Where is Digital Renminbi Heading: Is Alipay Facing Challenges? Are Banks Facing Opportunities?

Will there be changes to the monetary policy framework? Will the payment systems dominated by WeChat Pay and Alipay face challenges? Will commercial banks seize opportunities?

Will there be changes to the monetary policy framework? Will the payment systems dominated by WeChat Pay and Alipay face challenges? Will commercial banks seize opportunities?This article is sourced from The Paper, authored by Ye Yinghe

Digital RMB is approaching, the butterfly flaps its wings, and a "storm" is brewing.

As digital RMB enters reality, bringing convenience to people's lives, as a new form of currency, it will inevitably bring a series of changes to the domestic economic system:

Will there be changes in the monetary policy framework? Will the dominant payment systems of WeChat Pay and Alipay face challenges, and will commercial banks seize opportunities…

What possible impacts will it have on monetary policy

Mu Changchun, director of the Digital Currency Research Institute of the People's Bank of China, stated in a speech in August 2019 that the dual-layer operation system of digital RMB will not change the creditor-debtor relationship of circulating currency. To ensure that the central bank's digital currency is not over-issued, commercial institutions must pay 100% reserves to the central bank. The digital currency of the central bank remains a liability of the central bank, guaranteed by the central bank's credit, and has unlimited legal tender.

Additionally, he pointed out that the dual-layer operation system will not change the existing currency issuance system and dual-account structure, nor will it compete with commercial bank deposits. Since it does not affect the existing monetary policy transmission mechanism, it will not strengthen the pro-cyclical effects under pressure, thus not negatively impacting the real economy.

Fan Yifei, deputy governor of the central bank, noted in an article that commercial banks providing digital RMB exchange can accelerate the speed and efficiency of fund flows back to commercial banks, promoting their role as financial intermediaries and providing a more direct and efficient channel for monetary policy transmission.

"The issuance and redemption of DC/EP (central bank digital currency) will have a neutral impact on the monetary system. Additionally, if a portion of deposits turns into DC/EP, there will be some monetary tightening effect, but the scale of the effect will not be large, and the central bank's monetary policy can easily counteract it," said Zou Chuanwei, chief economist of Wanxiang Blockchain, to The Paper.

Wang Yongli, former vice president of Bank of China and chief economist of Shenzhen Haowang Group, pointed out that using new technology to promote the construction of a new digital currency system may solve the problem of how to scientifically and reasonably grasp the issuance and total control of credit currency.

He proposed the idea of "one account for digital currency": the central bank's digital currency platform will be open to society (open source), allowing all social entities (including financial institutions) to directly open a "unique basic account" on the central bank's digital currency platform, requiring real-name registration, recording each payment amount and maintaining timely account balances, but the account balance will only be for reference and will not accrue interest; social entities can also open "business-specific accounts" at commercial banks and other financial institutions to specifically record the changes in rights and obligations arising from the establishment of specific businesses and their results. This account will be linked to their basic account at the central bank, with some relaxation on real-name registration; when social entities conduct digital currency payments, relevant information needs to be transmitted simultaneously to the central bank and the relevant banks and financial institutions for accounting processing, and the results of the relevant account processing should be fed back to the account holder to protect their interests; the central bank and the financial institutions handling the business should also adjust their inter-account relationships one by one to maintain a balance in accounting processing.

"This way, the central bank can achieve comprehensive and full-process strict monitoring of the circulation of digital currency, enhancing the anti-money laundering, anti-terrorism financing, anti-commercial bribery, and anti-tax evasion capabilities of digital currency, while also achieving limited anonymity outside the central bank, moderately protecting commercial secrets and personal privacy, without causing a huge impact on the existing monetary financial system."

Stop at M0, or take another step forward?

According to the central bank's vision, digital RMB is positioned as M0, which refers to cash in circulation.

Wang Yongli believes that the central bank's digital currency may only start by replacing M0, but it should not be limited to this and should aim to replace all forms of currency as much as possible.

