What are the considerations for the dual-layer operation architecture of digital renminbi, and how to build the wallet ecosystem?

A towering building rises from the ground, and the digital renminbi is not a castle in the air; its construction relies on a solid and intricate underlying framework. Beyond the lofty concept of digital renminbi, what kind of underlying design supports its circulation and operation?

A towering building rises from the ground, and the digital renminbi is not a castle in the air; its construction relies on a solid and intricate underlying framework. Beyond the lofty concept of digital renminbi, what kind of underlying design supports its circulation and operation?On the global central bank digital currency (CBDC) track, China's central bank digital currency (DC/EP) has achieved remarkable results, leading in both research progress and internal testing work.

According to Zhou Xiaochuan, former governor of the People's Bank of China, DC/EP is a dual-layer research and pilot project plan, rather than a payment product. The DC/EP project plan may include several payment products that can be tried and promoted, which are ultimately named e-CNY, or digital renminbi.

In concept, the digital renminbi is a digital form of legal currency issued by the People's Bank of China, operated by designated operating institutions and exchanged with the public. It is based on a broad account system, supports loosely coupled bank account functions, is equivalent to cash and coins, possesses value characteristics and legal tender status, and supports controllable anonymity.

A tall building rises from the ground; the digital renminbi is not a castle in the air, and its construction relies on a rigorous and sophisticated underlying framework. What kind of underlying design supports the circulation and operation of the digital renminbi?

Issuance and Circulation of Digital Renminbi: Dual-Layer Operating Structure

The digital renminbi adopts a dual-layer operating system of "central bank - commercial banks/other operating institutions": the first layer is the central bank, and the second layer includes commercial banks, telecommunications operators, and third-party payment network platform companies.

According to Fan Yifei, deputy governor of the central bank, the central bank occupies a central position in the digital renminbi system, responsible for wholesaling digital renminbi to designated commercial banks and managing its entire lifecycle, while commercial banks and other institutions are responsible for providing digital renminbi exchange and circulation services to the public.

According to Wang Yongli, former vice president of Bank of China and chief economist of Shenzhen Haiwang Group, the central bank chooses commercial banks with strong capital and technological capabilities as designated operating institutions, opening different categories of digital renminbi wallets based on the strength of customer information identification, and providing digital renminbi exchange services. Designated operating institutions collaborate with other commercial banks and related institutions to jointly provide circulation services for digital renminbi.

Digital renminbi can only be used for payments and cannot be used for loan issuance, so it does not accrue interest. The central bank establishes a free digital renminbi value transfer system and financial infrastructure, does not charge the issuance layer for exchange and circulation service fees, and commercial banks do not charge individual customers for digital renminbi exchange services. Referring to the current arrangements for cash issuance, the issuance costs are allocated to designated exchange operating institutions, and a reasonable and effective incentive mechanism is established.

Wang Yongli pointed out that the digital renminbi red envelope pilot in Shenzhen also reveals the context of this dual-layer operation: winners need to download the central bank's unified "Digital Renminbi APP," and then open a "digital renminbi wallet" at a selected bank (one of the four major banks: ICBC, ABC, BOC, or CCB) to obtain and use digital renminbi, with mobile phones becoming an important carrier for digital wallets and QR code confirmation becoming the main payment method.

Wang Yongli thus concludes that the central bank can obtain the names, ID numbers, mobile phone numbers, and other information of digital renminbi holders through the "Digital Renminbi APP," and establish a reference account for each holder on the digital renminbi platform, forming a "single ledger" of digital currency for the entire society at the central bank, comprehensively mastering all transaction information related to digital renminbi exchange and circulation, and conducting necessary monitoring and analysis.

Designated operating institutions also need to download the central bank's digital renminbi APP and open accounts, making the central bank the clearing center for digital renminbi, achieving interconnectivity across operating institutions; for each payment made with digital renminbi, relevant information must be sent to the central bank simultaneously, allowing the central bank to comprehensively grasp all transaction information, while the digital renminbi wallet operating institutions can only understand information related to their own wallets. If the digital renminbi wallets of the payer and payee do not belong to the same operating institution, then each operating institution cannot grasp all information of both parties in the transaction, thus achieving "limited anonymity" for digital renminbi.

Centralized Management Responsibilities of the Central Bank

In the dual-layer operating structure, the digital renminbi emphasizes the centralized management of the central bank while prudently selecting strong commercial banks as designated operators to provide digital renminbi exchange services to the public.

Fan Yifei pointed out in an article that adhering to centralized management of digital renminbi issuance is of great significance: 1. Maintaining the status of legal currency and the right to issue currency, preventing the loss of currency issuance rights in the digital economy era; 2. Improving the efficiency of the payment system, enhancing the transmission of monetary policy, and facilitating the breaking of retail payment barriers and market segmentation; 3. Maintaining financial stability. The digital renminbi adopts a controllable anonymity mechanism, allowing the People's Bank of China to grasp all information, utilizing big data, artificial intelligence, and other technologies to analyze transaction data and fund flows, preventing and combating money laundering, terrorist financing, and tax evasion.

