Dragonfly Partners: Exploring the Evolution Blueprint and Ultimate Form of Stablecoins

The "Stability Act" is a harbinger of future outcomes, and decentralized crypto dollars will become the currency of the crypto world in the future.

The "Stability Act" is a harbinger of future outcomes, and decentralized crypto dollars will become the currency of the crypto world in the future.Written by: Haseeb Qureshi, Managing Partner at Dragonfly Capital Translated by: Perry Wang

The recently proposed STABLE Act in the U.S. Congress has sparked considerable debate in the crypto industry, as the bill requires stablecoin issuers to obtain a banking license.

If the bill is passed into law, it will force stablecoin reserves to be regulated like bank deposits. Given that stablecoins have become the de facto currency of today's crypto ecosystem, this would be a significant setback for stablecoins if this scenario comes to pass.

The crypto industry has responded swiftly and angrily. Exchanges, wallet providers, and entrepreneurs have strongly condemned the bill and its potential consequences.

Currently, the sword of Damocles has not yet fallen, as the STABLE Act may not pass Congress into legislation. However, the U.S. President's Working Group on Financial Markets has just released a regulatory statement regarding stablecoins, indicating that stablecoin holders should undergo Know Your Customer (KYC) verification.

This statement does not have the force of law, but it shows that the spirit of the times has changed.

In the past few years, stablecoins have experienced massive growth, largely unimpeded by regulations. Is this situation sustainable? Does the STABLE Act foreshadow what is to come? What changes will occur for Tether's USDT or decentralized stablecoins?

I believe the answer is simple: regulation is a one-way street. Centralized stablecoins will gradually face increasing restrictions, pushing the crypto economy toward decentralized stablecoins.

This will not happen overnight. But I believe it will ultimately come to pass.

Let’s first review stablecoins and then present my views to the readers one by one.

1. The Origin of Cryptocurrency

Initially, Satoshi Nakamoto invented Bitcoin, creating a decentralized digital currency. In the early days, Bitcoin (BTC) was indeed the "decentralized digital currency."

Before 2018, BTC was the pricing asset for cryptocurrencies. If you wanted to purchase goods with cryptocurrency, you could use BTC; no other cryptocurrency had the global reach or liquidity that BTC did, making it the reserve currency for almost all crypto transactions. Most ICO fundraising was also conducted through BTC and ETH.

However, BTC is not a completely ideal currency. It is known for its high volatility, and with a block generation interval of up to 10 minutes and confirmation times of up to an hour, it cannot serve as an ideal medium of exchange.

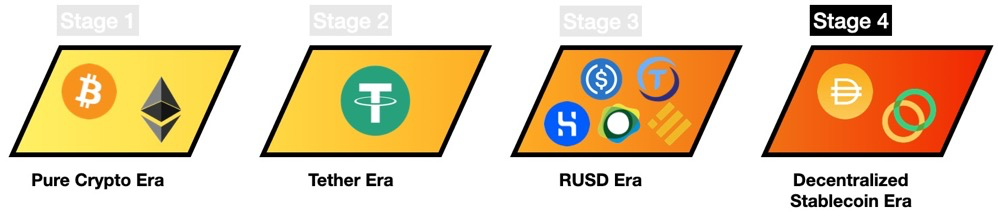

Thus, after the ICO bubble burst in 2018, we entered the second phase of cryptocurrency: the era of Tether's USDT stablecoin. This is the phase we are currently experiencing.