"If the central bank digital currency only replaces M0, it will only affect less than 4% of the total money supply, and the impact on the implementation of central bank digital currency policy and monetary supply control will be limited. If the central bank digital currency 'one account' is realized, it will be completely different," he told The Paper, "The launch of the central bank digital currency should make it more convenient for people to conduct monetary transactions, at least not worse than now. Otherwise, it will be hard to be competitive."

However, Zou Chuanwei believes that it is unlikely for the central bank digital currency to expand from M0 to M1 (narrow money) or M2 (broad money).

"From a legal relationship perspective, the central bank digital currency is a liability of the central bank, so it can only be M0. A large part of M2 is the liabilities of commercial banks, which are deposits. Therefore, it is logically very difficult for the central bank digital currency to become M2," Zou Chuanwei said. "If commercial bank deposits are turned into digital M2, it means they can be controlled anonymously like cash, which would effectively revert China's deposits to a non-real-name account state, making it impossible for financial regulation to function properly."

He stated that if DC/EP can sufficiently meet the public's demand for anonymity, there is no need for commercial banks to provide digital M2. If digital M2 is provided, it would have a significant impact on the financial system, and from the practices of various countries, whether retail or wholesale, central bank digital currencies have replaced M0.

Wang Zhicheng, an associate professor at Peking University's Guanghua School of Management, believes that the current publicly stated goal is to replace M0 (cash), which is also a correct entry point. Once successfully operated, it will be very easy to further expand to replace M1 (narrow money).

The relationship between digital RMB and Alipay, WeChat Pay

For ordinary people, the biggest confusion may be: what is the difference between digital RMB and third-party payments like Alipay and WeChat Pay?

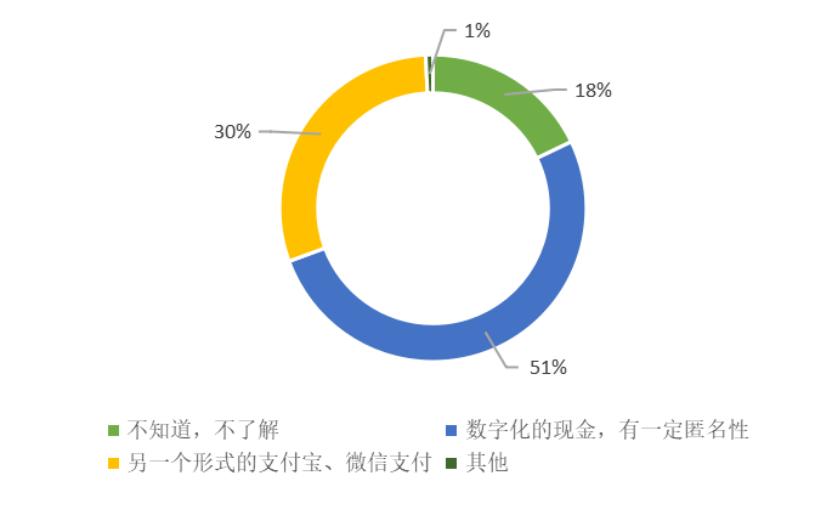

According to an online survey conducted by The Paper, nearly 30% of respondents believe that digital RMB is the same as Alipay and WeChat Pay.

Respondents' understanding of the concept of digital RMB

"Alipay and WeChat are not on the same dimension as digital RMB, and there is no competitive relationship." On October 25, Mu Changchun said at the Bund Financial Summit.

He believes that WeChat and Alipay are financial infrastructure; simply put, they are wallets. In the era of electronic payments, the contents of the wallet are essentially commercial bank deposit currency. In the digital RMB era, the wallet in WeChat and Alipay will include digital RMB as an option, allowing the public to continue using WeChat and Alipay for payments, but the payment tools will now include not only bank deposit currency but also digital RMB.

Zeng Gang, deputy director of the National Financial and Development Laboratory, told The Paper that Alipay and WeChat are front-end payment tools, while the back-end is cash digital. Currently, Alipay's back-end cannot link to cash, as cash is completely outside the system, only linked to bank accounts. In the future, Alipay can link both digital currency and bank accounts.

