Sought after by VCs, what is the current state of decentralized crypto derivatives?

DeFi derivatives will be one of the most important trends in decentralized finance in the coming future.

DeFi derivatives will be one of the most important trends in decentralized finance in the coming future.This article was published on November 29, 2020, on Defi Dao, by author Sato Xi.

As one of the most complex and mature tools in the financial market, the allure of derivatives is undoubtedly immense. Their characteristics, such as high leverage, attract a large number of risk-seeking traders pursuing high returns. According to data from the Bank for International Settlements (BIS), the total outstanding amount of derivative contracts was approximately $640 trillion in the first half of 2019, while the total market value of all these contracts was about $12 trillion.

In the cryptocurrency market, centralized derivative trading has long become a major source of income for various exchanges. We have heard many stories of overnight wealth from contract trading in the crypto space, as well as tragic tales of people losing everything due to liquidation. We all understand that those who can steadily achieve profits are the trading venues that provide these trading tools and charge transaction fees.

Decentralized finance (DeFi), which is still in the imitation stage, aims to rebuild these financial tools in a decentralized environment through smart contracts. This may eliminate some of the drawbacks of centralized platforms, such as custody, opacity, and susceptibility to manipulation. Of course, the ultimate goal of developers is to compete for this highly profitable market.

In this article, you will learn about:

- Common financial derivative tools;

- A brief history of centralized crypto derivatives;

- Investment institutions competing to layout DeFi derivative applications;

- A comparison of common DeFi derivative applications

- Synthetix

- dydx

- DerivaDEX

- UMA

- Perpetual Protocol

- Hegic

- opyn

- Serum

- Futureswap

- Potential risks faced by DeFi derivative protocols

- Conclusion

### 1. Common Financial Derivative Tools

In finance, derivative tools are contracts whose value is derived from the performance of underlying entities. The contract specifies the specific conditions under which the parties will trade, including:

- The predetermined time period;

- The defined outcome value of the entity and underlying variables;

- Contract obligations and nominal amounts;

The entities defined in derivative tool contracts can be cryptocurrencies, commodities, stocks, bonds, interest rates, and currencies. To understand the true utility of financial derivatives, we need to study different types of contracts. We can categorize derivatives trading into two markets:

- Over-the-Counter (OTC): Parties directly and privately enter into these contracts, with the underlying assets not being on any exchange. For example, investment banks typically use OTC derivatives.

- Exchange-Traded: As the name suggests, these derivatives are traded on exchanges, with contract terms predetermined and public.

Now, let’s take a look at the common types of financial derivative contracts, which include:

- CDO: Collateralized Debt Obligation (CDO) is one of the causes of the 2008 financial crisis, making it a notorious type of financial derivative;

- Credit Default Swap (CDS): CDS allows investors to exchange their assets or debts for another asset or debt of similar value;

- Forward: An OTC financial derivative tool that allows buying or selling an asset at a predetermined value on a specific future date;

- Contract for Difference (CFD): CFDs enable traders to buy or sell a certain number of asset units based on price fluctuations through leverage;

- Futures: Buying or selling an asset at a predetermined price on a future date;

- Options: Buying or selling an asset at a predetermined price on or before a future date;

- Perpetual Future Contract: A special type of futures contract that does not have an expiration date.

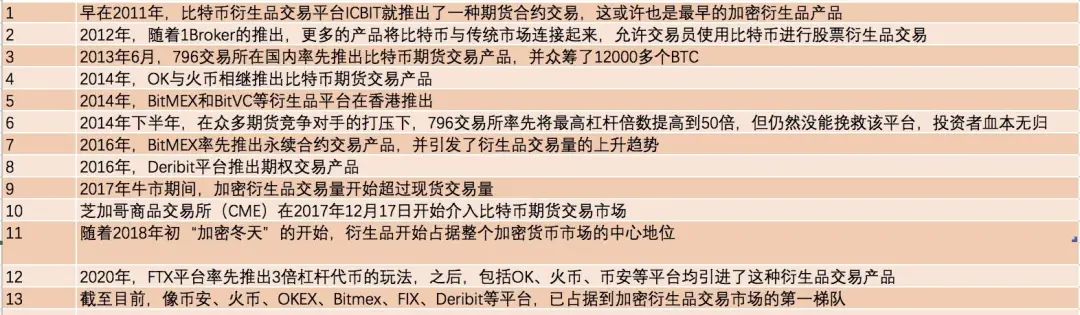

After briefly understanding these derivative types, let’s review the brief history of centralized crypto derivatives.

### 2. A Brief History of Centralized Crypto Derivatives

In the history of the cryptocurrency trading market, derivatives have played an extremely important role. The success of platforms we are familiar with today, such as OKEX, Huobi, Binance, Bitmex, FTX, and Bitfinex, is largely related to derivatives. Some derivative platforms have already disappeared from our sight, such as the once well-known 796 Futures Exchange in China.

From the current market performance, perpetual contracts and leveraged tokens have become the most popular crypto derivatives among retail traders.

