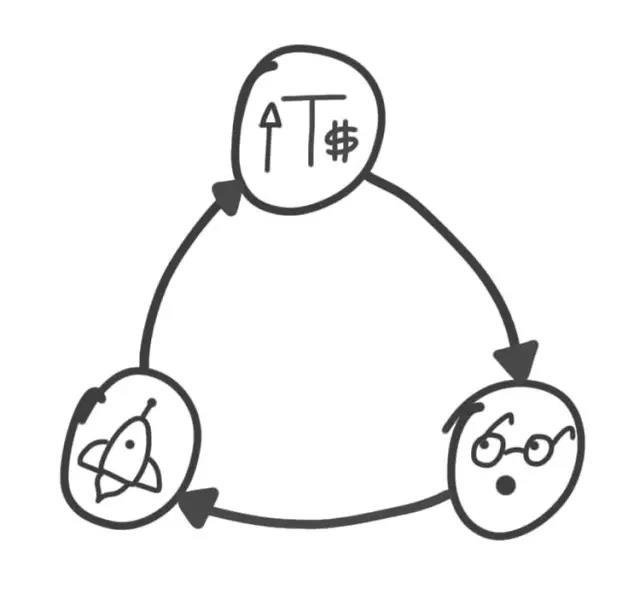

When tokens appreciate, they attract the attention of early speculators, developers, and entrepreneurs. They become stakeholders in the protocol and economically support its success. Then, some holders who gain early benefits will create applications and services around the protocol, believing that the protocol's success will further enhance the value of the tokens they hold. Some applications will become very successful, attracting more new users, perhaps venture capital or other types of investors. This further increases the value of the tokens, thereby attracting the attention of entrepreneurs, leading to more applications, and so on.

Regarding this feedback network, I need to point out two things. First, how much of the initial growth is driven by speculation. Since most tokens are defined as scarce in the program, as the protocol's profits grow, the price of each token and the market value of this network also increase. When profits grow faster than token supply, bubbles can form.

Aside from deliberately fraudulent projects, this is actually a good thing; speculation is often the engine of technology adoption【2】. The two aspects of irrational speculation—booms and busts—are very beneficial for technological innovation. Booms attract capital through early profits, some of which are reinvested in innovation (how much of Ethereum's funding comes from Bitcoin investors' profits, how much of the DAO funding comes from Ethereum investors' profits?), which can actually support the long-term use of new technologies. As prices fall and capital flows out, stakeholders hope to make it whole by promoting and creating value (look at how many Bitcoin companies today are from early users after the 2013 crash).

The second point worth noting is what happens at the end of the cycle. When applications begin to emerge and show early signs of success (whether measured by increased usage or by the attention of financial investors (resources)), two things will happen in a protocol token market: new users will be attracted to the protocol, increasing demand for the tokens (since you need them to access services—see Albert's analogy to tickets used at exhibitions), and existing investors, expecting price increases, will continue to hold the tokens, further restricting supply. This combination will drive the tokens up (assuming new token production is insufficient), and the new market value of the protocol will attract new entrepreneurs and investors, repeating the cycle.

The significance of this dynamic process is its impact on value distribution in the technology stack: since the success of the application layer drives speculation at the protocol layer, the market value of the protocol always grows faster than the total value of all applications built on top of it. The growth value at the protocol layer again attracts and stimulates competition at the application layer. The shared data layer significantly lowers the barriers to entry for applications, resulting in a vibrant and competitive application ecosystem that distributes substantial value to a wide range of stakeholders. This is how tokenized protocols become "fat," while their applications become "thin."

This is a huge change. The shared open-source data layer with reward mechanisms prevents a "winner-takes-all" market, changing the rules of the game at the application layer and creating a series of companies with business models that are completely different from the protocol layer. Many existing rules about starting businesses and investing in innovation do not apply to this new model, so today we have more questions than answers. But we will quickly understand the ins and outs of this market through blockchain research and continue to share our insights following the practices of Union Square Ventures.

Notes:

【1】Also known as application currencies, monetization—double entendre—Naval wrote about this in 2014.

【2】Edward Chancellor wrote a complete and interesting history of financial speculation and its social status (you will be surprised at how similar today's cryptocurrency speculation is to previous financial booms!), Carlota Perez describes the important role of capital bubbles in attracting financial funding for new technology research and development.