Zeng Gang believes that unless there is a significant breakthrough in application scenarios or innovative situations, digital RMB will not have a major direct impact on people's payment habits and the current payment market structure.

He said: "The purpose of digital RMB is to replace cash, improve the efficiency of cash management, and reduce various issues in the cash management process, rather than to achieve this process while minimizing the impact on the existing system."

Will digital RMB change the payment market structure?

In the current mobile payment market, the combined market share of Alipay and WeChat Pay exceeds 90%, and both have set barriers between each other. Will the emergence of digital RMB and digital RMB wallets change this structure?

Li Lihui, former president of Bank of China, believes that the central bank digital currency is expected to run in parallel with mature third-party payment platforms for a long time, becoming a major payment tool without quickly replacing them.

Dong Ximiao, chief researcher at the Zhongguancun Internet Finance Institute, added in "Breaking Four Misunderstandings About Digital RMB": "Digital RMB can break the barriers in the payment industry and achieve circulation among supported banks and payment tools, while transfers between Alipay and WeChat are not possible."

Some scholars have stated that the launch of digital RMB intends to break the monopoly of Alipay and WeChat Pay, which may impact the payment market in the future.

Wang Zhicheng, an associate professor of finance at Peking University's Guanghua School of Management, believes that new internet companies have occupied the payment market using technological advantages, and large state-owned banks have also been trying to enter the market in recent years, but due to user habits, the results have not been significant. "Currently, the approach is through digital currency, and anti-monopoly is a boost."

Hao Yi, a postdoctoral researcher at Renmin University of China, believes that even if digital RMB can be used in the wallets of WeChat and Alipay, it may still impact them.

"The most direct impact is that money in WeChat and Alipay can be transferred to the digital RMB wallet, saving related fees," he said.

Wang Yongli pointed out in his article "Where is the Real Innovation and Change of Digital RMB Similar to Alipay and WeChat Pay" that the digital RMB requires downloading a unified APP from the central bank, which will bring significant changes to the operational system and mechanism of digital RMB payments.

Wang Yongli noted that the digital RMB App can form the most complete big data of digital RMB transactions in society, becoming a valuable digital asset and replacing the big data of various financial institutions and payment companies, which will have a profound and significant impact on China's payment system and even the market structure of financial institutions.

"The impact of the operational model change of digital RMB will primarily affect the bank card system and related industries closely related to payment and settlement, as well as non-bank payment institutions! For example, the central bank may control all user information and transaction data of digital RMB, which could severely impact Ant Group, which relies on payment and big data to create huge market value," Wang Yongli wrote.

Ant Group, the parent company of Alipay, indicated in its prospectus released on August 25 that the central bank digital currency may pose risks, but it is still difficult to assess the impact of this work on the company's business, financial condition, and operating results.

Who will the market choose?

Will digital RMB impact Alipay and WeChat Pay? The key still lies in the market's choice. We may see some clues from the digital RMB testing in Suzhou.

On the merchant side, during The Paper's visit to merchants participating in the Suzhou pilot digital RMB red envelope program, many merchants mentioned the advantage of no handling fees for current digital RMB exchanges. However, some merchants pointed out that the lack of interest on the current digital RMB wallet makes it difficult to retain users, and some suggested promoting it to upstream and downstream in the future.

However, regarding whether digital RMB will replace Alipay and WeChat, a deli store employee stated: "I think the possibility of replacing Alipay and WeChat is low; people use Alipay and WeChat more now."

An employee of an electronics store also believes that the future will see a parallel state of digital RMB wallets with WeChat and Alipay payments, stating, "It won't replace them; people will still use Alipay and WeChat, just like how people still use other banks even if the four major banks are strong."

Another mobile phone store manager also expressed that coexistence is the most likely outcome, and replacement (of Alipay and WeChat Pay) is unlikely, "unless the government orders the exclusive use of digital RMB wallets."

