The DeFi asset management sector is gaining popularity; what are the potential and constraints of Melon?

The revamped Melon has the potential to grow alongside the DeFi market, but it still depends on the market's demand for active asset management.

The revamped Melon has the potential to grow alongside the DeFi market, but it still depends on the market's demand for active asset management.This article was published on August 26, 2020, by ChainNews, authored by Messari research analyst Jack Purdy.

As one of the first projects to raise funds through token sales, Melon predates the emergence of decentralized finance (DeFi) in the cryptocurrency lexicon by several years, aiming to restructure the core components of the financial system. Although Melon developed a viable product and led the trend of decentralized governance, its native token MLN has seen a brutal bear market, resulting in a 99% loss in value.

Now that DeFi is thriving, the bull market for asset management platforms has become clearer, with Melon experiencing a growth rate of up to 1600% over the past year. Nevertheless, its current market capitalization of $60 million is still significantly smaller than many other top DeFi projects. One major reason for the low valuation is that its economic design does not allow MLN to accumulate substantial value in its current state. This situation began to change only after several community members proposed an improvement suggestion, MIP7, which outlined a method to better link platform growth with MLN value accumulation.

- Current Economic Design of Melon

Before discussing MIP7, it is helpful to understand Melon's current operational mechanism. Melon allows potential fund managers to launch an investment tool based on a specific set of parameters without facing the numerous barriers encountered in traditional fund launches, such as heavy administrative costs, legal obstacles, and operational burdens.

On the other hand, investors can evaluate funds based on transparent on-chain reports and allocate funds to any funds that meet their preferences. Fund managers establish funds, investors request investments, and third parties approve investment requests, all of which require burning the network token MLN to execute. These can be viewed as the system's cash flow, meaning MLN holders will be compensated based on the number of funds created and the amount invested, with the former accounting for the vast majority of fees. Currently, there are 375 funds, generating approximately $23,000.

At the current price of 1.75 MLN required to create each fund (approximately $87, as the cost to create each fund has decreased from 8.75 MLN to 1.75 MLN following a recent price increase), it is challenging to support a market capitalization significantly larger than the current level, even if thousands of funds are created annually. The current token economics of MLN also make it difficult to predict the MLN burn rate, as the speed of fund creation varies greatly over different capping times.

- Entering the MIP7 Era

The MIP7 proposal put forth by Melon community members aims to alleviate these issues by introducing a new fee structure that does not charge a fee for creating each fund but instead charges an annual fee of 20 basis points on the total assets under management (AUM) of Melon funds. Therefore, if some funds succeed and attract substantial investments, the protocol can monetize them more effectively.

Similarly, since AUM is easier to model than fund creation, MLN holders can better predict the MLN burn rate. MIP7 also proposed withdrawal fees and fee discounts for MLN staking, but it faced resistance from the community and is unlikely to be implemented.