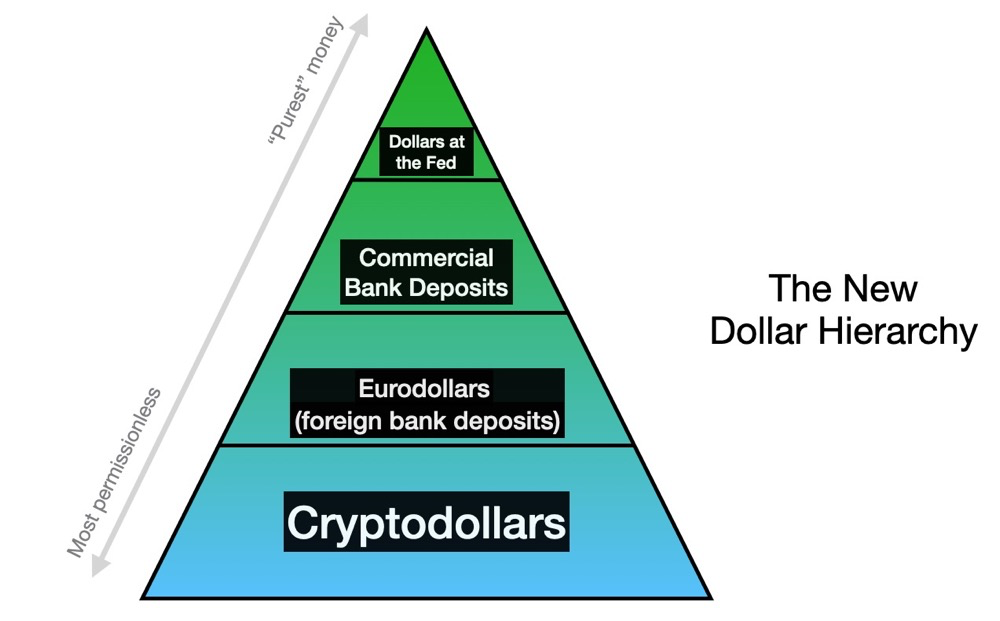

USDT is a stablecoin: a "permissionless" programmable digital dollar. The most common stablecoins are fiat-collateralized stablecoins, essentially equivalent to an IOU for the dollars held in a bank account. Technically, each USDT is an IOU issued by Tether Limited, giving you the right to claim their dollar deposits held at Deltec Bank in the Bahamas.

I prefer not to call it a stablecoin, but rather to describe USDT as a crypto dollar. The term "crypto dollar" clearly indicates that this will fundamentally be a new monetary phenomenon.

You can think of the crypto dollar as a new tier in the monetary system—dollars as abstract monetary assets, converted into permissionless ERC-20 tokens with no political authority, effectively decoupled from the U.S. banking system.

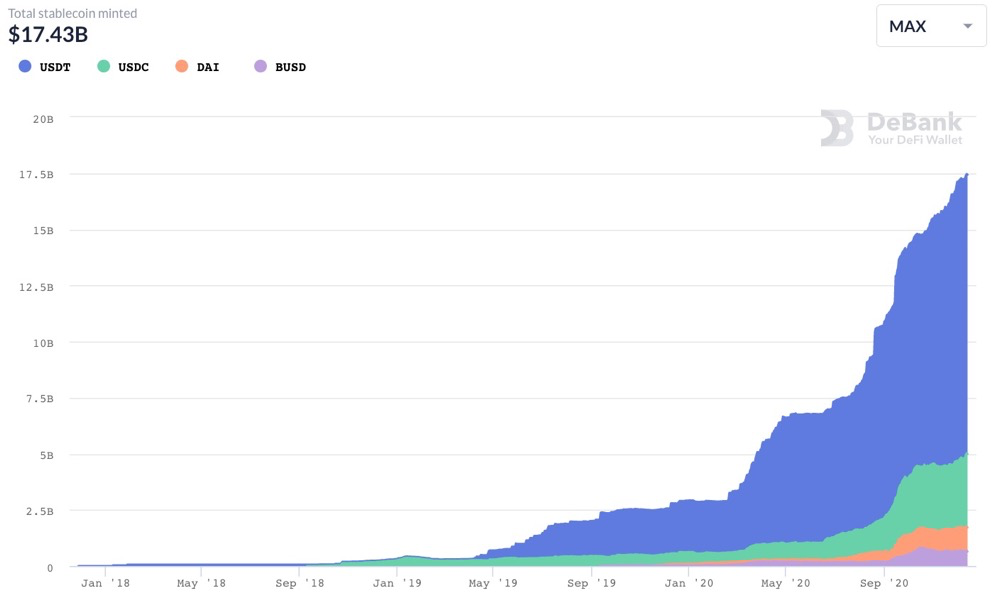

USDT is not the only crypto stablecoin. However, to date, it has achieved an astonishing growth rate, making it the leading stablecoin by market share.