For the general public, The Paper conducted an online questionnaire.

Regarding the question "Will you use the digital RMB wallet to replace Alipay and WeChat Pay?", the results from 526 valid responses showed that 42.59% of respondents indicated they would use the digital RMB wallet alongside WeChat Pay and Alipay, 26.05% said it would depend on the situation, 24.33% chose to replace Alipay and WeChat Pay with the digital RMB wallet, and only 7.03% clearly stated they would not use the digital RMB wallet to replace Alipay and WeChat Pay.

Respondents' willingness to use the digital RMB wallet to replace Alipay and WeChat Pay in the future

Among them, older respondents showed a significantly higher willingness to use digital RMB than younger respondents, with 37.5% of those aged 55 and above choosing "use digital RMB to replace Alipay and WeChat Pay," while this proportion was only 7.3% among those under 25.

Commercial banks: Can shed cash management costs, will the "Matthew effect" intensify?

Besides the payment market, what impact will digital RMB have on traditional financial institutions?

Zeng Gang believes that the emergence of digital RMB will primarily improve efficiency and reduce banks' cash management costs, but it will not have any other impact on banks.

He stated that the logic behind the issuance of digital RMB is the same as the use of cash today, akin to withdrawing cash from a bank counter or ATM. If the bank lacks cash, it will seek funds from the central bank, transferring money from the central bank's cash reserves, while the reserves in the bank's account decrease. Previously, the transportation process was inefficient and had security issues, requiring many security personnel; in the future, it will be sent directly through the account system.

"Currently, banks' cash management costs are quite high. If cash is eliminated in the future, cash counters at bank branches and outlets will no longer be needed, leading to a rapid decrease in costs. Vaults will also be less necessary, and fewer ATMs will be required, eliminating the need for armed security personnel. Moreover, from a social management perspective, every cash transaction involving digital currency can be tracked by the central bank, which can help prevent cash from being used for illegal purposes, thereby enhancing social governance capabilities," he said.

Zeng Gang believes that the challenge lies in the decreasing need for cash management, which may require adjustments to services related to bank cash management, and a complete transformation of the functions of counter outlets, along with the institutions supporting cash management, such as cash counting machine production and armored vehicle transportation, which may no longer be necessary.

"Digital RMB actually presents more opportunities for commercial banks (designated operating institutions)," Hao Yi believes.

He stated, digital RMB provides commercial banks with another opportunity to attract consumers in the retail sector. Currently, the retail sector is dominated by WeChat and Alipay, with very few opportunities for banks' own apps to be used, only involving when using bank cards.

With the arrival of the digital RMB era, commercial banks can leverage their identity as digital RMB operating institutions to integrate their digital RMB wallets into the digital RMB ecosystem during the circulation process. This will allow people to notice various information (such as wealth management products and other services) provided by commercial banks in the wallets during the use of digital RMB.

"How to develop will depend on how each commercial bank promotes digital RMB after the pilot, and how they encourage the public to use their bank accounts to exchange into and out of digital RMB," Hao Yi said.

Hao Yi noted: "From the pilot situation in Shenzhen, by binding the four major state-owned bank cards for recharging, users can withdraw the amount back to their bank cards. This itself is also a means to attract consumers to continue using commercial bank credit cards. It helps to redirect traffic back to commercial banks, aiding them in continuing to develop new scenarios in the retail sector."

However, for other commercial banks, Hao Yi believes that there will be some impact on non-operating commercial banks.

"For example, to use digital RMB, people must open bank cards from the four major banks and accept their services. This gives customers of originally city commercial banks an opportunity to accept services from the four major banks, and these users may abandon city commercial banks in favor of the four major banks. Additionally, during the use of digital RMB, people will need to transfer deposits from city commercial banks to the accounts of the four major banks, but it is unlikely to transfer small amounts like 5 yuan at a time; they may transfer larger amounts, which could lead to a 'migration' of deposits from small and medium banks to large banks."

Risk warning

Risk warning Risk warning

Risk warning