Zhou Xiaochuan pointed out that as the main body of the first layer structure, the central bank needs to fully mobilize the enthusiasm of all parties through its role design, so that the strengths of each party can be fully utilized. Specific responsibilities include the following: First, maintaining the stability of the digital renminbi's value; Second, building reliable settlement and clearing infrastructure; Third, the central bank is responsible for promoting interconnectivity between different payment products; Fourth, the central bank must be prepared with emergency and alternative plans in a dynamically evolving system.

Li Lihui, former president of Bank of China, believes that the central bank must maintain technological neutrality, and more importantly, maintain the model of centralized management to ensure the reliability of the monetary policy window mechanism and the efficiency of monetary control.

To maintain the central bank's position of centralized management, Fan Yifei also pointed out that the following must be achieved: First, overall management of digital renminbi quotas, establishing unified business standards, technical specifications, security standards, and application standards. Second, overall management of digital renminbi information, recording and monitoring the exchange and circulation of digital renminbi by grasping all transaction information, improving the central bank's issuance system in the digital age. Third, overall management of digital renminbi wallets, under the premise of adhering to a unified recognition system and anti-counterfeiting functions for digital renminbi, adopting a co-construction and sharing approach to jointly develop a wallet ecosystem platform by the central bank and designated operating institutions, while achieving their respective visual recognition and unique functions. Fourth, overall construction of digital renminbi issuance infrastructure, achieving interconnectivity across operating institutions, ensuring stable and orderly circulation of digital renminbi.

100% Full Reserve Requirement, No Interest Paid

In the dual-layer operating system, a 100% full reserve requirement is needed, and no interest is paid.

"The goal of issuing digital currency in our country is to replace cash M0. At the current stage, when commercial banks exchange cash, they need to pay a 100% reserve requirement to prevent commercial banks from overissuing digital currency; this is also to enhance public trust in digital currency, reflecting the national credit behind it," said Hao Yi, a postdoctoral researcher at Renmin University of China.

Song Jiajie, an analyst at Guosheng Securities, stated that not adopting a 100% reserve requirement means that commercial banks could use central bank digital currency to issue loans and derive deposits, which could disrupt the existing financial system.

Not paying interest is also related to the primary positioning of the digital renminbi as M0.

Fan Yifei pointed out in an article that according to Samuelson's definition of public goods in "The Pure Theory of Public Expenditure," legal currency is a public good. Therefore, central banks do not charge fees for cash transactions, and the costs related to design, production, transportation, storage, recycling, and destruction are borne by the government. The digital renminbi also belongs to pure public goods. The People's Bank of China implements a free strategy for digital renminbi that is consistent with cash. The central bank establishes a free digital renminbi value transfer system and financial infrastructure, does not charge the issuance layer for exchange and circulation service fees, and commercial banks do not charge individual customers for digital renminbi exchange services.

Based on a Broad Account System: Loosely Coupled Accounts

Compared to cash, the digital renminbi will provide users with a completely new experience: there is no need to open an account at a commercial bank; simply downloading the central bank's digital wallet app and completing registration allows for online payments.

Sun Yang stated that the central bank's digital currency is based on a broad account system, meaning that the central bank digital currency can achieve value transfer independent of traditional bank accounts, significantly reducing the reliance on accounts in the transaction process, representing a loosely coupled account system. Therefore, for users and enterprises, if they only use digital renminbi for small payments in daily life, there is no need to go to a commercial bank or institution to open an account; they can simply download the central bank's digital wallet app, complete registration, and use the central bank digital currency for transfers.

Sun Yang also pointed out that, in addition to withdrawing digital renminbi from the digital wallet or recharging it, users can transfer funds to each other without binding accounts. A digital currency wallet is not a bank account.

"The advantage of loosely coupled accounts is that they are highly accessible, which is beneficial for inclusive finance, especially significant for rural and remote areas. As long as there is a legal document that can identify your identity, it can serve as an account for carrying a digital currency wallet," Sun Yang said.

Li Lihui also pointed out that digital currency adopts a loosely coupled account + digital wallet model, achieving end-to-end transfers and enabling controllable anonymous payments. Foreigners coming to China can also apply for a digital wallet to gain payment convenience.

"However, there are still risks of money laundering. Even if limited management is applied to anonymous accounts, in the digital age, there is still the possibility of using technology to control a large number of anonymous accounts for small transactions to achieve money laundering," Hao Yi stated.