Stablecoins provided by issuers, source: Debank

However, USDT has a highly controversial history and is currently under investigation by the U.S. Department of Justice, the Commodity Futures Trading Commission (CFTC), and the New York Attorney General's office.

In 2019, Tether admitted that the supply of USDT was not 100% backed by dollars, but over time, its supply has only monotonically increased. Given this, you might wonder why Tether's USDT is favored over USDC, which is regulated and backed by Circle and Coinbase.

The answer is simple: USDT is the world's leading stablecoin because it was the first stablecoin to enter this market. It has been around for so long that it has become the most liquid, in-demand, and trusted neutral stablecoin in the world. (In Asia, Tether's ambiguous regulatory status is a plus compared to the more strictly regulated USDC.)

Most cryptocurrency exchanges quote trading pairs in USDT. The trading volume of USDT exceeds that of BTC itself. It can be said that USDT is now the reserve currency of the cryptocurrency realm.

2. How Long Can USDT's Dominance Last?

USDT's market share is growing rapidly. As it gains more attention, I expect that more and more people around the world will realize that cryptocurrency is a better way to access open dollar liquidity from anywhere in the world. Cryptocurrency is truly global digital cash. This makes it extremely attractive internationally, especially in countries with strict currency controls.

For example, in China, the law allows each citizen to have a foreign exchange quota of only $50,000 per year. Most BRICS countries face similar policies (not to mention countries like Argentina, Iran, or Lebanon that are experiencing severe inflation).

Regardless of the country/region involved, most cross-border transactions are conducted in dollars. The dollar is, more or less, the de facto universal currency for international business. This grants the U.S. government tremendous privileges, allowing it to execute its foreign policy not only through military power but also through its control over the global financial infrastructure.

However, countries are increasingly dissatisfied with America's powerful financial hegemony. Today, the use of USDT is growing, especially in cross-border trade, particularly in the Sino-Russian border regions. This allows businesses to enjoy the economic stability and neutrality of the dollar while decoupling from U.S. sanctions.

After the outbreak of COVID-19, the emerging global middle class may increasingly seek currency security and diversification. For many, permissionless cryptocurrencies will become their entry ramp.

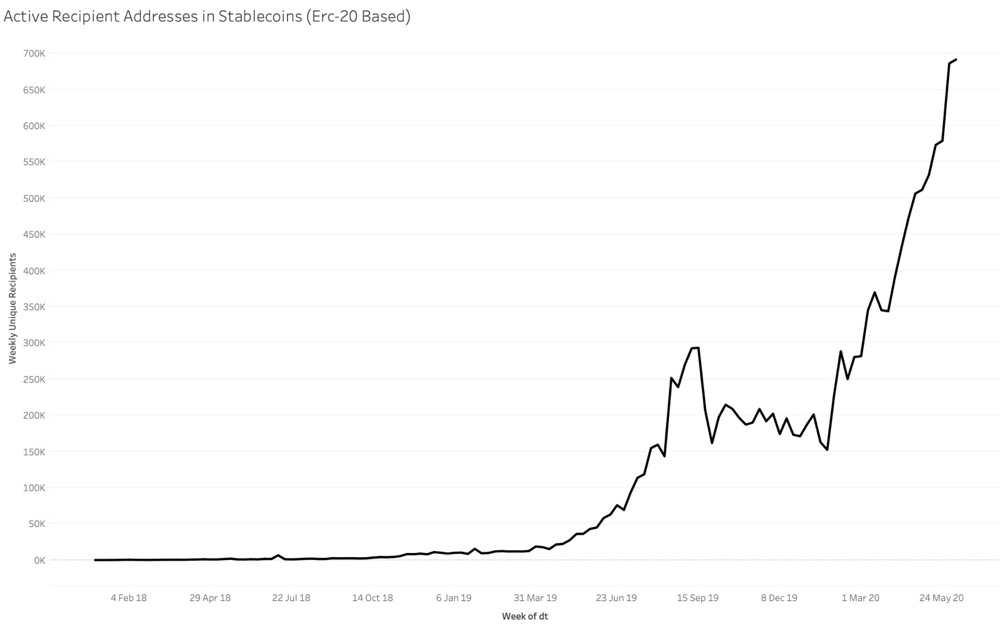

Growth of active Ethereum stablecoin recipient addresses (mainly USDT), source: Joel John

The future of cryptocurrency is bright. But can USDT survive long enough to see that bright future?