### 3. Investment Institutions Competing to Layout DeFi Derivative Applications

With the landscape of centralized crypto trading derivatives established and the gradual rise of decentralized finance (DeFi), investment institutions are increasingly turning their attention to the field of DeFi derivatives. Many investors believe that DeFi derivatives will be one of the most important trends in decentralized finance in the near future.

For example, well-known crypto investment institutions such as Multicoin Capital, Three Arrows Capital, Alameda Research, Polychain Capital, Andreessen Horowitz, Framework, Coinbase Ventures, Binance Labs, and Placeholder have all laid out DeFi derivative applications.

In the article titled "Competition and Trade-offs in the Decentralized BitMEX Track," TUSHAR JAIN, managing partner at Multicoin Capital, summarized some advantages of DeFi derivative protocols, such as:

- No centralized exchange operators, leading to lower fees in the long run;

- Permissionless access;

- Censorship-resistant features, preventing anyone from shutting down the exchange;

- No counterparty risk, as users hold their own funds;

- No withdrawal limits or trading volume restrictions;

- No unilateral changes to the exchange's rules;

- Any asset with public price feeds can be traded.

So, what DeFi derivative protocols have these investment institutions laid out? Let’s illustrate this with a chart:

In the fourth section, we will get to know these DeFi derivative protocols that are favored by institutions one by one.

### 4. Comparison of Common DeFi Derivative Applications

4.1 Synthetix

As the most well-known synthetic asset protocol on the Ethereum platform, Synthetix currently plays a "big brother" role in the DeFi derivatives space. According to its design, participants can synthesize various synthetic assets (Synths) by staking the protocol's native asset SNX. This collateral pool model allows users to execute conversions between Synths directly using smart contracts without a counterparty, solving the liquidity and slippage issues faced by DEXs.

As stakers, SNX holders can receive two types of rewards: 1) token rewards from the system's inflationary monetary policy, and 2) trading fee rewards from synthetic assets (Synths) (0.1%-1%, usually around 0.3%).

Currently, users can trade these synthetic assets (Synths) on Synthetix.Exchange, and they can also use another ecosystem project, Kwenta, for trading. Additionally, the asset management protocol dHEDGE based on Synthetix enables non-custodial hedge fund functions, forming a good complementary relationship with Synthetix.

As of now, the value of assets locked in the Synthetix protocol is approximately $720 million.

It is worth mentioning that starting from the end of June this year, Synthetix also introduced binary options trading, but there haven't been many users utilizing this trading product.

Moreover, according to plans, Synthetix will achieve scalability through the optimistic rollup layer-2 network next year and reduce transaction fees. The project also plans to introduce futures, leveraged tokens, and other derivative products.

Despite this, the current Synthetix has obvious flaws or limitations, such as low capital efficiency and systemic risks that may arise from traders betting against the system. Additionally, since Synthetix currently only supports participants staking the native asset SNX to synthesize Synths, this limits the scale of synthetic assets, providing some opportunities for other synthetic asset protocols.

4.2 dydx

The dydx protocol, favored by Polychain Capital and Andreessen Horowitz, is another DeFi derivative protocol worth paying attention to. Although it has not yet issued a token, the value of assets locked on the platform has exceeded $42 million.

Over time, dydx's product line has become increasingly rich. As of the time of writing, dydx offers four services: spot trading, leveraged trading (5X), perpetual contract trading (10X), and lending, with a total trading volume of approximately $5.779 million within 24 hours. However, the variety of trading pairs supported is relatively limited, currently only supporting ETH, BTC, LINK, DAI, and USDC.

In terms of user experience, dydx is easy to use, but the downside is that due to the order book model adopted, it is relatively difficult to initiate liquidity. Overall, the depth on dydx is not very good at present.

Additionally, according to plans, dydx will collaborate with StarkWare to utilize the StarkEx layer-2 network for expansion.

(Note: Since dydx has not yet issued a token, some analysts speculate that dydx may adopt a similar airdrop method to Uniswap for its users.)

4.3 DerivaDEX

DerivaDEX, which has received investment from well-known institutions such as Polychain Capital, Coinbase Ventures, and Three Arrows Capital, aims to achieve an efficient trading engine using the SGX Trusted Execution Environment (TEE). According to plans, DerivaDEX can support perpetual contracts with up to 25 times leverage.

As of now, DerivaDEX has not launched its mainnet and has not issued tokens (the tokens currently appearing on the market are all counterfeit). Due to the order book model adopted, guiding liquidity will be a major challenge for DerivaDEX. The new token distribution method it employs is called "insurance mining," and its specific performance remains to be observed.

4.4 UMA

The UMA protocol, supported by Coinbase Ventures and Placeholder, is another synthetic asset protocol worth noting in the current market. One of the main differences between it and Synthetix is that collateral and debt exposure are isolated in UMA, which reduces systemic risk, but the trade-off is lower liquidity.

Additionally, UMA does not use oracles like Chainlink; instead, it employs a mechanism called "priceless contracts," which is an innovative mechanism but has not yet been sufficiently tested.

As of now, the value of assets locked in the UMA protocol is approximately $40 million.

