Central Bank Working Paper: What Can Blockchain Do and What Can't It Do?

So far, no technological innovation has had a disruptive impact on the financial system, and blockchain will be no exception.

So far, no technological innovation has had a disruptive impact on the financial system, and blockchain will be no exception.This article was first published on the official website of the People's Bank of China on November 6, 2018, and was organized by Planet Daily.

On the afternoon of November 6, 2018, the People's Bank of China released a working paper titled “What Can Blockchain Do and What Can’t It Do?”, which mainly studies what blockchain can and cannot do from an economic perspective. This article provides a brief excerpt of its content.

I. Here is the conclusion from the end of the paper:

Overall, there are currently very few blockchain projects that have truly landed and generated social benefits. In addition to the low physical performance of blockchain, the shortcomings of its economic functions are also an important reason. A rational and objective assessment of what blockchain can and cannot do should be based on continuous research and experimentation.

First, do not exaggerate or blindly believe in the functions of blockchain. The industry practices over the years have proven that some blockchain application directions are not feasible. In particular, the modern financial system continuously absorbs various technological innovations during its development. As long as technological innovations help improve the efficiency of financial resource allocation and the security and convenience of financial transactions, they will be integrated into the financial system. So far, no technological innovation has had a disruptive impact on the financial system, and blockchain will be no exception. The supply of cryptocurrencies lacks flexibility, lacks intrinsic value support and sovereign credit guarantees, and cannot effectively fulfill the functions of money, making it impossible to disrupt or replace fiat currency. The anonymity of blockchain may actually increase the difficulty of implementing anti-money laundering (AML) and "know your customer" (KYC) in financial transactions. However, it should also be noted that some national conditions in our country provide opportunities for practical blockchain applications, such as digital bill trading platforms that help alleviate the fragmentation of our bill market.

Second, blockchain applications should be based on actual situations and should not be constrained by overly idealistic purposes. For example, it is very difficult to replace systems and trust with technology, and in many scenarios, it is even utopian. Furthermore, decentralization and centralization each have applicable scenarios, and there is no distinction between superiority and inferiority. In reality, complete decentralization and complete centralization are both rare. Many blockchain projects start from the purpose of decentralization but introduce centralized components to some extent later on; otherwise, they cannot be implemented. For example, writing external information into the blockchain often requires a trusted centralized institution, making complete decentralization impossible.

Third, there is a clear bubble in the current blockchain financing field, with speculation, market manipulation, and even illegal activities being common, especially in projects involving publicly issued trading tokens. Relevant government departments should strengthen regulation to prevent financial risks.

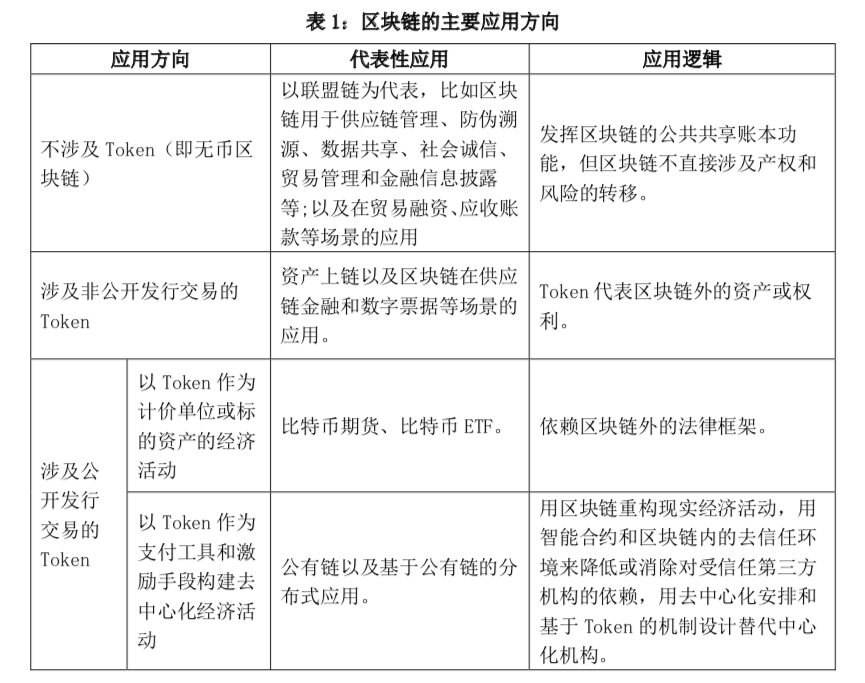

II. "Token" Paradigm and Four Main Application Directions of Blockchain

Before reaching this conclusion, the paper mainly analyzes the functions of blockchain from an economic perspective, summarizing the "Token paradigm" adopted by mainstream blockchain systems from three aspects: Token, smart contracts, and consensus algorithms, and provides economic explanations.