This is a serious question at the core of the crypto industry.

3. Free Reserve Currency

USDT is essentially a free reserve currency.

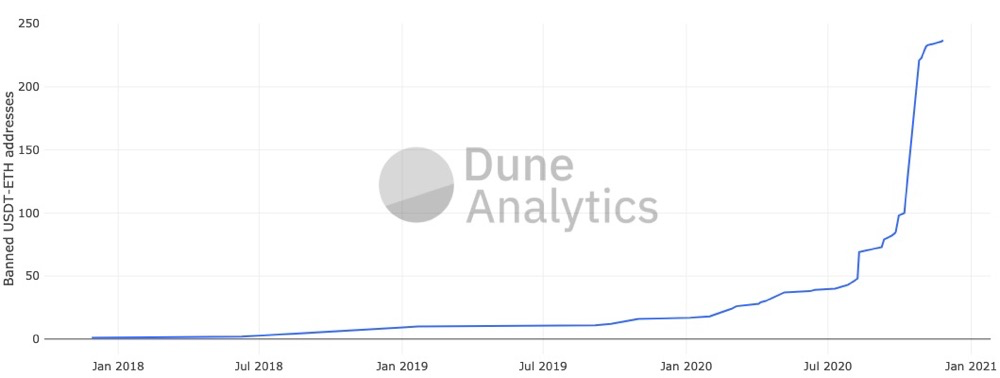

Recall that USDT is currently under investigation by multiple U.S. agencies and prosecutors, and so far, there has been almost no strong defense evidence. It has never undergone a comprehensive audit of its reserves. Tether does conduct KYC verification for its entry and exit ramps, but this extremely weak compliance facade is unlikely to allow them to escape U.S. government regulation. Note that Tether has blacklisted 250 addresses among its millions of token holders.

Everyone knows this situation is unsustainable. The larger the USDT market, the bigger the target.

Number of Tether addresses banned over time (less than 0.1% of total addresses), source: Dune Analytics

Of course, Tether is well aware of this. They are currently playing a cat-and-mouse game with banks, jumping from one bank to another (Wells Fargo, ING, Noble Bank, Deltec) until they find a bank willing to accept their funds.

This will not last forever: eventually, Tether will be shut down or regulated out of existence.

Indeed, the day Tether shuts down will trigger catastrophic consequences.

The crypto market will be raided, exchanges will be thrown into chaos, and millions of crypto traders may have their assets frozen, leading to price crashes everywhere. (This would once again declare Bitcoin dead.)

But as always, cryptocurrencies will eventually rise from the ashes. When the dust settles, we will enter the third phase of cryptocurrency.

Order books will be rebuilt around new cryptocurrencies. The international cryptocurrency market will soon recognize this new standard and be eager to resume operations.

But which crypto dollar will replace Tether's USDT?

4. The Rise of RUSD

Currently, competing with Tether's USDT are regulated stablecoins such as USDC, BUSD, and TUSD (soon to be joined by Facebook's crypto project Libra, also known as Diem). We need not concern ourselves with which stablecoin will win this battle; for now, we can refer to the winner as "RUSD," or regulated U.S. dollars.

RUSD will have the same intuitive functionality as USDT, but will be more compliant and trustworthy. Over time, RUSD will replace USDT's role in the international market, meeting the demand for permissionless, non-political dollars.

Will this be the final stage? The ultimate form of the dollar in the world?

I don't think so. In my view, the third phase, the RUSD era, will also eventually end.