4.5 Perpetual Protocol

Perpetual Protocol, as the name suggests, is a derivative protocol focused on perpetual contract trading. In theory, it can support perpetual contract trading for various synthetic assets such as BTC, ETH, gold, and ERC-20 tokens. The protocol adopts a new mechanism called vAMM, which, unlike traditional AMMs, does not require liquidity providers (LPs). Traders can provide liquidity to each other, and the slippage of trades is determined by a k-value set manually by the vAMM operator based on the situation.

According to plans, Perpetual Protocol will launch on the xDAI sidechain in the coming weeks, meaning that trading on the protocol can save on expensive gas fees. However, based on recent testing experiences, the slippage on Perpetual Protocol is still relatively high, and further observation will be needed after its mainnet launch.

Holders of the Perpetual Protocol token (PERP) can stake their tokens in the staking pool to earn transaction fee rewards and staking incentives.

4.6 Hegic

Unlike other DeFi derivatives mentioned in this article, Hegic does not have backing from well-known investment institutions. As an options protocol, it has quickly become one of the hottest derivative protocols under the recommendation of yEarn founder Andre Cronje.

Hegic uses an AMM model to solve the liquidity problem of options. Anyone can provide funds to the liquidity pool and automatically sell call and put options, forming a counterparty with the buyers of the options. One notable advantage of Hegic is that it simplifies the complexity of purchasing options. However, options products are relatively distant from retail investors and are more suitable for professional investors.

As of now, Hegic has approximately $70 million locked in funds and is in a clear leading position in the options derivatives field.

4.7 opyn

Opyn is an early-established DeFi options protocol that uses the Convexity protocol to allow users to create put and call options. Users can purchase its option tokens (oToken) to hedge DeFi risks or deposit collateral in the vault to mint and sell oTokens, thus earning rewards.

As of now, opyn has approximately $2.6 million in locked assets, which seems a bit "meager" compared to the rapidly growing Hegic, but this is partly due to its not having issued its own token.

Overall, opyn is another options protocol worth paying attention to, but compared to perpetual contracts and futures, the development of the crypto options market still requires more time.

Additionally, although opyn has undergone a security audit by OpenZeppelin, it experienced a security incident in August this year, resulting in a loss of nearly $400,000.

4.8 Serum

Compared to other Ethereum-based DeFi derivative protocols, Serum is built on the Solana blockchain, which brings it scalability and cost advantages while eliminating the composability advantages of the Ethereum platform, similar to constructing real estate in a remote area.

Nevertheless, Serum's progress in derivatives has been relatively slow. Currently, it only offers swap trading services, while lending, margin trading/contracts will only be realized in the third phase.

Other Ethereum-based DeFi derivative protocols can achieve scalability through rollup layer-2 networks, which will put greater competitive pressure on Serum. The potential advantage of Serum lies in the FTX team and Alameda Research behind it, which may provide it with some competitive leverage.

4.9 Futureswap

Futureswap is another DeFi derivative protocol that was once highly anticipated and has received support from well-known institutions such as Three Arrows Capital and Framework. In April of this year, Framework announced the launch on the Ethereum mainnet, but after a brief operation of 3 days, the official suddenly announced a suspension, citing "the alpha version's user trading volume grew too quickly." Since then, Futureswap has not disclosed any updates on its progress. On November 14, a team member named Derek stated on Discord that they would update an article explaining the specific mechanism of large perpetual contract trades not generating slippage.

### 5. Potential Risks Faced by DeFi Derivative Protocols

Like any DeFi protocol, DeFi derivative protocols face potential risks of contract vulnerabilities and composability risks. Additionally, due to the higher leverage used in DeFi derivative protocols, they are more susceptible to oracle manipulation attacks. For example, recently, after an abnormal price of DAI on the Coinbase Pro platform, Compound, which used that platform's oracle price feed, liquidated collateral worth nearly $100 million, ringing alarm bells for derivative protocols.

Currently, most DeFi derivative protocols rely solely on Chainlink for price feeds. Such security measures may not be sufficient for the future large decentralized derivatives market. In the future, it will be essential for DeFi derivative protocols to adopt a composite price from multiple oracle quotes.

Furthermore, due to the more complex contracts of DeFi derivative protocols, there may also be unknown attack vector risks. As time goes on and the industry scales up, these issues may gradually become apparent.

### 6. Conclusion

By reviewing the development history of the traditional cryptocurrency circle, we can find that the development of derivatives trading has started relatively slowly compared to spot trading. However, as the market enters a highly volatile bull market cycle, derivatives will gradually catch up with spot trading and eventually dominate.

As of now, spot DEX exchanges represented by Uniswap have been able to compete with spot trading platforms like Coinbase, while in the derivatives trading field, no DeFi protocol has yet posed a sufficient threat to centralized derivative platforms like Binance and Bitmex. However, this also means that every protocol has significant opportunities.

Perhaps in the next 1-2 years, 1-2 applications among these derivative protocols will emerge with a market value reaching billions of dollars, and they will be able to effectively address scalability, security, and usability issues. Perpetual contracts and leveraged token products may be very important components of this.