III. Other Points Worth Noting

In addition to analyzing these main application directions of blockchain, this paper further discusses the economic issues involved. There are several points worth noting regarding the economic issues involved:

1. Stablecoins

Currently, stable cryptocurrency schemes launched by companies such as Tether, Gemini, and Circle adopt a 1:1 issuance of stable cryptocurrencies backed by fiat currency, which is equivalent to a currency board system. Other stable cryptocurrency schemes adopt the so-called "algorithmic central bank" model, mimicking central bank open market operations by issuing and redeeming bonds denominated in cryptocurrencies to regulate the supply of cryptocurrencies and achieve price stability. Eichengreen (2018) pointed out that "algorithmic central banks" are difficult to defend against speculative attacks. When an attack occurs, bonds denominated in cryptocurrencies will have significant discounts, and the effectiveness of issuing such bonds to redeem cryptocurrencies to support their prices will significantly decrease, so "algorithmic central banks" have inherent instability.

It should be noted that central bank digital currency (CBDC) is fundamentally different from stable cryptocurrencies. Central bank digital currency has a liability attribute and is electronic money issued directly by central banks to financial institutions and the public, belonging to a form of fiat currency, and does not necessarily take the form of tokens within a blockchain. This paper does not delve into central bank digital currency; interested readers can refer to CPMI (2018).

2. Key Points of Cryptocurrency Regulation

The focus of cryptocurrency regulation is on the exchange between cryptocurrencies and fiat currencies, with one important issue being anti-money laundering. Cryptocurrency money laundering refers to the use of the anonymity and global nature of cryptocurrencies, making it difficult to trace the source and nature of illegal gains.

Cryptocurrency money laundering consists of three stages: 1. Placement, converting illegally obtained fiat currency into cryptocurrency. Some cryptocurrency exchanges do not implement real-name systems, which greatly facilitates the placement stage. 2. Layering, using mixers, coinjoin, and tumblers, along with the anonymity of blockchain addresses, to transfer cryptocurrencies between multiple addresses, making their source difficult to trace. 3. Integration, consolidating "cleaned" cryptocurrencies and transferring them to "clean" addresses, then converting them into fiat currency or goods. Cryptocurrencies represented by ZCash, Dash, and Monero use anonymity technologies such as zero-knowledge proofs and ring signatures, which increase the difficulty of anti-money laundering. In addition, the global circulation of cryptocurrencies, along with varying regulatory standards across different countries or regions and difficulties in information sharing, also increases the challenges of anti-money laundering.

3. Some Governance Shortcomings of Blockchain That Cannot Be Ignored (This section has been abbreviated; for the full version, please click the download link at the end of the article)

First, the impact of Token price volatility on the Token-based incentive mechanism.

Second, the functional shortcomings of smart contracts make it difficult to transplant some commonly used governance mechanisms in the real world into blockchain scenarios.

Third, the rapid liquidity mechanism of Tokens affects the binding of interests between the parties involved in blockchain project financing.

Fourth, the issue of combining on-chain governance and off-chain governance. On-chain governance is characterized by address anonymity, a trustless environment, and automatic execution of smart contracts, while off-chain governance is characterized by real identities, integrity records, trust and reputation formed through repeated games, informal social capital and social penalties, and formal legal protections. Whether these two types of governance can be effectively combined is a complex issue that requires further research.

4. The Economic Security Boundaries of Blockchain

Budish (2018) studied the security of public chains based on POW, represented by Bitcoin, from the perspective of being attacked, and proposed several economic incentives to enhance security. The author believes that the higher the economic importance of such blockchains (for example, imagining Bitcoin's market value approaching that of gold), the higher the likelihood of malicious attacks on them, thus maintaining a skeptical and cautious attitude towards the large-scale application of public chains, as enterprises and governments have cheaper technologies for data security than public chains.