5. The Curse of Digital Cash

Currently, fiat-backed stablecoins are effectively viewed as cash. Anyone, anywhere can pay any amount to anyone they wish. Only when these tokens are redeemed for their underlying dollars do they reach a legitimate checkpoint. Before that, there is no meaningful legal oversight in their circulation.

Imagine a scenario where these stablecoins are sanctioned and prohibited from being legally considered cash. As JP Koning pointed out, don't all banks start adopting them? Stablecoins would effectively allow you to bypass the U.S. Bank Secrecy Act. In this version of the world, anyone could freely transfer $50 million immediately to anyone else in the world without asking any questions, and no party's identity could be determined afterward.

If this situation persists, stablecoins will become the most powerful bank hack in history. Once bank deposits become targets of financial regulation, they will pale in comparison to digital cash. If this is recognized by regulators, it will only be a matter of time before stablecoins consume a large portion of global dollar settlements.

I'm not saying this is impossible! But I have serious doubts about it.

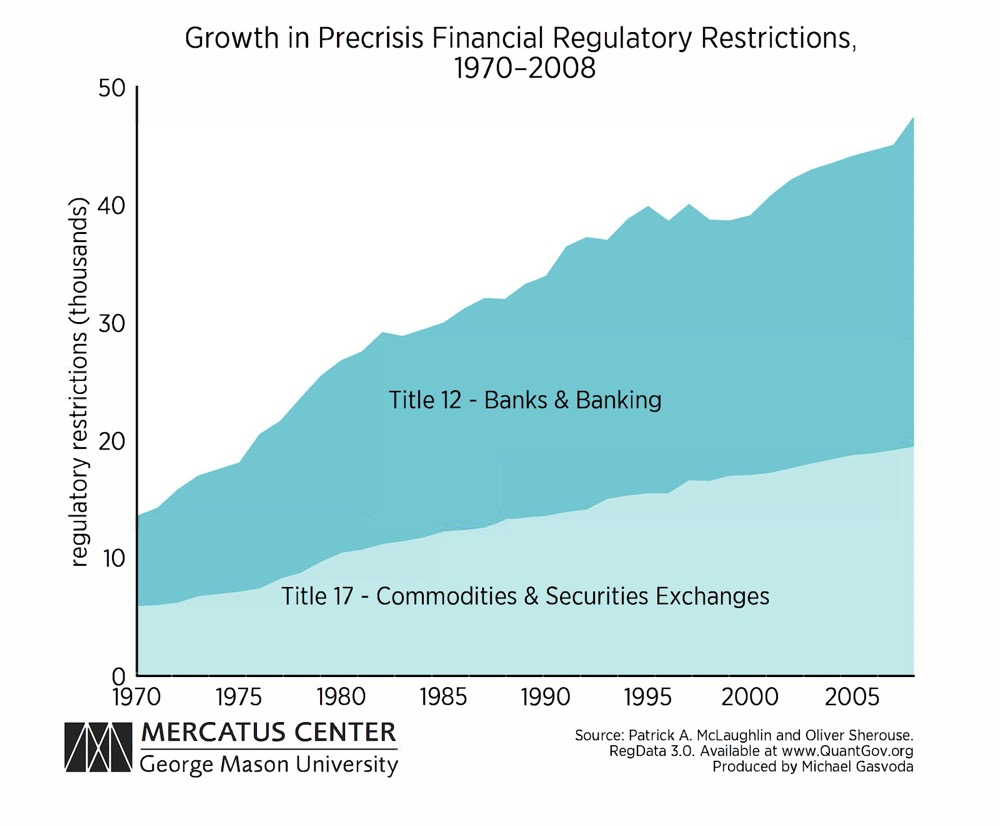

Over the past 50 years, regulatory development has been one-way: increasingly stringent financial regulation, combined with domestic and foreign policies aimed at controlling the global financial system. This trend accelerated after 9/11 and the 2008 financial tsunami.

Source: Mercatus Center

Of course, whether or not the U.S. government gives its blessing, permissionless digital currencies will ultimately exist. But will regulators recognize their inevitability and allow the U.S. government to sanction its own digital dollar?