Sun Yang also believes that loosely coupled accounts raise requirements for security and risk control, as other account systems, such as social security, driver's licenses, ID cards, and student IDs, may not possess the online risk control capabilities of financial institutions, which requires the central bank digital currency system to deploy more technology in KYC and risk control to ensure safety.

Song Jiajie pointed out that the ideal "loosely coupled" scenario is that small payments do not need to be bound to bank accounts (but large payments do), but we expect this situation to be difficult to achieve because as long as different banks are involved, user identities need to be marked to avoid confusion, and this marking is precisely the concept of "accounts."

Digital Renminbi Ecosystem

Mu Changchun, director of the Central Bank Digital Currency Research Institute, previously stated: "Building the digital renminbi ecosystem requires exploring cooperation models between designated operating institutions and other commercial banks as well as other commercial entities."

Fan Yifei stated that to ensure the widespread availability of digital renminbi without causing significant disruption to the existing financial market, it is necessary to fully leverage the positive roles of other commercial banks and non-bank payment institutions within the digital renminbi system. Designated operating institutions, such as commercial banks, along with other commercial banks and related institutions, will undertake the circulation services of digital renminbi under the supervision of the People's Bank of China and be responsible for managing the retail segment, ensuring the safe and efficient operation of digital renminbi, including payment product design innovation, scenario expansion, market promotion, system development, business processing, and operation and maintenance services.

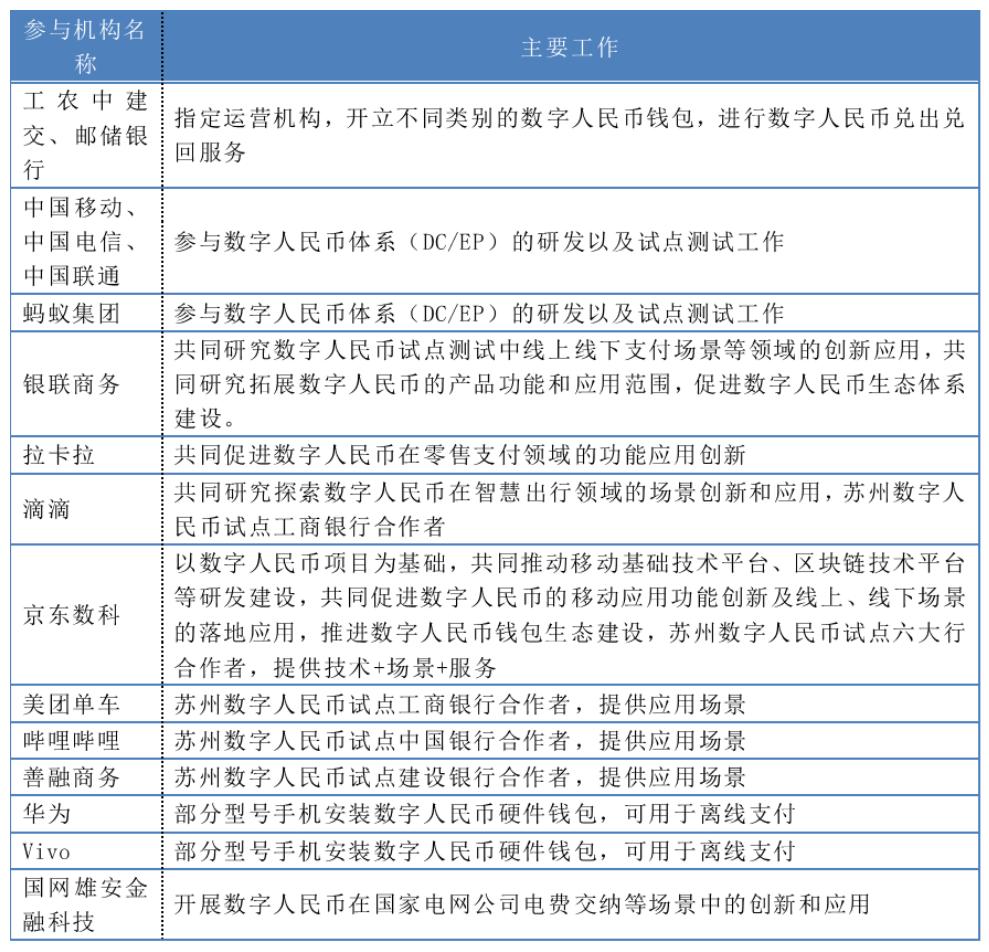

Since the beginning of this year, several internet technology companies, payment companies, clearing institutions, and other entities have joined the digital renminbi project, mainly undertaking the work of developing application scenarios and continuously enriching the digital renminbi ecosystem. The following table summarizes the currently exposed participating institutions:

Some institutions participating in the digital renminbi project

So, how are these companies collaborating with operating institutions to participate in the digital renminbi ecosystem?