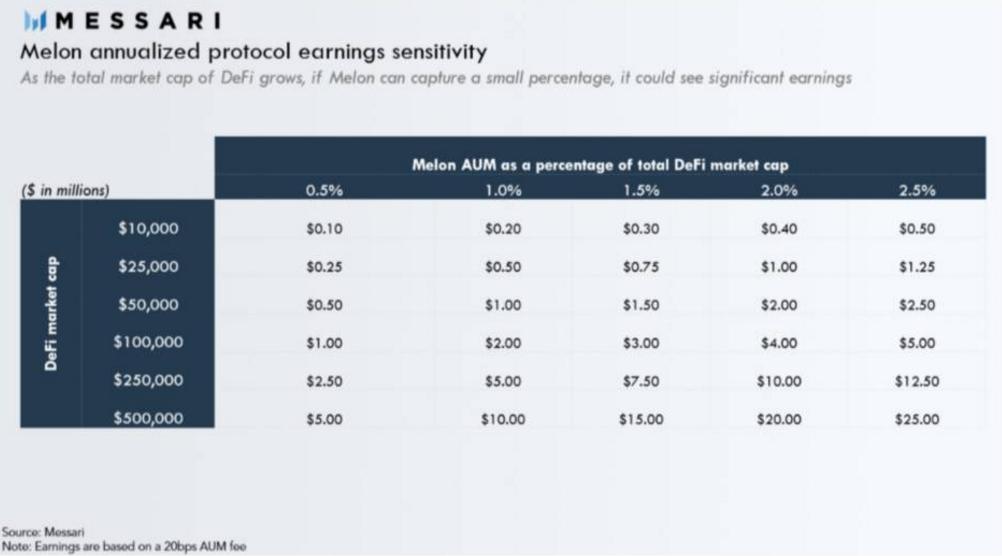

Focusing on AUM fees allows for potential revenue assessments through various assumptions regarding the growth scale of DeFi and the proportion of Melon funds held. I use the market capitalization of DeFi to estimate, rather than the entire cryptocurrency market capitalization, as the growth of Bitcoin or other Layer 1 assets has not significantly expanded Melon's investable universe.

This is a conservative assumption, as there are already packaged versions of BTC and ETH on the market, holding the largest share. However, I believe Melon's success depends on the growth of other investable assets, as most BTC investments will continue to remain off-chain, while the unique opportunities we see in the DeFi space will remain on-chain.

Currently, the total market capitalization of DeFi assets is approximately $6 billion, while Melon's share is only $2.2 million. However, I anticipate that the overall market size will increase significantly in the future, and the demand for asset management will naturally rise. Let's take a look at how changes in these two variables could affect Melon's potential profitability.

Melon's annualized protocol profit sensitivity: As the total market capitalization of DeFi grows, if Melon can capture a small proportion, it may see substantial returns.

Based on the actual growth scale of DeFi, we can derive profit results ranging from less than $1 million to $25 million using the proposed 20 basis points annual fee as a coefficient. By estimating revenues and applying multiples from other asset management protocols, we can derive Melon's total network value.

For the composite coefficient, I used the coefficient from yearn.finance, which offers various yield-generating strategies through its vault products, and I also adopted the coefficient from Balancer, which provides ETF-like automated balancing products through automated market maker (AMM) liquidity pools. Using a range of yield figures from $1 to $10 million, along with the price-to-earnings ratios of YFI and BAL (20x and 56x), we can arrive at many different outcomes, ranging from a market capitalization below Melon's current $65 million level to an appreciation of over 750%.

At this stage, predicting future profits is at best wishful thinking, but providing scenario analyses helps assess the network value under various circumstances. To evaluate the likelihood of any scenario, it is essential to study the favorable factors that could drive revenue growth. As mentioned in their latest community meeting, the team is pushing for a release in the fourth quarter that covers multiple improvements, including the addition of decentralized exchange (DEX) aggregators, OTC trading, simplified fund creation, and fund migration.

However, more importantly, Melon version 2 (v2) will support the integration of other DeFi protocols. This means that fund managers can not only buy and sell assets but also lend out native governance tokens and engage in yield farming. Most of the funds in DeFi projects are currently used for yield farming, so this additional functionality will attract investors looking to enhance their yields. Furthermore, the range of assets will be further expanded, allowing fund managers to invest in DeFi assets that have emerged in recent months, which will further attract investors interested in these high-growth assets.

Yet, even with all these new improvements, whether Melon can grow to such profit levels will largely depend on the demand for active management in this space. Although Melon allows for automated strategies, it has not gained significant traction. This niche market is served by automated strategies, such as Yearn's Vault and Set Protocol, which are several orders of magnitude larger than Melon. These strategies optimize certain parameters using on-chain data and execute them automatically, so users do not have to trade actively all the time, saving on gas fees.

Active management funds, such as those we see on Melon, differ in that they do not follow an existing set of rules but allow fund managers to trade based on their judgment. Ultimately, their success will depend on these managers' ability to capture alpha returns. In the traditional fund market, fund managers oversee $43 trillion in assets.