I doubt they can resist the temptation to enter the ledger, banning enemy addresses, rewarding allies, and directly pursuing policy goals through control of the monetary system. If they do so, this version of the digital dollar will be no different from the current banking system.

Currently, due to the high-profile pursuit of "innovation," "RUSD" is able to persist. However, the designers of the STABLE Act, Assistant Professor Rohan Gray of Willamette University, briefly introduced the regulators' perspective: aren't these fiat-backed stablecoins just fully reserved digital banks?

Should their liabilities really be permanently viewed as cash rather than bank deposits? Can the U.S. regulatory machine resist the impulse to regulate this matter? The brief history following the enactment of the Patriot Act tells us: probably not.

Even the global intergovernmental organization Financial Action Task Force (FATF), which sets global standards for anti-money laundering regulations, recently stated that stablecoins "should never be exempt from anti-money laundering controls." Similarly, the Financial Stability Board (FSB) recently urged regulators to follow the principle of "same business—same risk—same rules, regardless of the underlying technology" when regulating stablecoins. The President of the European Central Bank recently agreed with this.

Currently, these RUSDs are entering the regulatory radar as "digital cash." But make no mistake: regulators do not want any such thing to exist.

Cash, what need is there for anonymity and untraceability? Cash reduces the readability of the economy, making it the enemy of the state. If cash no longer exists, the government will never allow it to be reinvented.

The only thing that can save RUSD today is that its scale is too small to attract the regulators' serious attention. Currently, they are mainly used for speculative trading in cryptocurrencies, which is a harmless pastime. In the broader dollar environment, they are merely a blip on the map (overall, the total issuance of all RUSD stablecoins is less than $20 billion, about one percent of commercial bank dollar deposits).

So what factors will pull the regulators' trigger to intervene and stop the crypto feast?

I can imagine two scenarios. One possibility is a surge in RUSD issuance to meet the growing global demand. Concerns about stablecoins exhibiting exponential growth could lead the U.S. Congress to take strong action to reverse the situation.

The second scenario could be triggered by a black swan event: for example, headlines about someone using stablecoins to fund terrorists, or a dictatorship using stablecoins to evade U.S. sanctions. At that point, there will be calls for immediate regulation of cryptocurrencies.

Note that I believe RUSD will not completely exit the historical stage. They will likely allow small balances without KYC, but once they exceed a certain size, accounts must undergo KYC to receive more funds. Alternatively, they could be regulated like banks and enforce KYC on all cryptocurrency holders. RUSD will have to start enhancing usage terms and actively regulate account fraud (which is currently not very strict).

Once this happens, RUSD will no longer be a satisfactory solution to meet global demand for crypto dollars. They will be used for institutional purposes in the U.S., but for non-U.S. individuals or those excluded from financial services, the regulations will be too strict to access. RUSD will essentially become enhanced bank deposits.

Only then, and not until then, will we enter the fourth phase of stablecoins: the phase where decentralized crypto dollars prevail.

6. The Ultimate Form of Crypto Dollars

So far in this article, I have not mentioned any decentralized stablecoins. This is intentional: decentralized stablecoins will only have a chance to be truly adopted once the aforementioned points are reached.

Why do I say it takes so long? Why must all other avenues reach a dead end before decentralized stablecoins have a chance to win?

The main feature of stablecoins is, of course, that their value is pegged to $1. However, the price anchoring of decentralized stablecoins is always relatively weak, putting them at a disadvantage compared to centralized stablecoins.