On December 11, the results of the lottery for the digital renminbi red envelope activity in Suzhou were announced. After winners downloaded the digital renminbi wallet, the partners of the six major state-owned banks (ICBC, ABC, BOC, CCB, CEB, and PSBC) as designated operating institutions also emerged: Agricultural Bank of China, Postal Savings Bank, and Bank of Communications can only choose whether to connect to the JD APP; China Construction Bank, in addition to JD, can choose whether to connect to Shanzhong Business (CCB's B2C shopping platform); Bank of China, in addition to JD, can choose whether to connect to Bilibili; and Industrial and Commercial Bank of China has the most partners, in addition to JD, also including Meituan Bike and Didi Chuxing.

Among them, JD Technology is the first technology company to cooperate with all six major banks (ICBC, ABC, BOC, CCB, CEB, and PSBC) and connect to the digital renminbi e-commerce platform consumption pilot scenario. "In the digital renminbi pilot, JD Mall and JD Technology provided technology + services + scenarios," said Peng Fei, head of the digital renminbi project at JD Technology.

He pointed out that JD Technology's work in the digital renminbi pilot mainly connects with three types of entities: First, the central bank and the digital currency research institute; Second, the designated operating institutions for digital renminbi (the six major banks); Third, various merchants.

In the recently exposed digital renminbi wallet, the digital renminbi App can push sub-wallets to the institutions cooperating with the six banks.

An industry insider told The Paper: "This is a very interesting innovation because, in the current encrypted digital currency system, users can only control wallets through private keys, and each wallet is independent, without the paradigm of 'parent wallet - sub-wallet,' and there is no sub-wallet push function. This new type of wallet paradigm will bring more application scenarios to DC/EP."

He also believes that the privacy protection of sub-wallets confirms another function of digital renminbi: controllable anonymity. People need not worry about personal privacy being leaked when using digital renminbi in normal economic life.

Digital Renminbi Pilot Areas Expected to Expand

On April 19, 2020, a relevant person in charge of the Digital Currency Research Institute of the People's Bank of China stated that the research and development of digital renminbi is steadily advancing, with initial internal closed pilot tests being conducted in Shenzhen, Suzhou, Xiong'an New Area, Chengdu, and future Winter Olympic scenarios.

Currently, the internal testing work in the four major pilot cities is continuously progressing, mainly focusing on small, retail, and high-frequency business scenarios such as retail, transportation card recharging, and dining.

In addition, places such as Beijing, Shanghai, Hainan, Chongqing, and Hong Kong have also mentioned exploring digital renminbi.

On August 22, Hainan Province's Vice Governor Shen Danyang mentioned at the "2020 Golden Bull Asset Management Forum" that Hainan will actively strive for the application of legal digital currency pilots in cross-border trade in Hainan Free Trade Port.

On September 29, the Beijing Municipal Financial Supervision Bureau and the Economic and Information Technology Bureau issued a notice stating that they will actively seek national pilot policy support and explore the application of central bank legal digital currency in data transaction payment settlements at Beijing Data Exchange under the guidance of the People's Bank of China, aiming to create a payment settlement system that meets the characteristics of data transactions.

On November 24, at the China-ASEAN Financial Cooperation and Renminbi Internationalization Forum during the China-Singapore Financial Summit, Li Bo, Vice Mayor of Chongqing, stated that Chongqing will actively strive to carry out pilot projects for cross-border payments using digital trade and digital currency, exploring ways to assist the cross-border use of renminbi through digital currency.

On December 4, according to the official website of the Hong Kong Monetary Authority, HKMA Chief Executive Eddie Yue mentioned in an article titled "New Trends in Financial Technology - Cross-Border Payments" that the HKMA is studying the technical testing of using digital renminbi for cross-border payments with the Central Bank Digital Currency Research Institute and making corresponding technical preparations.

On December 10, the "Suggestions of the Shanghai Municipal Committee of the Communist Party of China on Formulating the 14th Five-Year Plan for National Economic and Social Development and the Long-Range Objectives Through the Year 2035" was officially released, proposing to "actively strive for the pilot application of digital renminbi."

Given the relatively sufficient preparatory work for digital renminbi and the smooth progress of internal testing, Dong Ximiao, chief researcher at the Internet Finance Research Institute of Zhongguancun, suggested in "Breaking Four Misunderstandings About Digital Renminbi" to further expand the pilot testing scope of digital renminbi and to launch it officially as soon as possible to better meet the public's demand for legal digital currency in the digital economy era.

He stated that the pilot testing cities should be expanded in an orderly manner. On one hand, cities with rapid digital economy development such as Beijing, Shanghai, and Hangzhou in the Beijing-Tianjin-Hebei and Yangtze River Delta regions should be increased; on the other hand, cities in the western regions with relatively weak financial infrastructure, such as Lanzhou, Urumqi, and Lhasa, should also be included.