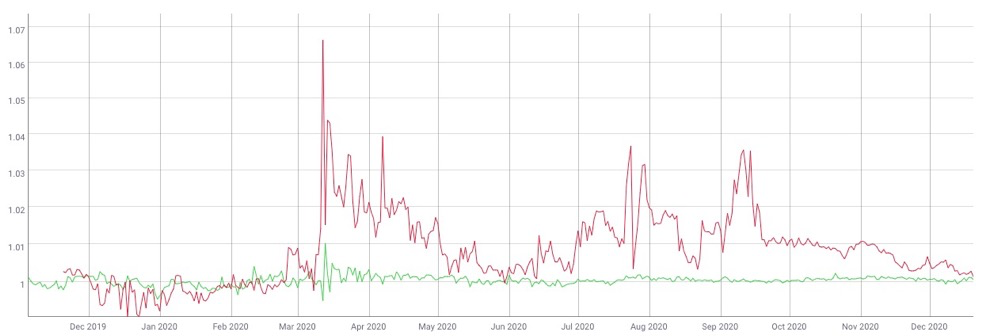

The relationship between USDT price anchoring (green line) and Dai price anchoring (red line) in 2020, source: Coinmetrics

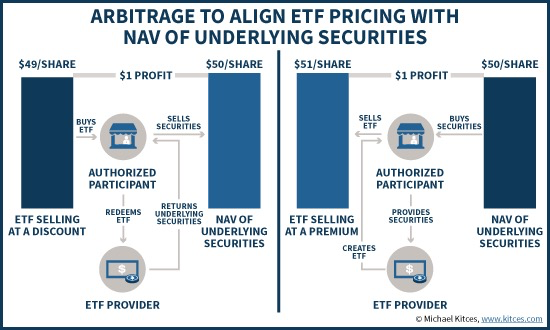

Fiat-backed stablecoins maintain their price anchoring through a creation-redeem cycle, similar to ETFs. If the price is too high, arbitrageurs can invest dollars to mint new stablecoins and sell them on the open market for profit. If the price is too low, they can buy stablecoins and redeem them for dollars to profit. All of this is a quick and low-risk operation, allowing arbitrageurs and market makers to swiftly ensure stablecoins are pegged to the dollar.

Demonstration of ETF creation-redemption arbitrage, source: Michael Kitces

Crypto-native stablecoins are different. Their price anchoring power is weaker because there is no real arbitrage for their price anchoring; their operation resembles central banks setting price range targets. Monetary policy operates slowly, and when the currency deviates from its peg, central banks will try to respond in real-time. Speculators may bet that the peg will soon be restored, but this is not arbitrage; it is better described as short-term speculation on the future effectiveness of monetary policy.

But this mechanism is effective! It does create decentralized stablecoins. The current Dai proves this, as it survived a roughly 95% drop in ETH collateral prices over the course of a year in 2018, maintaining its peg to the dollar, even surviving Black Thursday, when ETH collateral prices plummeted by over 50% in a single day.

We know that the mechanisms behind decentralized price anchoring can work in highly volatile markets. However, we also know that they do not thrive as much as centralized stablecoins, given that their mechanisms are much more complex, which is not surprising.

Decentralized stablecoins cannot compete directly with fiat-pegged stablecoins. However, decentralized stablecoins have one advantage: they indeed possess censorship resistance.

Unfortunately, the market does not care about this at all. Because currently, no one is conducting large-scale censorship of stablecoins.

If there is no actual censorship of these centralized stablecoins, then USDT offers you the same thing that Dai aims to provide, just with stronger liquidity and tighter price anchoring. For practical purposes, Dai is a worse stablecoin compared to USDT.

But this situation will eventually change.

The blade of censorship will fall, as regulators will not tolerate truly unregulated digital cash. Once they implement regulations on fiat-backed stablecoins, only those with censorship resistance will hold value among stablecoins, and then only assets like Dai, Celo, or ESD will become suitable pricing assets in the crypto industry.

This is why I believe decentralized crypto dollars will become the long-term view of future currency in the crypto world. I believe they will fundamentally change the global financial landscape.

But all of this will not happen quickly. It is difficult to specify a timeline here, but it may take over 3 years for it to fully manifest. Given that there will be many other changes in the world by then, any prediction that seems so distant will inevitably become vague.

Currently, the STABLE Act is a legislative proposal. It is not an ending in itself, but a harbinger of future outcomes.

As an investor, I am optimistic about decentralized crypto stablecoins. In the long run, they are the only truly long-term effective way for people to obtain dollars in a decentralized manner from anywhere in the world.

Conflict of interest: Dragonfly has invested in MKR, CELO, and ESD projects.